Q1 FY21 UPDATE

Liquid Business

The liquid business was very good in Q1. The business model in this business is based on fees for storage tanks. Even though there was less economic activity, companies still needed storage tanks to store chemicals etc.

The company is doing liquid business for 40 years and there are 50-60 clients like traders, chemical companies etc. This business does not have client concentration risk as gas business. The main advantage company has is land/infrastructure at prime locations in ports. e.g. Mumbai port volumes are still growing, even if someone new wanted to come, there is no land.

The entire capacity at Mangalore liquid terminal is pre-booked.

There is consolidation happening in liquid terminals business and there are few distressed players. The company might considering acquiring one or two.

Gas Business

Sourcing Business

The gas business was particularly pulled down by sourcing business. Sourcing business was impacted due to lowest crude prices and corresponding gas prices in a decade. In addition to this, there were high inventories leading to lesser imports. Government had announced 3 free LPG cylinders during lockdown period. In anticipation of additional demand, PSUs had overbooked the imports. But the demand did not go up as expected and hence the additional inventory.

Near Term Growth Triggers

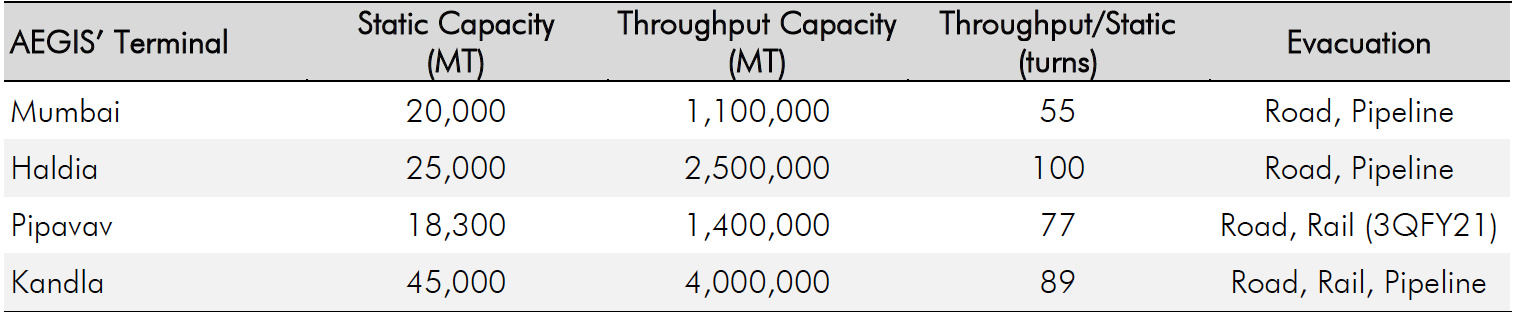

The company is planning to take LPG throughput capacity from 5mn to 9mn in next 1-2 years. Current utilization throughput is at 3mn. The expansion is primarily happening at Kandla for capex of 350cr with throughput capacity of 4mn. This will come online over next 6 to 12 months.

Mumbai-Uran-Chakan-Shikrapur (Pune pipeline) is at 50% throughput and expect throughput to reach good levels from Oct onwards. This should help in profitability meaningfully from Q3.

Pipavav railway gantry will come online from Q3 and that should help to vacate more volumes and should help to boost earnings.

The margin in LPG throughput services is around 1000rs per tonne and it is a small part of overall transport cost to customer.

Haldia Gas Terminal

- There is a BPCL gas terminal coming up in Haldia which will be commissioned over next 6 months.

- The anchor customer in Haldia is HPCL which consumes 80% throughput. Rest 20% is consumed by BPCL. Once BPCL terminal comes up, BPCL share will be taken over by HPCL.

- Gas penetration is low in east and northeast and HPCL is building out distribution network. Don’t see much demand disruption.

Medium/Long Term Growth Triggers

- The company is planning to take gas stations from ~110 to 200 over 3-5 years.

- The company is planning to build the retail business state by state. Even if company achieves its plan by 2025, its share in retail business would still be only 1%. This business requires very little capital and has EBITDA margin of 2500-3000 per tonne which is margin accretive.

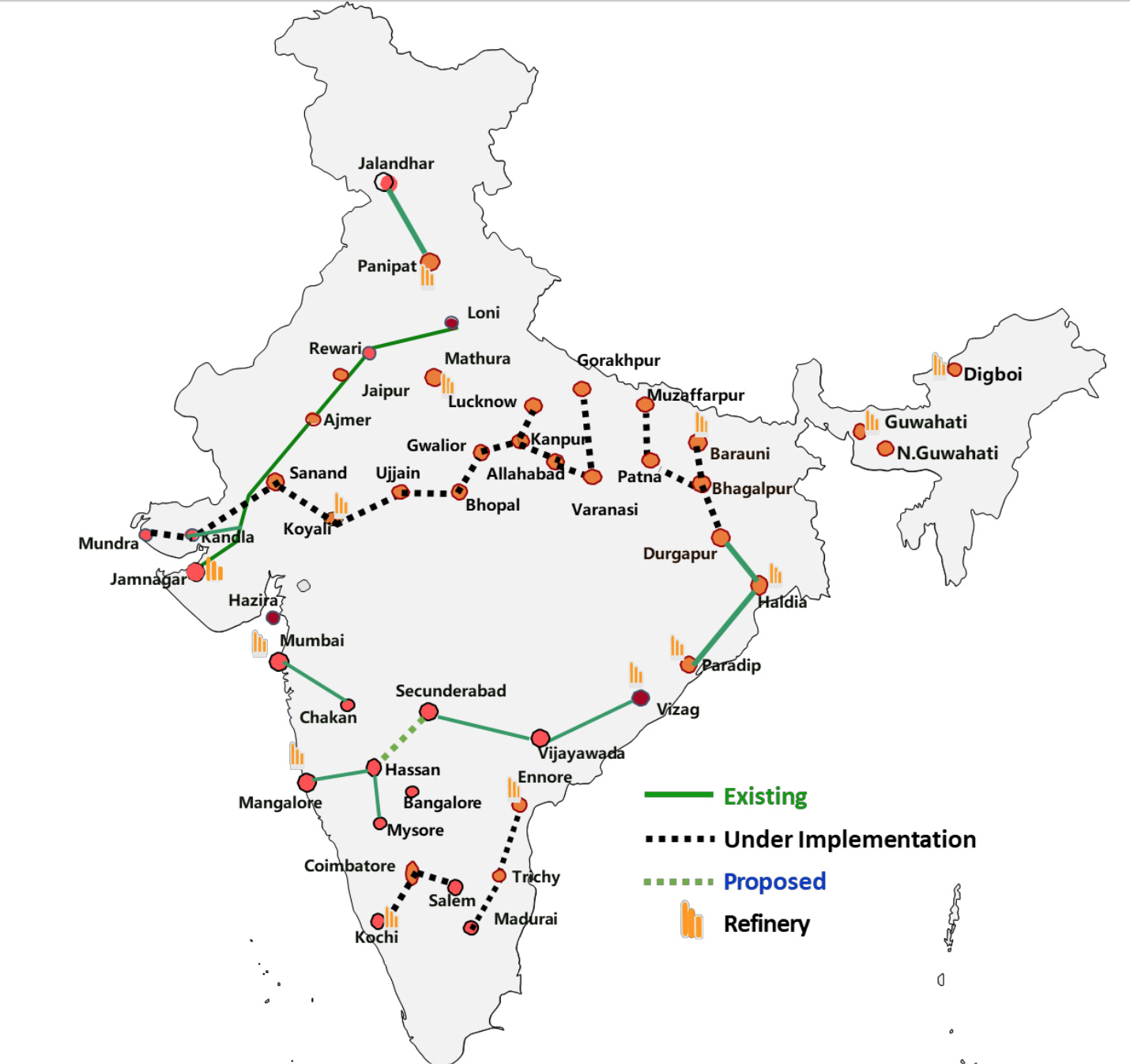

- Pipelines across India till 2025 -

- Kandla - Gorakhpur, 2800 kms, planned completion of 2024-25, largest pipeline in the world

- Uran - Chakan - Shikrapur, 168 kms, completed

- Paradip - Haldia - Durgapur, most probably completed

- Kochi - Coimbatore - Salem, work in progress

- The LPG consumption is expected to grow at 6% over a decade as per various reports and that serves as underlying supporting trend.

BPCL Privatization

We need to see if BPCL really gets privatized. Aegis feels that if profitability is main objective of new owner, he would find relationship with Aegis beneficial.

My View

Over next 18-24 months, I see 2-3 things happening.

First off, the impact of ESOPs will wear off and PAT numbers and corresponding optical valuation would start to look better.

Then I see a growth trigger pretty much every 6 months for next 2 years - Pune Pipeline, Pipavav Railway Gantry Line, Kandla Capacity Coming online, then various liquid terminal projects and growth on retail/commercial side.

We need to do more work on promoters (history, background, ambition etc.) as well as competition mapping. The sector has lost fancy long time ago and it remains unexciting for investors. Can Aegis become an exception?

Disc - I have < 5% allocation and I am still tracking and understanding the business. This is not a buy/sell recommendation.

but might finally get over - how much of an impact does that make?

but might finally get over - how much of an impact does that make?