Eris Lifesciences -

Q3 FY 24 concall highlights -

Current rank in IPM @ 21st vs 29th in Mar 18

Make share in Diabetes @ 5 pc, in Vit/Minerals @ 2.5 pc

Last 6 yrs avg GMs > 80 pc, EBITDA margins > 35 pc

Therapy wise sales breakdown -

Diabetes - 28 pc

Cardio - 19 pc

Vit/Min - 16 pc

Derma - 14 pc

CNS - 6 pc

Women’s health -5 pc

Nephro - 3 pc

Others - 8 pc

Q3 financial outcomes -

Sales - 486 vs 423 cr

EBITDA - 176 vs 137 cr ( margins @ 36 vs 32 pc )

PAT - 116 vs 107 cr ( due higher amortisation, interest costs )

Vision 2029 - to hit a annual revenue run rate of Rs 5000 cr / yr

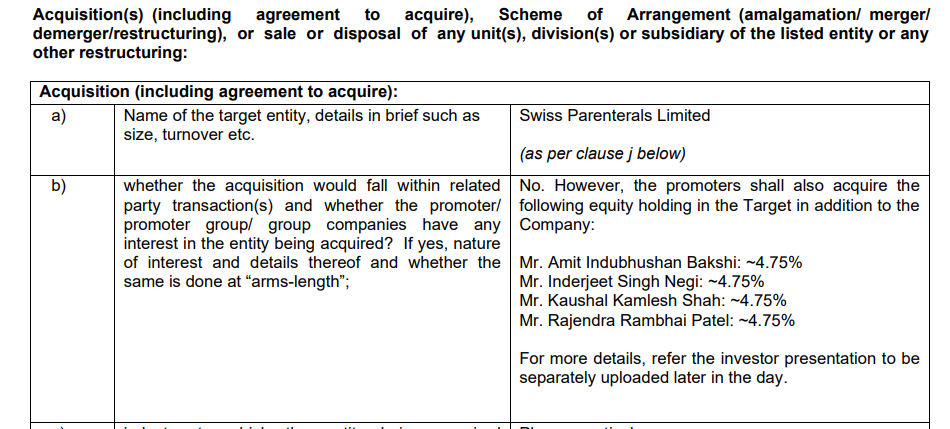

Acquired SWISS PARENTERALS in Q3. Its a dossier driven - generic and speciality Injectables business focussed on RoW Mkts ( Africa, LATAM, ME, Asia Pacific ). They own 02 manufacturing plants in Gujarat. Swiss Parenterals currently does a topline of 250 cr with 25 pc PAT margins. Eris has bought 51 pc stake for 637 cr in the company. An additional 19 pc stake shall be acquired separately by Eris promoter group for 237 cr

It also offers Eris an ideal platform to launch India focussed Sterile - Injectables portfolio

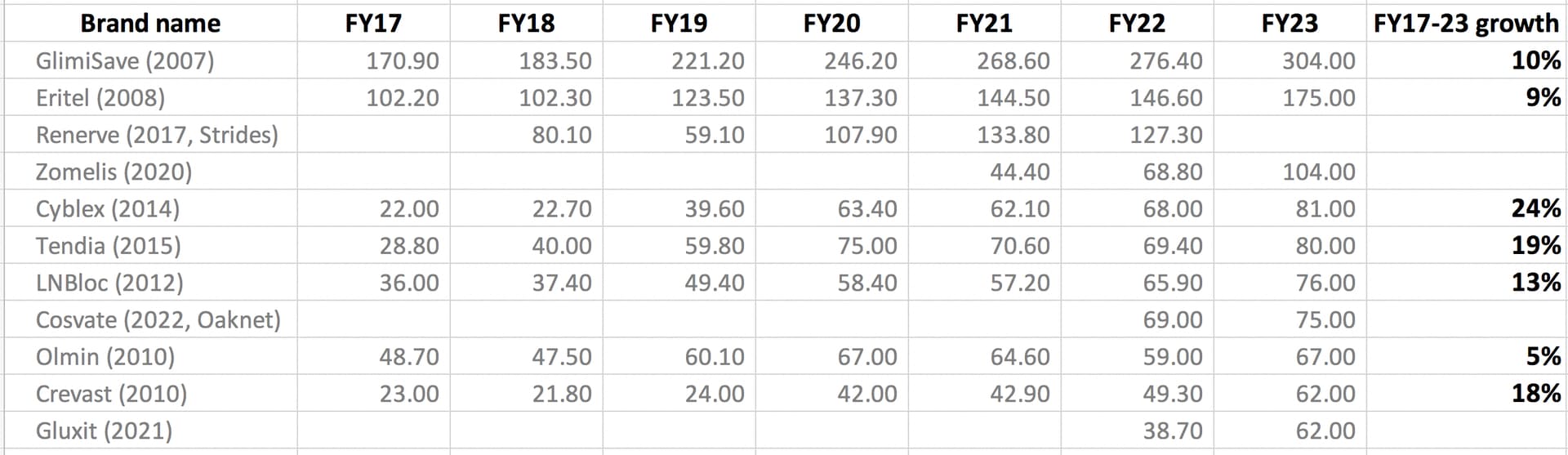

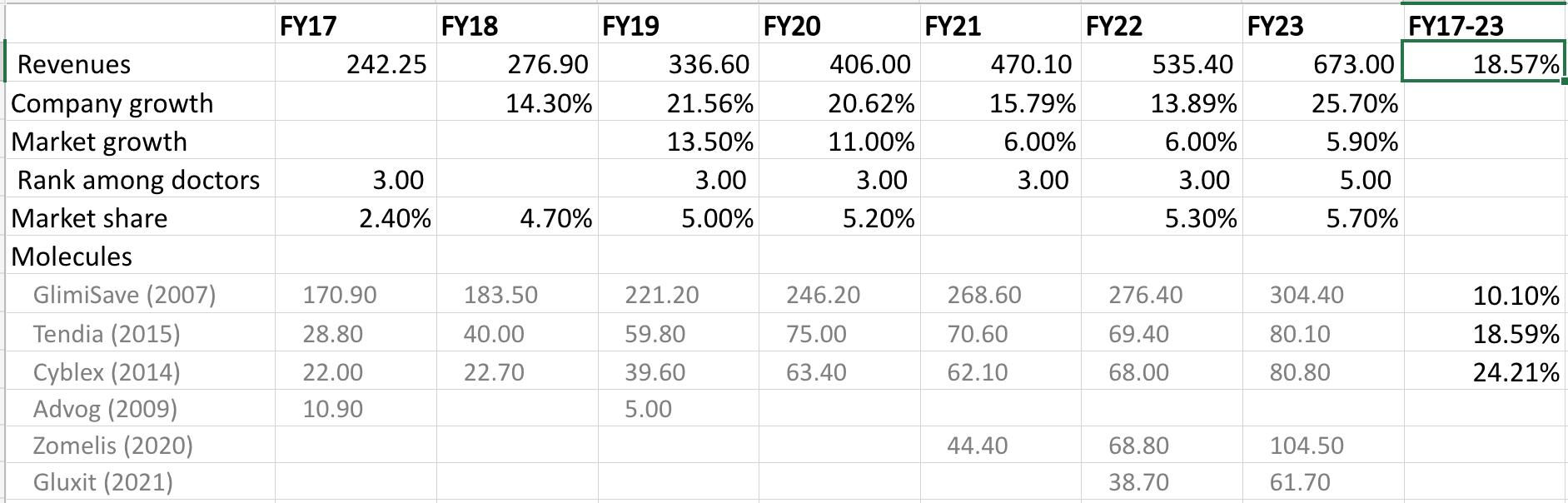

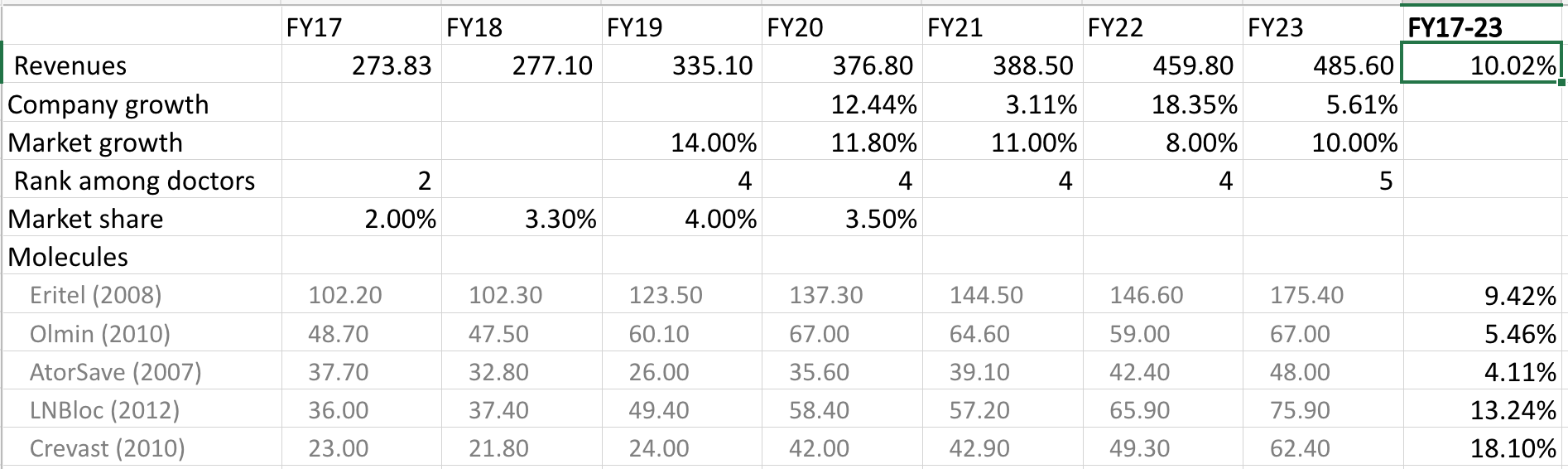

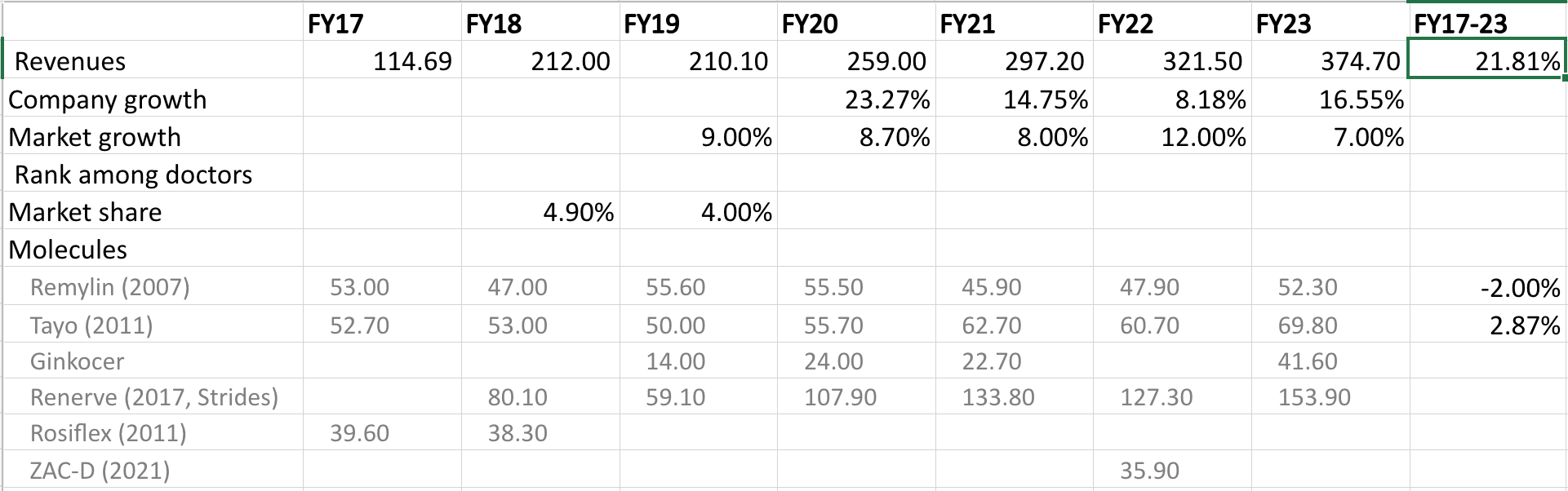

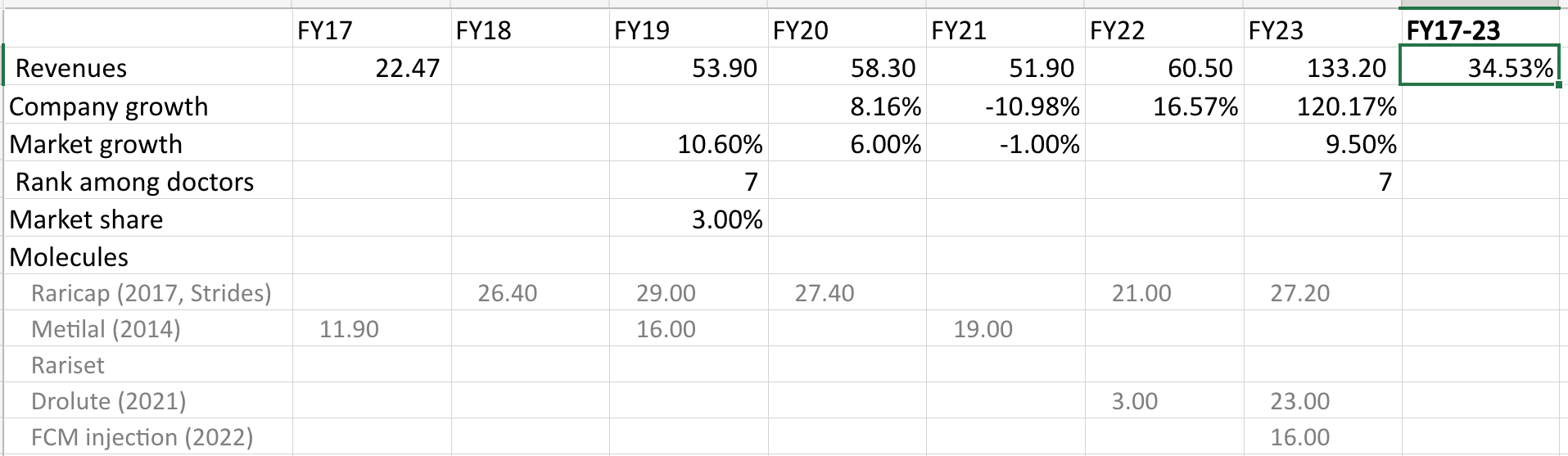

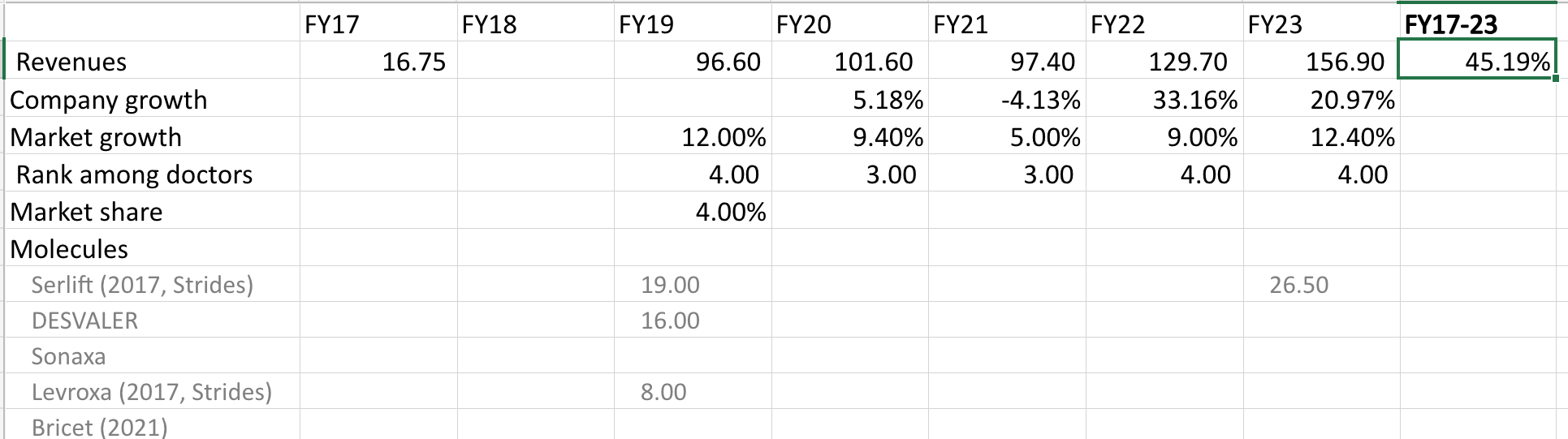

Company’s 100 cr/yr brands -

GlimiSave ( anti-diabetic ) - 300 cr

Eritel ( Telmisartan - anti-hypertensive ) - 170 cr

ReNerve ( Gabapentin + Methylcobalamin - CNS drug ) - 160 cr

Zomelis ( anti-diabetic ) - 105 cr

Company’s 50 cr/yr brands -

Tayo ( Calcium + Vit D supplement ) - 80 cr

Gluxit ( anti- diabetic ) - 75 cr

Remylin ( folic acid supplement ) - 70 cr

Company plans to launch Glargine and Liraglutide in Q4 ( both are biosimilars )

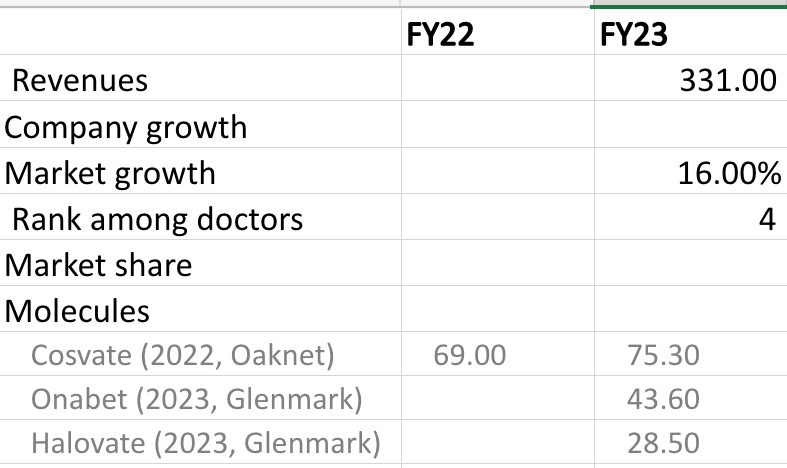

The Derma companies and brands acquired by the company in FY 22 have seen an EBITDA margin improvement from 10 pc to 35 pc inside 2 yrs !!!

Both the injectable plants acquired by Eris are currently running on single shift basis offering significant operating leverage opportunity to the company

Eris intends to do a business of 100 cr in the domestic mkts from year-1 iro the newly acquired Injectable facilities

Looking at Swiss Parenteral’s RoW focus ( basically branded and unregulated mkts ), wide product portfolio ( they make a lot of injectable antibiotics ) , R&D focus and juicy EBITDA margins - its a sweet sweet deal for Eris

Swiss Parenteral currently operates on distributors led front end in the RoW mkts. After partnership with Eris and Eris’s brand name, the front end distribution challenge in the Indian Mkt is virtually gone for Swiss. Hence, its a win win for both

Eris had acquired the derma and nephro brands of Biocon Biologics for 366 cr in Mid Nov 23. This business is doing a Gross Margins of around 70 pc vs 50 pc at the time of acquisition !!! This portfolio is likely to do a revenue of 10 cr or so / month from next FY onwards

Eris intends to put up another Injectables plant under the guidance of Swiss Parenteral. It may need a capex of 40-60 cr

Company is on track to achieve 2000 cr topline, 700 cr EBITDA, 400 cr PAT for FY 24

Disc: holding, a core holding, biased, added more recently, not SEBI registered