- Recent new IPO at Rs603 with Rs8540crs market capitalization

- Eris is a pharma company that derives all of its sales from India.

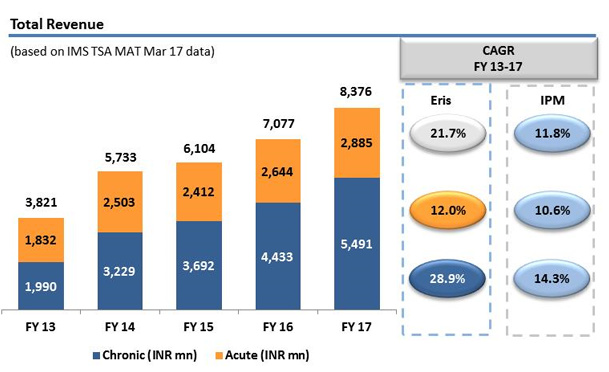

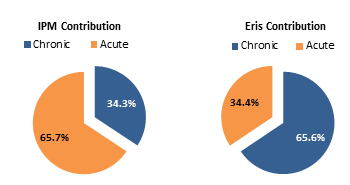

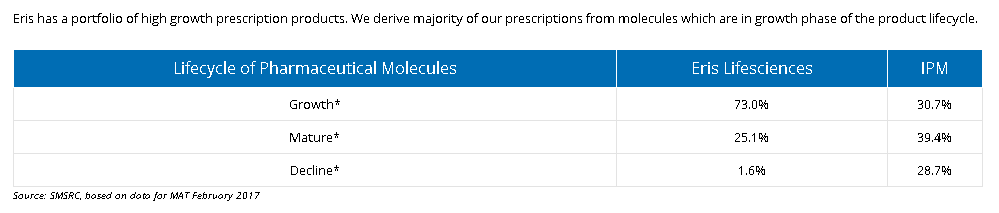

- Chronic category contributes to over 65.6% of sales.

- Eris has outpaced the Indian Pharmaceutical Market (IPM) growth with a CAGR of 28.9% in Chronic and 12.0% in Acute therapy segment.

- Eris is the fastest growing company in Chronic therapy amongst the top 25 companies.

- Eris is the 3rd fastest growing company in Cardiovascular and Anti Diabetics therapeutic segments.

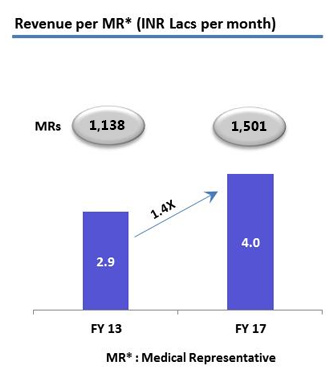

- Field force productivity of INR 4 Lac( YPM – Yield per Man per Month) is industry leading and -

- Eris is amongst most productive companies in the Industry.

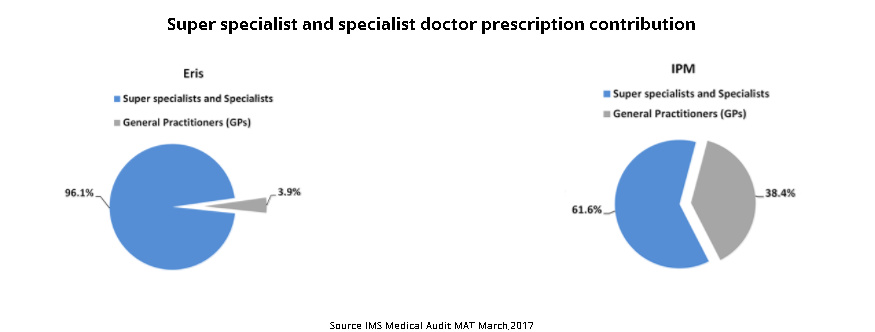

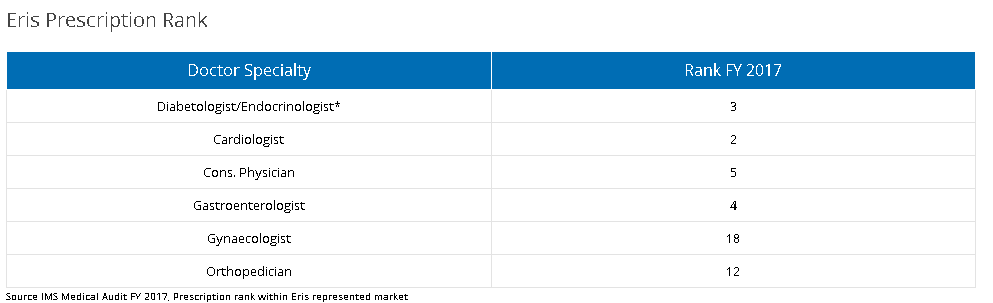

- Eris product portfolio is primarily focused on therapeutic areas which are treated by super specialist and specialist doctors such as Diabetologists, Endocrinologists Cardiologists, and Gastroenterologists.

- Super specialists and specialists contribute to 96.1% of our total prescriptions as compared to 61.6% for the IPM. We have a prescriber base of 50,282 doctors for Fiscal 2017 as per IMS medical audit.

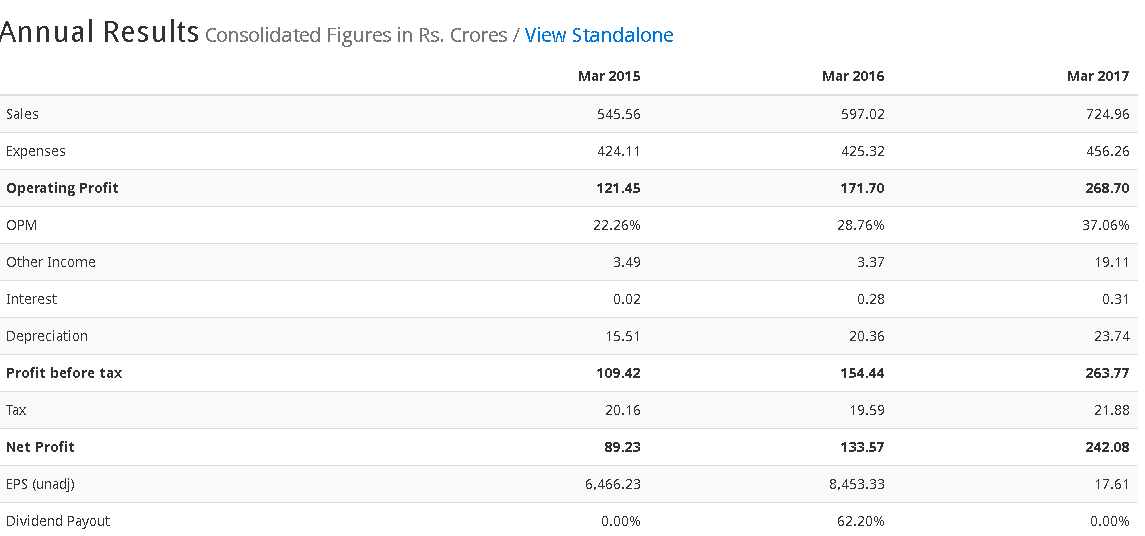

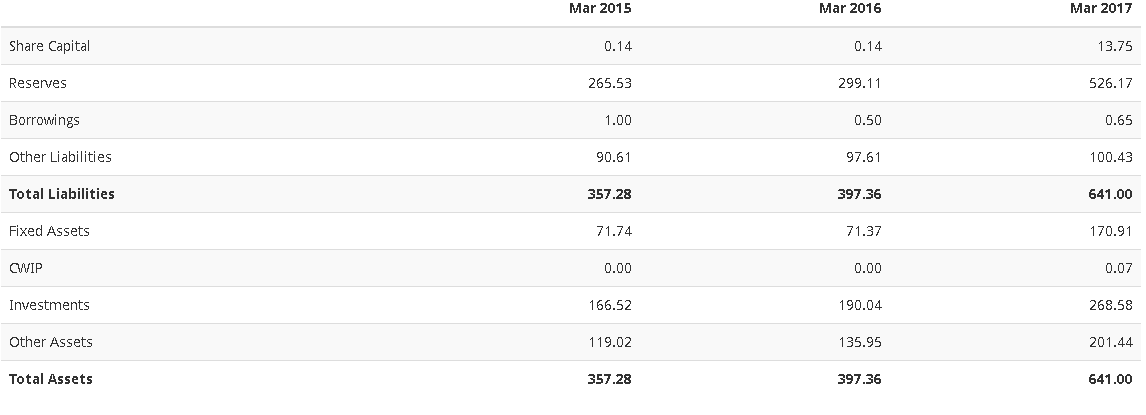

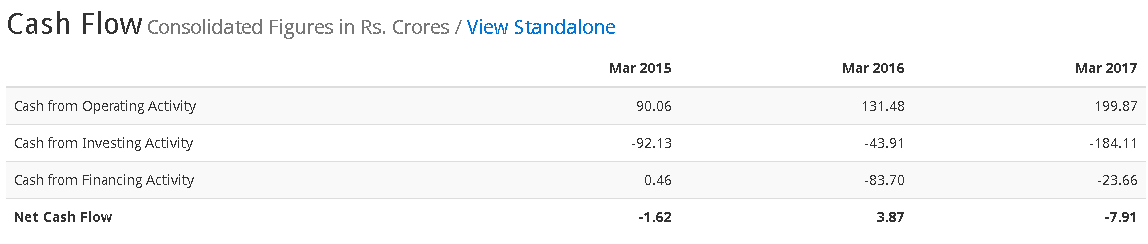

Financials from screener

Company is zero debt.

2Q results over the weekend

- 25% sales growth

- EBITDA margin expansion of 208bps

- 35% PAT growth

Acquires Strides’ India business

Eris has agreed to acquire Strides’ India branded formulations business with 130 brands and Rs181crs sales for Rs500crs.

Key risks as I understand

- If products are brought under price control

- Business built around strong brands and relationships with specialists/ super specialists, a shift to unbranded generics is a big risk

Disclosure: Invested