Aegis reported another good set of nos with 31% growth in earnings. Kandla terminalling operations have started and management is guiding 4mn+ terminalling volumes in FY24. In addition, they have added a large number of industrial customers in retailing business. Concall notes below.

FY23Q3 concall

- Future growth drivers: Ramp up of gas volume in Kandla, increase in gas volumes in Pipavav and Haldia due to jetty commissioning, ramp up in industrial distribution volumes from Kandla, ramp up in liquid volumes

- Growth headwinds: Lower LPG distribution to industrial customers if LNG prices correct a lot

- Pipavav: LPG jetty work for handling VLGC got completed and is awaiting approval for commercialization

- Kandla: Commenced LPG handling

- Haldia: Additional Jetty commissioned increasing unloading rates, operations have now normalized

- Mumbai: Operating LPG at full capacity

- Autogas division: Quarterly volumes was 5’100 MTPA (flat QoQ)

- Commercial & industrial volumes were 151’400 MT in this quarter (vs 191’300 MT in H1FY23), huge ramp up has happened here.

- Distribution margins will be maintained at Rs. 3000/MT

- Total sourcing tender volume contracts for CY22 was 800’000 MTPA. They did volumes of 658’000 MT vs 286’000 MT last year

- Additional liquid capacity of 50’000 MT will be commissioned by end of FY23

- LPG comes from refineries or from natural gas fields. Management believes no new refinery capacities will come onstream. Some of the existing refineries (e.g. Bhatinda refinery) will be switching out of LPG to higher value products which might imply that domestic LPG supply will not increase over the next decade

- In gas logistics division, 1mn quarterly run rate should be sustainable (did 988’000 MT this quarter). Confident of doing 4mn run rate in FY24 in logistics

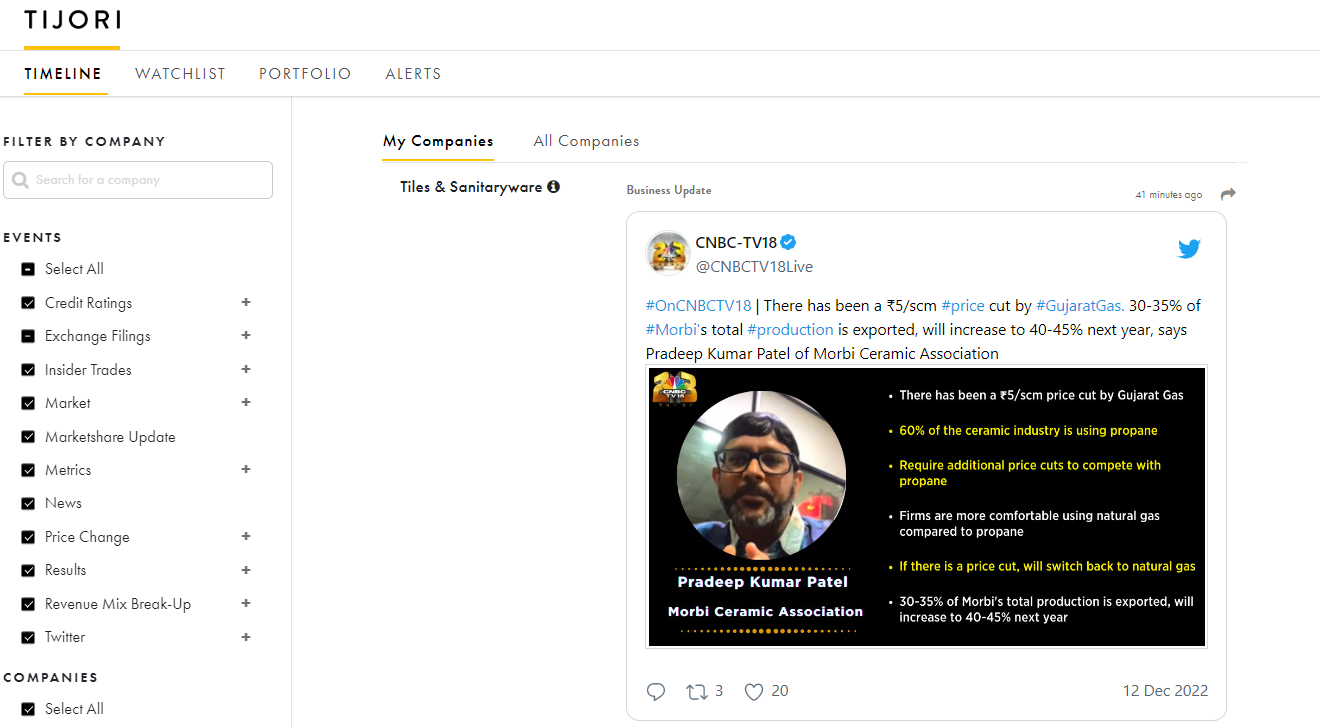

- In Morbi, 70-80% conversions have happened from LNG to LPG

- Keshav Shenoy was made President - Strategic Planning

- Large addition in industrial customers with a lot of new names (highlighted customers not mentioned in previous presentation)

Disclosure: Invested (position size here, sold shares in last-30 days)

Hi @harsh.beria93: with the recent price cut by Saudi Aramco; Morbi is going to be using LPG for more time it seems like… What made you book profits in this counter? the results also seemed decent, was the market expecting more? what am I missing?

Aegis reported another good set of nos with 56% growth in earnings. Real earnings are a bit lower as they had a large other income component in this quarter (something related to valuation of JV). More importantly, they have maintained their bulk industrial retail volumes at 1.3 lakh MT. Another really interesting move was their forey into JNPT, this is a significant move as JNPT handles higher volumes compared to Trombay. The other large liquid player at JNPT is Ganesh Benzoplast and they were planning to start a LPG storage unit there. Will be interesting to see how dynamics between Aegis and Ganesh plays out. Concall notes below

FY23Q4 concall

- Pipavav: allocated 1.25mn MT in KGPL pipeline in phase I which should increase to 1.5mn MT in phase II; Phase I commissioning of pipeline is scheduled in H2 2024. Setting up a cryogenic terminal (48’000 MT) to fulfill additional demand from KGPL pipeline

- Kandla: 70’000 MT/month utilization currently. Its an open port with HPCL and BPCL using LPG from this port

- Haldia: Natural growth of 10-15%

- Liquid division: 230’000 lakh kl under construction which will commercialize in FY24 and contribute in FY25. Current capacity is 1.6mn, so this will add 14% additional capacity

- Autogas division: 4’888 MT in Q4 (vs 6’280 MT in Q4FY22; 5’100 MT in Q3)

- Sourcing volumes: 2.73 lakh MT in Q4 (2.7 lakh MT in Q4FY22). For FY23, total sourcing volumes were 8.95 lakh MT (vs 5.56 lakh MT in FY22). Expect this growth to continue in 2023

- Mangalore: Setting up 80’000 MT cryogenic LPG terminal (4mn MT throughput) which will be India’s biggest cryogenic LPG terminal

- JNPT: Entry into JNPT port with 110,000 KL Liquids Terminal; to be commercialized in mid-2024. Still to be decided if it will be in Vopak JV (JV has first right to refusal)

- Terminaling quarterly volumes were 877’000 MT (vs 988’000 last quarter). Will try to reach 4 mn MT in FY24

- Commercial & industrial: Quarterly volumes was 136’100 MT (vs 151’400 MT in Q3; 191’300 MT in H1FY23)

- Bulk industrial volumes were 1.31 lakh MT (vs 1.32 lakh MT in Q3; 0.45 lakh MT in Q4FY22)

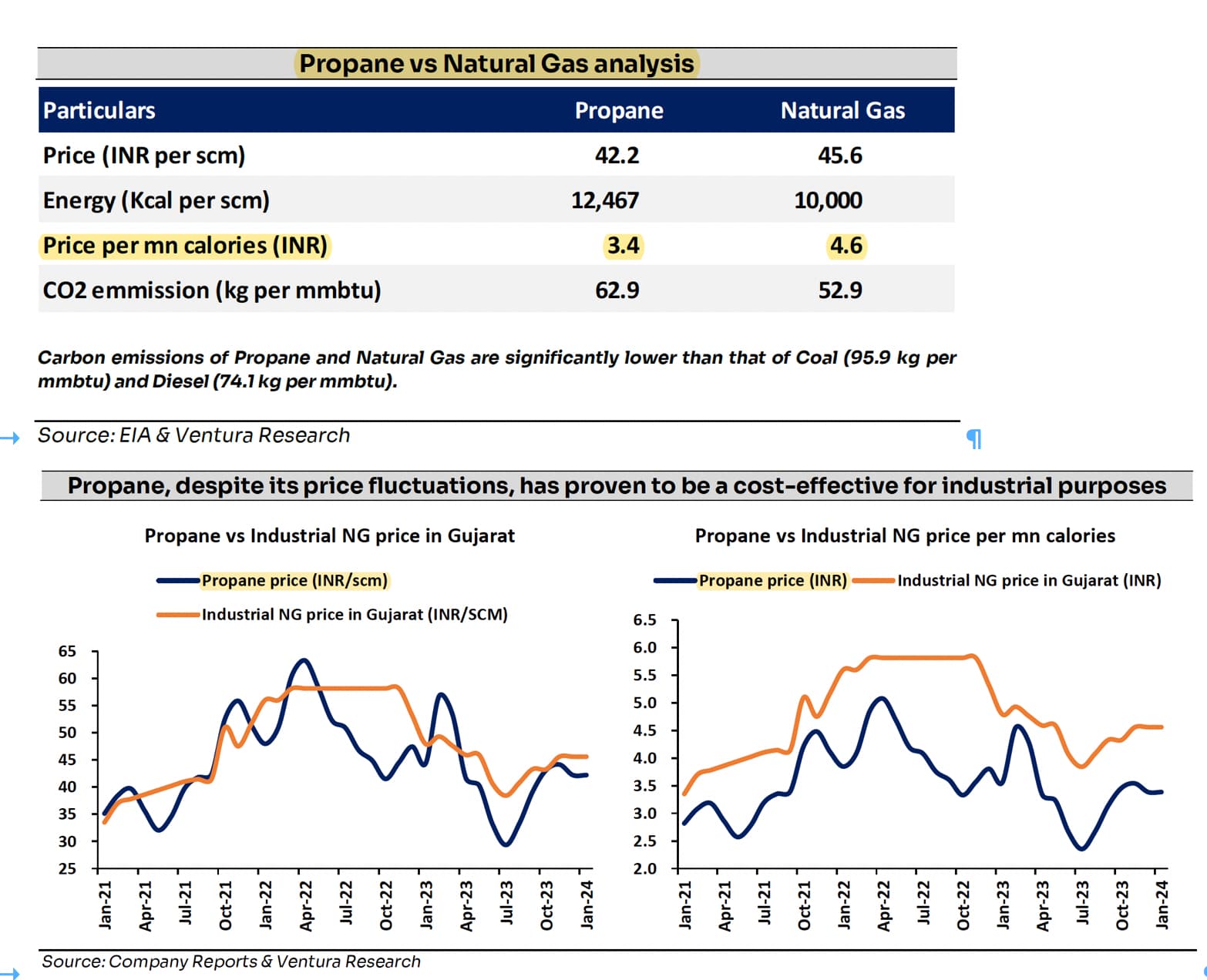

- Propane is still cheaper vs natural gas (15-20%), which should sustain with LPG price cut announced by Saudi Arabia

- Liquid capacity is at full utilization

- Expect 15-20% EBITDA generation on the 4500 cr. capex investment over FY22-27

- Guidance: EPS growth of 25% (FY22 to FY27)

- Higher other income is because of option valuation of the JV

- Vopak gearing will be maintained at 0.6x gearing

Disclosure: Invested (position size here, no transactions in last-30 days)

Aegis reported another good quarter with highest ever distribution volumes, largely driven by bulk industrial volumes. Concall notes below.

FY24Q1 concall

- Pipavav: First VLGC will start soon

- Kandla: Capacity utilization is >20% and higher than expectations

- Haldia: Operations are normal now, its a captive terminal now for HPCL

- Liquid division: All facilities except Pipavav are running at 100% utilization

- Sourcing volumes: 2.26 lakh MT in Q1 (2.3 lakh MT in Q1FY23)

- Terminaling quarterly volumes were 881’000 MT (vs 637’000 in Q1FY23)

- Commercial & industrial: Quarterly volumes was 159’000 (vs 136’100 MT in Q4FY23; 85’000 MT in Q1FY23)

- Bulk industrial volumes were 1.44 lakh MT (vs 1.31 lakh MT in Q4FY23)

- Capex: 1750 cr. will be in JV

- Propane is still 20-25% cheaper than natural gas

Disclosure: Invested (position size here, sold shares in last-30 days)

Two news - Govt cuts agri cess on LPG and Gujarat Gas hikes natural gas rates by ~6%. this might benefit Aegis gas distribution volumes.

Aegis continued reporting very good nos (23% growth in EBITDA, 36% growth in EPS). Even with QoQ decline in distribution volumes, they were able to increase absolute EBITDA by focusing on product mix. Another important trend was terminalling volumes crossed 1mn MT this quarter, and management seemed confident of reaching 4mn MT in FY24. Pipavav will likely drive LPG volume growth in next few quarters. Concall notes below.

FY24Q2 concall

- Pipavav:

o 2 additional spheres commissioned (3700 MT static capacity)

o Cryogenic 45k MTPA will be tanked with the jetty that Gujarat Pipavav is building (Gujarat Pipavav’s $90mn investment)

o The jetty has already been upgraded to birth VLGC and railway gantry is doing large volumes, feeding in-land demand in that region

o Very very bullish on Pipavav LPG operations

o Started doing renewable fuels in Pipavav

o Will see a step growth once KGPL pipeline gets commissioned in December 2024 - Kandla: Kandla Gorakhpur pipeline: work is going at full stretch and pipeline is expected to start by January 2025

- Mumbai: JNPT liquid terminal is expected to finish by end of FY24

- Mangalore: Liquid capacity is expected to finish by end of FY24

- Kochi: Liquid capacity is expected to finish by end of FY24

- Sourcing volumes: 1.74 lakh MT in Q2 (vs 2.28 lakh MT in Q2FY23). Reported sourcing volumes is only for outside sales (not for their own retailing volumes)

- Terminaling volumes: 1’020’000 MT in Q2 (vs 832’000 MT in Q2FY23). Hoping to get to 4mn MT in FY24

- Commercial & Industrial: 131’000 MT in Q2 (vs 159’000 MT in Q1FY24, 116’000 MT in Q2FY23). With Kandla rampup, expect consistent growth in commercial & industrial volumes

- Bulk industrial volumes: didn’t give breakup as it now accounts for 80% of distribution volumes

- 90% of LPG usage is in household consumption as cooking gas. Have seen huge adoption of propane and LPG for industrial usage in last year

- 15-25% discount between propane and natural gas. Conversion of natural gas to propane equivalent is current price of NG (Rs. 46)/0.75 + 6% VAT ~ 65

- Hurdle rate is always 15% on any capex and 20% margins, with gearing of 0.6, expect ROE of 35-40%

Disclosure: Invested (position size here, bought shares in last-30 days)

After Spending a 3 days and Refer Above Thread Here is My Take

Industry Overview

According to the fortune business insights the size of the world market for liquefied petroleum gas was estimated at USD 128.48 billion in 2020, and it is expected to increase at a compound annual growth rate (CAGR) of 7.3% from USD 129.17 billion in 2021 to USD 211.96 billion in 2028.

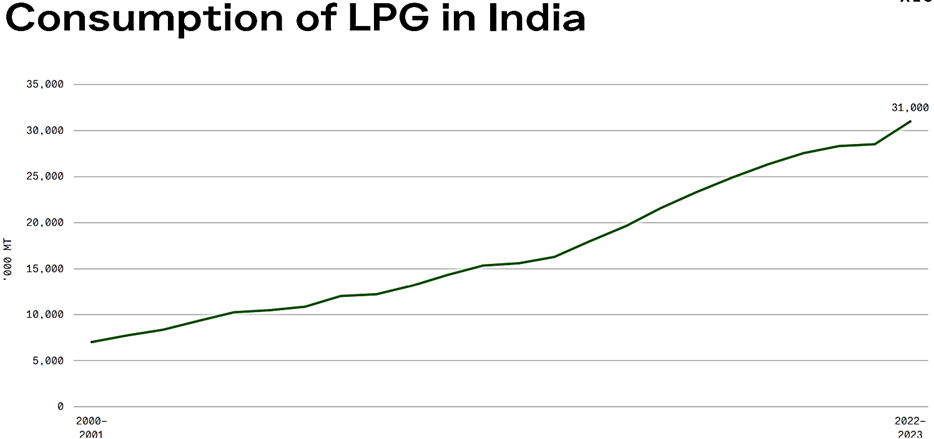

The demand for LPG in India was 30.6 million tonnes in FY2021 and is expected to grow at a healthy CAGR of 1.78% until FY2030, when it is expected to reach 36.9 million tonnes.

Company Profile

Aegis Logistics incorporated in the year 1956 and plays a key role in India’s downstream oil and gas sector

The Company is engaged in providing logistic solutions for Oil Gas, Chemicals and Petrochemical Industries and operates a network of bulk liquid handling terminals, liquefied petroleum gas (LPG) terminals, filling plants, pipelines, and gas stations to deliver products and services

Company has Network of 142 Autogas stations in 10 states, and 290 LPG distributors across 140 cities in 15 states.

The company operates through its state-of-the-art Necklace of Liquid & Gas terminals across major ports of India having a storage capacity of 15,70,000 KL for Chemicals & POL and 1,14,000 MT of static capacity for LPG.

Why I Liked To study?

- Liquid Division: New capacity from acquisitions, volume and revenue growth, and capacity expansion

- Gas Division: Record Volume of 1 million metric tonnes handled

- Company Fixed Asset Jump in FY21 Rs 1711 Cr To Sep FY23 Rs 3766 Cr and Expected to Cross Rs 4200 Cr

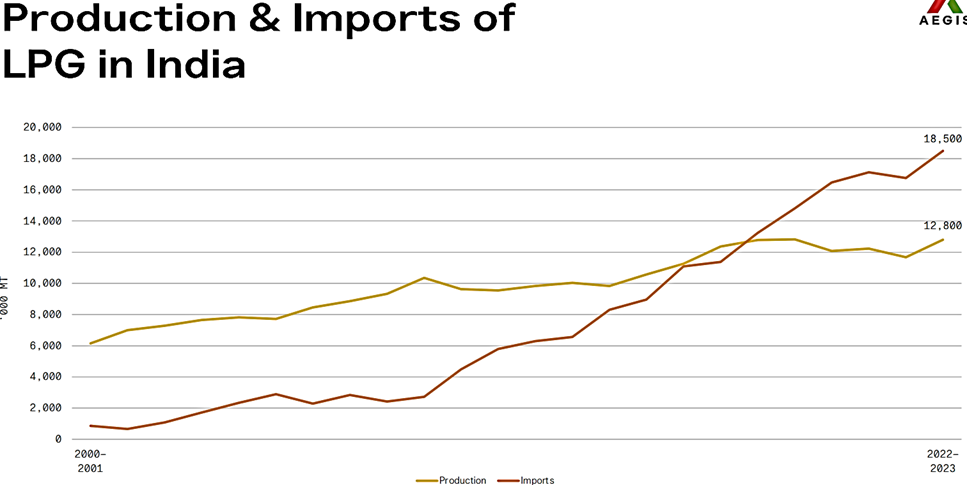

- 55%-60% Import we are dependent and likely to create 25 mmt Gap by FY30 which brings an Opportunity for the Company due to market leadership

- Expect 15-20% EBITDA generation on the 4500-cr. capex investment over FY22-27

Business Model

Aegis Logistics Ltd, along with its subsidiaries, provides logistic solutions for oil, gas, chemicals and petrochemical industries. The business of the company can be divided into two broad segments, viz., liquid logistics division and gas division.

Business Segment -

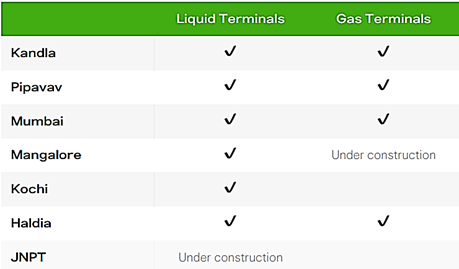

- Liquid Division: Liquid Division Contributes 30% revenue and complete logistics services from sourcing, storing, moving and distributing products .Company LPG Sourcing done with JV of Itochu in Singapore and having terminal ports in Mumbai, Haldia, Pipavav & Kandla and also provides storage for Refrigerated Gas

- Gas Division: Gas Division contributes 70% revenue and Provides import, export, storage, and logistics services, handling Class A, B, and C products as well as all types of chemicals , POL Products and Vegetable Oils and have Tanks includes MS, SS, Epoxy Coated, IFR tanks with Pipeline connectivity with major clients like HPCL, BPCL, HPFR, BPFR and Oil installations in Sewree and Wadala and located at Mumbai, Kochi, Haldia, Pipavav, Kandla, Mangalore. Integrated LPG Supply Chain

Key Clientele & relationship

Competitive Strength

- Aegis Logistics is a leader in Oil Gas and Chemical Logistics and Creating India’s No. 1 private LPG Company

- Cost leadership in the LPG import market and lowering the delivered price to most competitive levels

- Aegis and Vopak propose to form a JV to take advantage of the numerous growth opportunities in the field of oil, gas and chemical logistics in India

- Large & Diversified Client Relationships

- Company has Network of 142 Autogas stations in 10 states, and 290 LPG distributors across 140 cities in 15 states

Future Outlook

- Completed Aegis-Vopak Joint Venture

- Executed important acquisition of 550,000 KL of Liquids capacity at Kandla port

- Kandla LPG terminal fully operational and The management anticipates that the Kandla terminal’s ramp-up will Drive throughput volumes to increase 20% YoY in FY24.

- Entry into JNPT port with 110,000 KL Liquids Terminal as first step is expected to be commissioned in mid-2024.

- Connection to LPG pipelines (KGPL and JLPL) secured for Pipavav & Kandla terminals

- Haldia Liquids expansion completed

- Additional LPG Pipelines installed at Jetties in Haldia and Mumbai

- Pipavav LPG bottling plant completed

- At Mangalore, work is presently in progress on Building the biggest cryogenic LPG terminal in India, which has a capacity of 80,000MT. The end of FY24 is also likely to see the commissioning of liquid capacity expansions of 50,000CBM at Kochi and 70,000CBM at Mangalore.

- The company maintains its guidance of Achieving a growth of 20% to 25% compared to the previous year

- Expect 15-20% EBITDA generation on the 4500-cr. capex investment over FY22-27

- Guidance: EPS growth of 25% (FY22 to FY27)

Risk

- For the period of 2023–2027, the JV has scheduled a capex programme of INR 45 billion, to be financed by debt, internal accruals, and a small amount of shareholder cash infusions. The focus will be diverted from the LPG business, which could increase uncertainty, and such a large and ambitious Capex will strain AGIS’s balance sheet.

- Moreover, the competition from private companies and oil marketing companies makes it difficult to ramp up LPG throughput.

- Needs To Monitor LPG Volume, Distribution and Sourcing QoQ & YoY any gap should be Closely monitored

Dis: Only For Educational Purpose

There was a recent Ventura report on Aegis, which talked about a 1000 cr. expansion in storage of green ammonia (80k MTPA capacity) in Odisha. I dont remember management talking about this during concalls, but its good to see them finally pushing the pedal on capex. I am sharing the relevant excerpts from the report.

09.01.2024 Ventura report

- The next stage of expansion includes developing a facility in Odisha for storing 80,000 MTPA of green ammonia with an investment of 1,000 cr.

- Green ammonia, a derivative of green hydrogen, will also be produced under NGHM and it will be especially relevant for the fertilizer industry. Currently, Indian fertilizer companies primarily derive ammonia from imported LNG, leading to higher production costs

- Government’s strategy to shift from imported LNG to a cleaner and domestically produced feedstocks is expected to increase the demand for green ammonia and its related transportation/storage infrastructure. AVTL’s upcoming green ammonia storage facility is poised to be a key strategic asset, potentially benefiting from the NGHM.

Disclosure: Invested (position size here, bought shares in last-30 days)

Thank you for the summarization of the company. I am a long term shareholder, and have seen this company executed projects very well since 2007. Upto 2027, lots of capex is on the cards, and timely execution will be key to success to the company.

One area I have not seen anyone try to answer/explore, and myself not being very research analyst kinds i have also struggled to understand myself. Aegis works in a field that has a lot of govt breaucratic red tape for approvals, etc and they have done it well, indicating they understand how to deal with govt systems. I have always believed that govt needs to get out of this business of terminalling, logistics, etc which IOCL, HPCL, BPCL are doing, and privatize these. Maybe the next term (of Namo) might see some progress on this front. Q is, Will Aegis have the required balance sheet size, technical expertise, etc to bid for these assests when it comes online?

I understand, Its a big IF, and since there is no clarity, there is no purpose in diving into it. If anyone has visibility on this aspect, please share your views. Thanks in advance.

A post was merged into an existing topic: About the Company Q&A category

This quarter results has some misses especially for the distribution. Is the LPG distribution to industries really a sustainable business ? I mean with the LNG coming as alternative and probable price softening maybe due to increased production in USA not sure how that will pan out. @harsh.beria93 as you are tracking this business from a long time your thoughts will be much appreciated.

Aegis reported flattish nos, its good to see that their terminalling volumes are now consistently over 1mn MT and management is confident of 20%+ volume growth in FY25 (probably reaching 5mn MT). Concall notes below.

FY24Q3 concall

-

Pipavav: Commissioned spheres of 3700 MT generated revenues in Q3

-

Haldia: Industrial distribution is small here, will look to slowly build up

-

Sourcing volumes: 1.79 lakh MT in Q3 (vs 2 lakh MT in Q3FY23)

-

Terminaling volumes: 1’097’000 MT in Q3 (vs 988’000 MT in Q3FY23). Expect 20% volume growth in FY25 (from existing assets)

-

Commercial & Industrial:

-

144’000 in Q3 (vs 131’000 MT in Q2FY24, 157’000 MT in Q3FY23)

-

Margins vary from 2500-3200 which causes volatility in reported EBITDA from gas segment

-

Reduction is natural gas prices has not impacted volumes (QoQ basis).

-

Customers have been using natural gas and propane as two alternate fuels. Have been focusing on converting more customers to have the dual fuel option

-

Newer bottling plants that Aegis has been putting up has helped them increase their reach to smaller companies

-

Current price differential between LPG and LNG is 10-15% (after accounting for calorific value)

-

-

Liquid capacity: will reach 1.9 mn kl post current expansion (vs 1.6 mn kl in FY23). Will increase by further 300,000 kl in FY25

-

Ammonia: Working on an active set of projects which will be announced when its confirmed

-

Capex: announced projects of 1750 cr. will be finished in next 18-24 months

-

Cash: 1700 cr. (debt: 1200 cr.)

Disclosure: Invested (position size here, bought shares in last-30 days)

The JV has bought liquid terminals of 76000 KL at the mangalore port and also plan to expand the capacity further by 85000 KL.

Aegis Logistics Ltd_638404200638984818.pdf (1.3 MB)

Good analysis cum insights report on business and valuation!!!

Confcall notes: Confcall Link & FY24 - Q4 PPT Presentation

Aegis business getting supercharged now, with capex and growth lining up nicely.

Main Announcement from Raj Chandaria

Dividend Announcement:

- Final dividend recommended: INR 2 per share.

- Total dividend for the year: INR 6.50 per share.

- Two interim dividends already paid in February and August.

Company Mission and Strategy:

- Focus on transitioning to a more sustainable India.

- Mission to store and distribute bulk liquids and gases in a safe and sustainable manner.

- Looking for M&A opportunities to expand.

- Expanding distribution footprint by installing more LPG filling plants.

- Building out capex plan for growth.

Financial Performance:

- Surpassed INR 1,000 crores in normalized EBITDA for FY '24.

- Record revenues and EBITDA in Liquid Division.

- Highest-ever volumes in Logistics and Distribution segment.

- Operating EBITDA for Liquid division: INR 396 crores, for LPG division: INR 612 crores.

- Record volumes in LPG logistics business and distribution volumes.

- Profits for FY '24: INR 672 crores, 32% year-over-year growth.

Expansion Projects:

- Various expansions and acquisitions across different ports like JNPT, Pipavav, Mangalore, Kandla, Kochi, and Haldia.

- Total liquid capacity to reach almost 2 million KL.

- Additional 300,000 KL to be constructed in FY '25.

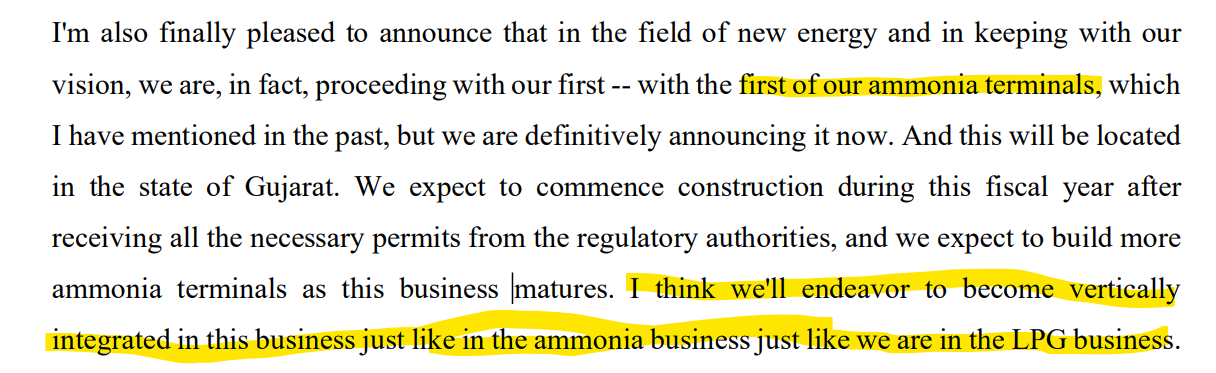

- Plans for ammonia terminals to be constructed in Gujarat.

- Major capex plan of INR 4,500 crores by FY '27.

Q&A Insights:

- Discussion on ammonia terminal capacity and financials.

- Margins improvement in Distribution business due to procurement efficiencies.

- Expectation of logistics volumes to exceed 5 million tons in FY '25.

- Liquid revenue growth attributed to capacity addition and product mix.

- Liquid capacity utilization at 87%.

- Expectation of 10-15% growth from capacity addition in Liquid business.

- Confidence in delivering 25% EPS growth year-on-year.

- Logistics division EBITDA per ton around INR 1,100.

- Distribution EBITDA impacted by procurement efficiencies.

Overall Outlook:

- Management optimistic about continued earnings growth.

- Focus on leveraging different business segments for profit growth.

- Emphasis on sustainable and strategic expansion for the future.

Ammonia Terminal:

- Revenue between ₹2,500 to ₹3,500 per stacking capacity metric ton.

- Potential profitability similar to LPG, around 90% EBITDA.

- Expected EBITDA of ₹120 crores at full or 3x asset turn.

- Terminal equipped to handle import and exports of various types of ammonia.

- Initial focus on gray ammonia imports and green ammonia exports.

- Expected demand for green ammonia in the future.

- Infrastructure already in place at Pipavav for the terminal.

- Initial capex estimated at around ₹500 crores.

LPG Business:

- Throughput EBITDA per ton in FY '24 was ₹1,100.

- Distribution EBITDA per ton in FY '24 increased to ₹4,500 to ₹5,000.

- Minority contribution to profit expected to be between 15% to 20%.

- Healthy competition with natural gas in markets like Morbi.

- Propane continues to be in demand due to cost advantages over natural gas.

- Focus on replacing dirty fuels with clean fuels like LPG.

Liquid Business:

- Return on capital employed for the Liquid division varies due to factors like CWIP, assets under construction, and cash reserves.

- IRR for Liquid division expected around 25%.

- Capacity utilization expected to be high as demand drives usage from day one.

Distribution Business:

- Procurement efficiencies led to improved EBITDA in a particular quarter.

- Average EBITDA margin in the Distribution business expected to be around ₹3,000 per ton.

Future Outlook:

- Anticipated growth in LPG demand in India due to energy transition.

- Government initiatives supporting the growth of clean fuels like LPG.

- Potential for significant growth in LPG demand in the coming years.

- Confidence in delivering good financial results in FY '25 and beyond.

Challenges and Opportunities:

- Potential challenges from natural gas distribution plans by the government.

- Strong push by the government for LPG usage and distribution.

- Focus on continuous growth and expansion in the sector.

New Projects and Developments:

- Announcement of a new ammonia terminal project.

- Expansion of storage facilities and tanks to enhance capabilities.

- Positioning the company well for future growth and sustainability.

- Confidence in executing expansion plans and delivering strong financial performance.

Aegis had another good quarter and a very good full FY24, with FY24 EBITDA growing by 25% and EPS by 23%. They finally announced their ammonia expansion which should deliver 120 cr. EBITDA at full utilization and require 500 cr. investment. They are confident of growing terminaling volumes to 5mn MT in FY25 (vs 4.1 mn MT in FY24) and distribution volumes by 25-30%. Concall notes below.

FY24Q4 concall

- Pipavav

- 45,000 MTPA capacity will be commercialized by Q1FY26 (around the same time as KGPL pipeline)

- Recently commissioned LPG bottling plant

- Haldia : Added 50,000 kl of liquid capacity

- Kandla :

- Commissioned 35,000 KL of liquid tanks, taking total capacity to 970,000 MT. Additionally constructing 25,000 KL which will be operational next year

- Mangalore:

- Following these expansions, total liquid capacity at Mangalore will reach 154,000 KL and are constructing an additional 71,000 KL in liquids that will be operational in the next 12 to 15 months

- Kochi : Acquired 16,000 kl liquid capacity and expanding by 25,000 kl

- JNPT : will be commissioned in 2024

- Terminaling:

- EBITDA/ton was 1100 EBITDA/ton (vs 1000/ton earlier) due to procurement efficiencies which they get as they handle more gas volumes. Expect this improvement to continue

- Expect 5mn MT volume s in FY25

- Current price differential between LPG and LNG is 7-10%

- Distribution

- EBITDA/ton was 4500-5000 (normal margins should be around 3000/tons)

- Expect large growth in distribution business as Mangalore and Pipavav come onstream in FY26

- 40-50% of Morbi volumes are now LPG

- Expect 25-30% volume growth

- Sourcing volumes: 798,400 MT vs 895,300 in FY23

- Liquid

- Capacity was 1.9 mn kl and will increase by 300,000 kl in FY25, operated at 87% utilization

- Revenue growth was higher than volume because of some take-or-pay contracts

- Liquid contracts are 1-year and they generate 3000/CBM

- Ammonia:

- Will start construction of first terminal in Pipavav (36,000 MT capacity) which can result in throughput of 3x a month and 1.2-1.3 mn MT in a year at optimum utilization - 500 cr. investment

- Expect 3x turns, 1.2 mn MT volumes at peak utilization with 1000/ton EBITDA (i.e. 120 cr. EBITDA at peak utilization i.e. 3x asset turns). Expect slightly under 1000/ton EBITDA

- Can handle any kind of ammonia (gray/blue/green)

- Currently most users have their own terminals

Disclosure: Invested (position size here, sold shares in last-30 days)