CMP 380

Market cap 3800 cr

Debt 2000 cr

Enterprise value 5800 cr

Sobha Developers (Sobha) was incorporated in 1995 and is a leading real estate player in Southern India (total saleable area of 243msf) with a strong presence in Bangalore, Pune, Chennai, Kochi, Gurgaon etc. The company has a uniquely backward integrated business model through presence in contractual and manufacturing segment.

For this post I am not considering the value of the contractual business and only focusing on the real estate.

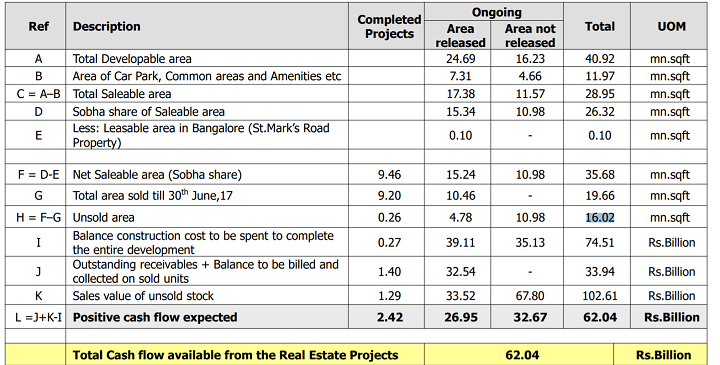

Sobha has 24 mn.sqft of ongoing projects from which it expects 6200 crores of net cash flow. The value of unsold inventory is 10000 cr and pending dues to be collected are 3300 cr. Pending construction cost is 7400 cr hence net cash flow of 6200. Assuming this inflow will be spread over 5 years its discounted value to todays date is 4000 cr.

Now coming to the land bank. Sobha has 2300 acres of land bank spread across the southern region out of which 700 acres is in banglore. The total developable are of the banglore land is 75 mn sq.ft. Hence if we value the Banglore land at the lowest range of the MTM value (300 rs / sq ft) it is worth 2250 cr. And the rest of the land (1600 acres) can be valued at 1 cr per acre which the management has said is the cost of acquisition. Hence the total land bank is worth 3850 cr. We have assumed that there has been no appreciation in the value of the other land (1600 acres) which may not be correct since a lot of the land has been acquired a while age and definitely there mustve been some appreciation.

So the total business is worth 4000 cr (ongoing projects) + 4000 cr ( land bank) = 8000 cr

The contractual business of the company is valued at 500 cr by all of the research firms hence the total enterprise value by these calculations is 8500 cr

Subtracting net debt of 2000 cr we get an equity value of 6500 cr. And the market cap is 3800 cr

And bear in my mind we have taken a very conservative valuation of the land bank which may be worth much more actually

I request all of you to share your view. The promoter has recently sold 4 % stake BUT I dont think it is worrisome because 38% of the company is owned by large instituitions ( Franklin Templeton, Morgan stanley etc) with Franklin buying 14 lac shares very recently.

In my opinion -when valuing developers from a quantitative point of view one must keep a few things in mind.

Are the operating margins more than the cost of land in relation to revenue ? e.g if operating margins are 20% and land forms 40% of the average realization per sqft then its not a happy situation for developers

What is the sellout ratio? From the total units launched what is the % sold? This indicates demand for the project , a sellout ratio that is less than 65 to 70% is bad news & indicates pricing pressure. These sellout ratios must be achieved within the 1.5 yrs of launching else you can expect all kinds of construction delays.

What is the average realization per sqft? is it increasing or decreasing? A good brand has a realization that increases by at least 10% every year.

What is the slab cycle and what is the sales cycle in days. Ideally you should be selling faster than you construct - if these things are not present its a problem.

What is the cost of capital? In my experience the average cost of capital in real estate is 15% to 18% for an average developer. Good developers have a cost below 12 to 14% and great ones are below 11-12. Quite clearly cost of capital has to be more than the return at a project specific level. That is why many developers are transitioning to the JV model to reduce cost of capital employed. Unsold inventory (including land lying idle) increases the cost of capital and is detrimental to valuation. Units being built without being sold increase inventory and do more harm than good.

Accounting standards followed.

The encumbrance of the land shown on balance sheets. Developers book land on their balance sheets but no one knows whether its unencumbered or not. The cost of liasoning is an important parameter here which indicates what developers are spending to get land marketable.

These are a few factors that make it very difficult to evaluate developers only from the financial numbers and financial numbers are almost always unreliable when it comes to real estate.

I appreciate your efforts in starting this post but there are vital things missing

Risk factors involved in your thesis

Disclosures of your holdings

Quality of promoters - vital in real estate. Sobha is the name of Mr Menons spouse incidentally.

Just my 2 cents regarding Bangalore - Sobha is a pretty reputed builder here in Bangalore and commands a premium price but overall real estate situation is not so good because of recent strict laws regarding construction near lake beds, IT sector slowdown, lot of unsold inventory in the system, high prices on paper but no liquidity for resale apartments, change in IT laws thereby buying second homes is no longer lucrative, RERA rollout, bad traffic situation and general worsening of the IT part of the city.

Update Shobha QuarterlyOperationalUpdateSep2017.pdf (843.0 KB)

Real estate division of Sobha, Q2fy18 Sales up qoq 5.3 and 14.4% yoy. There is a marginal impact in price realization per sft which is ₹6883 vs ₹6903

Sobha Q2 net profit up yoy 30% at Rs 50.2 cr.

Good quarter and company seems to be sustaining the sales, tailwinds like input costs gst reduction might help Profit growth.

Another point i would like to add is that taking debt is an integral part of real estate. Some developers take on more debt than what they can handle and some less. However, debt is a business reality not just in india but globally as well. Hence, if you find a developer with little or no debt on books - you should be wary because it is an abnormal situation. There are some listed developers with a debt free balance sheet and i would avoid them because the industry structure doesnt allow debt free balance sheets.

The stock has run up a lot in the past couple of months. What is your rationale for adding more at cmp? Because on a pe multiple basis the stock is now not much cheaper to it’s peers.

My rough analysis is ,Sales momentum is sustainable and per qtr sales would be > Rs 700 cr, at OPM 20%, net profit would be > 70cr. Total 12 month forward PAT = 280cr. So Mcap at that time would be 30*280 = Rs 8400cr(based on PE multiple of 30 ). Current market cap = Rs 6140cr.

I haven’t got time to analyse new launches.

Please correct me if you are contradicting majority of my views.

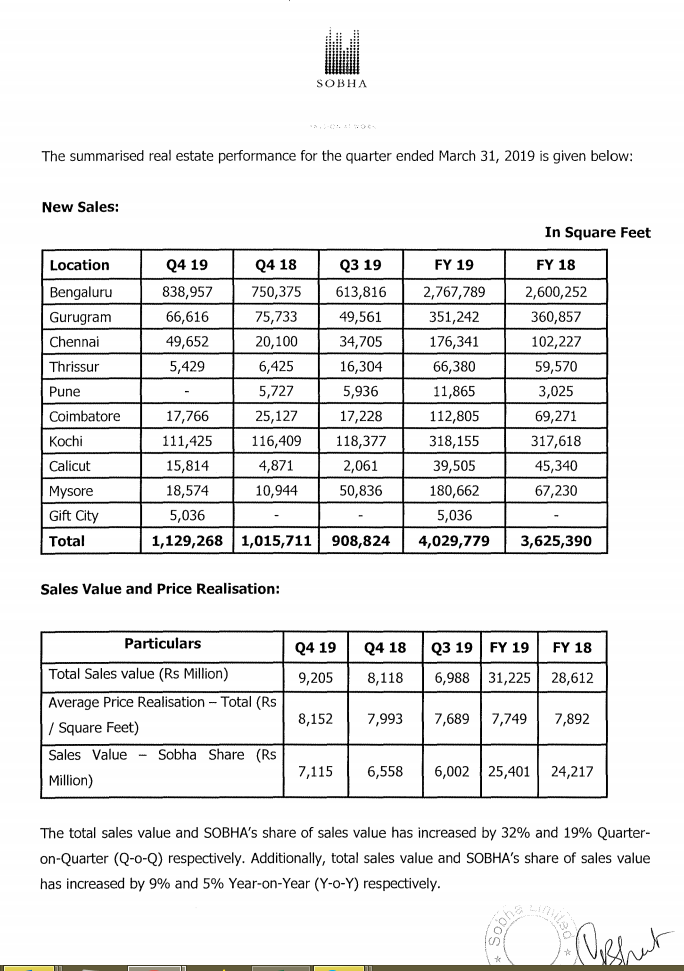

For the fourth quarter, the Company has achieved new sales volume of 1.02 million square feet, total valued

at ~ 8.12 Billion at an average price realisation of~ 7,993 per square feet (Sobha Share of sales value at ~

6.56 Billion, at an average price realization of~ 6,457 per square feet). Sales volume and values are up by

40% and 31% respectively as compared to corresponding quarter of last year and are up by 9% and 7.5%

as compared to preceding quarter.

This is good deal … they are investing 115 cr in getting development right ( that too in 4 year period they have to pay ) and they are getting 1.3 million and project would be under PMAY so no tax for company … Demand is not good in Ahmadabad but since its affordable and brand is great and if company price it right ( they can as they have tax breaks also) . It looks like good roce deal to me…Margins are not expanding as we are in lower end of real estate cycle and hopefully trend changes in forward years and when revenue reorganization of new projects comes.

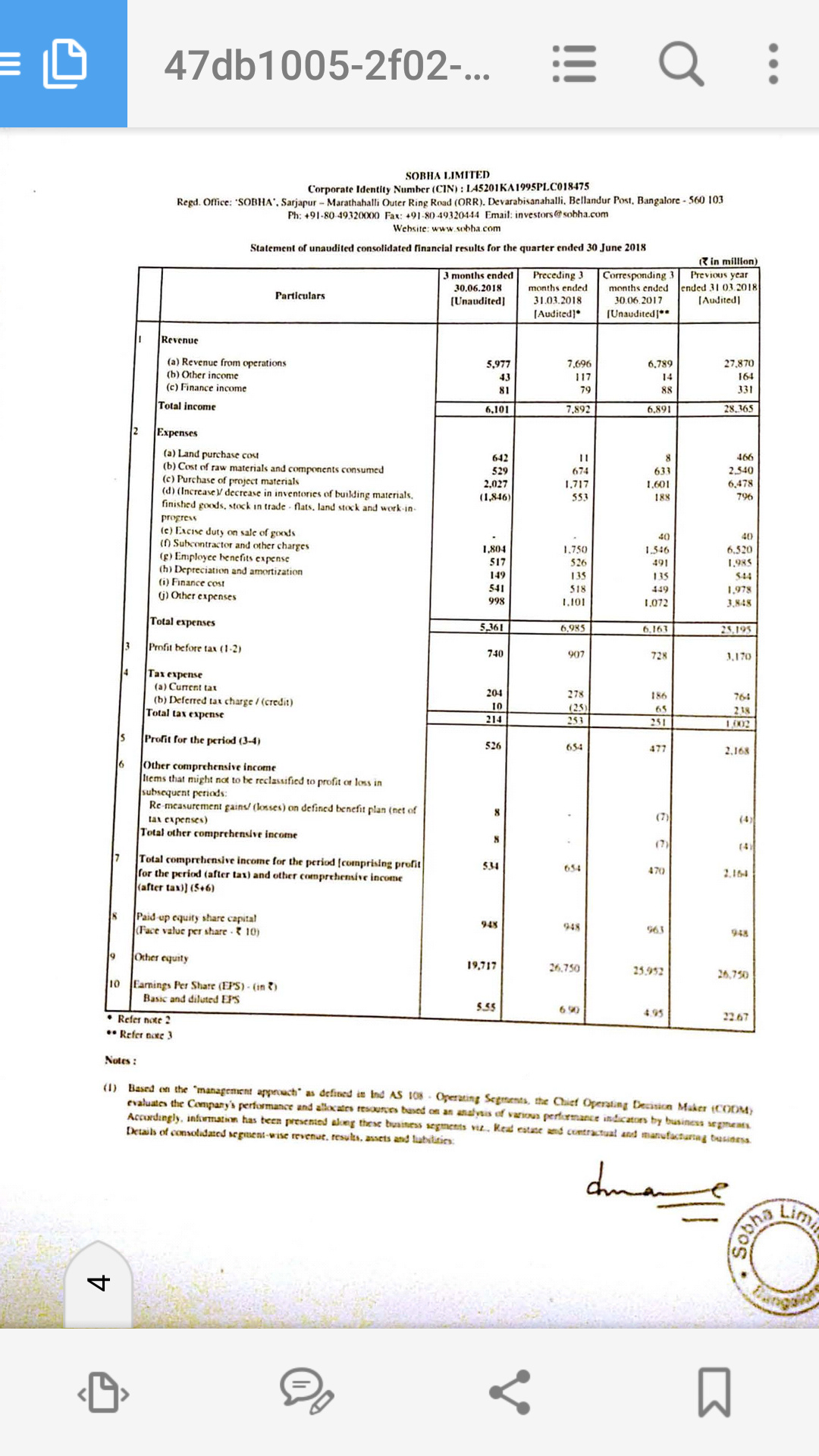

Mixed result, pat up 10.1% yoy and OPM up yoy, sales down yoy, margin improvement is good sign if that will end up into more pricing power due to rera ?

The down sales snd increased debt equity is more impact of real estate accounting changes implemented. Attached investor PPT gives old vs new accounting comparison. If numbers could be trusted,then,seems a reasonable quarter with double digit volume n value growth in bookings

Yes, Saurabh is correct. The company has decided to book revenue on the receival of OC. Ideally the profit would’ve been 70 cr with sales of ~800 cr for the quarter. So solid result overall.

Quite decent result from Sobha in the back of real estate slowdown overall. Posted highest ever quarterly revenue and share from real estate segment vs. contractual has seen uptick.

Robust operating level cashflow gives comfort in terms of their maturing market debt repayment as well as raising fresh funds as rollover.

As such contract manufacturing is picking up quite well.

Broadly the debt levels is same, with cost of borrowing ~9.6% (though ~30 bps uptick vs. last quarter) which is one of the lowest in the industry.

2 new projects launched in Bangalore and 1 in Kochi this quarter, is quite a good sign.

Broadly Bangalore still contributes to ~68% of revenue, but seeing good realization of ~7000 per sq ft. Demand for “< Rs 50 Lakhs” & “Rs 1cr to 2cr” has been increased and other product categories are stable.

Interesting to see that ~35% buyers are self funded, which likely signifies upgrade rather than new buy. Interestingly, Bangalore market has max % of buyer aged 30-40 while other market its more from 40-60 (implies faster growth in networth/confidence to buy from current salary income).

As such good visibility of pipeline of 40+ ongoing projects to be completed in next 3-4 years. Good part is many of these are located very near to existing/upcoming metro stations.