Having been in shipping industry, the turn around of the vessel depends on following.

Size of pipelines from Terminal to Shore tanks.

Number of connection provided by Terminal.

Distance of tank from Terminal.

Capacity available in the Shore tanks.That will depend on number of shore tanks and connectivity from Shore tanks to futher supply.

I have seen vessel waiting for days due to this, thus Terminal incurring demurrage charges.

I have also observed lot of gas terminal, cropping up all around the world.

Infact during my last interaction in US the amount of Gas terminal coming in US gulf area is something worth noticing.

Have seen downtrend in Oil terminals , observed lot of Oil Major ,like SHELL, existing their position in Australia and US area.

Been to VOPAK terminal in US, Singapore and Europe, though on oil tankers. Have seen them dealing with all sizes of ships, going upto

300,000-350,000 Mt.

They will certainly add to the table.

It hasn’t been reported in the thread before, but it was reported to the exchange on 12th Sep that one of the promoters Mr. Anish K. Chandaria unfortunately expired on 11th Sep.

Pipavav:

o Port has started work on making LPG jetty compliant for handling VLGC (completion expected by April 2022)

o In KGPL terminal, Pipavav has been allotted 1.25mn MT in phase 1 which will go to 1.5mn MT in phase 2.

Kandla:

o Port has started work on making LPG jetty compliant for handling VLGC (completion expected by June 2022)

o

Haldia:

o Pipeline connecting Haldia terminal to HPCL Panagarh bottling plant to be commissioned soon

o Should reach normal volumes by March 2023 with HPCL taking up volumes given up by BPCL

o Acquired 2.5 acres land in Haldia

Kochi: Signed 10 (with 15 years extension) year contract for use of 21’000 kl of petroleum storage with Shell

Mangalore: Acquired 21 acres land

JV Vopak: Propose to add 175’000 kl liquid storage (LPG + other chemicals) + 100’000 MT gas storage capacity across Pipavav, Haldia, Mangalore and Kochi with capex of ~1’250 cr.

Expect Phase I completion of KGPL terminal by December 2022

Want to reach 25% market share of LPG imports

Recently market share in LPG has come down to ~15%, this should go up with ramp up of Haldia by uptake of HPCL + Kandla commissioning + better Pipavav connectivity and ramp up of railway gantry volumes

Autogas division: EBITDA margin has reached 10’000/MT

This was an interesting prospect for investment for me but I decided against it at this time. I thought I’d share my views on what made me want to avoid investment at this time.

Company has been (of late) losing market share in the LPG segment due to various factors such as loss of BPCL at Haldia, medium size LPG carrier availability affecting Pipavav operations. This will take longer than expected to resolve and their aspirations of 25% market share will be difficult to achieve.

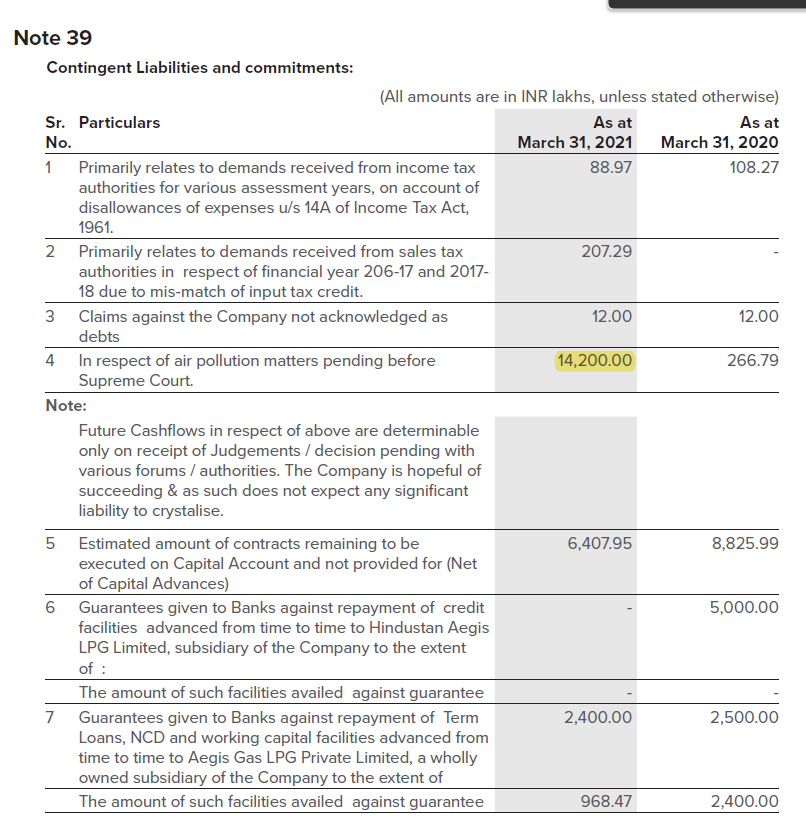

Sharp increase in the Contingent Liabilities yoy on account of 142cr NGT order with regards to the Air pollution issue at Mumbai. Contingent Liabilities now stands at 243cr (12.5% of networth) FY21 AR

The air pollution issue just highlights the exponential threat associated with the nature of this business what accidents/fire/pollution can wipe out years of profitability.

LPG domestic segment demand is linked to government policy (subsidy etc) and its cost relation to alternatives such as PNG etc

An unknown element of risk with the BPCL - Adani stake acquisition (if that were to materialize)

Please note this is just my opinion and I am open to learning and understanding the business better. Contrary arguments would be greatly appreciated as I may be wrong in my analysis.

I think your inference for <1> is not right. I will request you to check volumes for liquid cargo for GPPL and its management guidance and capex. It will help you in doing channel check for what Aegis management is saying.

I think, share price is in correction due to uncertainty around Vopak merger and demise of Anish (MD).

Best thing about aegis is location of its terminals and moat of entering in GAS sector.

It takes time and significant investment to achieve good scale.

The recent series of disclosures about slump sale of liquid division into a new entity gives very good insights into the contribution of Mumbai terminal (which was 100% retained by Aegis) to company’s profitability.

FY21 Liquid division revenue: 234 cr.

Haldia: revenue: 27.01 cr.; net worth: 197.09 cr.; slump sale at 240 cr. (capacity: 174’690 kl) (link)

Kandla (LPG storage + liquid): revenue: 40.66 cr.; net worth: 486.35 cr.; slump sale at 830 cr. (capacity: 140’000 kl) (link)

Mangalore: revenue: 8.79 cr.; net worth: 97.49 cr.; slump sale at 120 cr. (capacity: 25’000 kl) (link)

Pipavav: revenue: 4.05 cr.; net worth: 78.36 cr.; slump sale at 170 cr. (capacity: 120’120 kl) (link)

Kochi: revenue: 8.39 cr.; net worth: (-) 16.72 cr.; slump sale at 18.5 lakhs (capacity: 54’000 kl) (link)

So Mumbai contributes >60% of revenues and probably higher profitability (because of mix of more complex chemicals). No wonder why this was not merged into the Vopak JV.

Pipavav: LPG jetty work for handling VLGC is expected to completed by June 2022 (extended from April 2022)

Kandla: Targeting 1 MT gas volumes in first year of operations (assuming commercialization goes smoothly)

Haldia: Recovered significant volume due to HPCL ramp up, should be back to pre BPCL exit volumes in 2 quarters (revised from earlier guidance of March 2023)

Mumbai: Current throughput capacity is only 1.1 MTPA, this will increase to 1.5 MTPA only in FY23

Autogas division: Not happy with the current volumes and want to improve it, EBITDA margins have been maintained at 10’000/ton

Liquid division margins largely vary b/w 65-70% (depending on the kind of liquids stored)

Aegis reported good set of numbers with 3-year EPS growth reverting back to 20% trajectory (FY20Q1 ~ 1.71, FY23Q1 ~ 2.95). Industrial gas supply through Kandla led to strong growth in realizations, with gas division reporting EBITDA of ~1510 / MT. Industrial gas distribution profitability contributes directly to Aegis’ nos as it is outside the ambit of Vopak JV, which is why EPS grew strongly despite muted gas logistics volumes. The concall notes are below.

FY23Q1 concall

Pipavav: LPG jetty work for handling VLGC is expected to completed by September 2022 (extended from June 2022)

Kandla:

o Distribution volumes shot up due to supply to industrial belt of Morbi and nearby regions. This is not a one-off and should sustain

o On course to achieve 700’000 MT of gas logistics which should contribute to 70 cr. of EBITDA in FY23 (@1000 EBITDA)

Haldia: 10% lower volumes due to upgradation of both the jetties

Higher other income was due to valuation of options under JV amounting to 76 cr.

Higher other expense was due to JV related expenses amounting to 62 cr.

Confident of growing earnings at 25-40% based on current assets on ground

On a consolidated basis, company has net cash of 600 cr.

Disclosure: Invested (position size here, no transactions in last-30 days)

Launch of JV with Vopak commenced operation on 25-May

Kandla port operation has commenced

Interim Dividend - Rs. 1.5

LPG Volumes handled ~ 6.37 L MT at Mumbai, Pipavav and Haldia compared to ~5.67 L MT Q1’22. Despite 10% lower volume at Haldia due to Upgradations

Bulk distribution reported 176% growth supported by Kandla volumes. Expect increased volume to sustain in coming quarters.

AutoGAS sale improved 45% in volume vs Q1’22

Spike in other expenses about ~ 3x, JV related expenses are ~62 Cr which caused the steep increase.

Pipavav would LPG jetty compatible in Q3.

Outlook for FY23 - Liquid business and Gas business expect to be doing well

Kandala is operationally stabilized

~1500 Cr. of cash(after taxes on 2050 Cr) on balance sheet, Consolidated debt is ~ 900 Cr. This is as a result of ~2,050 Cr is received from the Vopak deal

Kandla -

Guidance for full year from Kandla port is - 0.7 mn via distribution or through putting. Confident of 70 cr Ebita from Kandla in FY23.No current agreement with any oil company from Kandla port for through putting, yet.

Kandla Gorakhpur pipeline update - is being constructed would have connection to Pipavav. The allocation of 1.5 Mn. ton volume for Pipavav port. There would be similar allocation to Kandla port. The pipeline is being constructed by a third party. The LPG will be throughput to this pipeline from Pipavav and Kandla.

Management expect to grow business and earnings by 25-40% per annum over next few years. (when asked about - For 3-5 yrs perspective, Gas volume projections at LPG terminals from current 3 Mn.)

CRL terminals and Friends group terminals have put company in commanding position at Kandla port. Brings 700,000KL capacity in liquid business. Objective is to bring the margins up for these over the next period. Scope for operational efficiencies improvement in future.

Sourcing Business- On volumes still not at Pre-covid level, New tenders are coming out and volumes are expected to be back on track this year. Sourcing is not a big profit contributor.

On why AutoLPG has not grown rapidly, Presence of subsidized CNG, Company expects subsidy for CNG is not sustainable. The LPG distribution provides good margins. Difficult to do business at local level. Multi-Fuel distribution model is being built up. And dealers are able to make money. Company trying to push multi-fuel distribution rather than only Auto-LNG.

This can potentially increase the throughputs (increase wherever ports have both railway and road connectivity) of the gas terminals, although Aegis is primarily in LPG, not LNG.

Anyone else having a better understanding how this impacts Aegis, please add.

Aegis reported decent nos, with most growth coming from rampup in distribution business along with revival in terminalling volumes at other ports. Its interesting to see that company has achieved this growth despite no contribution from terminalling in Kandla port, and 1-month shutdown in Morbi belt. Terminalling volumes in Kandla (which was the base behind this whole stock story) will finally start this quarter, they already have 3 ships booked for this month. Will be interesting to see ramp up in volumes along with more contribution coming from industrial division. Concall notes below.

FY23Q2 concall

H1 LPG volumes for Mumbai, Haldia, and Pipavav was 14.70 lakh MT vs 13.05 lakh MT, increase of 13%

Pipavav: LPG jetty work for handling VLGC is expected to completed by Q3FY23 (extended from September 2022). Railway gantry is being used by all 3 OMCs

Mumbai: Operating LPG at full capacity

Autogas division: Quarterly volumes declined 14.8% YOY to 5’100 MTPA

Almost half of Morbi tile cos switched to LPG (propane) from natural gas

Bulk industrial volumes were 173,990 MT in H1 vs 45,816 MT last year. 35-40% was to Morbi. This was despite 1-month shutdown in Morbi

Commercial and domestic cylinder volumes were 17,310 MT vs 11,352 MT last year

Aegis makes 2,000–2,500/ton margins on bulk industrial volumes (through trucks) to Morbi customers. They make 4,000/ton margin for industrial distribution segment done through cylinders. Blended retailing margins are 3000/ton

Total sourcing tender volume contracts for CY22 was 800’000 MTPA. They did volumes of 457’960 MT vs 159’633 MT last year

H2 is generally stronger than H1

One-time special dividend of Rs. 2 celebrating JV transaction

7 cr. profit was accrued to minority interests. Focus is on growing EPS of the company