I have allocated 4% to buy Godfrey Phillips by allocating remaining 2% cash and reduced position in ITC to 2% (from 4% earlier). When I had exited Godfrey earlier in March 2023, this was the note I had shared.

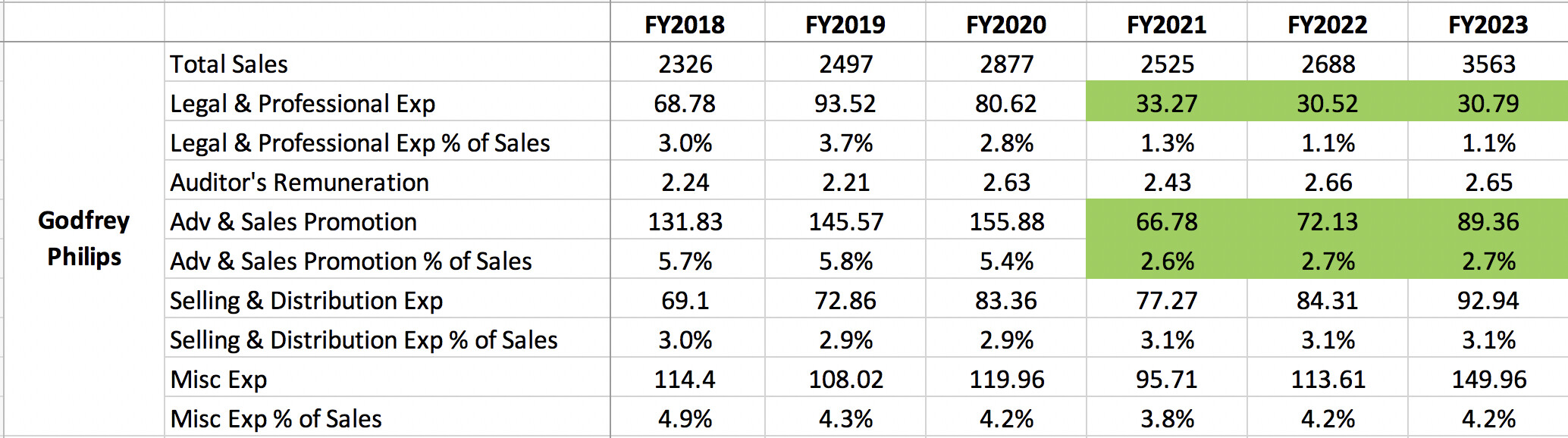

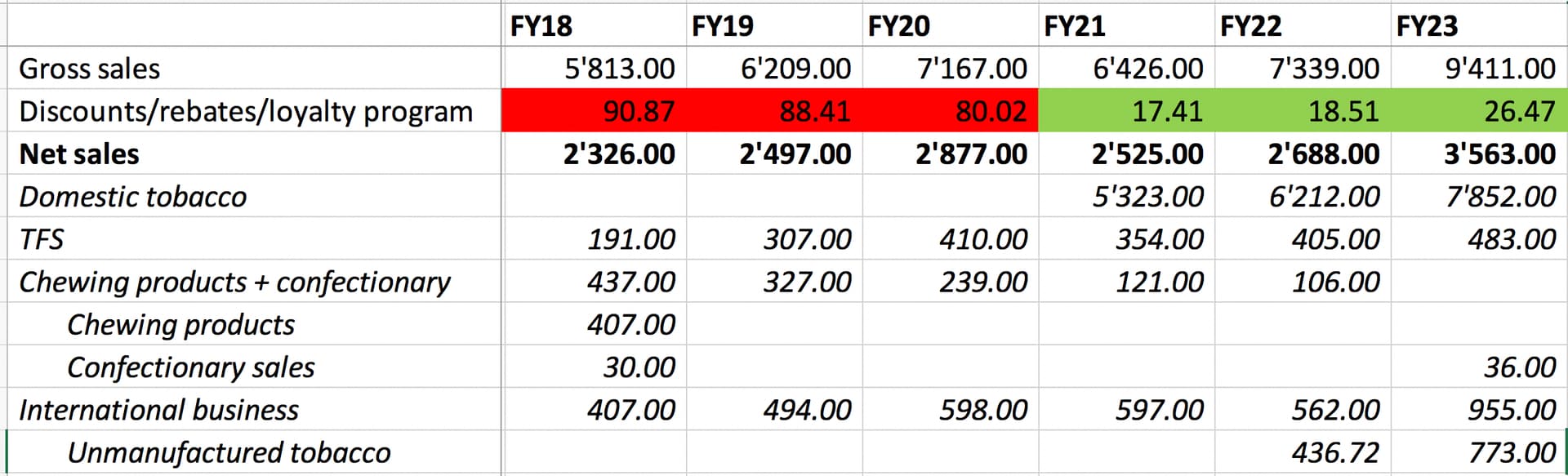

Since then, Godfrey has continued reporting fantastic numbers with margins and growth being maintained. In last quarter, they reported their highest ever quarterly profits of 250+ cr. and looks set to report 1000 cr.+ profits in FY24. Just to give some context, they had 260 cr. annual profits in FY19, so there has been a 4x scalability in profits since 2019.

This large jump in profits has come on the back of reduced legal and advertising costs. Whats even more impressive is they have managed to grow despite reducing discounts/rebates. Generally, this is very uncommon for a FMCG co.

International business continues to be their growth driver with them benefitting from realignment of Russian supply chain. At their AGM, they mentioned that global tobacco cos like Phillip Morris are now buying more raw tobacco from Indian cos after the Russia Ukraine war. At 11’000 cr. market cap and a potential 1000 cr. PAT, I find them to be a very reasonable bet in this heated market. Cash comes down to zero. Updated folio is below

Core compounder (42%)

| Companies | Weightage |

|---|---|

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Bank Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Gufic Biosciences | 4.00% |

| Godfrey Phillips | 4.00% |

| I T C Ltd. | 2.00% |

| Aegis Logistics Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

| Caplin Point Laboratories Ltd. | 2.00% |

| P.E. Analytics Ltd | 2.00% |

| Aptus Value Housing Finance India Ltd. | 2.00% |

Cyclical (47%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 2.00% |

| Stylam Industries Limited | 2.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

| ANUH PHARMA LTD. | 2.00% |

| Shree Ganesh Remedies Ltd - PP | 2.00% |

| Aditya Birla Sun Life AMC Ltd | 2.00% |

| Dharmaj Crop Guard Ltd | 2.00% |

| MAYUR UNIQUOTERS LTD. | 2.00% |

| Godrej Agrovet Ltd. | 2.00% |

| KSE LTD. | 1.00% |

Turnaround (2%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 2.00% |

Deep value (9%)

| Companies | Weightage |

|---|---|

| Geekay Wires | 2.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| RKEC Projects | 1.00% |

| Worth Peripherals Ltd | 2.00% |

I have been very concerned about the state of Best Agro’s balance sheet and cashflow generation. Not only do they have large debt, but they also don’t generate any cashflows. P&L and balance sheet paints completely different pictures. On the other hand, Dharmaj has managed to grow while maintaining very strong control on their working capital. Also, I find their promoters very grounded and focused at their jobs.

Please search this thread to know my thoughts on diversification. I will not repeat the same thing over and over again.

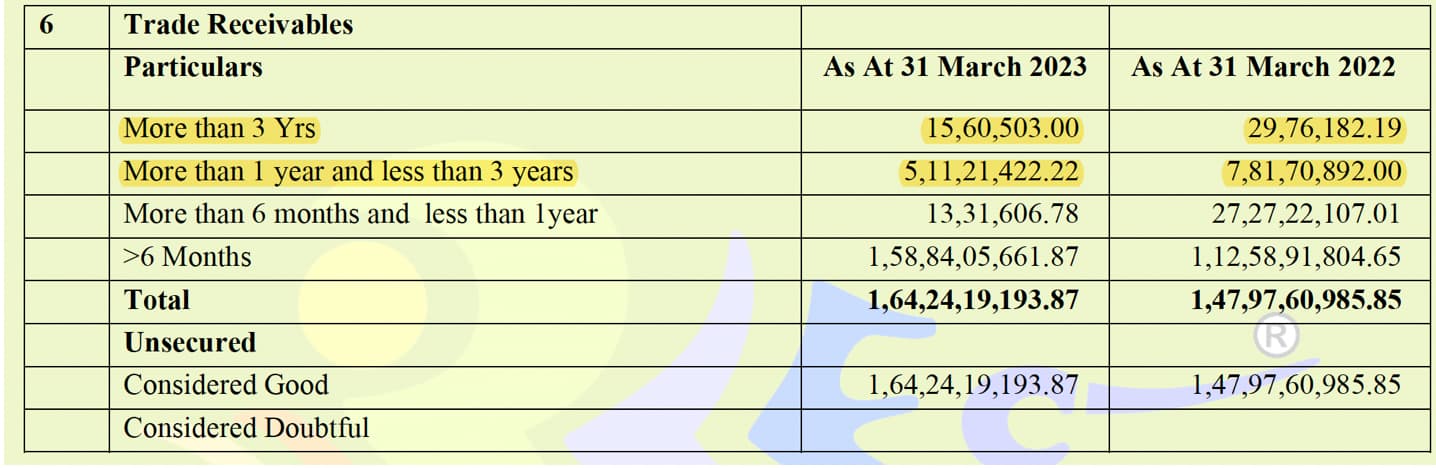

Ageing of receivables do not show anything very alarming (~3% older than 1 year).

If you carefully read their annual report, you will see that they paid 3.4 cr. interest on statutory dues which suggests they delayed these which might be due to liquidity constraints. Recently, I noticed in their EPFO filings that they have cleared large amounts of EPFO payments, and have become regular in their statutory deposits. This suggests that their liquidity situation is improving. In FY23, they also generated very good cashflows.

Additionally, they won a few arbitration orders which will further help them fund their projects. Their outstanding order book in March 2023 was around 1050 cr. which gives good visibility on revenues. Lets see how they are able to scale, current market cap of 170 cr. is quite small and captures a lot of risk.