I started investing globally sometime in 2018. The current portfolio is shown below. The buy and sell rules are the same as that for my Indian portfolio which is shown here. The long term goal is to generate >10% returns in USD.

Entry strategy:

- Shares are acquired in 3 equal tranches with difference of atleast one month between two traches

- Single sector allocation < 25%, single stock allocation < 20%

Exit strategy:

- Shares are sold in 3 equal tranches, similar to the buying rule

Exit reasoning:

- Flawed thesis

- Better opportunity in another company (switching)

- Expensive valuation

| Companies | Weightage (cost basis) |

|---|---|

| AB InBev (NYSE: BUD) | 3.50% |

| Berkshire Hathaway | 10.00% |

| Disney | 5.00% |

| Fairfax India Holdings | 10.00% |

| 10.00% | |

| Philip morris | 2.00% |

| Starbucks | 5.00% |

| UBS ETF CH-SMI | 5.00% |

| Vanguard Emerging Markets Stock Index Fd | 10.00% |

| Cash | 39.50% |

AB InBev: Its the largest global beer manufacturer owning brand such as budweiser, leffe, corona, stella, etc. They are really big in South America, and most of the incremental growth is coming from Africa, China, and emerging markets like India. The recent trend of craft brewery is definitely a risk, along with a moderately levered balance sheet (net debt/EBITDA ~ 4.8). Its not a very strong growth company but is trading at close to decadal low valuations, that’s why the 3.5% weightage.

Berkshire: This is a replacement for S&P 500. They own a very diverse pool of businesses and are trading at close to their lifetime low valuations, thats why the 10% allocation. I try to buy when its trading close to book value and sell at >2x P/B. Key risk is their insurance business which can be killed if negative interest rates persist for the next 2 decades.

Disney: Despite being a bluechip for decades, they have consistently found growth levers. Their content library is very valuable and their recreation parks business (though cyclical) is a monopoly. Most of the incremental growth in parks business comes from China. They are yet to enter India because its not a big enough market for them. With their recent foray into OTT, they have managed to find a way to capitalize their huge content library. Plus they have a quasi monopoly in sports television through ESPN. They have managed to grow their subscription base in US, are already the biggest OTT player in India (hotstar). Basically, they can grow earnings over 10% which is why the 5% allocation.

Fairfax India Holdings: I have written in detail about this investment vehicle here. Their current share price assumes that Bangalore airport has lost 50% of its value due to corona. Their public investments are quite reasonable. Long term stated management goal is to grow book at 15% USD. With the management fee, net shareholder returns should be in excess of 12.5%. At some point, their share price will go back to their NAV. Key risk is that their NAV might come down to the current share price.

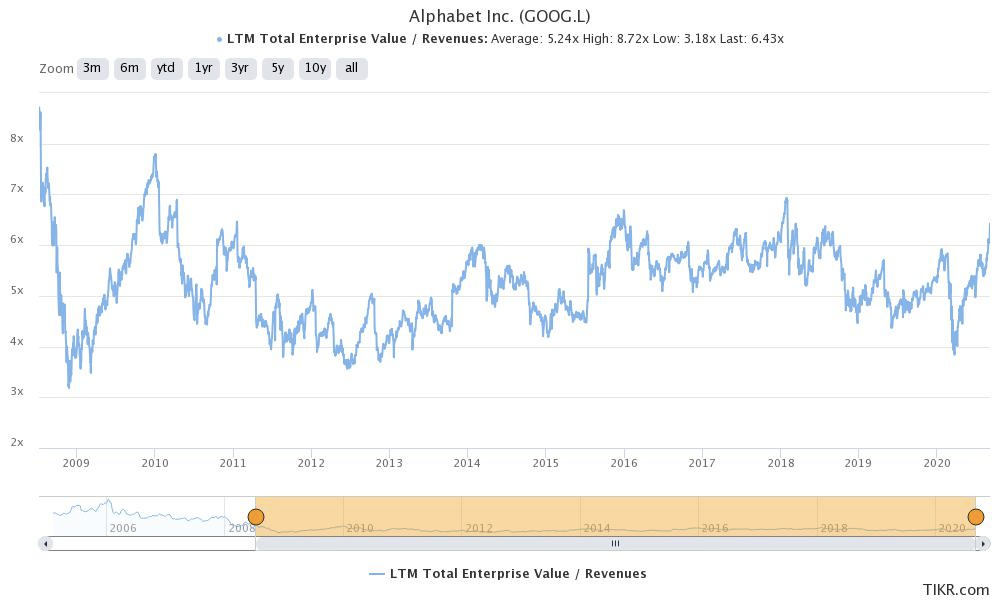

Google: Monopoly in digital advertising, growth continues at 15%. Their multiple lines of business offer reasonable optionality. Not so expensive on valuations. Key risk is the cyclical nature of advertising business, which they have avoided so far because they have been gaining market share over the last decade from traditional advertising. The 10% allocation is because of reasonably high growth rates along with reasonable valuations.

Philip Morris: Keeps innovating in their tobacco business. Valuations are very cheap for a monopoly, however growth days are behind, thats why the 2% allocation. Pays most of earnings as dividends.

Starbucks: This has been a great turnaround story post 2008. Their growth rates are close to 10% with most incremental growth coming from China. India is another market where they are growing quite fast through their partnership with Tata. They cater to the high end customer segment and have a long growth runway.

UBS ETF CH-SMI: This is the Swiss market ETF and my way of playing the Swiss innovation story (pharma, Nestle, and financials). The 5% allocation reflects the high dividend yield (~3%) but low growth potential.

Vanguard Emerging Markets Stock Index Fd: This is Vanguard emerging market ETF (VWO). Emerging markets used to be the darling in 2000-2010 decade, however the euphoria has gone in the past decade. This is my way of playing the China growth story (China has a ~44% weightage in this ETF) and the Chinese market is trading super cheap. Incremental global growth is coming from emerging markets and they are also trading cheap, that’s why the 10% allocation.

I keep on exploring about more businesses and want to deploy the cash in suitable companies. My current watchlist that are outside my assessment of fair value comprise companies like Dropbox, Markel, Uber, Visa, Mastercard, Nestle, Walmart, Geberit, etc. Once they come to my buying range, I will deploy the rest of capital. I look forward to more fruitful discussion about my portfolio companies and also other global businesses