Another good set of booking nos from Ashiana, they have been able to increase realizations and get volume growth. Reported nos look muted due to lower deliveries. They are doing very well as shown in sales of all 224 flats in Ashiana Amarah project in Gurgaon at launch (243 cr.). Concall notes below.

FY23Q2 concall:

Will have 1-1.5mn sq.ft launch in H2FY23. Have four more projects in pipeline for FY24

Malhar + Anmol: Low margin projects. Other projects are at significantly higher margins

Ashiana Amarah: Launched Phase I (224 units) and sold all of it (243 cr.). Will be booked in Q3FY23. This kind of sales implies investors are back in the market

Negative cashflows this quarter was due to front ending of expenses and pre sales happening towards end of quarter. It’s a QoQ issue

On economic basis (not reported basis), will reach double digit ROEs in FY23

Gurgaon realizations have now crossed Rs. 6000/sq.ft

Current land and projects is for 4-5 years of inventory

Disclosure: Invested (position size here, no transactions in last-30 days)

Very good set of nos from Ashiana, with presales growing to 485 cr. due to successful launch of Ashiana Amarah project (sold 243 cr. of inventory at launch). Delivery schedule should keep improving in the next few years leading to better reported numbers going forward. Concall notes below.

FY23Q3 concall

FY23 Launches: Ashiana Advik (senior living in Bhiwadi), Ashiana Amarah (Gurgaon; sold out at launch), last phase of Ashiana Umang (Jaipur), last phase of Ashiana Dwarka (Jodhpur)

FY23 launches: Had planned 5 greenfield project. 3 were done so far and 2 will be launched in Q4FY23 (Ekansh in Jaipur, Prakriti in Jamshedpur; 7 lakh sq.ft launches). Plan to have 1mn sq.ft launch in Q4 (7 lakh greenfield + 3 lakh phase extensions)

FY24 launches: Planned 5 greenfield launches (2 in Jaipur, 2 senior living in Chennai, 1 senior living in Pune) (10-15 lakh sq.ft) + 10-15 lakh sq.ft in existing projects (total around 3mn planned launches in FY24)

20-25 lakh sq. ft construction target in FY24

Have received RERA approval for Phase II in Ashiana Amarah, plan to launch it soon

Some signs of correction are seen in land prices. Plotting market in Gurgaon has slowed down

Higher realizations are due to Ashiana Amarah project

Ashiana Advik was launched at 7-8% higher prices compared to Nirmay (last senior living project)

Deliveries Q4: Ashiana Sehar (have received OC). In Ashiana Aditya, have applied for OC and might slip if they don’t get OC in time

Gross profit margin: In older projects, it’s at 27-28%. 4% selling costs in good projects (like in Jamshedpur). Generally selling costs varies between 2-8%. Margins should improve in 2-3 years once current projects start getting delivered

Senior living: Contributes 10-20% of sales volume (hoping to get 150 cr. area booked in FY23). Want to grow it to 300-400 cr. over next 2-3 years. These projects have 3-5% higher gross margins and similar selling costs as existing projects

FY24 deliveries: Blended gross margins will be around 27% and reported ROEs will be high single digit

In Ashiana Prakriti project (Jamshedpur), share of revenue is same as 73.61% (error in presentation)

Disclosure: Invested (position size here, no transactions in last-30 days)

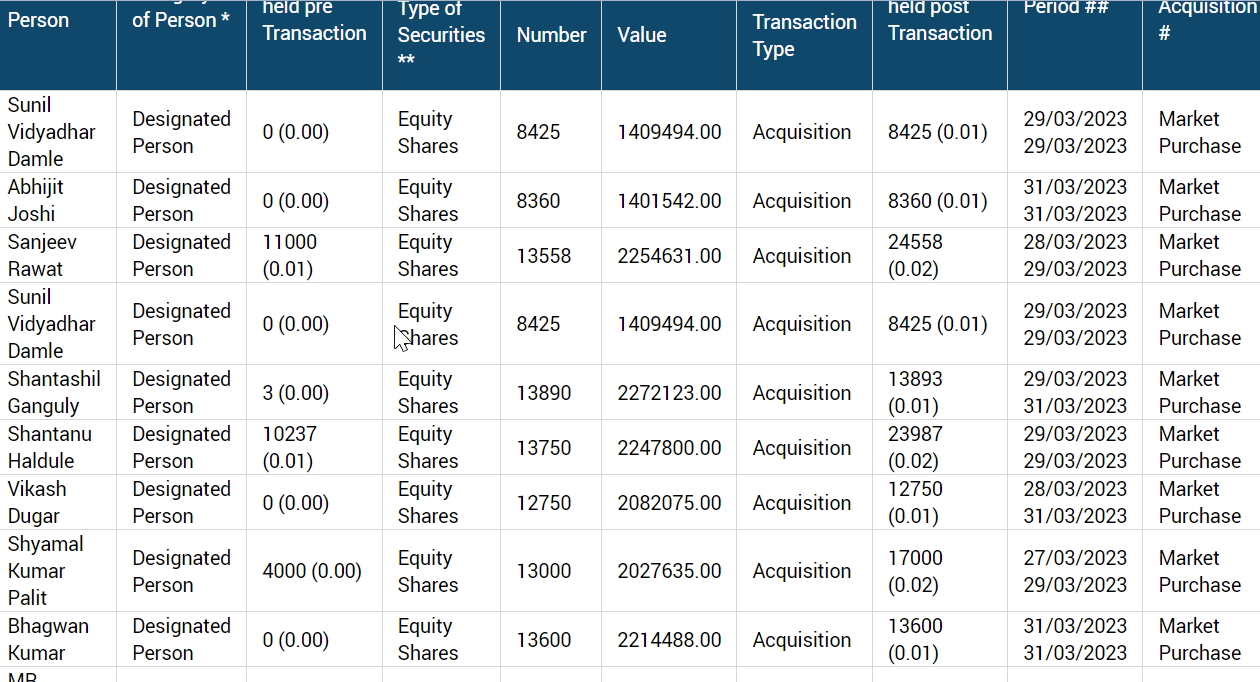

All the key person buying similar quantities and similar gross values. Could not understand this. How all of sudden some key people buying similar amount of quantities.

Another very good set of nos from Ashiana, on reported P&L they should have 850-900 cr. sales in FY24 and they are targeting 1500 cr. of pre-sales. Concall notes below.

FY23Q4

FY23 launches: 13 projects (5 greenfield + 8 phase extension in existing projects) accounting for 29.46 lakh sq.ft

Land acquisition: 2 in Jaipur (Ashiana Nitara in Bhankrota with saleable area of 6.5 lakhs sq ft + ‘The Amaltas by Ashiana’ in Jagatpura with saleable area of 4.00 lakh sq. ft) + 1 in Manesar (Gurgaon) with saleable area of 10.30 lakh sq. ft.

GIDC Manesar land: Have paid 25%, waiting for formal agreement to sell after which they have 12 months to make remaining payment and can then go for planned approval. Ashiana takes a lot of time in designing the project and will apply for environmental approval simultaneously. Expect launch in FY25

Ashiana Amarah: Phase 2 sold out at launch (224 units; 3.77 lakh sq.ft; 283 cr.) and booked in April 2023. Phase 1 (224 units; 3.95 lakh sq.ft; 243 cr.) was sold just 6 months back in Q3FY23. So there has been pricing increase of close to 22% in less than 6 months

NCR and Jaipur land prices have doubled since FY20 whereas sales prices have increased by 20-50%

Ashiana Prakriti (Jamshedpur): Sold at launch (162 units; 2.57 lakh sq.ft)

Current pipeline: 15 lakh sq.ft in ongoing projects + 94 lakh sq.ft in future projects + 10 lakh sq.ft in land (excluding Milakpur and Kolkata) ~ 119 lakh sq.ft

Thumb rule: Reach 15% ROE on a corporate level with 30% gross margin

Economic ROE: Have reached double digit in FY23 and will cross 15% in FY24

Land deals: Negotiating 2 land deals (Jaipur + another market) that will hopefully add 20 lakh sq.ft to saleable area

Pricing trends: Higher confidence in pricing in Gurgaon, Jaipur, Jamshedpur and senior living

P&L structure: 30% gross margins + 4-4.5% selling costs + 7% corporate costs + tax. PAT margin of 13-15%

Non-core assets: Slowly disposing them, looking to dispose school in Bhiwadi (wont dispose hotel in Bhiwadi; generates 15% on capital invested)

Red flags to watch when things are going south:

In JV transactions, increasing revenue share tells that builder is becoming more aggressive

If flat sizes go down, that means affordability is a problem

Disclosure: Invested (position size here, no transactions in last-30 days)

Another good set of nos from Ashiana, they have been able to maintain 400 cr.+ quarterly sales runrate and are guiding for 1500 cr.+ presales in Fy24. In this cycle, they are focusing much more on ROE (than volume growth). Concall notes below.

FY24Q1

Ashiana Amarah Phase 2 launch was sold for 290 cr. (224 units; 3.77 lakh sq.ft). Will launch Phase 3 in Q4FY24

FY24 launch: 5 projects to be launched (Ashiana Amodh in Pune was launched in July; 2 in Chennai and 2 in Jaipur)

Ashiana Malhar: Have sold 1.8 lakh sq.ft (out of 2.6 lakh sq.ft) launched in August 2022. Price increase has been lower than what they wanted (around 200-300/sq.ft); realizations increased from 5200 to 5400-5500/sq.ft

Ashiana Amodh: Have seen very good traction and were able to get higher realization, given its their first senior housing project in Pune

Saw very good sales traction in existing projects in July. Have pipeline of 1 cr.+ sq.ft (excluding Kolkata and Milakpur)

Don’t want to build a huge pipeline of land as focus is on improving ROE

In last cycle, they did mistake of going for volume and topline growth. In this cycle, they want to optimize ROE and not focus on volume growth

Economic ROE in FY23 was in low double digit and should achieve high teens in FY24

Want to reach 10-12% PAT margin, and with benefits of operating leverage to 15% levels in a good cycle

Aiming for 250-300 cr. pre-tax operating cashflow

In last 18 months, land prices have appreciated faster than improvement in flat prices. However, all of Ashiana’s deals since 2020 has been at higher margin vs historical margins

Disclosure: Invested (position size here, sold shares through participation in buyback in last-30 days)

Ashiana had their second best quarter since 2016. Demand seems to be very strong, and management is confident of reaching 1500 cr. presales in FY24. Project pipeline remains strong

Current pipeline: 12 lakh sq.ft in ongoing projects + 84 lakh sq.ft in future projects + 21 lakh sq.ft in land (excluding Milakpur and Kolkata) ~ 117 lakh sq.ft

Annual sales volume run rate should increase from 25 lakh sq.ft (12.45 lakh sq.ft sold in H1FY24)

Greenfield projects: 6 (3 in Jaipur, 1 in Gurgaon, 2 senior living in Chennai). 4 will be launched in remaining FY24 and 2 in FY25

Ashiana Amodh (Pune, senior living): Successful launch (27% of Phase 1 inventory sold this quarter)

Ashiana Shubham (Chennai, senior living): Last phase launched (56% of inventory sold this quarter)

Ashiana Prakriti (Jamshedpur): Phase 2 launched (76% inventory sold this quarter)

Jaipur: Acquired new land in Jaisingpura (11 lakh sq.ft). Its near the Ashiana Ekansh project

Construction: Will do 2-2.2mn sq.ft in FY24 (0.9 mn sq.ft constructed in H1)

Larger focus will be on increasing prices

Will not get into horizontal plotted development

New Gurgaon prices have increased 2-3x over last 5 years (Ashiana Amarah region)

Channel partners in NCR add a lot of value as there are lots of projects available in this region. This is not the case in Jaipur or smaller cities

Senior living is gaining a lot of traction

Economic ROE will cross 15% in FY24 and seem sustainable (and probably higher than 15%)

FY25-27: Plan to do cumulative delivery of 50 lakh sq.ft (2600-3000 cr. revenues)

Kid-centric projects: Planned launch of one project in Gurgaon and one in Jaipur. First sign is evident in Ashiana Umang.

Disclosure: Invested (position size here, no transactions in last-30 days)

Ashiana had a muted quarter in terms of presales due to very low inventory to sell. Their launch pipeline looks very healthy in next few quarters which gives them comfort to grow presales at 15-20% in next 2-3 years. Concall notes below.

FY24Q3

Current pipeline : 12 lakh sq.ft in ongoing projects + 80 lakh sq.ft in future projects + 21 lakh sq.ft in land (excluding Milakpur) ~ 113 lakh sq.ft

Didn’t launch any new projects in Q3 and had limited inventory to sell

Confident of 15-20% CAGR growth in presales over next 2-3 years (in a lumpy way). Looking to reach 30 lakh sq.ft pre-sales sustainably

November 2023 launches : Malhar Phase II + Tarang Phase V

Q4 launches :

New projects: Ashiana Nitara (Jaipur), One 44 (Jaipur) - will launch 5-6 lakh sq.ft out of 24-25 lakh sq.ft

Amarah Phase III: 3.77 lakh sq.ft (can slip to Q1FY25). Will see 40% price increase

Will cross 1500 cr. presales if they launch Amarah in Q4. Otherwise presales will be 1250-1300 cr.

FY25 launch : 3 projects (30 lakh sq.ft)

Near term launch pipeline: New project in Gurugram, 3 projects in Jaipur, 2 in Chennai

Realizations : 4,700-7,000 for senior living; 3,500-7,000 for premium homes, 4,500-8,000 for kid-centric home

Except in Bhiwadi, demand is very strong in other micro markets

Exited Kolkata project (Ashiana Maitri/Nitya)

Sold Marine Plaza Project in Jamshedpur (litigated non-core asset) in Q2 with a loss at gross margin level

Gross margins may reach 30% in FY25

Land prices have gone out of whack in Gurugram, and apartment prices haven’t kept up

Disclosure: Invested (position size here, no transactions in last-30 days)

Ashiana has crossed most of their peak metrics and are now expecting further scaleup with improved profitability (plans to reach 15%+ PAT margins in 3-years). Concall notes below

FY24 launches: 10 projects (4 greenfield + 6 phase extension in existing projects) accounting for 23.19 lakh sq.ft vs 29.46 lakh sq.ft in FY23

Targeting 2000 cr. presales in FY25 and 25-26 lakh sq.ft of constriuction. Plan to launch remaining phases of Amarah in FY25 and hopefully first phase of Sector 80 (Gurgaon) in Q4FY25.

Current pipeline: 12.65 lakh sq.ft in ongoing projects + 80 lakh sq.ft in future projects + 21.3 lakh sq.ft in land (excluding Milakpur) ~ 114 lakh sq.ft

Delivered Ashiana Aditya in Jaipur and Amantran in Jaipur which had cost overruns and generated lower margins but good ROCEs as they in JV

See continuous margin improvement in subsequent years and want to reach PAT margins of 17-18%. Indirect costs as % of sales should reduce significantly in FY27

Focusing more on senior living which is higher margin and less competition. Looking to grow to 900-1000 units in 3-4 years vs 354 now. Have two term sheets for senior living in Bangalore right now (50% failure rate generally). Panvel senior living termsheet fell through

IFC: 1st platform has Ashiana Daksh (almost complete), Amarah, Vatsalya. Money from 2nd platform is yet to deployed. IFC debenture pays IFC around 30% of net project cashflow

Crossed economic ROEs of 15% in FY24 and will cross reported ROEs of 15% in FY26

Disclosure: Invested (position size here, no transactions in last-30 days)

not so great results this quarter… margin contraction and negative profit. yet to go through con call that happened today. any views on the company now?

Bhiwadi sales has picked up this quarter , prices have also increased

Momentum in price increase is slowing down

Ashiana Shubham (Chennai, senior living): Phase IV delivery – lower margin project and paid 1 cr. interest to customers due to late delivery. This is an older project (signed in 2015), they had given very high revenue share to partner as they were just starting up in Chennai in 2015. Additionally, they had unexpected cost overruns. This problem will be lesser in Phase IVB and in Phase V due to price increases (6000+ sales realization in Phase V vs 5200 in Phase 4B and 4700 in Phase 4A)

Expect lower delivery in Q2 and will report losses, deliveries will pickup in H2

Amarah Phase IV launch in Q2, 25% higher realization than Phase III (4.7 lakh sq.ft). Not looking to sell at launch, want to maximize revenue potential. Phase V is planned to be launched in FY25

Ashiana Surbhi and One44 (Jaipur): sales were negative (-22,000 sq.ft). Saw cancellations in One44. Ashiana Surbhi: lot of old investors who had bought in the last boom cycle were not paying. Ashiana allotted these investors flats in other projects using proceeds earlier collected resulting in negative sales in Surbhi. Believe its one-time

Elite homes will be launched in One44 brand name (1.5 cr.+)

Phase II launch of One44 on Sunday, have left a lot of value for money

Maintain 2000 cr. presales guidance in FY25

Focusing more on business development in senior living housing

One termsheet in Bangalore fell through

Disclosure: Invested (no transactions in last-30 days)

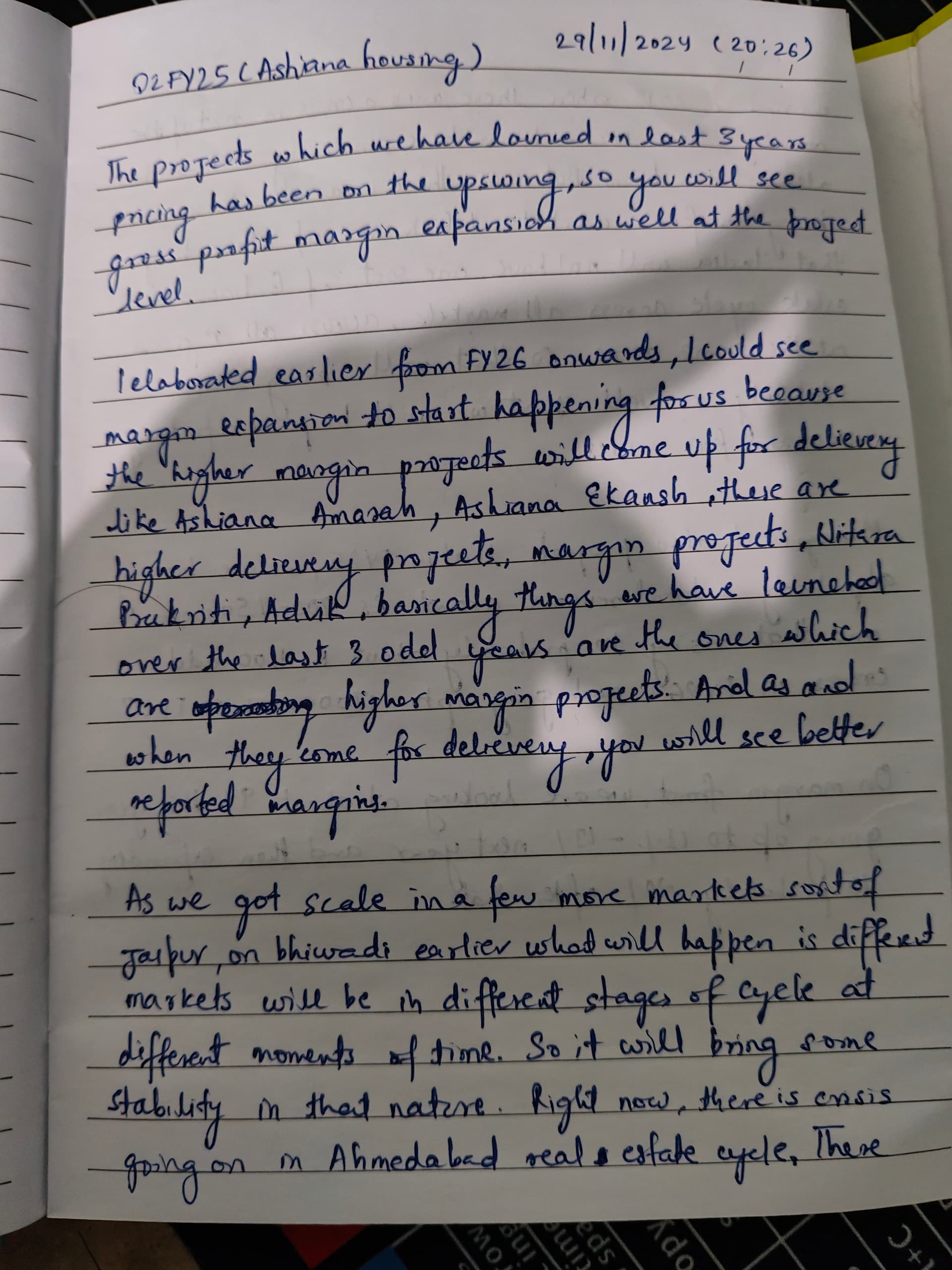

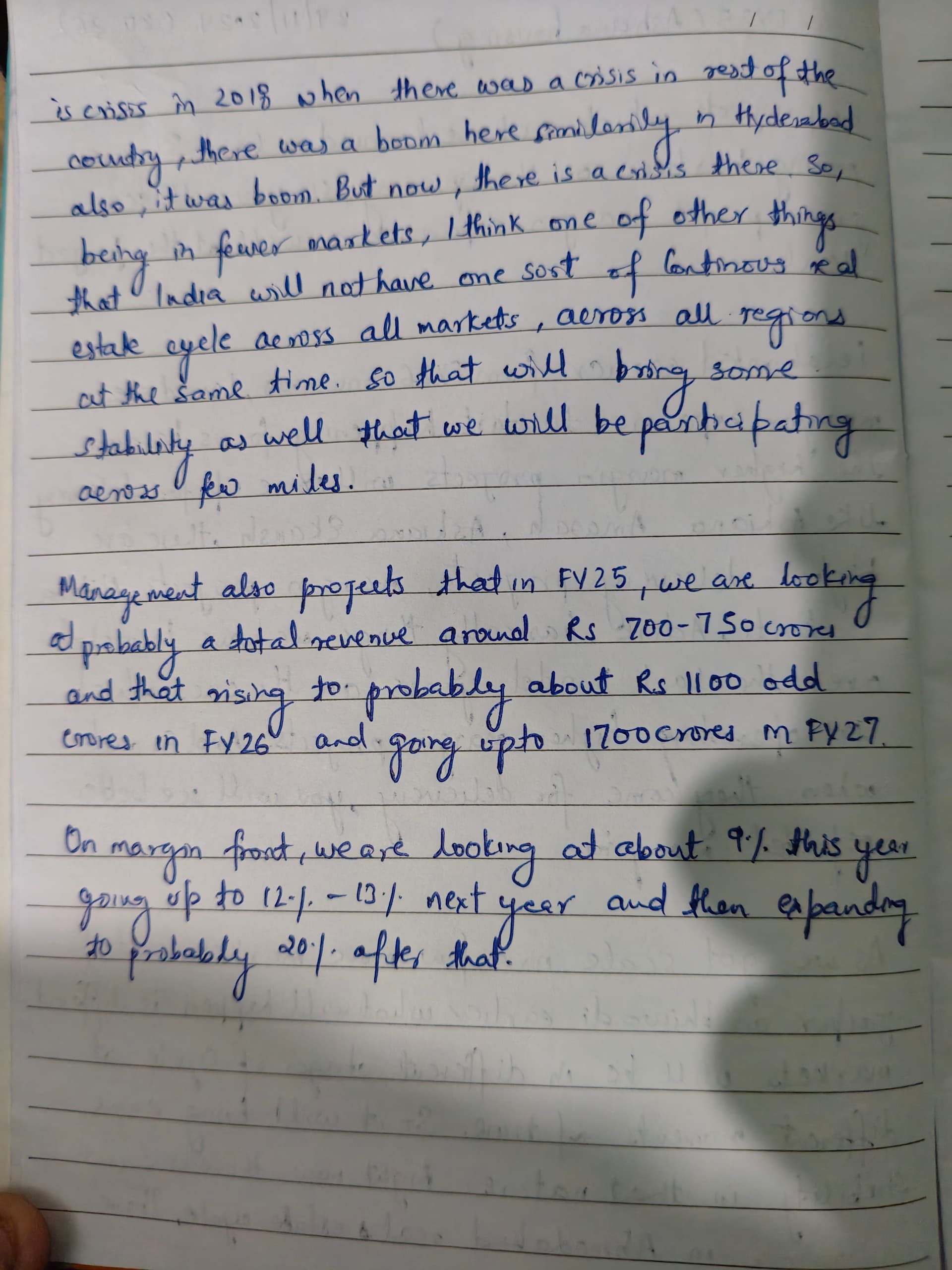

Ashiana is expecting reported nos to improve in H2FY25 and continued margin improvement in next few years. Concall notes below

FY25Q2

Land prices in Gurgaon are very expensive and they are finding it hard to find commercially viable projects

Will prefer not to launch projects for a year or two than pay very high land prices

Gurgaon Sector 80 project will be launched in Q1/Q2 FY26. The last auction in this area was 6-8 months back and land prices had already doubled vs what Ashiana had paid

Planned launches in FY25: Ashiana Amarah Phase V, Nitara Phase II, Ekansh Phase IV, Swarang, Amodh Phase II

In Ashiana Malhar, will now focus on increasing realizations

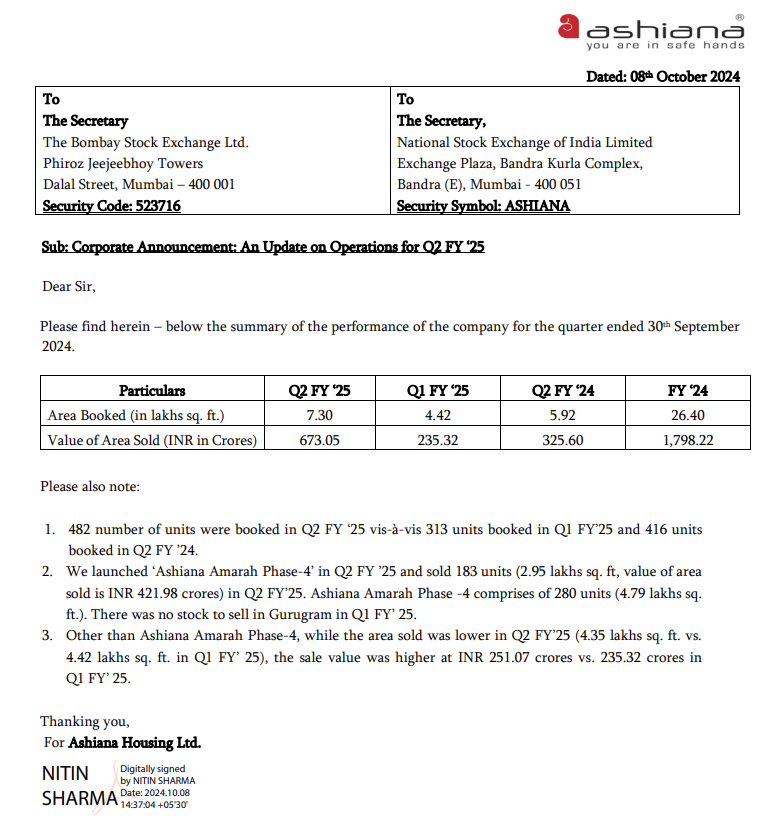

Believe they will deliver 700-750 sales and 9% PAT margins in FY25. Will start seeing margin expansion in FY26 (1100 cr. sales, 12-13% PAT margins) and FY27 (1700 cr. sales, 20% PAT margins)

Bhiwadi sales are quite good, supply situation is good with no new builders and sales price is increasing, looking to deploy money in Bhiwadi

Bangalore launch will take longer as they are setting up team there for the first time

Milakpur stuck money is 3-4 cr.

Disclosure: Invested (no transactions in last-30 days)

Superb answer from the management for a question of 'not having enough inventory beyond 2 years to maintain growth rate"?

Answer: Right now, we have good stock from another couple of year’s perspective for the next 2 years. After that a little bit of challenge might come in, but we have made up our mind if we might be like in Gurgaon, I would rather live with the problem of not having something to sell for a year or two rather than having the problem of having such an expensive land that selling it at profits or even a regular return just becomes very difficult and we don’t have the flexibility of having the liquidity available to respond to it as well. Between those two errors, I would rather make the error of not having enough stock to sell. That is according to me which side we will err on because having cash does provide flexibility in that aspect.

Like the management firmness. Invested around 304 levels.

")