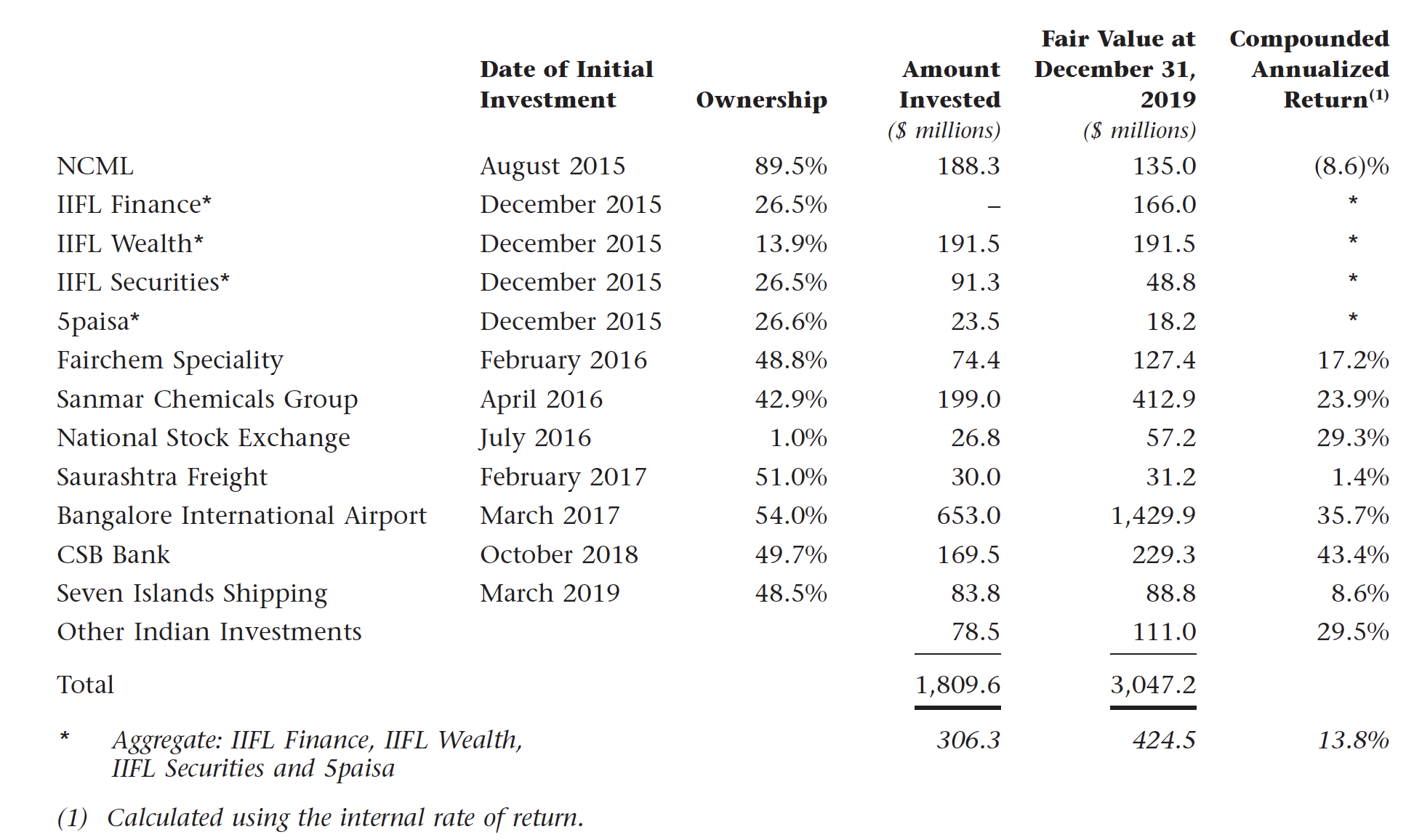

Fairfax India Holdings (Ticker: FIH.U, listed on Toronto stock exchange) is Fairfax’s investment vehicle for Indian investments. This was initiated in 2015 with an equity raise of $1.1bn at a book value of $9.5. Fairfax provided $300 mn capital (28.1% equity; 30 mn shares) that holds differential voting right shares having control of 95.1% of votes. Other investors held lower (subordinate) voting right shares (count: 76’678’879) with total share count of 106.68 mn at time of listing. They did a further equity raise of $500mn in 2017 at a share price of $11.75. Their major holdings (as on 31.12.2019) are shown below:

They invest in both listed and unlisted entities. Their largest investment is in Bangalore International airport, of which they hold 54% stake with the rest of stake with Siemens, Government of India and Government of Karnataka. Their original investment was $653mn in 2017 which has been recently valued at $1.35 bn (30.06.2020). They plan to list it by the end of 2021 at a target valuation of $3bn (implying their stake at $1.6bn).

Of their listed investments, the biggest one is in IIFL group ($22.3mn as on 30.06.2020) which was recently demerged. Other significant investments are in Fairchem Specialty (which will be de-merged into two units soon), Sanmar Chemicals group ($24mn as on 30.06.2020), CSB bank, 5Paisa, NSE, Seven Islands, etc.

They charge an advisory and investment fee of 1.5% on common shareholder equity + 0.5% of undeployed capital + 20% performance fee of increase in book value (including distributions) above simple interest of 5% increase in book value, chargeable every three years since inception in 2015. Basically, it looks like a classic hedge fund model (2 + 20). Their independent directors comprise Chris Hodgson, Alan Horn, Deepak Parekh, and Lauren Templeton.

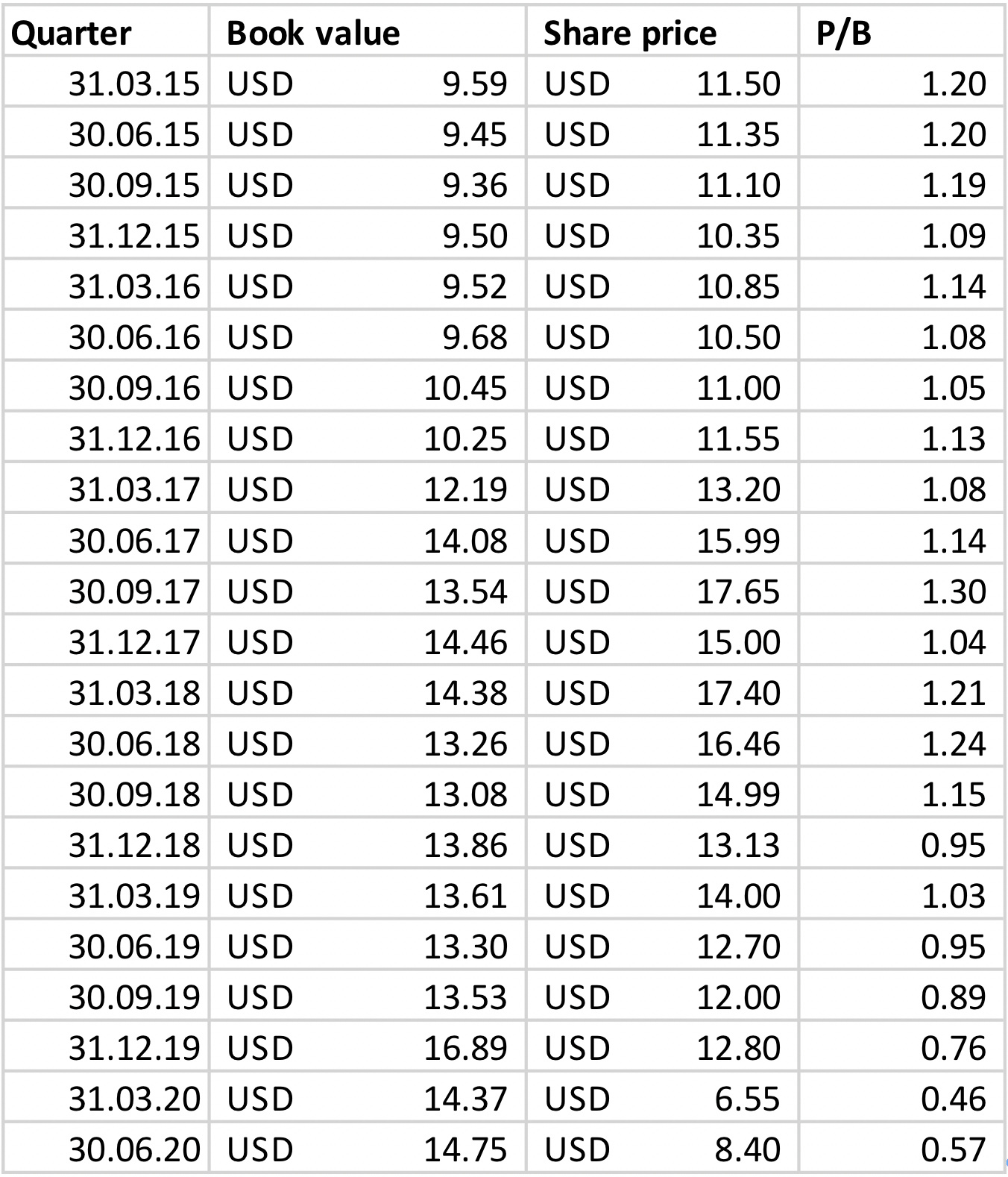

Here is how the book value has evolved over time, and also how market has valued this company.

The large increase in book value in 2019 came because of re-valuation of Bangalore airport based on a new investor buying 5% stake. However, this transaction is based on the assumption that Bangalore airport can be successfully listed at a market cap of $3bn. If that doesn’t happen the investor will get additional stake in the company. More details are available in the 2019 shareholder letter.

This fee structure can only be justified by superior execution.

Their recent investment of $84mn in Seven Islands Shipping seems to be at high multiples (1.7x P/B), which is steep for a company that operates and owns tankers.

Company announces a buyback of 3.5mn i.e. 4.7% of outstanding subordinate voting shares from open market over the next 1 year. Over the last 12 months, they have bought back 2.5mn subordinate voting shares from the open market at an average price of $9.05.

This podcast covers Fairfax Africa really well, although not Fairfax India. Also, provides good insights into insurance operations of Fairfax and how the Fairfax group has evolved over time.

Company announces their results, book value is at $15.63. At current prices of $7.6, they are trading at a 50%+ discount. Major update is the demerger of Fairchem specialty. Cash is at $185mn and company continues their buyback reducing sharecount to 150.4mn from the last year number of 152.6mn.

Thank you for putting Fairfax India into prominence here.

Maybe pertinent to point out that the relevance of book value or lack of it.

The book, which comprises publicly listed (less than a third) and private equity investments (about two thirds) is measured at fair value. Measuring private investments at fair value under IFRS that Fairfax India applies, involves substantial managerial judgement graded at various Levels up to Level 3, which has the highest levels of estimates. Fairfax applies Level 3 techniques to determine the fair value of its private investments. This ultimately flows into Equity and forms a substantial part of Book Value.

Consequently much of the Book Value is a managerial estimate.

I was a little stunned when this dawned on me. Let me repeat, Book Value of Fairfax India is a more or less a managerial estimate. For folks who have been associating Book Value with historical costs and tip toeing into Fair Value will know that they trade one accounting principle, of reliability, with another, i.e relevance. And that trade-off can be high if managerial estimates that goes into producing Fair Value is based on highly favourable assumptions that is not borne out by results, as the future ‘presents’ itself.

In case of Fairfax India such favourable assumptions are in-fact, the norm. I wrote about it in a well received article in Seeking Alpha. I should mention that my article was accepted only after I sought confirmation from Fairfax India about the accuracy of interpretation of some of their disclosures. I also wrote to the auditor PwC (no response) and found that Audit Report of Canadian Standards provided less assurance than say Singapore Audit, which sought more from auditors wrt assurance.

Sine the time I wrote this about 18 months ago, the managerial judgements used to arrive at Fair Value continue to be borne out to be highly favourable.

Investors should be meerkat vigilant about misuse of this measure of Fair Value, especially if managers benefit from favourable estimates. Fairfax which manages Fairfax India derives fee that is positively related to a higher measure of Fair Value.

I understand Fairfax has invested also in 2 general insurance companies in India namely ICICI Lombard (listed) and GoDigit Insurance. Am I missing something ?

CY20 results announced, book value is at $16.37 vs CY19 book value of $16.89. At current prices of $12.7, P/B stands at 0.77. Undeployed cash stands at $191mn and company continues their buyback reducing sharecount to 149.9mn (from CY19 sharecount of 152.6).

Here is the historical book value and corresponding P/B

Fairfax’s investee company (Seven Islands) files DRHP for IPO to raise upto 400 cr. Valuation is currently not known. Fairfax holds 48.5% stake in the company. A little bit information about Seven Islands was provided in CY19 investor letter.

Seven Islands Shipping: India’s second largest private sector tanker shipping company, owns and operates tanker shipping vehicles, Founded by Captain. Fairfax invested $84 mn to acquire 48.5% stake (8.9 EV/EBITDA, 32 P/E, 1.7 P/B). Strategy of Seven Islands is to acquire ships during downturns (hence at a sharp discount).

Disclosure: Invested (position size same as before)

Airport authority of India is planning to sell its stake in Bangalore airport. This will give a fresh valuation for Fairfax’s stake in it. Management has previously mentioned that they plan to list the airport holding company for a valuation > $3bn.

Fairfax sells their proportion of shareholding in Privi Speciality at $163mn. Fairfax had originally bought stake in Privi in 2016 at $55mn. Fairfax’s stake was valued at $138.4 mn as of 2020 end.

Fairfax will also invest $7mn in debentures issued to entities affiliated with Mahesh Babani (founder of Privi and the one who is buying shares from Fairfax). Overall it was a profitable investment for Fairfax.

On April 29, 2021 the company completed the sale of its 48.8% equity interest in Privi Speciality to certain affiliates of Mahesh P Babani and D B Rao for 12.2 billion Indian rupees ($164.8 million at current exchange rates). As a result, the company expects to record a realized gain since inception on its investment in Privi Speciality of approximately $134 million at current exchange rates, representing a 27% internal rate of return, due in large part to the visionary leadership of Mahesh, whom we want to thank and wish continued success in the future.

Fairfax India remains in strong financial health, with undeployed cash and marketable securities of approximately $210 million.

The company is continuing to buy back shares under its normal course issuer bid and in the first three months of 2021 purchased for cancellation 375,337 subordinate voting shares at a net cost of $4.1 million ($10.94 per subordinate voting share). There were 149.4 million and 152.4 million weighted average common shares outstanding during the first quarters of 2021 and 2020 respectively. At March 31, 2021 there were 119,641,497 subordinate voting shares and 30,000,000 multiple voting shares outstanding.

03-05-2021

Sanmar files for IPO to raise 3500 cr. (1500 cr. fresh issue + 2000 cr. offer for sale by Sanmar group)

Fairfax’s stake is 42.9% on a fully-diluted basis

16-06-2021

Comes up with a tender buyback offer for $105mn for a maximum of 8.4mn shares (offer price can be between $12.5-15)

Disclosure: Invested (no changes in position size)

Sanmar IPO will be 3850 cr. (1300 cr. Fresh issue + 2550 cr. offer for sale by Sanmar group)

Fairfax’s stake is 42.9% on full-dilluted basis which will probably be reduced to 23.6% (value is $438.5 mn as on June 30, 2021)

08-08-2021

Buyback tender offer concluded at $14.9 (7.047 mn shares; $105 mn; 4.7% of outstanding shares)

This will increase book value from $19.26 (June 30, 2021) to ~$20

16-09-2021

11.5% of interest in Anchorage was finally sold for $129 mn (950 cr.). This implies Bangalore airport valuations of 18970 cr. ($2.6 bn)

Invests 488 cr. ($66mn) for 67% equity stake in Maxop Engineering in 2 transactions. In 1st transaction (to be completed by Q4CY2021; completed on 30.11.2021), will invest 222 cr. for 51% stake and then 266 cr. for further 16% stake (to be completed by H2CY2022).

Maxop is a precision aluminum die casting and machining solution provider for aluminum die casting components used by the automotive and industrial sectors, with customers in India, Asia, North America and Europe. Maxop is based in New Delhi and operates with four plants in Manesar, Haryana and two plants in Jaipur, Rajasthan.

26-01-2022

Invested 245 cr. (~$33mn) for 70% stake in Jaynix Engineering Private Limited

Jaynix is a manufacturing company engaged in production of non-ferrous electrical connectors and electrical assemblies and is a critical Tier 1 supplier to major electrical original equipment manufacturers in North America and Europe

Jaynix is based in Gujarat and operates with three plants, one in Vadodara, Gujarat and two in Nashik, Maharashtra

Family owned by Diwakar family and will be operated by them only

There seems to be some interest in Fairfax India in the past few months. I am sharing a couple of relevant articles that summarizes the investment thesis in Fairfax India

This article does a very good job in plotting out longer term nos of Bangalore airport and concludes that Fairfax’s valuation of the airport is on the conservative side.

Another good article on Fairfax

Disclosure: Invested (position size here, no transactions in last-30 days)

Here are my notes from their 2022 shareholder letter

Book value: $19.11

Have bought back 15.1 million shares for $194.4 million (average price of $12.84 per share) over last four years. Bought back 3 million shares for $35.6 million (average price of @12/share) in 2022

In the current 3 year block (ending 2023), have accrued performance fee of $41.5mn

Investments:

Fairchem Organics: In November 2021, Fairfax India sold 14% of Fairchem for $45.6 million, recouping more than its entire investment while still owning 53% of Fairchem, valued at $111.1 million on December 31, 2022, down significantly from the $155.0 a year earlier

IIFL Wealth management: In November 2022 Fairfax India sold a 9.8% (of 13.6% held) shareholding in IIFL Wealth to Bain Capital for gross proceeds of $171.8 million, realizing a net gain of $54.0 million. Fairfax India sold an additional 1.3% shareholding in IIFL Wealth during December 2022 for additional proceeds of approximately $25.6 million, resulting in a realized gain of $9.8 million. At year-end Fairfax India’s share ownership in IIFL Wealth was 2.5%

Bangalore airport:

Once Anchorage is listed, proportion of publicly listed investments will increase from 39.2% to 79.8%

Inaugurated Terminal 2 (T2) spanning 255,661 square meter

Domestic passenger traffic was at 24.4 million passengers (annual run-rate) and exceeded pre-pandemic levels in December 2022

International traffic was at an annual rate of 3.1 million passengers (88% of pre-pandemic levels) in December 2022.

Valuation of Fairfax India’s interest in BIAL decreased to $1.2 billion in 2022 from $1.4 billion in 2021 due to unrealized foreign currency translation losses, implying an equity value of approximately $2.3 billion for the whole company

Revenue were $200.5 million, EBITDA was $119.9 million (101% of pre-pandemic levels), Loss after tax reduced to $6.0 million (vs profit of $53.8 million in 2019)

Disclosure: Invested (position size here, no transactions in last-30 days)

The substance of the report is that FFH enters into transactions and abuses accounting standards to show paper gains, often while incurring cash losses. Fairfax India has also engaged in similar gimmickry (which I highlighted in my piece in Seeking Alpha and posted above).

Muddy Waters also highlights some Indian transactions.

The report educates creative ways by which how accounting can be manipulated to keep numbers going and very helpful for Security Analysts going beyond what management say and look for numbers.