Lavasa is a failed city/township. You can simply google to know what was promised in Lavasa vs what actually happened. This is not specific to Ashiana, rather the entire city itself.

2 Likes

Ashiana is one of the best managed real estate companies.

The promoters seem pretty honest and disclosure levels in their presentation are also unlike any other real estate company I’ve seen. They give complete breakdown of when they’re going to deliver which projects, quarter wise 3 years into the future. The management seems pretty rational in their capital allocation decisions. They treat land as raw material rather than an asset to be hoarded.

Exciting times for the company. I’ve been following the company for many years, so I know they are conservative in giving guidance.

For the first time, management has given guidance on PAT.

PAT Guidance:

FY25: 70 cr

FY26: 140 cr

FY27: 350 cr

FY28: 500 cr

7x PAT in 3 years

Disclosure: Invested from 150 levels. Bought more in last 30 days

6 Likes

Guidance for this year would be missed because of regulatory hurdles in delivering Ashiana Advik. Next year should be better than previously guided because of delivery getting pushed to Q1 from Q4

4 Likes

Ashiana will report ~300 cr. revenues in Q4 with muted margins due to shift of delivery of higher margin projects to FY26. Concall notes below

FY25Q3

- Witnessed good bookings across projects this quarter, the 2000 cr. pre-sales guidance is contingent on launch of Ashiana Amarah Phase-V in Gurgaon

- Q3 launches: Ashiana Swarang in Nemmeli (senior living), Ashiana Ekansh (Phase-4) in Jaipur, Ashiana Amodh (Phase-2) in Pune

- Have 15 lakh sq.ft of unsold inventory in ongoing project + 47 lakh sq.ft of inventory to be launched in existing projects + 25 lakh sq.ft of land (excluding Milakpur). ~87 lakh sq.ft means ~3-4 years of inventory

- Are also in talks for 10-12 lakh sq.ft land in Bangalore (to be finalized in 2 quarters)+ 20 lakh sq.ft land in Jaipur + another 7-8 lakh sq.ft land parcel for a senior living project in another location (early stage)

- Excessive exuberance in Gurgaon has mellowed down, demand is more normal now

- They believe they in 2-years they will be reporting 1700 cr. revenues with higher margin projects that were acquired in 2021-22 + operating leverage due to optimization of fixed costs + higher contribution of senior living housing which have higher margins. Expect to reach high teen PAT margins in 5-years

- Expecting 300 cr. reported revenues in Q4 with much lower margins as Ashiana Anmol Phase-2 will get delivered which is a very low margin project. The high margin project Ashiana Advik Phase-1 delivery got shifted to Q1FY26

Disclosure: Invested (no transactions in last-30 days)

5 Likes

Can you please share the source of Profit guidance shared by you?

Enjoyed listening to this conversation between the brothers.

2 Likes

Good to listen Ankur and his eldest brother about their dream project and their journey. Ankur is very adept in talking. True sales man quality.

Disclaimer: Holding and biased and bought recently. After listening this, It’s clear they are " lambi race ka ghora" of their fields.

| FY21 | FY22 | FY23 | FY24 | FY25 | Total Profits | MCAP | MCAP/Total Profits | |

|---|---|---|---|---|---|---|---|---|

| DLF | 1,083 | 1,500 | 2,034 | 2,724 | 4,367 | 11708 | 217980 | 19 |

| Macrotech | 48 | 1,208 | 490 | 1,554 | 2,767 | 6067 | 151250 | 25 |

| Godrej | -189 | 351 | 621 | 747 | 1,389 | 2919 | 74307 | 25 |

| Prestige | 2,878 | 1,215 | 1,067 | 1,629 | 617 | 7406 | 73850 | 10 |

| Oberoi | 739 | 1,047 | 1,905 | 1,927 | 2,226 | 7844 | 69388 | 9 |

| Brigade | -96 | -65 | 222 | 401 | 680 | 1142 | 31203 | 27 |

| Sobha | 62 | 173 | 104 | 49 | 95 | 483 | 17932 | 37 |

| Ganesh Housing | -105 | 71 | 102 | 461 | 598 | 1127 | 8574 | 8 |

| Purvankara | -4 | 148 | 67 | 42 | -183 | 70 | 7659 | 109 |

| Sunteck Realty | 42 | 25 | 1 | 71 | 150 | 289 | 6680 | 23 |

| Kolte Patil | -5 | 85 | 113 | -67 | 109 | 235 | 3509 | 15 |

| Arvind Smartspaces | 9 | 25 | 28 | 51 | 119 | 232 | 3186 | 14 |

The table above has the profits of each company for last 5 years and MCAP/last 5 yr profit ratio.

If Ashiana delivers 2000 Cr profits in next 5 years cumulatively, I fail to understand why would it not be atleast 10K Cr MCAP company and maybe more. The stock is very undervalued.

2 Likes

As per the Q4 Concall Transcript, Ashiana plans to deliver 11,000 Cr of property in the next 5 years. Ashiana had guided a Net Profit Margin of 12-13% for FY2026 and 20% for FY2027. So considering a conservative 15% profit margin, results in 1650 Cr of profits over the next 5 years. If we consider the lowest multiple of 8 (Ganesh Housing), the MCap comes to 13,200 Cr where as the Current MCap is 3,500 Cr. So there is scope for 3X in 5years. Let’s see how things pan out.

Agreed. But other than delays in launches and leading to delay in profit reported there is no other big risk involved I feel. So money is to be made if not in the next 1-2yrs but atleast in the next 3-4yrs

1 Like

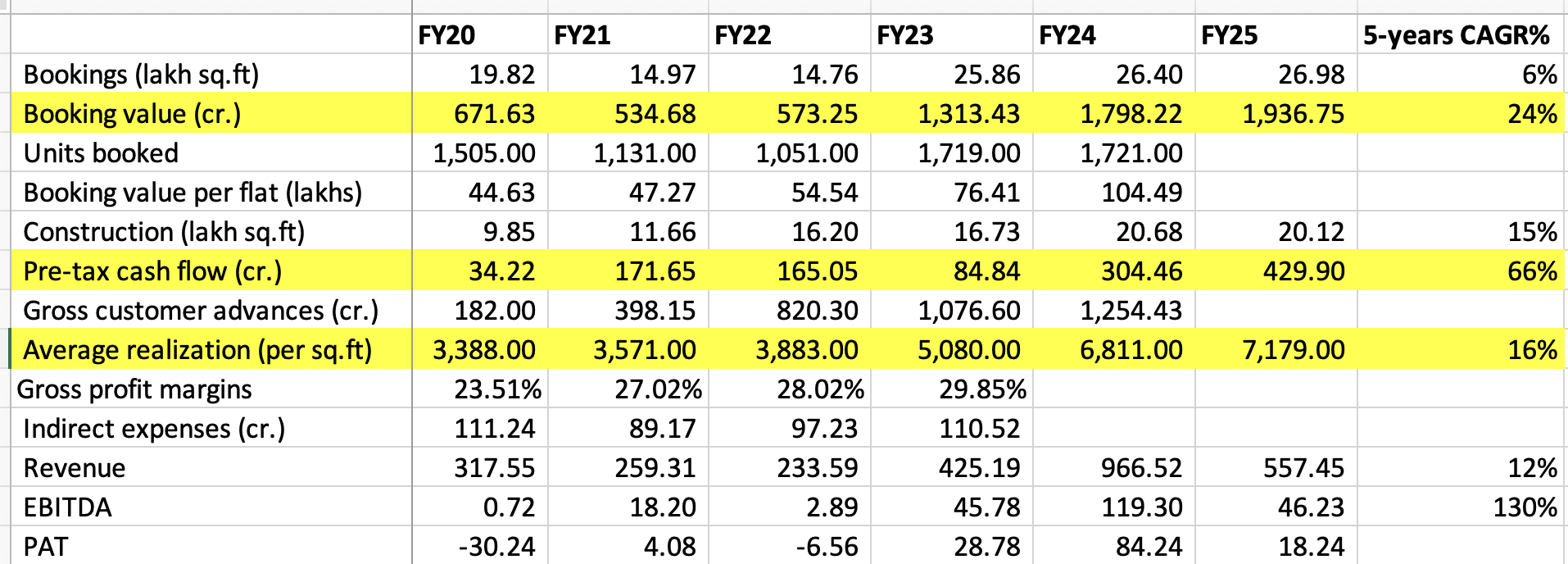

If we zoom out a bit, in last 5-years Ashiana has grown volumes by only 6% CAGR, but realizations have grown at 16% CAGR, reflecting a change in product mix (e.g., more sales in Gurgaon) and higher price realizations in their existing projects. Pre-tax cashflows has ballooned, growing at 66% CAGR! All these cashflows should be realized in terms of P&L in next few years (hopefully ![]() ). Q4 concall notes below.

). Q4 concall notes below.

FY25Q4

- FY25 launches: Ashiana Amarah Phase-4 and 5 in Gurugram, Ashiana Malhar Phase-3 in Pune, Ashiana Advik Phase-2 in Bhiwadi, Ashiana Ekansh Phase-4 and Nitara Phase-2 and 3 in Jaipur, One44 Phase-2 in Jaipur, Ashiana Amodh Phase-2 in Pune, Ashiana Swarang Phase-1 in Chennai

- Q4 launches: Ashiana Amarah Phase-5 in Gurugram, Nitara Phases 2 and 3 in Jaipur

- FY26 planned launches: Ashiana Aaroham in Gurgaon (greenfield, Q3FY26), Ashiana Amaya in Jamshedpur (greenfield, Q3FY26), Jaisingpura in Jaipur (greenfield, Q4FY26), remaining will be phase launches. One legacy project in Jaipur (Aravali ~1 lakh sq.ft) was stuck in regulatory issues and should be launched in FY26

- FY26 Presales target: 2000 cr.

- FY26 sales ~ 1200 cr. with lower EBITDA margins because of delivery of low-margin projects (Anmol, Shubham, Malhar). Will see strong margin improvement in FY27. On an economic basis, ROEs are already good

- Current pipeline: 17.31 lakh sq.ft in ongoing projects + 2.53 lakh sq.ft finished inventory + 38 lakh sq.ft in future projects + 25.6 lakh sq.ft in land (excluding Milakpur) ~ 83.44 lakh sq.ft (vs 114 lakh sq.ft in FY24)

- In terms of sales value, 2000-2500 cr. of inventory in unlaunched phases of existing projects + 2000-2500 cr. in three land parcels (Aaroham + Jaisingpura + Ashiana Amaya). In terms of unrecognized revenues (from presales), its ~4515 cr. and PAT margins should be 14-15%

- Senior living:

o Presales of 360 cr. in FY25 (vs 300 cr. in FY24). This was 100 cr. five years ago.

o Senior living is 33% of salable area pipeline currently, will be deploying significant capital in this. Focusing on Pune, Chennai, Bangalore, Mumbai, NCR

o Ashiana Amodh (Pune/Talegaon): Able to increase prices in Phase-2 to 8,000+/sqft

o Ashiana Swarang (Chennai): Increased prices to 9,000+/ sq.ft

o Two recent transactions: One in Panvel (outright buy, 7 lakh sq.ft) and one in Bangalore (development agreement), transactions are yet to be concluded

o Seeing announcement from other cos to enter this space, however only comparable project is Antara in NCR

o As they charge a pricing premium in senior living, they can launch projects in cities where land costs are higher - Ashiana Amarah Phase-5 is at Rs. 15,000/sq.ft. Phases 3-5 have better specifications than Phases 1 and 2. Do expect some competition in sales when they deliver Amarah Phases 1 and 2 because of the huge price rise, however confident that demand is enough to absorb these supplies

- Ashiana Aaroham (Gurgaon): Q3FY26 launch (11 lakh sq.ft, 1/3rd should be launched in Phase 1). Should be very profitable because land prices have increased a lot

- Advik Phase-2 slowed a little because they were launching building separately, from a sales perspective, they launched it in two pieces. From presentation it looks like Bhiwadi sales were very low in Q4FY25 (is demand hit?)

- Their current pipeline is sufficient until FY30.

- Construction cycle for a project of 10 lakh sq.ft is ~5 years

- Land prices are elevated in NCR and Jaipur. In Bhiwadi, no other developer is able to sell at a price which covers even construction cost, but land prices keep going up

- In Jaipur, to make sense of current land prices, price point for flats should be 30% higher

- Lower recognized revenues due to delays in delivery of Advik Phase-1, Anmol Phase-2 and Shubham 4B, these are shifted to FY26

- Their general plan is to sell 20% at launch, and 25% each year

Disclosure: Invested (no transactions in last-30 days)

11 Likes

View of Vishal Bhargava on Gurgaon real estate. Found him knowledgeable wrt to real estate markets in India.

Has anyone looked at the details of the case filed by consumers against Ashiana. Are the grievances genuine?

1 Like

Ashiana delivered good quarter results.

PAT at 28 cr versus -8 cr loss last year. QoQ growth more than 100%.

PAT of 28 cr includes one time income of 3 cr. So removing that it comes to be 25 cr which on a sales of 166 cr comes out to be 15% pat margin which is a significant improvement.

Ashiana Advik was the higher margin project delivered this quarter. Management is walking the talk finally about the Roe’s and margins improving.

On concall management was confident of reaching a double digit pat margin for full year. So if I take the full year sales of 1200cr, and pat margin of 10%, pat in fy26 comes out to be 120 cr at least. And it should only improve from here.

FY28 planned deliveries are 2500cr and mangement was confident of mid to high teens profit margins by then, which gives us a rough pat estimate of 375 to 450 crs. I love real estate companies because we get the numbers 2 to 3 years in advance, provided there are no hiccups in executions and deliveries.

So company is basically trading at FY28 PE of 7 to 8 in this overheated market which had more than 150 ipos in the last 3 months. Oh how I love the efficient markets. Or maybe the market is pricing in some risk which I’m unable to foresee.

Disc: Invested. Would love to buy more but already forms around 30% of portfolio

3 Likes

Agreed, I’ve been tracking Ashiana for a while now. FY’28 should be a bumper year with ~400+ crs profit. What are your return expectations though? Do you feel like the company should trade at atleast ~6K Mcap in a year or maybe even higher?

Also how are you comfortable taking 30% position in a single stock, what kind of risk analysis have you done?

Disc. Invested

I am not sure how much of the valuations are dependent on the launches… Has anyone evaluated real estate companies based on the TTM / NTM launches…

Because by FY28, if real estate gets into a down cycle then we may not realize any upside.

Adding my notes from last few quarters

FY26Q1

- Project Realizations

o Gurgaon: Amarah Phase 5 (59 units; 1.05 lakh sq.ft; 158.96 cr.; 15,140/sq.ft)

o Jaipur: Aravali (30 units out of 60; 0.745 lakh sq.ft; 56.26 cr.; 7,552/sq.ft)

o Jaipur: Nitara Phases 2 & 3 (295 units; 3.97 lakh sq.ft; 174.35 cr.; 4,392/sq.ft)

o Bhiwadi: Tarang Phase 6 (117 units out of 192; 1.457 lakh sq.ft; 68.23 cr.; 4,683/sq.ft) - Lower margins in deliveries (Anmol) as compared to deliveries (Amantaran) in Q4FY25

- Q1 launches: Tarang Phase 6 (Bhiwadi), Aravali (Jaipur, single phase)

- Remaining low margin projects: Anmol Phase 3 and Malhar

- Uunsold inventory is quite limited for deliveries in FY26 and FY27. For FY26 deliveries, 47cr. of unsold inventory

- Targeting 500 cr. of presales for senior living in FY26 (on track)

- Have 125 cr. of unused credit from IFC

- For FY26 to FY30, cumulative recognized sales should be 10,000 to 12,000 cr. with cumulative profits of 2,000 cr. (~18% PAT margins). PAT margins will be lower than 18% in FY26 and can reach 15-20% in FY27

FY26Q2

- Q2 PAT margins of ~15.6% due to delivery of higher-margin projects: Advik and Tarang (+ ~3 cr. one-time contribution from resolution of disputes in Maitri). Will deliver double digit PAT margins in FY26

- Targeting 2000 cr. presales in FY26

- Q2 launches: Swarang Phase 2 (Chennai)

- Settled disputes in Project Maitri (Kolkata) and received 18.50 cr. as final settlement against security deposit of 12.80 cr. and other expenses

- Ashiana Aaroham (Gurgaon) funded by IFC (100 cr.) – to be launched in Q4FY26. Early sense on sales is quite positive (will be in 3 phases)

- Pace of realization increase has slowed down, sales velocity in Amarah Phases IV and V have slowed down because of much higher realizations (sales velocity of 30,000 sq.ft+ is good, their inventory is 3.37 lakh sq.ft in Phase IV + V and is planned to be delivered in 10 quarters)

- Ashiana Amaya (Jamshedpur) will be launched in Q4FY26

- Acquired 22.71 acres on perpetual lease at Mahindra World City in Chennai to develop a Senior Living project adjacent to “Ashiana Vatsalya,” (15 lakh sq. ft. saleable area and 1200 cr. sales)

- Excluding Gurgaon and Malhar where sales largely come from channel partners, their reference sales are ~50%

- 200 customers went to customer forum (NCDRC) from Ashiana Town Beta (Bhiwadi) for deficiency in service and unfair trade practices and have asked for 54.88 cr. in compensation (project executed in 2013-2018). Ashiana has contested it (and were surprised) and they will fight it out in the court. Management thinks that the township is well run and were caught by surprise

Disclosure: Invested (no transactions in last-30 days)

2 Likes

Disclaimer: holding and biased. Bought at 250 earlier and that prices never came back to buy further.