Sales contribution outside Pune (Mumbai + Bangalore) ~ 35%

Have 11 priority launches (6.2 mn sq.ft saleable area, 5000 cr. potential topline, 8000-8500 / sq.ft realizations; most of these will be launched in FY22 with some spillover to Q1FY23)

Life republic portfolio realization has gone up from 4900/sq.ft to 5200/sq.ft. For premium projects in Mumbai, realizations have gone up by 2-4%

Will do >2.5mn sq.ft in FY22 and increase over that in FY23

9 mn sq.ft of current undergoing projects will get delivered in the next 3 years (expected sales ~ 5000 cr., EBITDA margins ~ 20-25% and PAT ~ 10-15%). This will be almost evenly spread over the 3-years

hello harsh , if possible pls solve my query for real estate,which company had cumilative EBITA exceeds the mkt cap, pre tax cash flow is equal to mkt cap, thanks in advance.

I think you are referring to Samit Vartak’s Bloomberg Quint interview where he says, buy a Developer when the next 5 years’ cumulative EBITDA is equal to current market cap. Kolte Patil has the ability to be one such Developer. Not 5 years but 7 years definitely.

According to sources, Samit is invested in Indiabulls RE. I haven’t studied them closely to project numbers. Few other developers can do it too. The problem is the recent rally. So at current prices, next 5 years cumulative EBITDA might not be equal to current market cap but definitely possible in 7 years. 5 or 7 years doesn’t matter. Its just a thumb rule. The bigger question is, will the current demand and pre-sales sustain? While large developers will definitely gain market share due to consolidation, will the prices and pre-sales go up? Have to be dynamic and keep watching quarterly numbers.

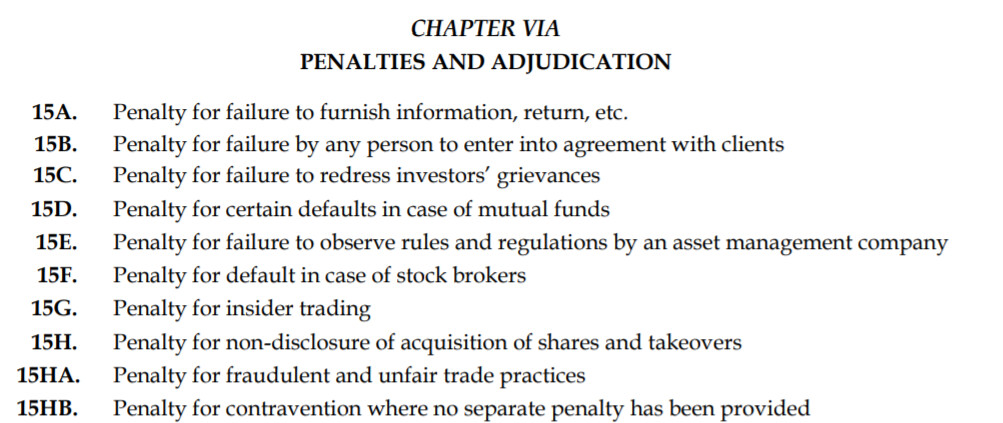

Kolte Patil received show cause notice from SEBI under rule 4(1) of SEBI (Procedure for Holding Inquiry and Imposing Penalties by Adjudicating Officer) Rules, 1995.

This can be due to the following reasons provided under Chapter VIA of Securities and Exchange Board of India Act, 1992:

Highest quarterly sales value in last seven years in Q3 FY22

They expect to this year as their best ever in volume year.

Guidance for next FY is Rs.2000Cr+ topline (3+ million sq. ft)

Will try to maintain margins around EBITDA 20-25% and PAT around 13%.

Target of 10mm sq. ft out of which 8mm will be in Pune. This leads to 6000-7000cr topline.

1238cr sales currently

Future potential:

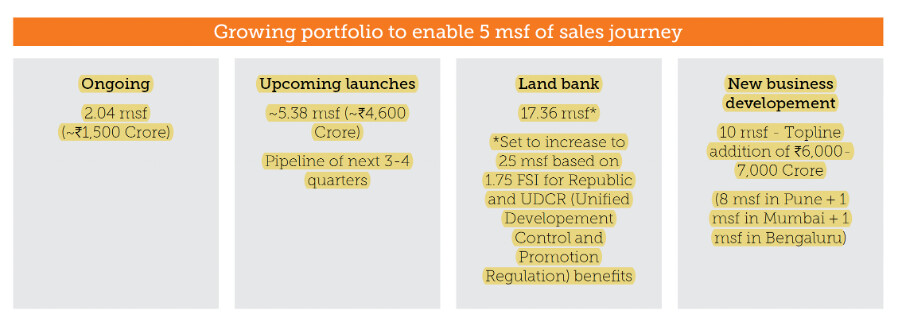

5.38 msf of saleable area

Rs.4,600 crore of topline potential

Revenue mix: Out side Pune 31%: Mumbai 26% - 5% Bangalore

Going forward, project size will be 300-800cr with ticket size 1.5-3.5cr.

Evaluating 30 mm sq ft which is in mid-advance stage but this can’t be taken as guidance because due diligence is still going on.

Out of this Bangalore 2.5-3.5 mm sq ft

Their plan is to cater to smaller categories to not compete with larger players.

Next few month there can be interesting announcement

Management repeatedly staying “hoping to announce something soon”

Created platform with Planet Smart City to develop 15,000 housing units (Area is 2 lakh sq ft.): There will be better realization due to partnership with Planet as they will bring in technology.

80% of amount will be put in by planet

DMA deals are going to be small portion like 3-4 deals going forward.

Have strengthen JD team in Mumbai: Identified few mico-market where they have strong presence.

There are few ready to launch deals because earlier dealer could not complete.

SEBI Notice:

It was not mandatory but they still disclosed it.

A technical violation and they have appointed Khaitan & Co.

Nothing to do with insider trading which comes under different notice.

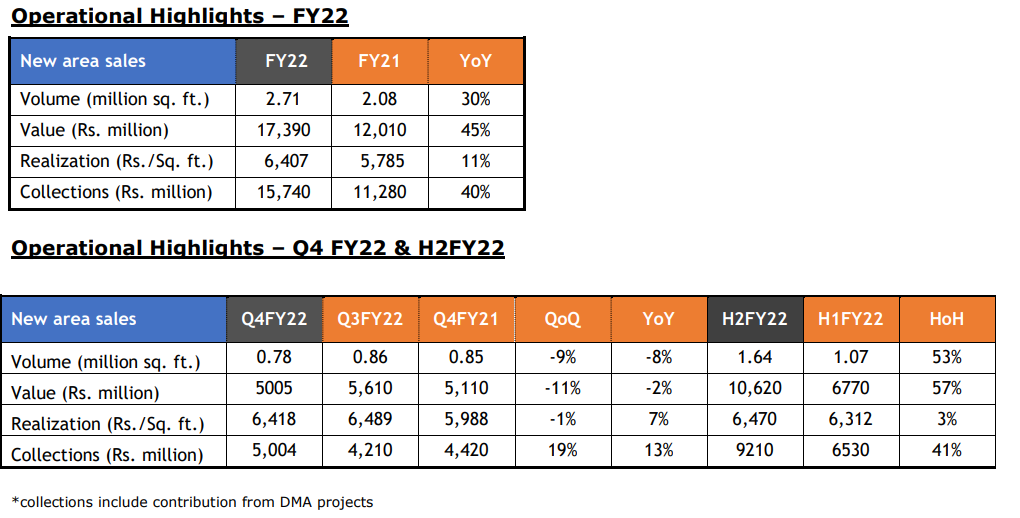

Collection is the highest in the 3 decades of Kolte Patil.

Guidance: “We now look forward to expand on the platform of these achievements; our objective would be to deliver 25-30% sales value growth in FY23. We have a solid balance sheet position and remain well placed to aggressively pursue business development initiatives in FY23 and expect to conclude deals with a cumulative top line of Rs.7,000. Further, in FY23 we are looking to launch projects in the pipeline that currently include saleable area of 5.4 million square feet with aggregate top line potential of Rs.4,600 crore.”

Confident of delivering 3 mm sq ft during FY23. Leading to Rs.1800+cr of revenue with EBITDA margins of 25%. (Today the market cap is around 1800crs)

Mumbai target of crossing Rs.650cr. IRR target of more than 25% of redevelopment portfolio. Margin is 22-25%

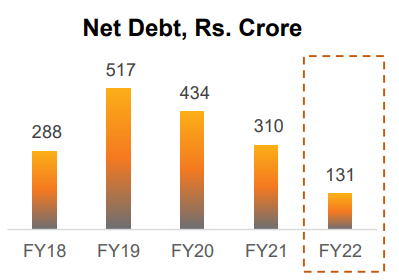

Debt to equity at 0.14 time

“We reduced Net Debt by Rs. 179 crore during FY22 and by Rs. 41 crore during Q4FY22. This was the third consecutive year of Net Debt reduction, with Rs. 386 crore being reduced in last three years. As on March 31, 2022 Net Debt/Equity stood at 0.14x.”

Current debt level is at 20 days of collection of business.

14-15% price hike in Pune Life Republic. Further increased, 5-7% in other projects as well. (On average 5% price hike)

Management believes there is possibility of settling down of the cost further.

They were able to sell the Mumbai project within one month even after the price hike.

Confident of launching projects worth 4,000cr in FY23. This year it was 1,000cr.

70% from Pune and 30% from Mumbai and Bangalore

7 non-binging sheet are present where commercial discussions has been closed but not 100% guarantee that it will god through as legal problems can still come in.

Q: Any change in customer behavior due to increase in interest rate?

There is good growth in the industries as well where the end customer would also be receiving high increase salary but it can be impacted if it increasing by 100 basis points.

They are not investors they are end users.

If required company is open to provide incentive to meet growth target but have not done yet rather increasing prices.

Contribution from Life republic project contributed 40% last year to now 31% next year guidance of 24-25%.

Reason being more projects being sold from other project and not slowing down Life Republic.

Evaluating Plotting projects of townships in Pune, already one first such project this year.

Less number of branded players in this segment.

Management is not seeing any slowdown in the real sector.

There has been multiple hiring in mid to high level management. New management team has joined this year like a position of COO. Plus, building a strategy team.

Booking:

Affordable: First 3 months and 50% is sold by that time then 100% by the time registration certificate is received

Premium: First 6 months 30-40%. 20% at finishing.

63% of inventory of last year has been sold.

In Mumbai customer are coming to them even at better terms for the developer showing brand recall.

P.S: Please notify if there are any errors in the notes as audio was not clear during the call.

Thanks for adding your notes, its very comprehensive. I will add a few data points in terms of long term sales cyclicality and the kind of Mcap Kolte got in previous cycles.

Reported sales 2008 peak sales ~ 421 cr.

2010 low sales ~ 148 cr. (-65% from peak) 2014 peak sales ~ 764 cr. (416% from low, 81% from peak)

2015 low sales ~ 697 cr. (-9% from peak, 371% from low) 2018 peak sales ~ 1403 cr. (101% from low, 84% from peak)

2021 low sales ~ 692 cr. (-51% from peak, 0% from low)

Share prices:

2008 peak: 272

2009 low: 18.7 (-93% from peak)

2015 peak: 238.75 (1177% from low, -12% from peak), market cap: 1’812 cr.

2016 low: 78.4 (-67% from peak, 319% from low), market cap: 595 cr.

2018 peak: 404.7 (416% from low, 70% from peak) , market cap: 3’072 cr.

2020 low: 103 (-75% from peak, 31% from low) , market cap: 782 cr.

Market cap / sales 2015 peak: 2.37 (peak market cap 2015 / peak sales 2014) 2018 peak: 2.19 (peak market cap 2018 / peak sales 2018)

2016 low: 0.85 (low market cap 2016 / low sales 2015)

2020 low: 1.13 (low market cap 2020 / low sales 2021)

In terms of Mcap/sales Kolte got 2.2x in 2015 and 2018 cycles. If we just look at projected FY23 deliveries, it should be around 1800 cr. (3 mn sq.ft * 6000/sq.ft). With 25% EBITDA margins, current EV/EBITDA ~ 4.5x. On a EV/pre-sales number, Kolte is currently trading at <1x. This is in stark contrast to previous upcycles where they traded at >2x sales.

Summary: Business is in an upcycle and valuations are towards the 2016 and 2020 lows. I think its an interesting opportunity if management executes. In the past, they have overguided and underachieved.

Disclosure: Invested (position size here, bought shares in last-30 days)

FY22 result is reflection IT boom and salary hikes. Is this going to repeat in FY23? I doubt.

Pune real-estate is driven by IT. Looking at current and near future bearish scenario in IT, layoffs fear, interest rate hike, prices hike in real-estate, etc. will definitely impact real-estate growth in city/region where IT drives growth.

Hence, management’s commentary should be taken with pinch of salt !!

Have been able to take price hike of 5-10% in last year, in last 3-months, 2-4% price hike across portfolio. In Q2 planned launches, prices will be at 5% premium to initial planed prices (when project was being finalized)

Kolte’s growth in their micro markets has mainly been due to increased ITES demand

Pre-sales target for FY23 ~ 2’300 cr.

Will have 10mn sq.ft of business development and 5’000 cr. launches in FY23

Disclosure: Invested (position size here, bought shares in last-30 days)

Has 9.1 mn sq.ft under execution (sold and unsold) vs ~9.13 mn sq.ft in FY21, 40 cr. of RTM inventory (vs 170 cr. in FY21)

Realizations increased by 11% to 6’407 due to increased contribution from Mumbai and higher realizations from Pune and Bangalore

Mumbai + Bangalore sales contribution ~32% of FY22 sales (vs 25% in FY21)

Pre-sales target of 8’000 - 9’000 cr. for next 3-years with 40-45% contribution from Bangalore and Mumbai by FY25. Intend to launch 10 projects with revenue potential of 4’600 cr.

FY23 project delivery will be 3mn sq.ft

New business development of 10 msf (8 in Pune + rest in Mumbai and Bengaluru), projected topline is 6’000-7’000 cr.

Came up with propositions like home financing and customization to drive sales

Mumbai:

o Mumbai portfolio reported sales value of 450 cr. (vs 180cr. in FY21)

o Evara, Verve and Vaayu projects were virtually liquidated

o 10 redevelopment projects signed (2 delivered + 3 ongoing + 2 under approval to be launched in Q1FY23)

o Planned launches of Golden Pebbles and Sukh Niwas. Total 3 launches planned in FY23

o Intends to unlock redevelopment deals that can contribute ~0.84 Mn sq. ft with an estimated revenue of 1,500 cr.

o Will execute outright/structured and joint venture or joint development deals with project revenue sizes of 300-800 cr., with apartment value of 1.5-3.5 cr. and an average saleable realization of 15-17,000 per square feet

o Will focus on large redevelopment properties that present possibility of generating at least 50 cr. in profit before tax.

Net debt declined to 131 cr. (vs 310 cr. in FY21)

Created 5 strategic business units (2 in Mumbai, 2 in Pune and 1 in Bengaluru)

Introduced net promoter score metric to understand brand strength in customer eyes

Partnerships:

o Onboarded Planet Smart City as a private equity partner in Three Jewels project

Brands:

o Kolte-Patil (addressing the mid-priced and affordable residential segment)

o 24K (addressing the premium luxury segment).

Number of shareholder: 49’593 (vs 37’665 in FY21)

Share price: low (206.2), high (360)

Number of employees: 567 (vs 558 in FY21), median remuneration: 5.88 lakhs vs 5.29 lakhs in FY21

CSR: Spent 38 lakhs (74 lakhs unspent)

Auditor remuneration: 1.33 cr. (vs 1.27 cr. in FY21)

Contingent liability: 317.92 cr. (vs 294.92 cr. in FY21). 245 cr. is corporate guarantee and rest are court or tax cases

Management in concall said around 3.5 mn sq ft to be delivered this year and same run rate to be maintained in next 2 years also. 1600-1900 cr. sales guidance for this year with 24-25% ebidta and 12-14% PAT margin guidance. For Fy24 2000 cr+ sales guided.

Kolte has been delayed in execution of their business development plan. They are maintaining pre-sales guidance of 2200+ cr. and deliveries of 1600-1800 cr. in FY23. It seems most of the nos will come in Q4. Notes from concall below.

FY23Q2 concall

Out of 13 priority projects, 11 have got environmental approval and are stuck in some stage of local approvals

Guiding for 4000 cr. launches in H2FY23. Expect 1200 cr. of pre-sales from new projects + 300 cr. from sustenance inventory in H2FY23

Q4 will be higher in terms of pre-sales than Q3

For mid housing inventory, they sell 40-60% in 6-months after launch. For premium or luxury housing, they sell 30-40% in 6-months after launch

Life Republic: prices have increased by 7-10%

Thane project: Underwritten at 7500 and will launch at 8500, but actual cost impact is only 100-150. So margins should improve

The idea of selling investments and land bank through planet city is to improve project IRRs as Kolte gets cashflows earlier in the cycle

Guidance of deliveries of 1300-1500 cr. in H2FY23. Some deliveries will be in later part of Q3 and large part of recognition will be in Q4

Disclosure: Invested (position size here, no transactions in last-30 days)