I think it has more to do with growth in their consumer business which is very low gross margin as trading silver bullion margins are only 8-10%. I think with growth coming back in their core switchgear division, margins can improve.

In this sector, I follow Kovai Medical and really like how they have scaled up over years. I track other companies but am uncomfortable in buying them as most hospital chains make subpar ROCE. Kovai makes one of the highest ROCE is this sector, have diluted only once in 1990s (that too through a right issue) and have very long term focus (shown in their investment in medical college which should lead to lower employee cost over time, but costs a lot to build). For me, Kovai becomes a buy at around 2x book value. Sorry that I don’t have anything meaningful to add about AsterDM.

This pattern of mean reversion in large caps is very common. Every few years, market falls out of love with certain large cap cos and people come up with all kinds of narratives to justify stock price movement. Many a times, business is only slightly impacted (or sometimes completely unimpacted like in the case of ITC/HDFC/HDFC Bank). This pattern was earlier used by value folks like Tweedy Browne who have been successful in implementing this over last 6-decades! You can read more about this strategy below.

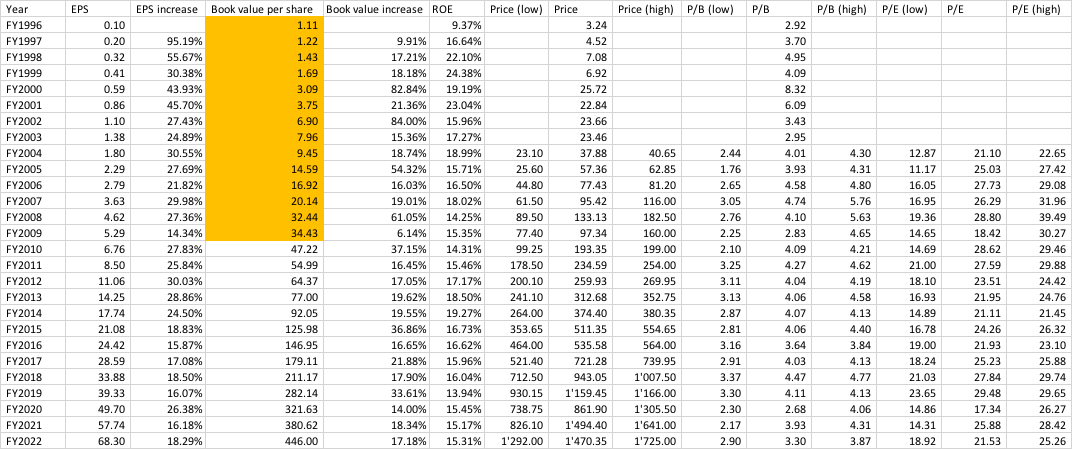

Coming back to HDFC bank, here are the longer term numbers. The lowest it has traded in last 20 years is around 1.76x P/B. On the higher side, it has traded upto 6x P/B. Generally, HDFC bank is a good buy below 3x P/B and a good sell above 4.5x P/B. I largely trade in this valuation band. Currently, HDFC is a better risk reward vs HDFC bank.

I am attaching my projections for both HDFC & HDFC bank.

HDFC bank projection on 02.05.2021

FY21 book value: 210’443 cr. (382/share), share count ~ 551.23 cr. In FY25 book value will grow @18% to ~ 408’000 cr. Long term share dilution ~ 2% i.e. 597 cr., Book value per share: 683 (including dilution). I would like to sell at >4P/B (share price: 2732).

HDFC projection on 07.05.2021

FY21 book value is 165’617 cr. which should grow to ~378’892 cr. (@18% growth) in FY25. Long term share dilution ~ 2% i.e. # shares ~ 195 cr. (from current ~ 180.4 cr.). Book value: 1943 share price. I would like to sell at > 3.1 P/B (share price: 6023). Start selling at >6000

Hope this is useful and clarifies my thought process ![]()