As of today, I have made the following changes:

-

Reduced position size in Punjab Chemicals from 4% to 2%. This reduction is because of their share prices seeing a sharp drop and not due to my own selling. As we are coming off a huge agchem upcycle, I want to be more measured in buying as channel inventory is still at high levels and might require 6-12 months to clear. I still feel Punjab is one of the most promising bets with multiple drivers (sales growth, margin improvement, balance sheet improvement), but want to add further once I have better visibility.

-

Added 1% position in Shree Ganesh Remedies (SGRL) PP (rights issue shares). SGRL IPO’d as a SME co in 2017. In the next 5-years, their sales multiplied by 3.5x and PAT by 4.3x. SGRL manufactures intermediates for pharma and agchem cos. Their business model is to manufacture intermediates with small market size and high realizations which large players don’t want to manufacture, thereby giving them higher margins. SGRL has garnered 50% market share in their top 4 molecules which is very impressive for such a small company. Additionally, they are doing multiple capexes which should result in good growth going forward. What attracted me towards SGRL was their margins, which have been maintained at 24-25% even in this chemical downturn. I think this is indicative of their differentiated business model. I initiated the position at a small size due to high starting valuations. In addition, I have preferred buying SGRL rights issue shares (SGRLPP) as there is a 15% arbitrage between SGRL and SGRLPP.

-

Added 1% position in Propequity (P.E. Analytics). Propequity runs a website that shows historical property prices in different parts of India. Their main customers are banks, NBFCs, investors, and real estate companies. Recently, they have started a new business vertical where they provide valuation services for housing finance companies. In this vertical, they do due diligence on real estate properties and give valuation reports to the financing co, on the basis of which financiers can underwrite loans. Co has been growing fast and have a very long growth runway.

Recently, Propequity has also announced a partnership with Berkshire Hathaway Home Service, but not much is known about the deal terms. I guess this will be a real estate agency kind of setup. Valuations are very reasonable for the co, especially if one removes the 55-60 cr. cash they have on their balance sheet. I want to scale this position as I get more conviction in this idea.

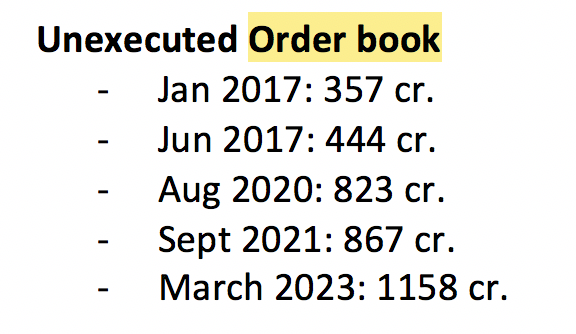

- Added 1% position in RKEC projects in the deep value portfolio: RKEC does EPC work and has strong positioning in marine works. Their current order book is around 1150 cr. and their Mcap is 150 cr. About 5-years back, their Mcap was 400 cr. on an order book of 400 cr. Company is coming off a poor couple of years and disclosed very good results in Dec-22 quarter (~10 cr. quarterly PAT). I am hoping they are able to execute their order book in 2-3 years, which can give them annual PAT of 40-50 cr. On a Mcap of 150 cr., it becomes a very interesting bet.

Apart from these, I am also looking to add Mayur Uniquoters and Glenmark Lifesciences in the model portfolio, and want to increase position sizes in Transpek and Caplin Point. I need to think what I can switch out of. My current thoughts are to sell Control Print and Chamanlal Setia, as both have done very well in the past few weeks and are reaching cyclical high valuations. Any other suggestions?

Cash stays at 0 and updated folio is below:

Core compounder (41%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 4.00% |

| Housing Development Finance Corporation Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Aegis Logistics Ltd. | 4.00% |

| Gufic Biosciences | 4.00% |

| HDFC Bank Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

| Caplin Point Laboratories Ltd. | 2.00% |

| P.E. Analytics Ltd | 1.00% |

Cyclical (51%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Aditya Birla Sun Life AMC Ltd | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Chaman Lal Setia Exp | 4.00% |

| Stylam Industries Limited | 4.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Control Print Limited | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

| Transpek Industry Ltd. | 2.00% |

| Shree Ganesh Remedies Ltd - PP | 1.00% |

Turnaround (2%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 2.00% |

Deep value (7%)

| Companies | Weightage |

|---|---|

| Geekay Wires | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| Suyog Telematics | 1.00% |

| RKEC Projects | 1.00% |

Sorry I haven’t looked at Kfin. At current multiples, I prefer HDFC AMC over Kfin or Cams.