My 2020 and 2021 notes are at the end. Despite higher than average natural catastrophe, Markel has executed very well. Book value has grown from $803 in 2019 to $1035 in 2021(13.5% CAGR). This is largely because of their superior underwriting (combined ratio has been in very good control) and good equity performance (15.2% in 2020 and 29.6% in 2021). It always helps to look back and see how company has evolved over time. 10-year book value growth has tapered down to 10-12%, price to book has largely been between 1-1.8x. Its a steady compounder that can offer 15%+ stock price returns in USD (if bought at 1-1.2x P/B) and low volatility.

Book value compounding

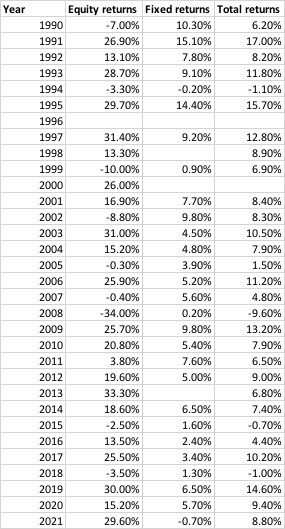

Equity and fixed market returns

2020:

- Underwriting: Combined ratio of 98%

- Equity returns: 15.2%, Fixed income returns: 5.7%, Overall: 9.4%.

- Insurance: Faced losses in pandemic related insurance policies (like tennis tournament in England, Japan Olympics, etc.). All of these correlated with each other. Despite this, combined ratio was 98%, thereby making the overall operations profitable. Have reduced exposure to natural catastrophe related businesses. Reduced expense ratio from 37.7% in 2018 to 36.0% in 2020 through better efficiency. Targeting $10bn of annual insurance premium in next 5-years (vs $6bn in 2020) with underlying profits of $1bn

- Not satisfied with stock price performance over last 5-years

- Acquired Lansing Building Products. Formal discussions begun in 2019

- During pandemic, company halted purchasing additional equity securities and liquidated a portion of portfolio to help fund opportunities in existing insurance business and to complete the Lansing acquisition. Company also stopped repurchasing shares. All this was resumed at the end of 2020

- Raised $600 million of preferred stock (callable in 2025) in May to improve balance sheet quality and fund growth opportunities

- ILS fund: Reported revenues of $316 mn and operating income of $5 million, which was after $59 million of amortization expense and $51 million of expenses from CATCo runoff operations

- Catco Enquiry update: Continued to resolve the lingering issues associated with the CATCo operations. Profitability from these operations was constrained by costs associated with winding up and settling matters related to CATCo, which obscured the underlying progress evident in the ongoing businesses

- Over last 15 years we’ve cumulatively invested $2.7 bn to acquire businesses in the Ventures group. These companies have dividended back and built up internal cash balances of $1.2 billion. Combined EBITDA from these was $367 mn in 2020

- Non-insurance business:

o Revenues of $2.8 bn

o EBITDA of $367 mn

o Several businesses in this segment are cyclical and sensitive to economic conditions (like auto sales, freight volumes, capital equipment, etc.)

2021:

- Underwriting: Combined ratio of 90% (vs 98% in 2020)

- Equity returns: 29.6%, Fixed income returns: (-) 0.7%, Overall: 8.8%. Purchased $88mn of net stocks and bought back $199mn of Markel stock

- Insurance:

o Gross premium written is $8.5bn (vs $7.2bn in 2020) with underwriting profits of $628mn (vs $128mn in 2020). With higher than average incidence of natural catastrophe, focus has been on reducing exposure to natural catastrophe insurance policies.

o On track with their 5-year plan (proposed in 2020) to reach $10bn in annual insurance premium and $1bn in underlying profits

o Hagerty (started partnership in 2013) went public in 2021 (is a specialty car insurance provider). In 2019, we purchased 25% of the company for $213mn. In December of 2021, Hagerty raised additional capital by going public. Markel invested additional $30 million and now own 23% of the company. Total market value of Hagerty is $4.7bn, valuing Markel’s stake at $1.1bn (vs invested amount of $257mn). Carrying cost on Markel’s balance sheet is $257mn (vs $1.1bn market value) - ILS (Insurance, reinsurance and insurance linked securities)

o Lowers cost of insurance for buyers by connecting them with capital providers (pension funds, endowments) who seek stability and non-correlation in their returns (especially with stock or bond markets) with acceptable rates of return.

o Acquired CATCo in 2015 which offered products with very high (and volatile) returns. This didn’t work out and winding up of operations started in 2019

o Acquired State National in 2017 which has certain ILS operations but is largely a traditional insurance operation. This acquisition has worked out wonderfully. State National, in its Program Services division, provides a suite of administrative services that any ILS provider requires to operate in the regulated industry of insurance. They produced record results and profitability in 2021, continuing to exceed expectations

o Acquired Nephila in 2018 which offered products designed to produce non-correlated returns with lower volatility than other ILS providers. In this segment, balance sheet risk is taken by their customers and Nephila earns incentive fees on achieving return expectations. Returns have been below initial expectations due to lower than expected returns. This is because of a series of larger than expected natural catastrophe losses in recent years, as a result of which they are increasing rates. Expect modest profitability in 2022 - Non-insurance business:

o Revenues of $3.6bn (vs $2.8bn)

o EBITDA of $403mn (vs $367mn)

o Acquired majority interests in Metromont which is the leading producer of precast concrete in the southeast US (used in data centers, parking garages, office buildings, multifamily residential buildings, and other facilities)

o Acquired majority interests in Buckner Heavy Lift Cranes which operates the largest domestic fleet of cranes that can lift up to 2000 tons. They are used for erecting wind turbines used to generate electricity at scale, large stadium construction, and renovation and other major construction projects

o Have cumulatively invested $3.4bn (vs $2.7bn until 2020) to acquire businesses in the Ventures group. These companies have dividended back and built up internal cash balances of $1.5bn (vs $1.2bn until 2020). Combined EBITDA from these was $403mn (vs $367mn in 2020)

Disclosure: Invested (position size here, no transactions in last 1-month)