Kolte management is guiding for a bumper Q4 quarter, with 800-900 cr. reported revenue, 30-40% gross margin, and 20-25% EBITDA margin. Lets see what they end up delivering. Concall notes below

FY23Q3 concall

Out of priority launch pipeline of 7’700 cr. (13 projects), have launched 2’000 cr. Remainder landbank has development potential of 15’000 cr. (11’000 is from Life Republic)

Planning to launch 4000 cr. of priority launch pipeline in Q4. There maybe some spillover to Q1FY24. Require 8-12% of upfront investment in terms of sales potential. Cashflows from Marubeni will be utilized for this investment

Baner project: Have acquired an adjacent land parcel which has improved economic outcome. Planning to launch at 9000 realizations in March 2023 vs 7500-7800 earlier

Life Republic: Average realizations have increased from 5200-5400 to 5900

Q3 losses were because of delivery of 2 projects in Pune (which were lower gross margin and contributed 31 cr. gross profits and were insufficient to cover overheads; Western Avenue and Green Olive). All costs related to these 2 projects have been booked this quarter

Launched premium Row houses in Life Republic and received overwhelming response. Price bracket has widened from 30-80 lacs to 30-250 lacs

Q4 revenue recognition will be 800-900 cr. bringing reported revenue in FY23 to 1600-1700 cr. Gross margin: 30-40%, EBITDA margin: 20-25%

Deliveries in FY23 + FY24 will be 3000 cr. (so 1300-1400 cr. of revenues in FY24)

OCs: Have received for 2.7mn sq. ft in 9M FY23, 60% of these were received in December 2022 and will be recognized in March 2023 quarter. After OC receival, revenues are recognized in 30-45 days depending on agreement with customers

Expect higher EBITDA margins in FY23 vs FY22

Expect 25-30% pre-sales growth in FY24

Referral sales have improved from 3-5% earlier to 7-9% in FY22 and further to 15% in 9MFY23

Disclosure: Invested (position size here, no transactions in last-30 days)

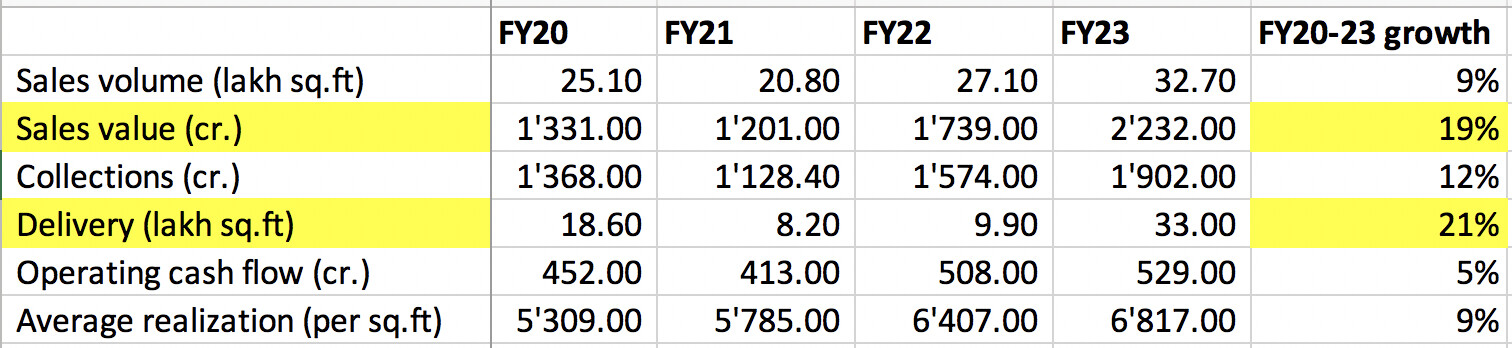

FY23 ended as a very good year with presales growing by 28%. One place where they lacked was in new launches, which was much lower than earlier guided and reported margins (again much lower than previously guided). However, since FY20 company has scaled up very well, with presales growing at 19% and company consistently generating very high cashflows (500 cr.+ in last 2 years). Realizations have also grown at 9% CAGR over this period.

Pre-sales increased by 28% to 2232 cr. (50% came from new launches), volumes increased by 21% to 3.27 mn sq.ft and collections increased by 21% to 1902 cr.

Delivered 3.3 mn sq.ft (exceeding guidance of 3mn sq.ft) but EBITDA margins were sharply lower at 13% (vs guidance of 25%). Lower margins are because revenues that are getting recognized are on a 5300-5400 realization (older projects) whereas marketing costs that are reflected in P&L statement are getting incurred on current projects which are being sold at 6800-7000 cr./sq.ft

Launched 3.05mn sq.ft of projects (2120 cr.) which was much lower than guidance of 4000 cr. in FY23

FY24 guidance: Pre-sales of 2,800 cr. + deliveries of 3mn+ sq.ft (1500-1700 cr.) + launch 7.39 mn sq.ft (5,265 cr.) + acquire projects with topline potential of 8,000 cr. (5000 in Pune + 2000 in Mumbai + 1000 in Bangalore)

In May 2023, acquired two projects each in Pune and Mumbai with top-line potential of 2500 cr.

Sustenance Inventory: 1700-1800 cr.; 30-40% of FY23 sales will come from sustenance inventory (~1000 cr.) and 60-65% from new launches

Received 206.5 cr. from Marubeni Corporation towards investment in the Pimple Nilakh project in April 2023

Business development: Net debt is 110 cr., need 500-550 cr. for current business development which they want to fund via internal accruals

Life Republic contribution in pre-sales was 1.76 mn. sq. ft (1070 cr. sales). Currently RERA launch inventory is ~1000 cr. in township. Price realization has improved to 5700-5800/sq.ft

Strategy in Life Republic during FY23 was to do high volumes, now with that strategy being successful pivoting to selling at higher realizations in Life Republic

Have seen 5-10% higher realization across projects

Margins & IRR: Outright projects (30-40% gross margins, 20-25% EBITDA margins), JV & Redevelopment (focus on IRR of 30%+)

Have been seeing higher demand in higher value housing rather than low and affordable housing

Customer profile: IT segment for entry level, beyond 1cr. inventory its spread across industries

Disclosure: Invested (position size here, no transactions in last-30 days)

“Kolte-Patil acquires two society redevelopment

projects in Mumbai Metropolitan Region with estimated saleable area of 4.8 lakh sq. ft. and topline

potential of Rs. 950 crore. These projects located in Goregaon will further strengthen the

Company’s presence in MMR.”

In April-May 2023, the Company announced acquisition of four projects, two in Pune and two in

Mumbai, with the total development potential of ~2.6 million sq. ft. and topline potential of Rs.

2,500 crore. With the two new additions in MMR, the new business development deals now aggregate

a topline potential of ~Rs 3,450 crore. The company is continuously assessing multiple business

development and expansion prospects in its targeted markets through innovative, capital-efficient

deals.

Some Observations : 1.Net D/E is down - 0.11

2.Pre-Sales almost doubled in last two years

3.Realizatoins are improving

4.New and Sizeble projects acquistions in Pune and MMR

5.Guidance of 25-30% presales for next 2 years…

6.Life Republic is at inflexion point interms of pricing…

Another very quarter from Kolte, with pre-sales exceeding 700 cr. and their new business development plans going well. Concall notes below

FY24Q1

Quarterly pre-sales have been maintained at 700 cr.+ levels

Maintain guidance of 2800 cr. pre-sales in FY24 and 3500 cr. in FY25. Expect deliveries of 1700 cr.+ in FY24

Business development: acquired projects worth 3450 cr. (out of planned 8000 cr.)

New project launches accounted for 43% of pre-sales in Q1FY24

New project launches was ~2000 cr. (guidance: 5200 cr. in FY24)

24k Baner project was launched in June (800 cr. potential). Within the launch week, sold 50% of inventory which was available on sale (sold 242 cr. in Q1FY24). There is strong demand in premium and luxury housing

Have delivered 5 24k projects so far, will launch 5 more in FY24. EBITDA margins are 4-5% higher vs MIG housing

Life Republic will cross 1.5mn+ sq.ft pre-sales in FY24 (vs 1.7 mn sq.ft in FY23) at higher realizations

Sold 200 units in R22 on a weekend (launched in July 2023). Demand is very strong in Life Republic

Currently evaluating 10 redevelopment projects in Mumbai, a couple of them are in advanced stage

Doing 20%+ EBITDA margins on a project level, corporate level will be lower due to investments in new projects

Equa / Wagholi project: waiting for some further approvals, sales velocity is not a problem

Business development costs will be higher than previously guided 500-550 cr. because they acquired JV stake in Baner project. Confident of funding most of this expansion from internal accruals

Life Republic surrounding areas is a no development zone, their FSI gives them advantage to develop a township

Ready unsold inventory is very low (20-30 cr.)

Disclosure: Invested (position size here, no transactions in last-30 days)

Kolte-Patil enters into second agreement with Marubeni Corporation (Japan) for Rs. 110.9 crore.

As a part of this agreement, Marubeni Corporation will invest Rs. 110.90 crore in the Alora project, entitling them to a total saleable area of 59,949 square feet in the project. The Alora project was launched in February 2023 and has a total development potential of ~1.3 lakh sq. ft.

Company maintains their presales runrate, however they weren’t able to launch any new project in Q2 as a result of which most sales came from Life Republic. On reported numbers, they are guiding for 1500 cr. revenues in FY24 and 2000 cr. in FY25. Concall notes below

FY24Q2

No new launches in Q2, as a result sales only came from sustenance inventory (462 cr. from Life Republic out of 632 cr. in Q2)

Few projects saw realization drop (24K Altura – 8965 vs 9105 in Q1, Little Earth – Kiwale – 4843 vs 4979 in Q1). Is this a cause for worry?

Ownership in Life Republic reached 100% from 95% post acquisition of 5% stake from minority holders in October 2023, will also need to make some payment to ICICI (125 cr. total payment and then Life Republic township will be 100% owned by them)

24k projects: have launched 3 (out of 5 planned in FY24). Have sold out 60%, 20% (in pre-launch stage), and 25% (row house) in these

Confident of delivering 3mn+ sq.ft in FY24 and book revenues of 1500 cr. (& 2000 cr. in FY25)

Doing 25-30% EBITDA margin at project level in currently sold projects. This will likely reflect in numbers from FY26. In low rise projects, margins are 40%+

Construction costs have been locked for next 4-8 quarters for multiple raw materials due to long term construction agreements with vendors

Exceptional item: Impairment of goodwill (12.4 cr.) on account of merger a subsidiary earlier + reversal of land transaction in Life Republic (6.78 cr.)

Disclosure: Invested (position size here, sold few shares in last-30 days)

Company sold a lot of premium projects (24k) which has caused a huge jump in realizations. Reported nos will be subdued until FY26, and management expects current projects to start getting recognized in FY27/28 when the real economics should be reflected on P&L statement. Concall notes below

FY24Q3

Volume declined by (-13%) in Q3, realization increased by 20% due to higher sales of 24k projects. Price realization has increased by 5-15% across projects

In next 2 project launches in Life Republic, realizations will be 6,500/sq.ft (vs 4,800/sq.ft 2 years back)

Will reach 20-25% EBITDA margins by Q4FY26

Construction scaleup will not be a problem, they were earlier doing 2.5-3mn sq.ft which has now increased to 4mn sq.ft. Can handle 1.5-2x of earlier volumes (material procurement is centralized, labor for construction is outsourced)

Life Republic minority stake buyout (stake increase from 95% to 100%) - paid 60 cr.

In low margin projects, gross margin is 25%. For projects sold in last 2-years, are making 25-27% EBITDA margin

Make 18-20% EBITDA margins in redevelopment projects but much higher IRRs

9MFY24

Business development of 4,000 cr. (guidance of 8,000 cr.)

Launched 3,200 cr. projects (guidance of 5,200 cr.)

Presales of 2,080 cr. (guidance of 2,800 cr.)

Will launch 1,800 cr. (2 mn sq.ft) of projects in Q4FY24 of which Life Republic will be 1,000 cr.

Will launch 7,000 cr. projects in FY25 (8mn sq.ft)

Business development of 3,000-4,000 cr. over next 3-4 months and 8,000-10,000 cr. in FY25

Reported revenues guidance: 1,500 crore in FY24, 1,600-1,700 cr. in FY25 & FY26

FY25 guidance: Presales of 3,500 cr. & launches of 7,000 cr.

Disclosure: Invested (position size here, no transactions in last-30 days)

Kolte came with horrific set of nos, with margin misses coming from even recently acquired projects. Management keeps giving very bullish guidances and are now guiding for 13,500 cr. presales over next 3 years, when their FY24 presales was only 2800 cr. Their execution in terms of growth while preserving balance sheet has been decent during the industry downturn but they are not really showing good nos during the upcycle. Nos below

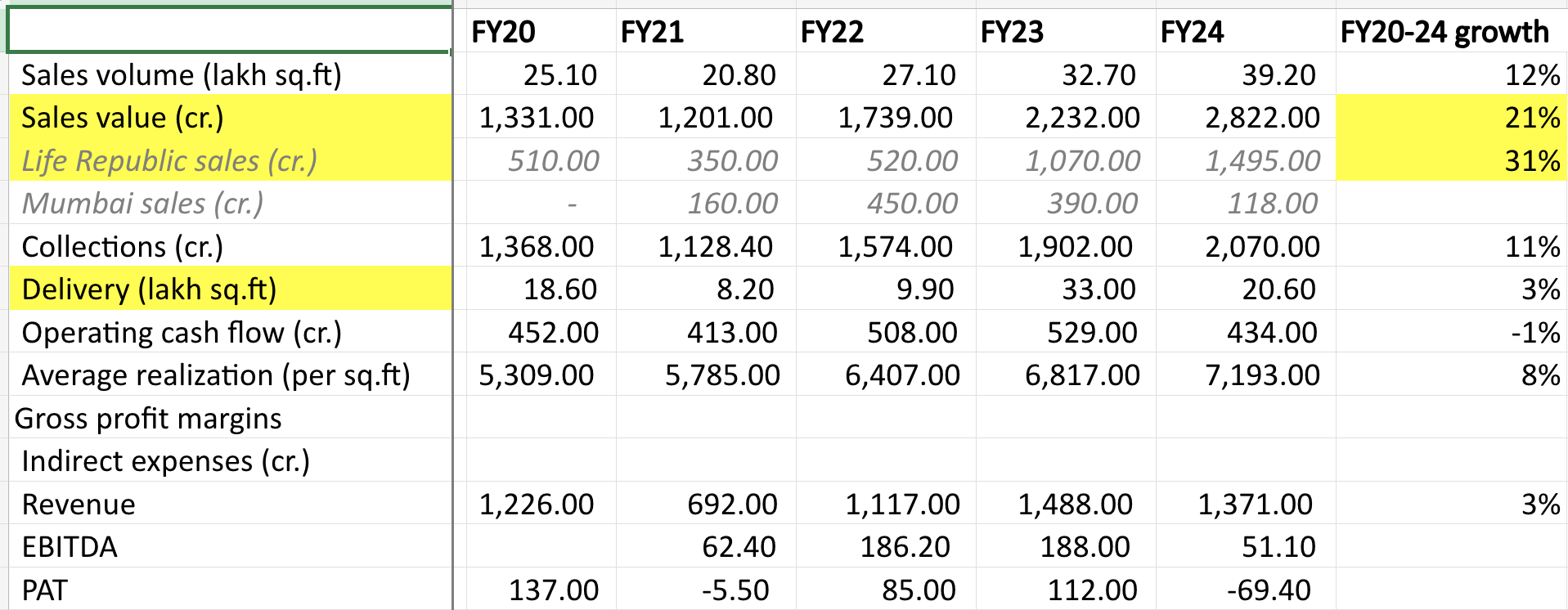

2,822 cr. presales value in FY24 (guidance of 2,800 cr.) – 20% volume growth + 6% realization growth

Acquired projects worth 6,095 cr. including 2,100 cr. in Life Republic (guidance of 8,000 cr.)

Launched 3,816 cr. projects (guidance of 5,265 cr.). Missed timely launches in Wagholi (400 cr.) and NIBM (360 cr.) which will get launched in Q1/Q2 FY25. Strategically delayed a premium project in Life Republic (1300 cr.) as they wanted to reach a volume run rate before launching it. They plan to launch it in FY25. H1FY25 will see 3,500 cr. project launches which will be driven by Pune, Mumbai launches will happen in H2FY25

Delivered 2.06 mn sq.ft (guidance of 3mn+ sq.ft)

Guidance for FY25

Expect 25% sales CAGR from FY24-26 + 13,500 cr. cumulative presales from FY25-27

Acquire projects with topline potential of 8,000 cr. (5,000 in Pune + 2,000 in Mumbai + 1,000 in Bangalore)

Launch 8.95 mn sq.ft (8010 cr.)

Deliveries: 2000 cr. with early teens EBITDA

Sold 1,800 cr. of 3,800 cr. inventory launched in FY24 (lower than historical runrate of 50%+)

Potential sales from Life Republic is 12,000 cr.

Kiwale was a stalled project with inventory having been sold by earlier developer at very low realizations. Their delivery has also adversely impacted their margins (when they had acquired Kiwale in FY23Q1 they had said “Kiwale acquisition (~120 cr.) gives revenue visibility of 1400 cr. (with 24-26% EBITDA margins) with all regulatory approvals in place.”

Margins were lower because delivered projects in Life Republic were lower margin (average realization of 5,100 vs realizations of 6,400 in FY24). Life Republic projects had 25% gross margins in FY24, other projects had 11-18% gross margins. Overall gross margins was 22% for FY24. EBITDA margins will start improving from FY25 (early teens) and high margin projects will start getting delivered in FY26 (late teens)

Life Republic: construction costs were 2500/sq.ft, land and utility at 1000/sq.ft and realizations delivered was 5100/sq.ft

Pune real estate market is ~80,000 cr.; northwest Pune is 20-25,000 cr. and Kolte has 12% market share in northwest Pune. But in rest of Pune, they have less than 1% market share

Focus now is really to increase realizations, did 900 cr. of presales in 24K in FY24

They also calculate like-to-like margins, presales in FY23 generated 18-19% margins and in FY24 generated 26% margins

Projects launched after October-November 2022 have good margins. Before that there were higher contracting costs

Goodwill due to merger of a subsidiary was impaired by 23.46 cr.

Anticipate 100 cr. annual finance costs in next 3-years

Announced dividend of Rs. 4

Disclosure: Invested (position size here, no transactions in last-30 days)

Another bad set from Kolte, felt management was very elusive in most of their answers. Maintain their guidances, concall notes below.

FY25Q1

Expects delivery of 1800-1900 cr . with early teen EBITDA margins in FY25

Launched 0.6mn sq.ft inventory worth 400 cr. at Life Republic. After Q1, have launched 1.4mn sq.ft in Pune, taking YTD launches to 1500 cr. (further launches of 6500 cr. in FY25)

Life Republic quarterly revenue run rate declined from 370 cr. in FY24 to 300 cr. in Q1. Mostly sustenance inventory driven

Spent 145 cr. on land and approval

Presales scaleup is expected to happen from Q3

Disclosure: Invested (no transactions in last-30 days)

@harsh.beria93 : What’s the best way to judge valuation of RE companies in your opinion since their profits are lumpy due to accounting imposed revenue recognition methodology?

20 Aug: I see that you have mentioned in one of the earlier posts that Mkt Cap/Sales or Pre-Sales at peak vs trough could be used as a reference for valuation. That answers the above question.

What keeps you hopeful to stay invested in this business? Management keeps overpromising and underachieving year after year.