Economy moves in cycles, Ray Dalio explains this beautifully in this 30 minute video. Dalio explains cycle using three factors:

- Productivity growth: This matters over the long term where more productive elements of the economy go ahead of their peers over a long period of time. Productivity growth doesn’t vary a lot over time, hence not causing swift economic swings over short term.

- Short and long term debt debt cycle: The amount of credit (or borrowing) in the economy is much larger than the amount of money in the economy, which causes huge economic swings. The short term debt cycle generally takes place over 5-8 years and is largely controlled by changes in interest rates made by the central bank. When the short term debt cycles keep on going for a long period of time (over decades), the overall debt in the economy increases to such an extent that a large part of income is made to simply service the interest payment, implying lower spending in the economy. The long term credit cycle generally takes place over 75-100 years. At the end of a long term credit cycle, there is cut in spending, reduction in debt (through defaults or restructing), wealth redistribution (via higher taxes from rich or inflation) and printing of money (leading to inflation in asset prices).

This picture from the above video summarizes everything very well (straight line is productivity growth)

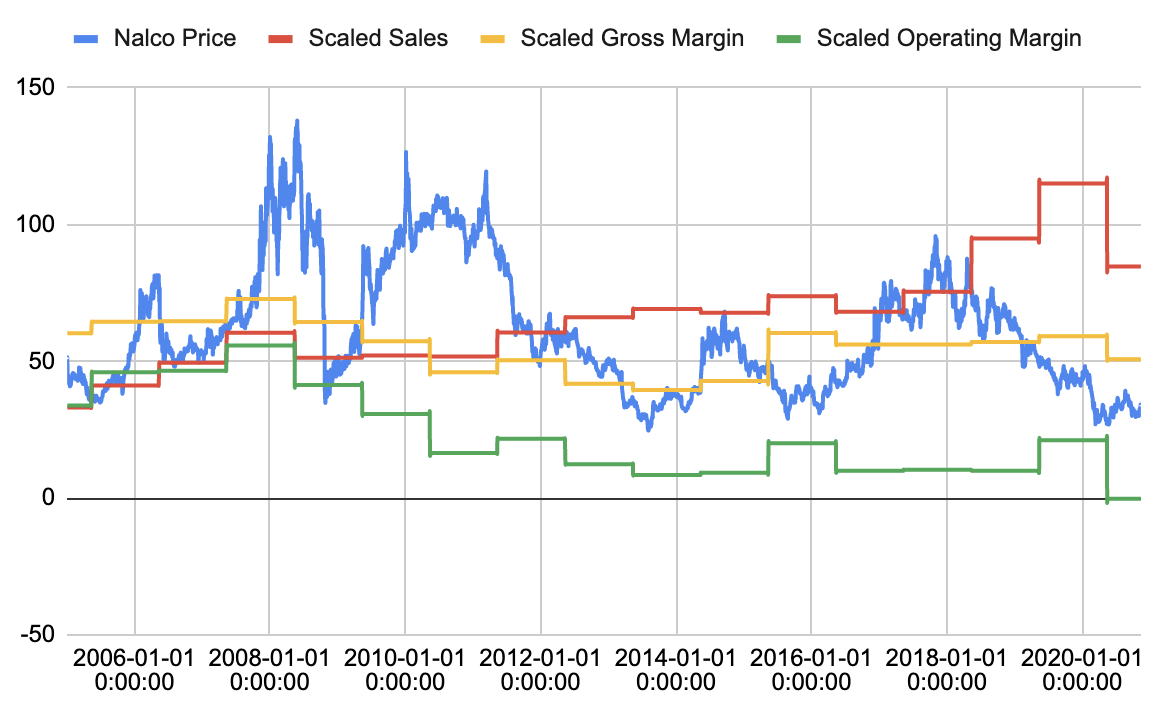

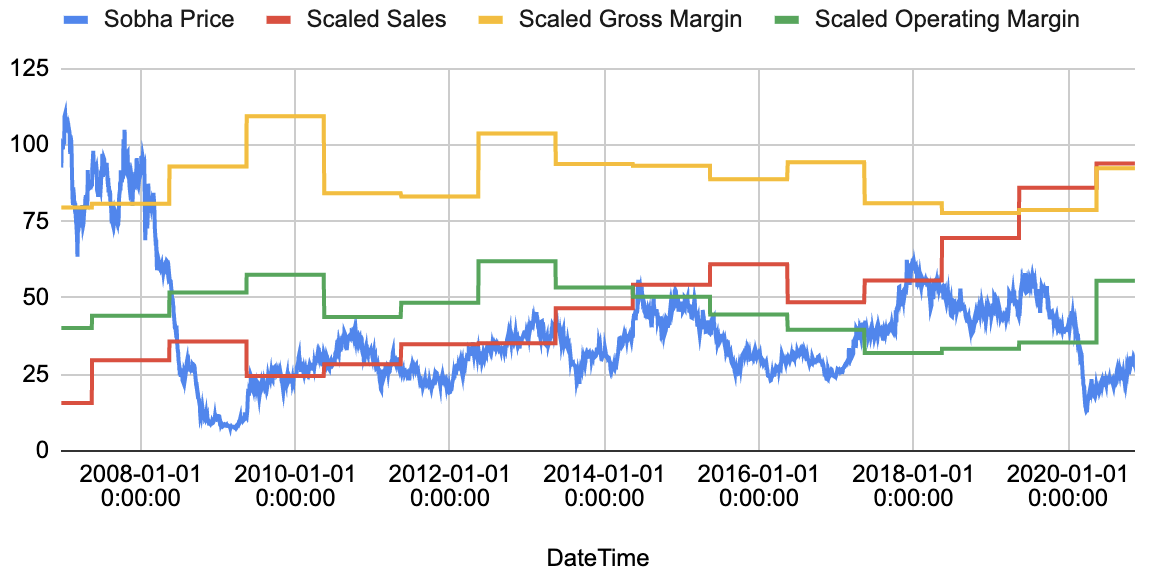

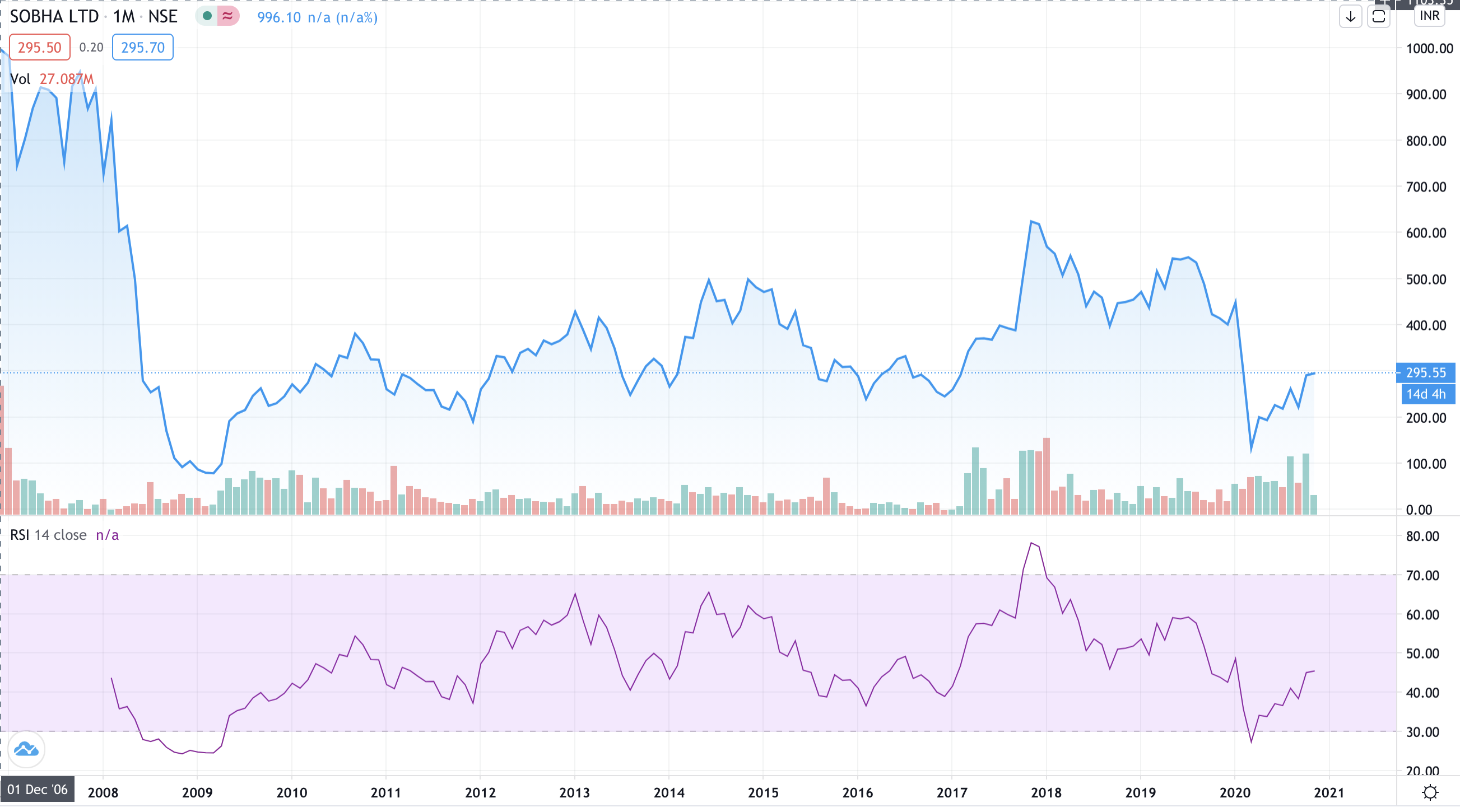

Credit influences infrastructure and real estate sectors disproportionately as both these are largely funded on credit. I will illustrate this with the Indian real-estate sector.

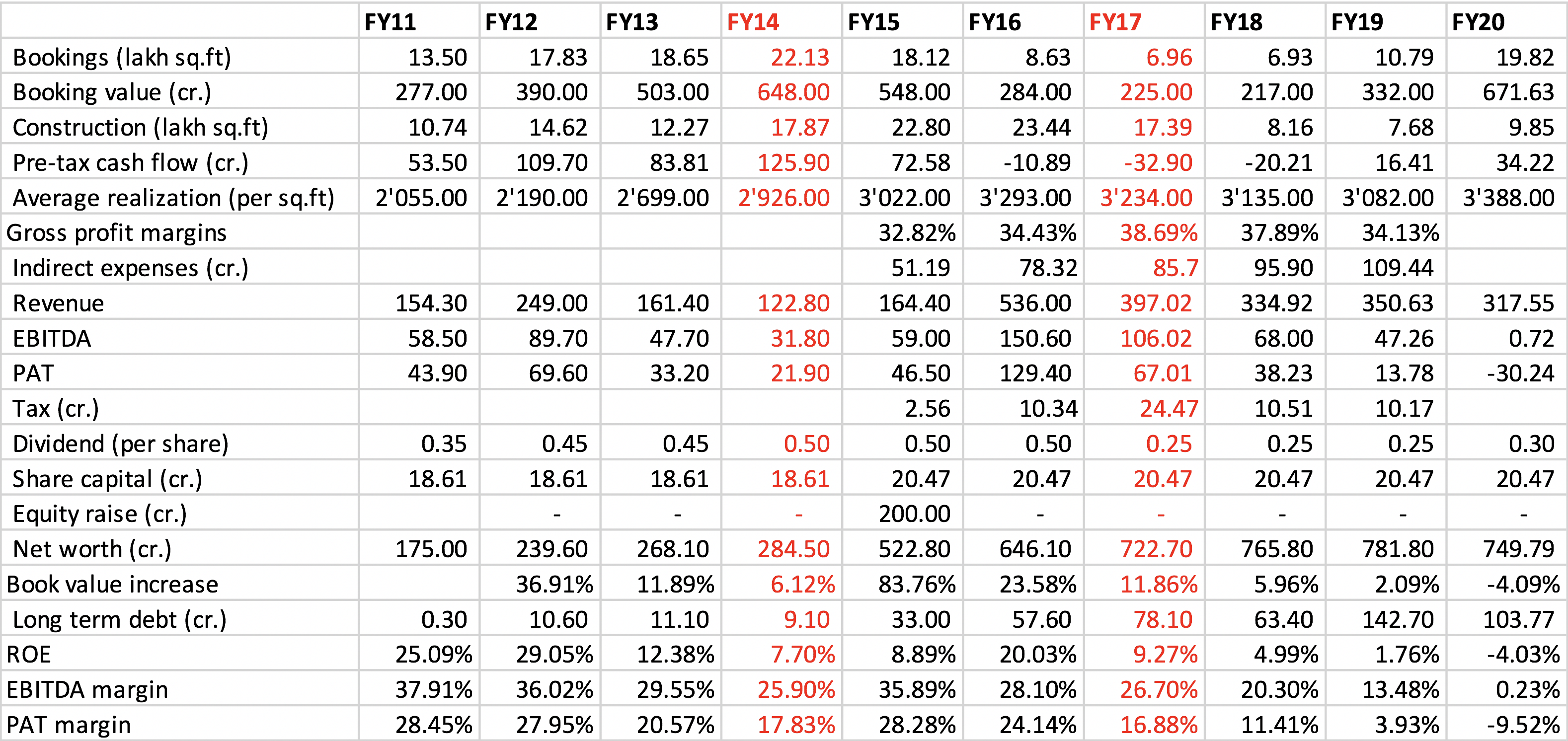

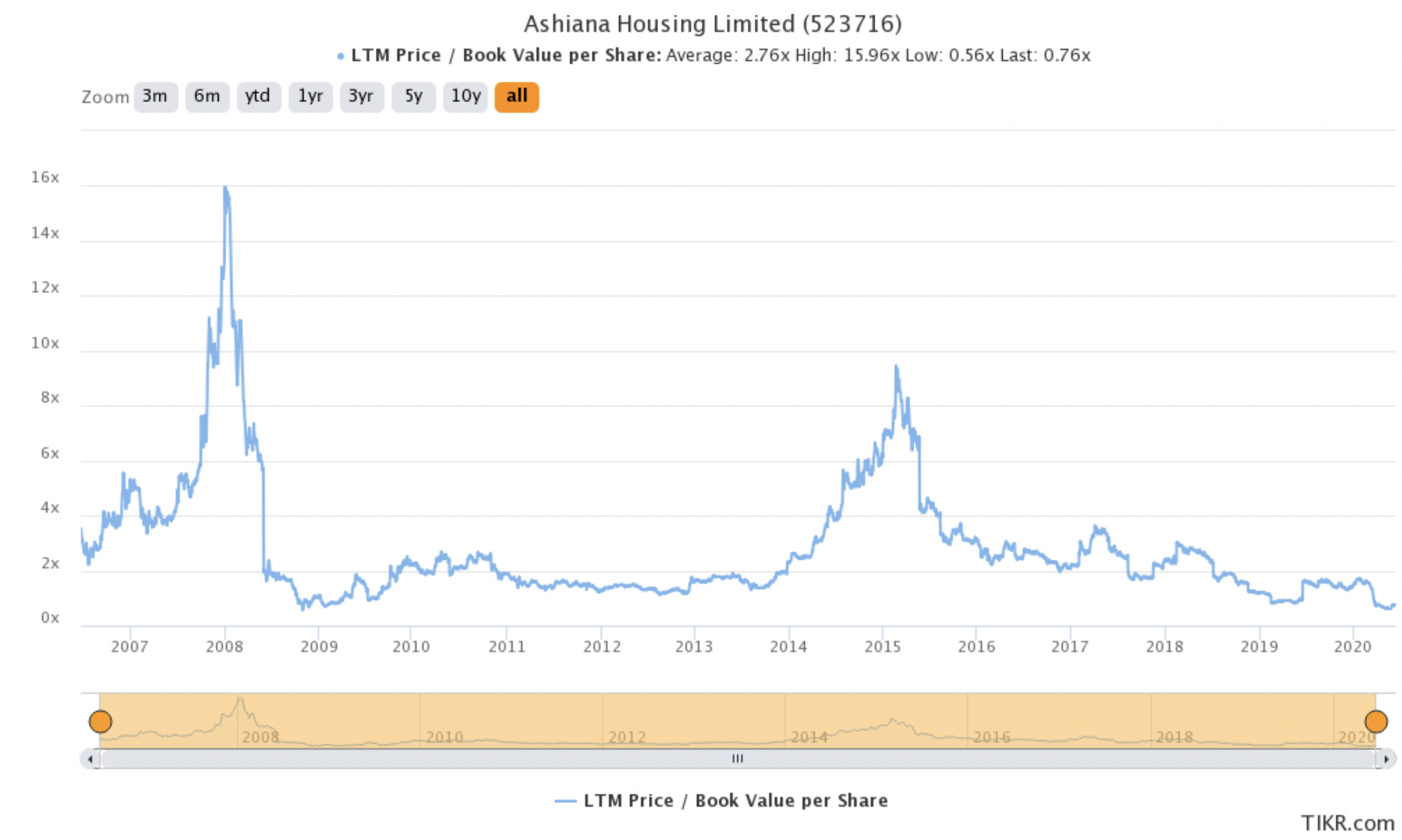

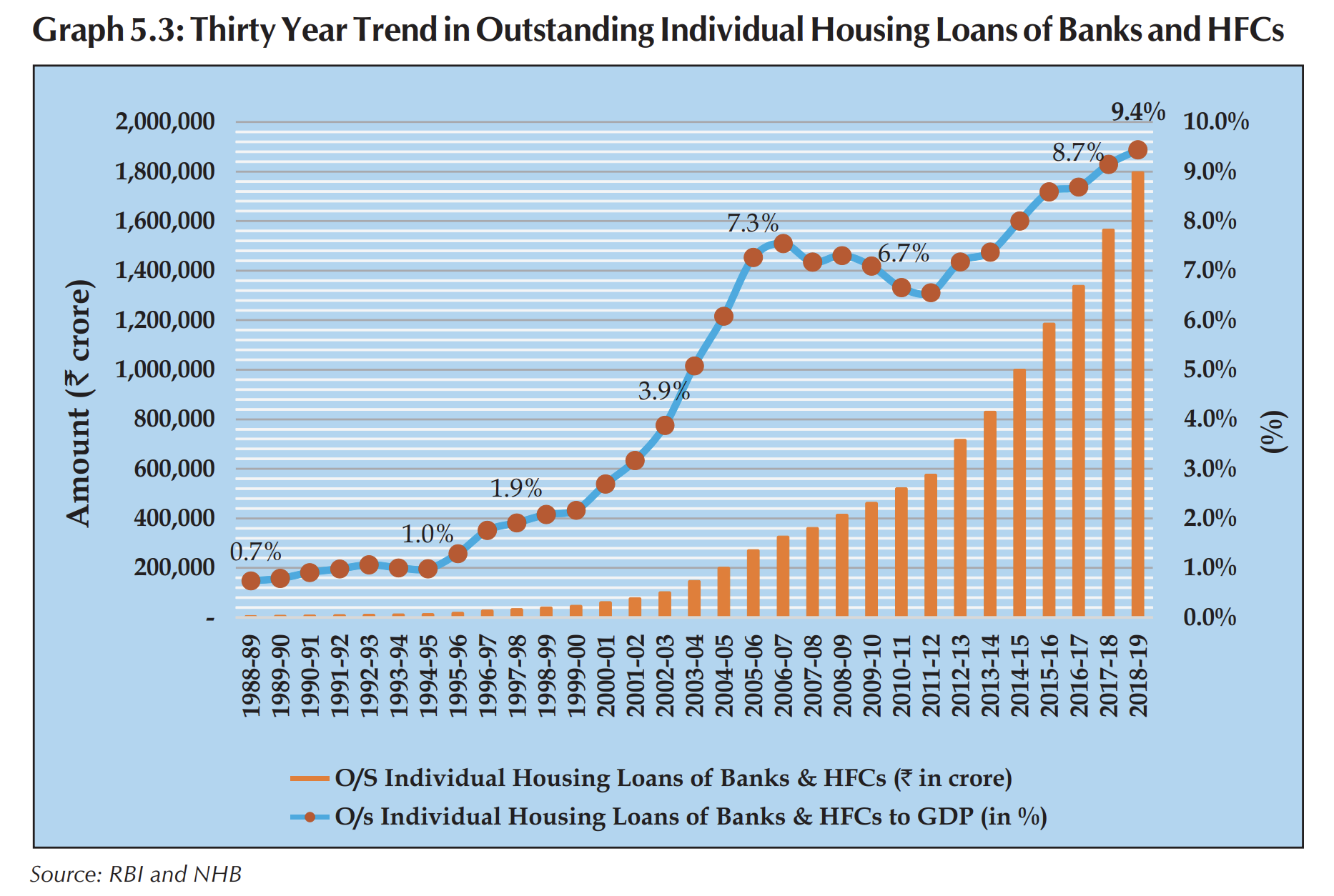

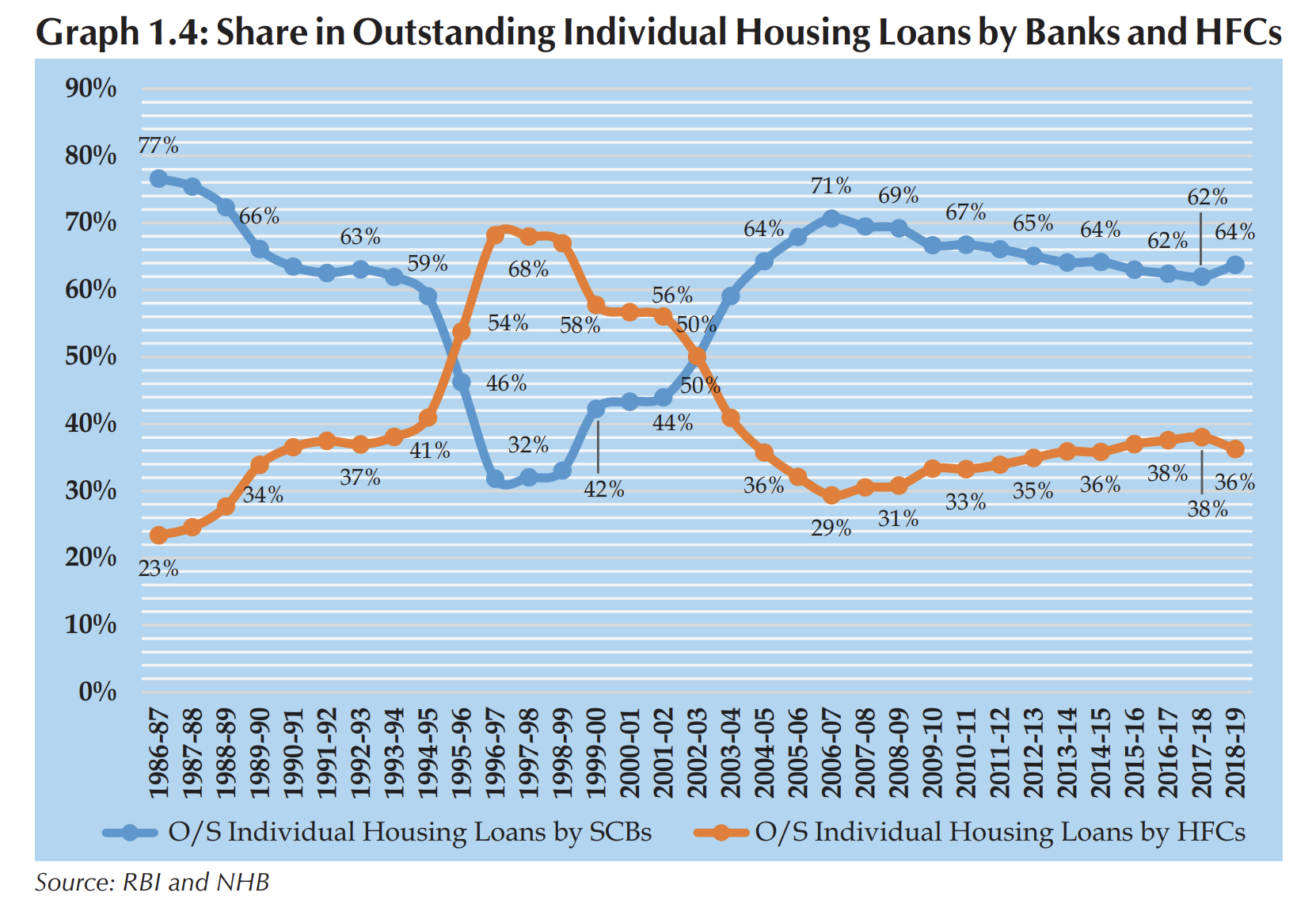

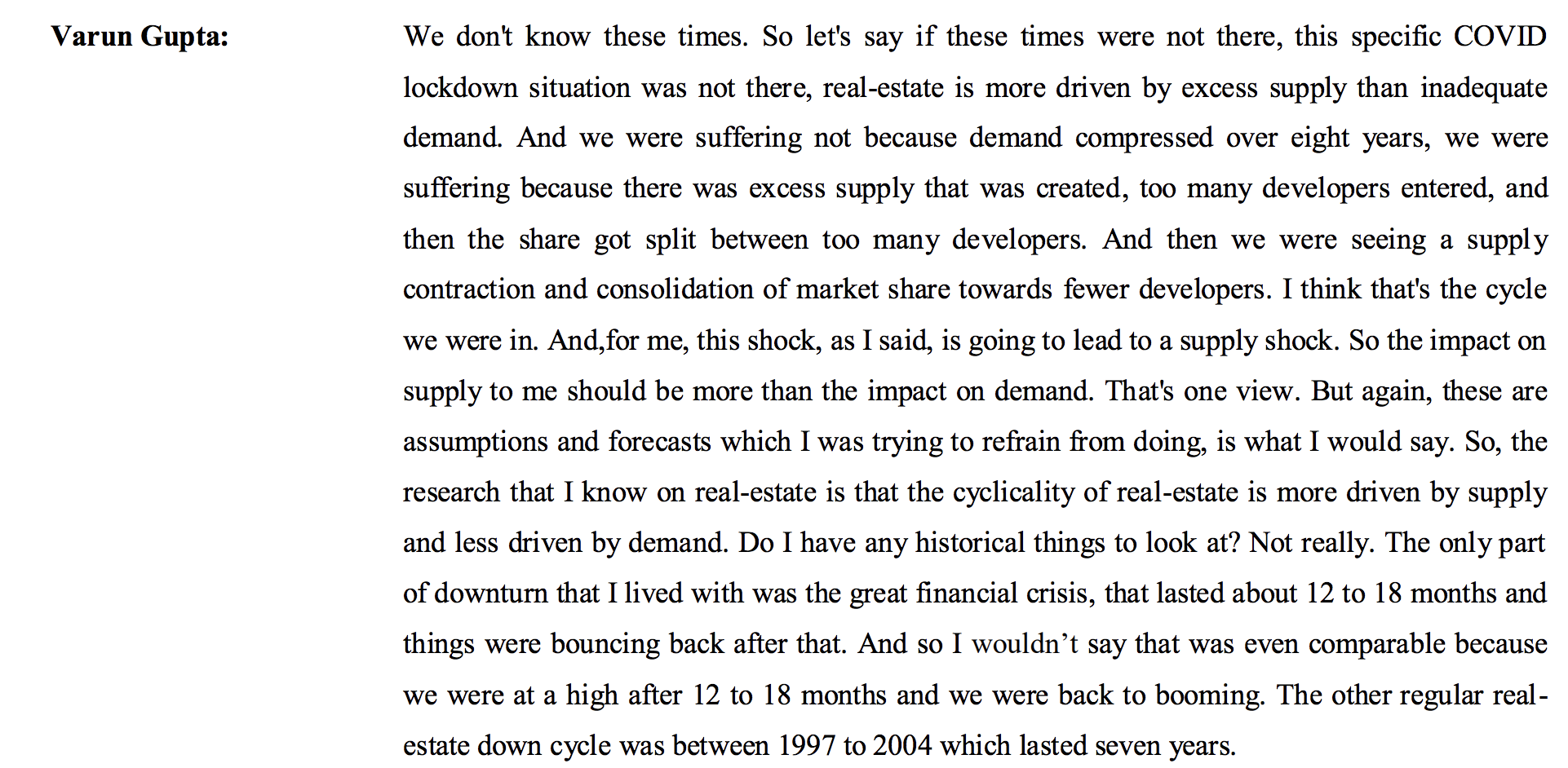

The Indian real-estate sector went through a major boom in the early 1990s on back of large credit growth, with oustanding housing loans rising from 0.7% in 1989 to 2% in 1998 of total outstanding loans (see fig1, link). This was because Housing Finance Companies (HFCs) grew at a breakneck speed, with their market share rising from 28% in 1989 to 68% in 1998 (see fig2). This boom turned into a major bust, with very low housing sector growth until 2003, on back of HFCs losing market share. Its interesting to see that housing credit growth started around 2000, but the real-estate companies only saw growth coming back in 2004 (on basis of concall from Ashiana housing shown in fig3). The rapid credit growth in early 2000s led to housing loan market share rising from 2% in 2000 to 7.3% in 2008. This time around, it was the banks which gave out loans with their market share increasing from 35% in 2000 to 71% in 2008. Again, housing loan as a percentage of total outstanding loans went down to 6.7% in 2013 after which we saw another real-estate collapse. However, since then housing loan as a % of outstanding loans have gone up to 9.4% in FY19.

Fig1. Housing loans as a fraction of total outstanding loans given by banks and HFCs (link)

Fig2. Housing loan market share between HFCs and banks (link)

Fig3. Conference call of Ashiana Housing (link)

Now, that we know that real-estate goes in cycles, what next?

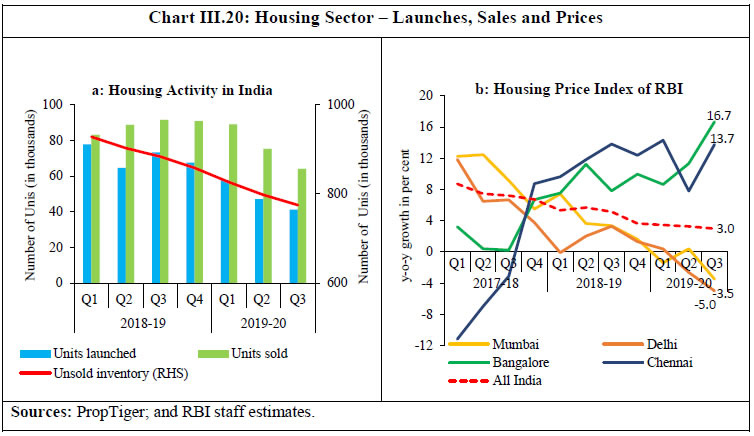

Its clear that we are nowhere close to the real-estate peak, my personal viewpoint is that the bust peaked in 2017-18 and the sector is already recovering. As real-estate is a hugely local market, it really depends on the micromarket where the company operates. Its a simple demand and suppy game. At times of boom, supply grows higher than demand which is reversed in times of bust. Different micromarkets behave differently. If we look at all-India level, the number of units sold in the last couple of years has been way higher than number of new launches (see fig4).

Fig4. Housing sector launches, sales and prices trends in FY19 and FY20 (link to RBI report)

How does COVID impact real estate?

Level 1 thinking says that demand will be impacted because of COVID’s impact on personal finances (bad for real estate companies). Level 2 thinking will say that supply will be more adversely impacted because a lot of developers who were already facing challenges might find it even more challenging to fund their projects. If supply goes down more than demand, prices increase (good for real-estate companies who can survive the current downtrend).

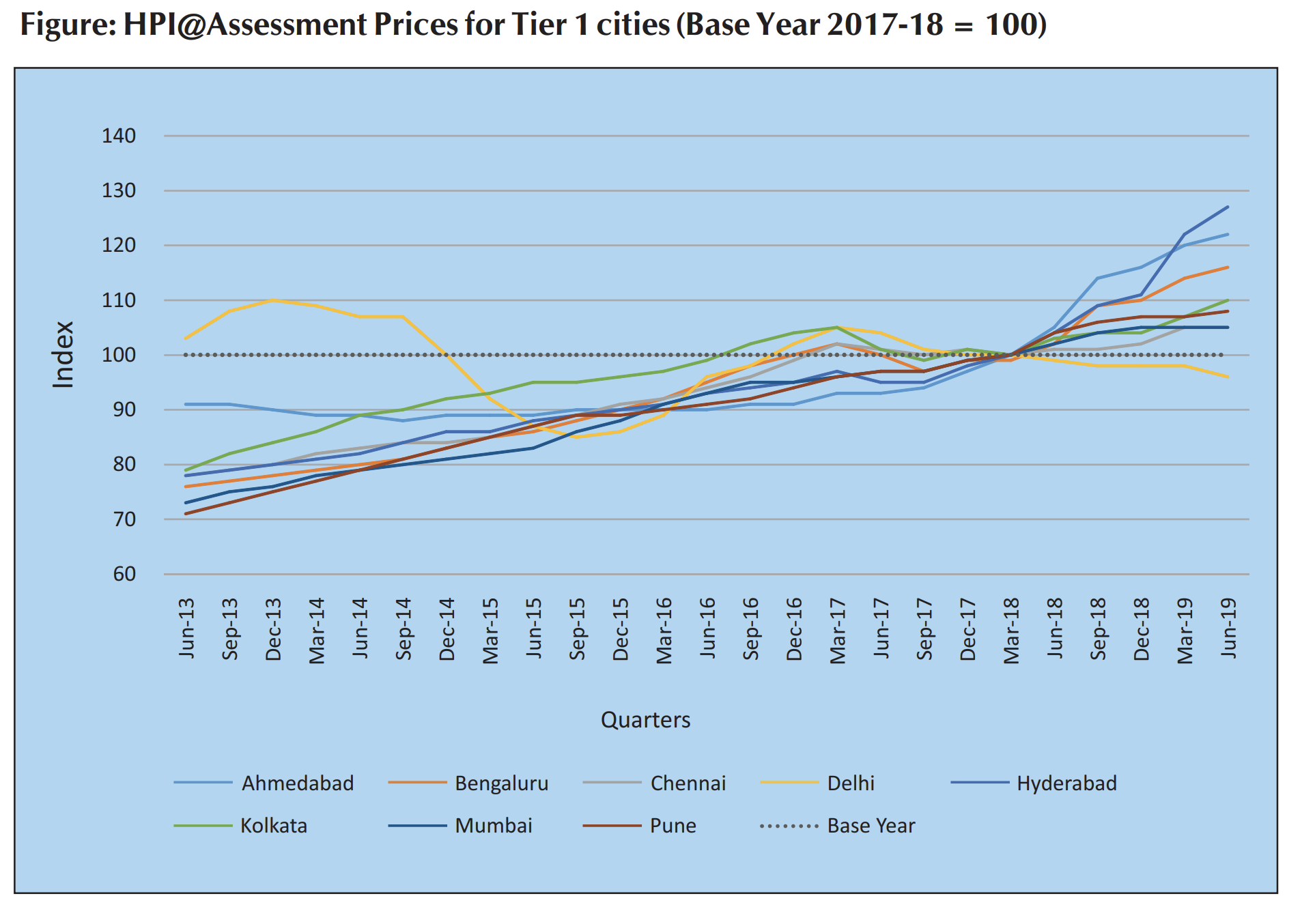

Micromarkets also make a huge impact on the fortunes of a company. This is clearly visible from the property price chart (called NHB RESIDEX) in Fig5. Except for Delhi, prices have been going up in different residential markets.

Fig5. Housing price charts normalized to 2017-18 fiscal year (link)

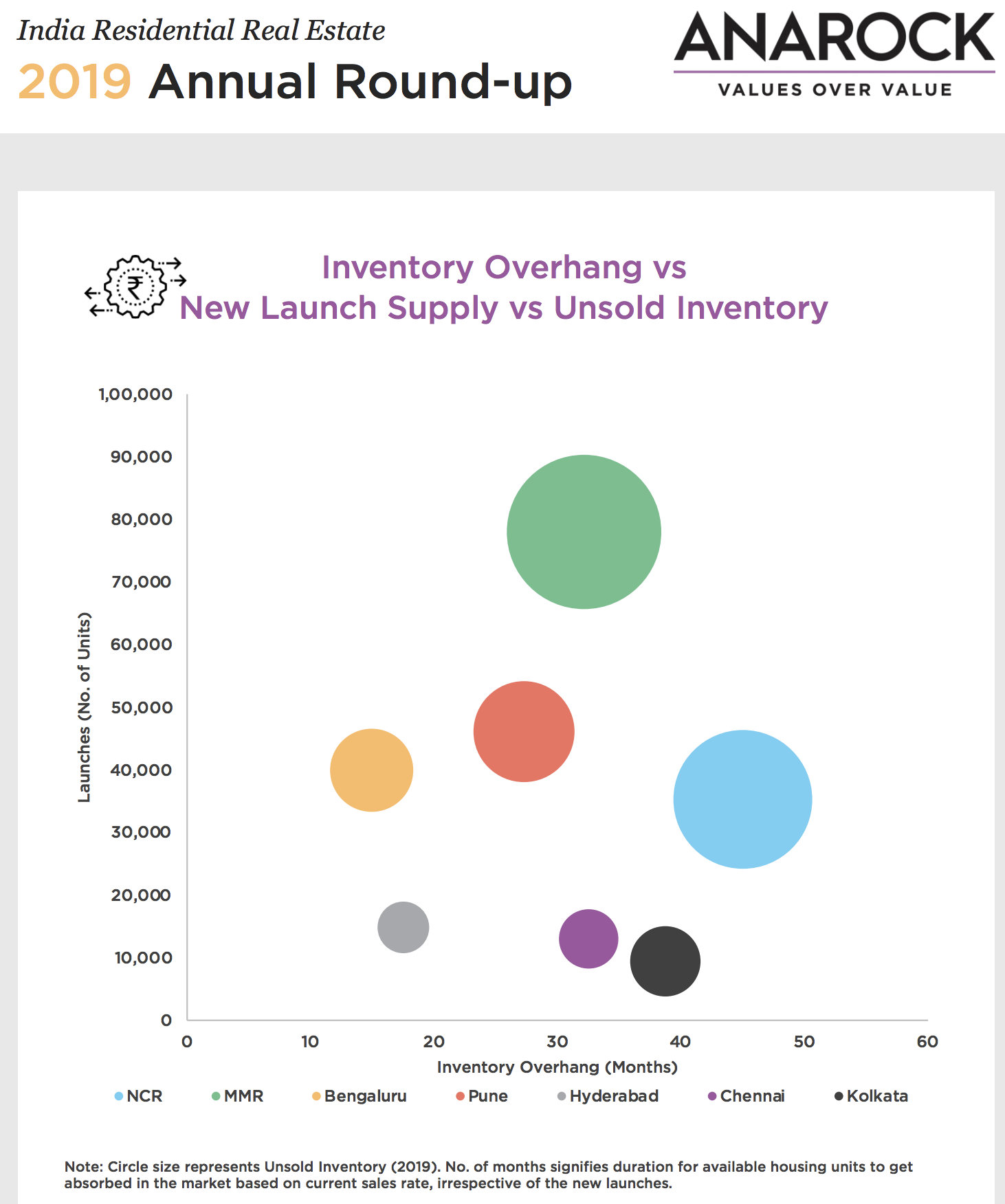

Another way to look at it is in terms of inventory duration i.e. how long will it take to liquidate inventory in a given region. The Anarock 2019 report clearly identifies Hyderabad and Bengaluru as two micromarkets with low inventory and reasonable number of launches (see Fig6). NCR region is a huge problem with >4 years of inventory and still large number of launches. This report from Knight frank also identifies Hyderabad, Pune and Bengaluru as low inventory markets.

Fig6. Anarock report extracts (link)

In the next post, I will write about how we can play the real estate cycle giving example of a few companies that are trading at throw-away valuations.