Here are my notes from their FY21Q3 concall. Overall, sales numbers are starting to improve, cashflow visibility is very high allowing management to be more aggressive in deals. They have clearly addressed what went wrong in Gurgaon and Bhiwadi in the last down cycle (too high land prices paid). Management believes that we are at the beginning of a residential real estate recovery cycle.

- Majority of projects that were launched in the past 1-2 years will be completed in the next 8-10 quarters, leading to improved cash position. 9MFY21 cashflow numbers should sustain going ahead. Ashiana will be more aggressive in signing new projects due to improved cashflow visibility

- Deal terms with land owners have become better, land market has started hardening (i.e. prices have started increasing) in the past couple of months

- Ashiana Malhar (Pune): MOU was done and deal was closed in August 2020. Currently environmental approvals and building plans are under approval. Hope to have launch in FY22 (hopefully early part). Pune in general is a low margin fast moving market

- Ashiana Shubham (Chennai) has realizations of 4200/sq.ft and Anmol (Gurgaon) has realization of 4500–4900/sq.ft. Higher sales in Shubham and Gurgaon have increased overall company level realizations. Chennai – have been able increase prices. In Gurgaon, have not been able to increase prices yet.

- Real estate market in NCR has changed to a buoyant mode. Strategic change to drive sales in NCR has been partnership with third party consulting firms like anarock, additional relationships with the broker community. Should be able to clear most ready inventory in Anmol by Q1FY22. January has gone very well in Anmol. Hope to have closure on 2 projects in NCR market by next quarter. Costs involved to sell in Gurgaon make Ashiana business model unsustainable

- Anmol: Because Ashiana paid higher land prices, gross margins are very low leading to very low ROE.

- Bhiwadi mistake: too much capital was spent on land acquisition in the last upcycle. Will be more careful this time around

- Kolkata: No outlook to do any more transactions

- Chennai: In advanced discussions (term sheet not yet signed)

- Have a hit ratio of 1 in 3 i.e. 1 of 3 signed term sheets deals go through

- Jaipur and Jamshedpur: can sell at much lower cost in relation with sales compared to a market like Gurgaon.

- Noida: Senior living project term sheet in Greater Noida, hope to have it done soon

- Senior living: Enjoys higher margin and has much higher returns. Should contribute to 40% of organization profitability going forward (and 25-30% to sales). For that, Ashiana has to create a major preference in Chennai, NCR, Pune and Mumbai markets as these are the major senior living markets. Bhiwadi (Ashiana town Gamma): Plan is to move entire Ashiana town Gamma to senior living

- Kid centric home: Currently most kid centric projects that Ashiana has executed have been retrofitted. Ashiana Umang (Jaipur) has been successful in kid centric home where houses were not retrofitted and provides a model that Ashiana wants to pursue. They are currently evaluating one particular project in NCR with a clean slate design and not retrofitting.

- Focus markets: Jaipur, NCR, Chennai, Pune

- IFC platform: To fund new land purchases. Otherwise, looking for joint project development

- Poor ROE for most real estate players: because of higher land costs leads to lower ROEs. Ashiana wants to only do land transactions which give a certain ROE (pre-tax IRR threshold is mid 20s i.e. close to 25%), which also means low number of deals. However, what matters more is the conservative and reasonable nature of the underlying assumptions behind the IRR rather than the actual IRR number

- With the current management setup, can do 2.5-3mn sq.ft/year. Sales should be >2mn sq.ft in FY22. Expect margins to expand going forward. Hope to get to mid-teens ROE in next 3-years. Want to create a floor on ROE in the next downcycle (how?)

- No new project launches in FY21, its mostly been additional phases in existing projects. For FY22, most launches will be on similar lines i.e. new phases in existing projects.

- Longer term plan: to create an annuity income stream from commercial real estate? Or provide contract manufacturing? NOPE!

Disclosure: Invested (position size here)

Does anyone have any insights or sources (apart from management commentary) on the Bhiwadi real estate market? It seems a lot of Ashiana’s current & future inventory is in Bhiwadi.

But, have you arrived at a valuation for the company?

IMHO, the investment thesis for Ashiana is PRIMARILY based on a turnaround in the real estate cycle, which according to most people should happen soon. The current selling rates are too less for Ashiana (or for that matter any real estate developer) to get decent profits. A turning real estate cycle means two things: Increase in Selling Price/Sq ft and higher sales velocity.

People have been correctly pointing out that a lot of their saleable inventory is in Bhiwadi. While it will be great if Bhiwadi starts selling well again, but this point can be (SOMEWHAT) addressed if the management gets new projects in other markets that they operate in and they are indeed trying to do the same.

However, the most important part of the thesis is improvement in selling prices.

Hence the valuation and the entry point in this stock will be based on your personal call as to when the cycle will turn.

19th Mar 2021

Ashiana Housing has received approval to raise Rs 120 crore through Non-convertible Debentures/ Bonds (secured/ unsecured) on Private Placement basis. The Board of Directors of the company in its meeting held on March 19, 2021 has considered, discussed and approved the same.

Ashiana Housing is a real estate development company. It is engaged in building residential and commercial projects. The firm also offers retirement resorts, group housing, hotels, retail and facility management.

The first land transaction for FY22 (of the 3 planned this fiscal), proposed acquisition of 22.1 acres in Wazirpur, Sector- 93, Gurgaon Manesar Urban Complex, Gurgaon (anyone has insights into this area?). The potential saleable area for this project will be 21 lakh sq ft, with a floor space index of approximately 17 lakh sq ft. This transaction will partly be funded by issuing NCDs and is expected to finish this quarter.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/bec04902-9410-4cd3-a711-4fb0ddbc60af.pdf

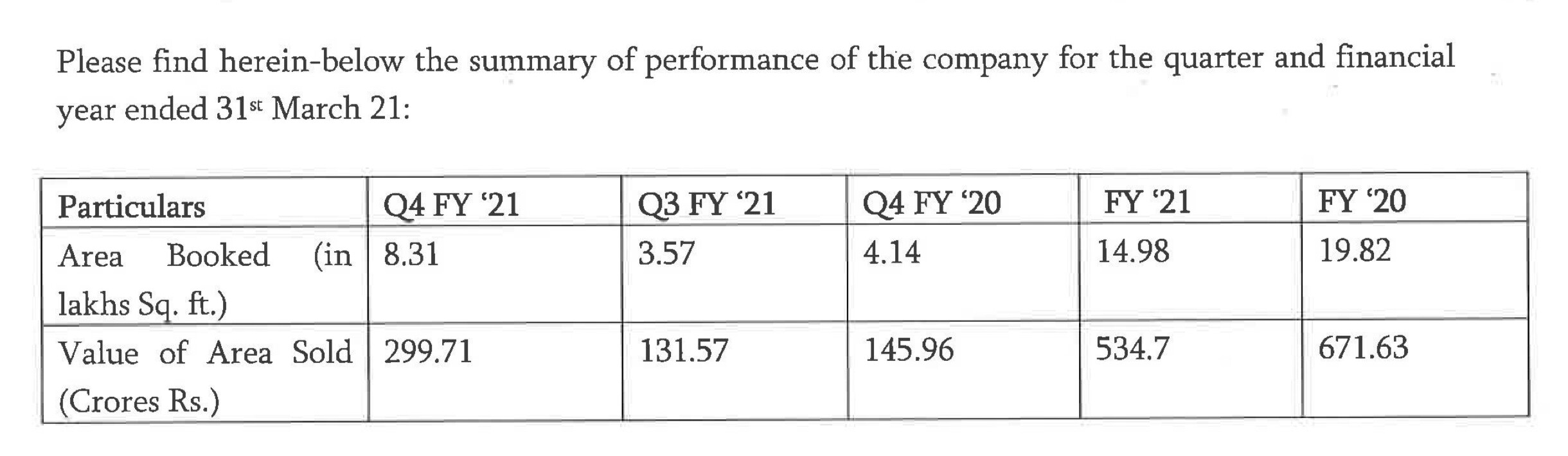

FY 21 Q4 results

Ashiana Housing has acquired 22-acre land in Gurugram from Ramprashta group for about Rs 170 crore to develop a residential project. Recently, the company entered into a development agreement to build a 12-acre residential project for senior citizens in Pune on a revenue-sharing basis.

Here are my notes from today’s concall.

- Chennai: Hopefully should be able to close a couple of transactions in the next year, have been scouting for last 1.5 years

- Ashiana Anmol (Gurgaon): Strategic partnership with Anarock really helped in driving sales

- Kolkata: Still stuck

- Jamshedpur: Have very strong brand equity in Jamshedpur which is why sales have been concluded so quickly. Problem is generally in acquiring good title land

- Bhiwadi: Shifting it more towards senior living (Gamma has been already shifted). Senior living is getting traction in the Bhiwadi market and also getting very good realizations. So Bhiwadi will become more of a margin play rather than volume play

- Noida: Still doing diligence on regulatory risks

- Focus markets for new transactions: Jaipur, Jamshedpur, Chennai

- 20-year IFC NCD: Linked to return on the project (quasi-equity, no fixed return terms, not purely equity)

- Margins were positive impacted through reduced overheads and savings on marketing costs

- Higher collection across projects led to higher pre-tax operation cashflow in FY21 (171.65 cr. vs 34.22 cr. in FY20). 1’131 flats sold in FY21 vs 1’505 in FY20

- Expect launches of 1.5mn sq.ft in FY22. Expect 2.5-3mn sq.ft launches in FY23 onwards. 4 new planned launches at the end of FY22 or in early FY23. New launches will be in Pune, Gurgaon, Bhiwadi and Jaipur

- Gross margins are ~ 1’000/sq.ft for on-going projects. New launches should see further improvement in gross margins over 1’000/sq.ft. There is not much difference in gross margins for bigger sized flats

- Cost breakup: 15-20% land cost, 40-50% project costs of sales. Commodity cost impact? 60-65% of construction cost is materials price making 30-35% of overall sale value

- Expect apartment prices (or realizations) to increase going forward given they have lagged CPI for the last 14 years (expect 10-15% increase yearly). 1.5% increase in blended prices in FY21. Supply side dynamics is very favorable due lower number of new launches in the last few years. Expect the start of a 5-6 year bull market in residential real estate

- In the last 2-weeks of June, things are coming back to normal (in terms of demand and sales)

- Land prices have inched up in the last 6 months for FY21. Continue to focus more on JVs and on city outskirts where impact of land prices is lesser

- Halol as a strategy failed, Jodhpur has also not delivered results up to mark, Jaipur worked very well. Idea is to see where the bet is paying off and scale up in that market

- For non-senior housing in bigger cities, Ashiana has to go to distributors to bring in customers to the project. However, customers will still be handled by the in-house sales team

- Revenue recognition should be much higher in FY23 when deliveries will be kicking in

- Split b/w investor and end user demand currently? Broadly 50-50, long term investor demand (especially people who rent out properties) never evaporated

- Any plan to foray into Ranchi market? More from the softer side, scouting for sites. Nothing in advanced stage yet. Generally harder to operate in Eastern India

- Will be happy to sustain OCF over 100 cr. which will cover construction costs that should be higher going forward

Disclosure: Invested

NCR housing sales news

Here are my notes from FY22Q1 concall.

- Launched Phase III of Ashiana Tarang (Bhiwadi) and Phase IV of Ashiana Dwarka (Jodhpur) during the quarter

- Detected fraud of 2.37 cr. at one of its sites (accounting fraud on the payable side)

- Vrinda Gardens (Jaipur): Sales have picked up substantially in July. Project has been constructed faster than expected, will have a little bit of inventory at project completion but not of a material size to put stress on the balance sheet. This has been one of the slowest moving projects in Jaipur

- Jaipur: High land prices have stopped them from new projects in the last couple of years

- Ashiana Amara (Gurgaon): Kid-centric homes (~21 lakh sq.ft). Expect to launch in the next 9-months after getting RERA approval (Q4FY22 or Q1FY23). This project has been designed as kid-centric from the scratch rather than retro-fitting. Have spent a lot of time in designing this project (~3 years). Funded substantially from IFC money

- IFC fund usage: Ashiana Amara, Ashiana Daksh and evaluating one more project in Chennai. Only comes in outright land purchase deals

- Sales are back to normal levels post Q1 lockdown, pricing has improved with price hikes across projects (~3% from Q4FY21). Current price hikes are enough to maintain gross margins

- Expect 1.5mn sq.ft launches in FY22

- The large amount of cash accruals in the last fiscal has led to lots of discussion on land and new projects. Currently have four signed term sheets (1 in Jamshedpur)

Disclosure: Invested

Here are my notes from their AR.

- Theme of the annual report is “Need for speed” – finish construction of 2mn sq.ft in FY22

- Provides rental and resale services through a dedicated team

- Post-delivery NPS score of 33

- Referral sales were 55% of total sales

- Ranked #1 senior living brand (fourth consecutive time) and among top 10 real estate brands by Track2Realty

- Successful launch of Ph-4 of Ashiana Shubham (Chennai), Phase-V of Vrinda Gardens (Jaipur), Ph-3 of Ashiana Daksh (Jaipur), Ph-5 of Ashiana Umang (Jaipur) and complete sale out of Ph-2 of Ashiana Aditya in Jamshedpur

- Witnessed good demand across projects in Jaipur, Jamshedpur, Bhiwadi, Chennai and Sohna (Gurgaon)

- Targeting 15 lakh sq.ft of launches in FY22

o Plan to launch Ph-2 in Ashiana Anmol (Sohna, Gurgaon) due to very good sales supported by strategic partnership with Anarock

o Plan to launch Ashiana Amarah (Gurgaon) in Q4FY22 or Q1FY23

o Plan to launch Pune senior living project subject to regulatory approvals - Land deals

o Acquired 22 acres land parcel in Gurgaon (21 lakh sq.ft, Ashiana Amarah) with IFC as a co-investor.

o Signed a new land deal in Varale (Pune) in June for a Senior Living project which a potential saleable area of around 9 lac sq ft

o Looking for land acquisition opportunities in Jaipur, Chennai, Pune and Gurgaon - Looking for senior citizen projects in Noida/Greater Noida

- Senior living projects have done well in Bhiwadi and Chennai. The Lavasa senior living hasn’t done very well

- Comfort Homes category is largely concentrated in Jaipur, Bhiwadi and Jamshedpur.

- Jaipur as market has been doing exceedingly well. The latest 2 project launches in Jaipur i.e. Ashiana Daksh and Ashiana Amantaran, both from comfort homes Category have shown strong performance in terms of sales.

- Generated operational cashflow of 171.65 cr. (vs 34.22 cr. in FY20)

- Raw material inflation: Have already started increasing prices in few projects

- Number of permanent employees: 524 with 52% in company for >5 years and 25% for >10 years; Median salary: 3.36 lakhs (no increase in salary of employees or managerial personnel)

- Maintenance & hospitality revenue: 43.98 cr. (vs 49.12 cr. in FY20). Café’s sales crossed 20 lakh/month benchmark regularly even with limitations of covid situation

- Advertising and business promotion expense: 17.4 cr. (vs 28.28 cr. in FY20)

- Land bank: 71.69 acres (Bhiwadi: 40.63, Kolkata: 19.72, Pune: 11.34)

- Gross profit: 931 / sq.ft (vs 853 in FY20). Partnership Profit was at 316 / sq.ft.(vs 300 in FY20)

- Number of shareholders: 20466, price (low): 39, price (high): 150

- Tax disputes: 11.75 cr.

- Auditor remuneration: 56.88 lakhs (vs 73.82 lakhs in FY20)

Below are the detailed financials for the last decade.

| FY11 | FY12 | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Bookings (lakh sq.ft) | 13.50 | 17.83 | 18.65 | 22.13 | 18.12 | 8.63 | 6.96 | 6.93 | 10.79 | 19.82 | 14.97 |

| Booking value (cr.) | 277.00 | 390.00 | 503.00 | 648.00 | 548.00 | 284.00 | 225.00 | 217.00 | 332.00 | 671.63 | 534.68 |

| Units booked | 1’015.00 | 1’298.00 | 1’346.00 | 1’673.00 | 1’477.00 | 668.00 | 533.00 | 526.00 | 810.00 | 1’505.00 | 1’131.00 |

| Booking value per flat (lakhs) | 27.29 | 30.05 | 37.37 | 38.73 | 37.10 | 42.51 | 42.21 | 41.25 | 40.99 | 44.63 | 47.27 |

| Construction (lakh sq.ft) | 10.74 | 14.62 | 12.27 | 17.87 | 22.80 | 23.44 | 17.39 | 8.16 | 7.68 | 9.85 | 11.66 |

| Pre-tax cash flow (cr.) | 53.50 | 109.70 | 83.81 | 125.90 | 72.58 | -10.89 | -32.90 | -20.21 | 16.41 | 34.22 | 171.65 |

| Gross customer advances (cr.) | 120.00 | 244.00 | 90.00 | 267.00 | 571.00 | 379.00 | 320.00 | 240.00 | 164.00 | 182.00 | 398.15 |

| Average realization (per sq.ft) | 2’055.00 | 2’190.00 | 2’699.00 | 2’926.00 | 3’022.00 | 3’293.00 | 3’234.00 | 3’135.00 | 3’082.00 | 3’388.00 | 3’571.00 |

| Gross profit margins | 32.82% | 34.43% | 38.69% | 37.89% | 34.13% | 23.51% | 27.02% | ||||

| Indirect expenses (cr.) | 51.19 | 78.32 | 85.7 | 95.90 | 109.44 | 111.24 | 89.17 | ||||

| Revenue | 154.30 | 249.00 | 161.40 | 122.80 | 164.40 | 536.00 | 397.02 | 334.92 | 350.63 | 317.55 | 259.31 |

| EBITDA | 58.50 | 89.70 | 47.70 | 31.80 | 59.00 | 150.60 | 106.02 | 68.00 | 47.26 | 0.72 | 18.20 |

| PAT | 43.90 | 69.60 | 33.20 | 21.90 | 46.50 | 129.40 | 67.01 | 38.23 | 13.78 | -30.24 | 4.08 |

| Tax (cr.) | 2.56 | 10.34 | 24.47 | 10.51 | 10.17 | 6.51 | |||||

| Dividend (per share) | 0.35 | 0.45 | 0.45 | 0.50 | 0.50 | 0.50 | 0.25 | 0.25 | 0.25 | 0.30 | 0.40 |

| Share capital (cr.) | 18.61 | 18.61 | 18.61 | 18.61 | 20.47 | 20.47 | 20.47 | 20.47 | 20.47 | 20.47 | 20.47 |

| Equity raise (cr.) | - | - | - | 200.00 | - | - | - | - | - | - | |

| Net worth (cr.) | 175.00 | 239.60 | 268.10 | 284.50 | 522.80 | 646.10 | 722.70 | 765.80 | 781.80 | 749.79 | 750.80 |

| Book value increase | 36.91% | 11.89% | 6.12% | 83.76% | 23.58% | 11.86% | 5.96% | 2.09% | -4.09% | 0.13% | |

| Long term debt (cr.) | 0.30 | 10.60 | 11.10 | 9.10 | 33.00 | 57.60 | 78.10 | 63.40 | 142.70 | 103.77 | 46.59 |

| ROE | 25.09% | 29.05% | 12.38% | 7.70% | 8.89% | 20.03% | 9.27% | 4.99% | 1.76% | -4.03% | 0.53% |

| EBITDA margin | 37.91% | 36.02% | 29.55% | 25.90% | 35.89% | 28.10% | 26.70% | 20.30% | 13.48% | 0.23% | 7.02% |

| PAT margin | 28.45% | 27.95% | 20.57% | 17.83% | 28.28% | 24.14% | 16.88% | 11.41% | 3.93% | -9.52% | 1.57% |

Disclosure: Invested (position size here)

FY22Q2 concall

- Purchased land in Chennai (senior living; Mahindra World city) and Gurgaon (Ashiana Amarah)

- Will close another land transaction for senior living in Chennai in Q3FY22

- Pune: 1 senior living + 1 regular housing project

- Undertook price increases in all projects except normal housing in Bhiwadi. In Bhiwadi, undertook price increases in senior living projects. Expect to have price increases higher than cost increases going forward

- For next 18-24 months, have enough projects to maintain annual sales of 2mn sq.ft run rate

- Need higher number of projects in Jaipur to fulfill growth, land prices have increased significantly

- Approval generally takes 12-15 months from land transactions

- Launched Phase II of Ashiana Anmol (2.8 lakh sq.ft)

- FY22 sales will be lower than 2 mn sq.ft

Disclosure: Invested (position size here)

A decent quarter, company is building up its pipeline that can lead to pre-sales of 2.5-3 mn sq.ft going forward. Need more projects in Jaipur to fulfill growth ambitions.

FY22Q3 concall notes

- In the past few years, company has been able to increase prices in senior living housing in Bhiwadi and Chennai (especially Chennai where price increases have been high)

- Have been able to pass on construction price increases in current projects (sales/sq.ft has gone >4000 for the first time). Margins should actually expand thereby more than covering construction price increases, however they are unsure of passing full increase in land prices. In Jaipur, current land prices are factoring in 10% higher final selling prices per sq.ft

- Have enough projects (except in Jaipur due to high land prices) to do 2.5-3 mn annual pre-sales run rate. Out of the 7-8 planned launches in FY23, 6 should be enough to fulfill this pre-sales run rate

- Targeting 15% ROE on consolidated level. This number should be met (on a reported numbers) in FY23. Not sure if it will sustain after that. This answer will be clear in FY23

- Cost of debt has come down to ~10% (improved from 12-13% a couple of years back). Ideally, customer advances pay for construction cost

- Hoping to finish inventory of Ashiana Town in next 24 months

- Land acquisition funding sources: Jamshedpur + Jaipur + Pune => JV route; Gurgaon => IFC financing + ICICI bank debt; Chennai (Mahindra World City) => Purchased through internal funds as IFC had some regulatory issues in deploying funds, this should get resolved by April and IFC should be able to finance this land purchase. One of the Chennai project is JV with Arihant

- Gurgaon: Sohna project doing well in terms of brand building, margins are very low due to higher land prices paid earlier. Ashiana Amarah should give better financial results, very confident in their design for this project

- Pune: Lot of legwork required, first project is regular housing. Using channel partner for sales (similar to Gurgaon model)

- Kolkata: No resolution yet, no planned launches

- Older projects are doing 25-27% of gross margins (lower than 30% target). The newer projects should work at 30% gross margins given the land prices paid. Looking for projects of value where Ashiana is able to make it work where other players are not interested

- Implementing a new ERP system (Far vision) and appointed Grant Thornton to improve internal controls

- Apart from Milakpur (3.1 mn sq.ft) and Kolkata project (1.5 mn sq.ft) which are stuck, the other existing projects (~7.1 mn sq.ft) along with existing inventory (~1 mn sq.ft) should be exhausted in a 6 year time frame

- Annual fixed cost excluding SG&A but including finance and depreciation is ~65 cr.

| - | Selling costs: |

|---|---|

| o | Chennai: Selling cost has come down from 8% of sales to 4% |

| o | Gurgaon: Selling cost per unit of sales should come down in Amarah project |

| o | Pune: Should see increase in selling costs because it’s a new market |

Disclosure: Invested (position size here)

07.04.2022 (CNBC awaaz interview)

- Witnessing very strong demand across markets

- Market can easily absorb 10-15% increase in overall sales value, however 15% increase might not be enough given even land prices are increasing significantly

- Company is planning to increase prices by 10-15% in FY23. Company will increase prices by 5-7% over the next 45 days with the remaining being passed over next. However, this price increase is mostly to cover increase in costs (and not for increase in ROCE)

- Increased prices by 6-8% in FY22 (in tranches). There was no demand destruction because of this

- Gurgaon sector 93 launch: Kid centric housing (1200 flats) with total sale value of 1200-1300 cr.

- Targeting 1100 cr. presales in FY23 (2x of FY21)

Disclosure: Invested (position size here, no transactions in last-30 days)

Company is targeting 1100 cr. of pre-sales in FY23 (vs 573 cr. in FY22 and peak of 672 cr. in FY20). On a reported basis, ROE will be in early double digits implying PAT of 80-100 cr. Their overall pipeline is of 110 lakh sq.ft giving visibility for next 3-4 years and the land bank is currently on the lower side. They need to do more transactions for growth beyond FY24. Concall notes below.

- 25-30 lakh sq.ft launches planned in FY23 (15-20 lakh will be new greenfield projects and remainder will be phase extension of existing projects)

- Targeting 1100 cr. presales in FY23 (aspirational figure, confident of doing 1000 cr.), environment is currently very positive. Gurgaon should be >25% of sales (existing Anmol project Phase II + Phase III which will be launched in FY23 + Amarah). Will probably cross realizations of 4500 / sq.ft

- Will only reach double digit ROE on reported basis in FY23 (and not mid-teens)

- 3 greenfield projects will be launched in H1FY23 (RERA filed; can get delayed to Q3FY23) and 3 in H2FY23

- When construction is quick, raw material price escalation doesn’t impact significantly (e.g. Daksh, Aditya). In Amantran Phase II, got hurt due to commodity price escalation

- Can have gross margin compression in next 1-2 years. However, expect expansion in net profit margins in 3-5 years

- Target gross profit margin (sales – land cost – construction cost - project overhead cost which includes regulatory cost, project interest, etc.) of 30%. In construction, material cost ~ 70%, labor ~ 20%, site overheads ~ 10%

- Land costs have ballooned in last 3-4 months because of higher demand for plotted development, happy to have locked in land prices 6-8 months back. Seeing frothy land prices in Jaipur. Scouting for land in Gurgaon, Jaipur, Jamshedpur

- Current pipeline: 10 lakh sq.ft in ongoing projects + 70 lakh sq.ft in future projects (of which 25-30 lakh sq.ft will be launched in FY23) + 38.94 lakh sq.ft in land ~ 108.94 lakh sq.ft

- Have to work on project pipeline beyond FY23/24. Current pipeline is 10/11 mn sq ft majority of which majority has realizations >4500 implying potential sale value of 4500-5000 cr. This is enough for 3-4 years

- Lot of capital will be released from underperforming projects (like Ashiana Anmol). Have enough capital for the next few years, currently land prices is a challenge rather than capital availability

- FY23: Looking to spend 200 cr. in acquisitions or JVs (prefer JVs as its more capital efficient)

- Chennai: Have achieved revenue, profit and ROCE targets

- Gurgaon: FY24 onwards should start hitting minimum profit threshold and ROCE

- Pune: Not able to get projects off the ground, don’t have clear visibility on when company will hit profit target

- Conventionally have targeted 5-7 years of land banking. Currently, due to higher land prices feel that land bank might go below 4 years (in order to maintain ROEs). Current thought process is to maintain and improve profitability (and 15% ROE) rather than sell more sq.ft. Organization is geared up for 2.5-3 mn sq.ft sale

- Kolkata project is still stuck, looking for opportunities to sell the land

- Indirect/other expense breakup: 66 cr. (18-20 cr. are selling expenses which are booked at time of delivery). Finance costs should reduce going forward

- Selling expenses are generally ~4.5% of sales

- Booking value per flat has gone up to 54 lakh from 40 lakhs since FY19 (30-35% increase). This is a function of changing mix (average flat area has increased from 1250 sq.ft to 1300-1400 sq.ft and project mix has also changed towards higher realization markets like Gurgaon). Till now, margins have not benefitted. Currently, the projects being sold are at higher margins which will only be visible in number in FY25/26

- JVs: At lower gross margins (can go to 20-24%) but much higher ROCE

Disclosure: Invested (position size here, no transactions in last-30 days)

Good set of results from the company, they are very confident of exceeding 1000 cr. in pre-sales. Now the pipeline and RERA approvals are also falling in place and sales velocity seems to be strong. My concall notes are below.

FY23Q1 concall

- Learnings from Sohna project (Ashiana Anmol): Takes 5-6 years to create a brand in a new market + need to be agile with marketing strategy such as engaging with channel partners for sales. They adopted this model in Nov 2019 and since then project kicked off

- Ashiana Amarah: Child centric amenities + spaces are lavish + thoughtful design from scratch. Positioned as an aspirational project. Have received RERA approval for phase I and will be launching in a couple of weeks. Will use channel partner network for bringing in customers, but sales will be taken by own team

- Jaipur: Land prices haven’t fallen, hopeful to do a couple of land transactions in next 8-10 months

- Goal for company is to reach 15% ROE which is still sometime away, double digit ROE looks reasonable and likely

- More supply is coming in plotted layouts in Jaipur and Gurgaon and not in apartments. Do not see supply side challenges for Ashiana (maybe in Pune supply can be an issue in 2-3 years)

- RERA approvals have been secured for Ashiana Amarah Phase I, Advik Phase I (senior living Bhiwadi), Ashiana Malhar in Pune (has also been launched for EOI)

- FY23 launches: 12-13 lakh sq.ft of greenfield projects + 13-14 lakh sq.ft as phase extensions in existing projects (so in-line with >25 lakhs sq.ft)

- FY23 target: Targeting 1100 cr. of pre-sales. Sales velocity is not an issue, need 2 more RERA approvals (1 in Jaipur, 1 in Jamshedpur) to meet pre-sales expectations. Overall pipeline (excluding stuck projects) is around 6000 cr. and current view is to maintain 1000 cr. annual run rate

- Maintaining gross margins of 25-30% in current sales with some projects even doing 40%+ gross margins (e.g. Ashiana Nirmay). On a broader basis, 40-55% of sales goes into construction costs

- Senior living: Don’t see lot of competition + end market is growing

- IFC credit line is more or less exhausted, don’t see the need for debt for reaching 15% ROE. Very conservative in debt

Disclosure: Invested (position size here, no transactions in last-30 days)