I think results were reasonable, Q4 is always a low base quarter so QoQ comparison will give an incorrect picture. On a YoY basis, company grew around 9-10% which is higher than IPM growth. If we look at IPM data, there has been volume de-growth at an industry level whereas Eris has managed to maintain its volumes. The recent insulin launch will reflect in FY23 numbers, lets see how it goes.

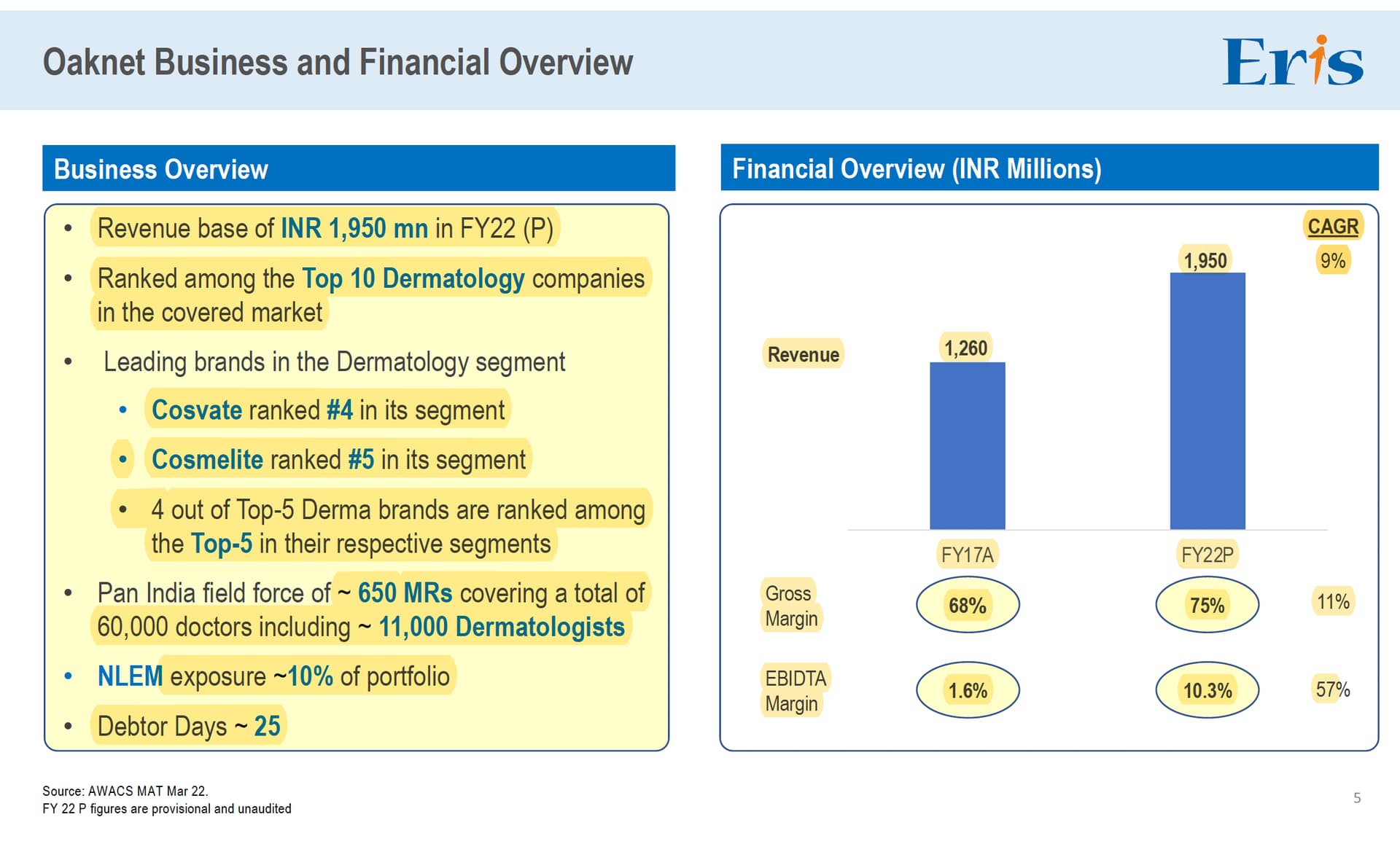

Today’s acquisition of Oaknet is also very interesting, it gives Eris an entry in Dermatology segment. Oaknet is supposed to do sales of 195 cr. in FY22 with gross margins of 75% and Eris paid 650 cr. for this (~3.33x sales). This is probably close to a fair price (or maybe a bit undervalued), specialty brands generally sell at 4-6x sales in private markets. I think Eris will rationalize the MR strength (or make them sell more products), you generally don’t need 650 MRs for maintaining sales of 200 cr.

The recent acquisition of Oaknet by Eris is an interesting foray into dermatology and other branches where Oaknet has strength.

Oaknet has a good basket of products, though none of the products are highly differentiated. The whole game here could be using Eris marketing skills in a company which is already present in certain segments and try to accelerate the growth in the acquired company.

Oaknet has been a not too agressive, not too sleepy kind of company, and that is reflected in the 9% cagr sales growth as depicted in previous post. If eris can somehow sweat existing products and bring in new novel products, this can be a value accretive acquisition.

disc: no positions. But got interested due to Oaknet (a company I am familiar with) acquisition. I think earlier name of Oaknet was Cosme healthcare and that too probably was acquired by Oaknet, or underwent a name change.

Today’s interview of Eris Life’s MD - Mr Amit Bakshi where-in he clearly spells out the rationale and economics behind the acquisition of Oaknet.

Looks like a very good catch for Eris. Plus the growth guidance for the organic business is also reasonably strong.

At CMP, Eris Lifesciences looks to be undervalued and ripe for buying considering its a pure play branded India generics business with excellent return ratios. Plus these smart acquisitions are a cherry on the cake.

Notes from AR iro Eris Lifesciences for FY 21-22 -

Company remains focussed on brand building. Their top 15 mother brands clock in 80 pc of the company revenues. Company grew in double digits despite IPM growth of 1.3 pc ( only - due pandemic hitting acute therapies ). The same was due to company’s focus on chronic therapies. Field force productivity improved 15 pc during the year.

Company has exiting organic and inorganic growth opportunities ahead -

(a) Rich pipeline of new product launches led by patent expiries in cardio-metabolic and allied segments.

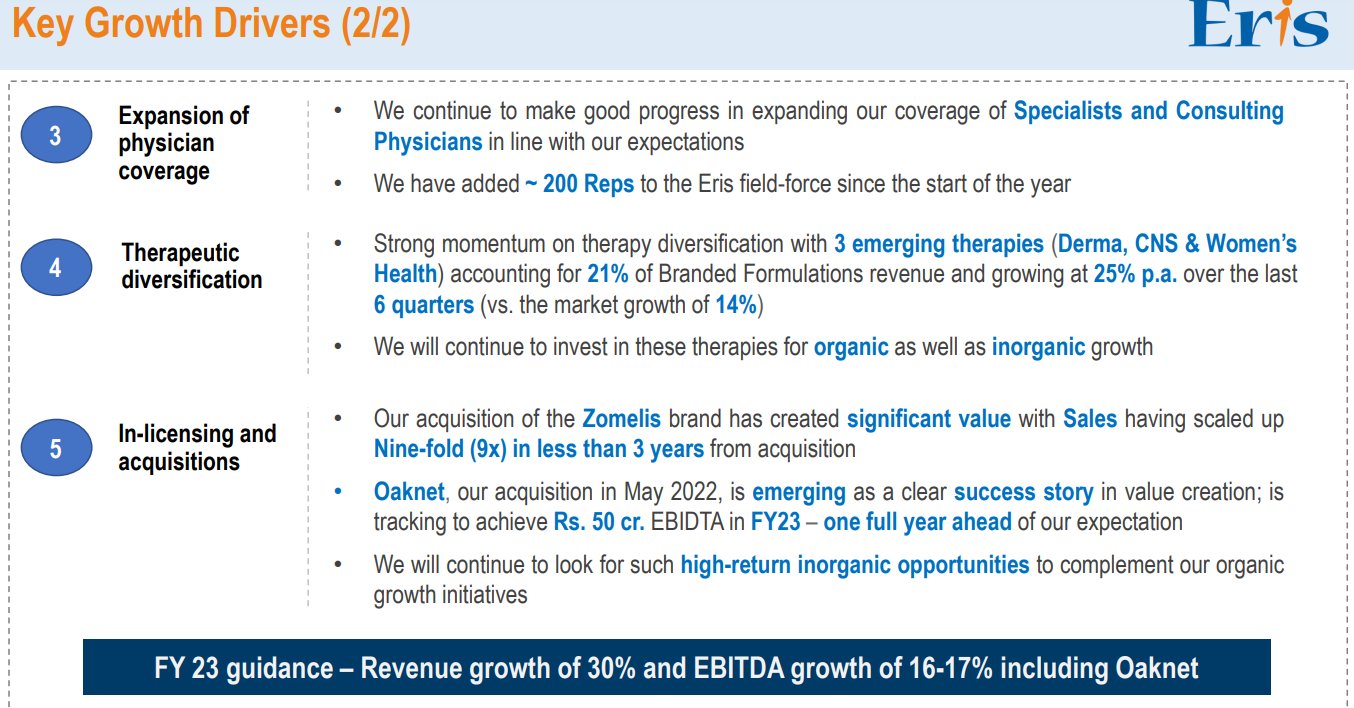

(b) Expanding coverage of specialists and consulting physicians.

(c) Company’s push for early detection and better life cycle management through patient care initiatives.

(d) Tech investments to improve sales force productivity.

(e) Company is on the look out for high-return in-licensing and acquisition opportunities.

Currently, ERIS is ranked 22 in IPM and is the only pure play India focussed company in the listed space. Revenues have grown 6X in last 10 yrs and 2X in last 5 yrs. Company has maintained ROIC > 30 pc for last 12 Yrs. Chronic focussed portfolio contributes 91 pc of sales with 7 pc of sales coming from NLEM drugs. Company is ranked no 3 among diabetologists and no 4 among cardiologists. Company’s top 10 products are ranked among top 5 in their respective categories. Two of company’s brands rank no 1 in their respective categories - Gluxit ( Dapagliflozin ) and Zomelis ( Vildagliptin ). Another dominant brand from company’s stable is Renerve ( nutraceutical ) is clocking annual sales of 135 cr.

For FY 21-22, Cardio metabolic segment ( 60 pc of company revenue ) grew by 9.7 pc vs Mkt growth of 9.3 pc. Nutraceuticals ( 20 pc of business ) grew by 15 pc vs Mkt growth of 8.6 pc. Gross margins reduced from 84 pc to 80 pc due to increased investments behind new launches.

Therapy wise revenue breakdown -

Oral diabetes care - 32 pc

Cardiac care - 26 pc

Vitamins, Minerals,Nutrients - 20 pc

CNS - 7 pc

GI - 6 pc

Gynae - 4 pc

Pain - 2 pc

Others - 3 pc

Manufacturing infra - Manufacturing facility at Guwahati accounted for 74 pc of all products sold in FY 21. Also eligible for tax benefits till FY 24 and GST subsidies till FY 25.

Q1 results from Eris Lifesciences. Prima facie, results look mixed.

However, company has guided for 30 pc revenue and 16-17 pc EBITDA growth for FY 23. Will have to listen to concall to figure out where is such confidence emanating from.

I was on the call, most growth is coming from Oaknet acquistion (contribution will be ~185 cr. to Eris in FY23). Also, a few of their products are doing very well (zomelis crossed 100 cr. runrate, CNS is growing at 20%+, Insulin portfolio should do 20 cr. annual revenues, and they have 15+ launches planned this year). Margin wise, it will be a soft year. They are guiding for margins reverting to 36% by FY25.

Disclosure: Invested (position size here, no transactions in last-30 days)

Thanks for the prompt reply. One doubt that I have… In Q1, Oaknet’s contribution was only 31 cr ( as per investor PPT ). Doing 185 cr for full FY from Oaknet looks like a tall ask.

Did the management throw any light on this?? Is the Oaknet business showing increased momentum in Jul-Aug etc??

Quarterly run-rate of Oaknet is actually 55 cr., only 31 cr. was accrued to Eris in Q1 as the acquisition was done in early May 2022 (so 24 cr. did not accrue to Eris). Management is guiding that 55 cr. quarterly sales look sustainable, if thats the case for the full year Eris should get 31+55*3 ~ 196 cr. So 185 cr. is doable if Oaknet maintains the runrate.

Guidance: 30% consolidated revenue growth, 32-33% EBITDA margin. Will be back to 36% EBITDA margin by FY25

Zomelis brand has crossed 8.3 cr. monthly sales (annual run-rate of 100 cr.). This should be the 4th 100 cr. brand by end of FY23

Oaknet: Quarterly run rate of 55 cr. sales and 10 cr. EBITDA

Cardio market has started reviving in June-July (average growth has increased to 13% vs 2% in the past twelve month)

Aprica: profitability will be maintained ~20%

In order to get to 14-15% organic growth trajectory, IPM growth has to come back to 8-10%

Expect 200 bps pressure on gross margin due to newer launches

Expect to deliver 20 cr.+ annual sales of insulin with EBITDA loss of 15 cr. Will launch insulin Glargine in Q3FY23 (in-licensed from Biocon). One-time payment and then sourcing arrangement (no recurring royalties)

Gujarat facility will commence in Q4FY23 – capex incurred was 34 cr. (100 cr. incurred till date). Total expected capex ~ 170-180 cr.

EBITDA margins will be impacted: (1) EBITDA losses due to insulin launch, (2) a lot of new product launches in cardiology in Q2 and Q3, (3) Oaknet margins

Have not had new launches in CNS, but this segment is growing at 20-25%

Trade generics: Had 8 cr. EBITDA loss in FY22 and will move to breakeven in FY23

Very insightful interview, management covers their diabetes and CV launches along with the rationale for Oaknet acquisition. Also, they mention that current rules will mostly impact trade generic companies.

Company came up with reasonable results, Oaknet business has turned around faster than earlier guided and is already doing 24% EBITDA margins. Management is guiding for 30% sales growth and 16-17% EBITDA growth in FY23. Recovery in cardiovascular division is the reason behind the confidence. Concall notes below.

FY23Q2

Guidance maintained at 30% sales growth and 16-17% EBIDTA growth for FY23. Tax rate will be ~10% for FY23

Oaknet’s 50 cr. target EBITDA will be achieved in FY23 vs earlier guidance of FY24. Expanded dermatologist coverage to 90% from 60%

Oaknet will be amortized over 20 years

Growth in cardiovascular division has resumed. SGL2 & DPP4 contributes 35-40% to diabetes sales

The stark difference in primary (10%) vs secondary sales (19%) is because of certain products (probably Zayo, link) which have gone into legal issues, which were already supplied to the market (but are no longer being supplied). So these are captured in secondary sales data but not in primary sales

Launched 4 drugs (Zomelis D, Glura, Gluxit S & FCM Injection) in H1 FY23

Aim is to get 18-20 cr. of revenues from insulin in FY23. This will not be a cash burn business in FY24