I had sent out a query to some senior investors. Here’s the query and a brilliant throught-provoking response received from a very respected senior and VP well-wisher.

_

)-----_

Sir,

Need guidance - to take our ART of Valuation discussion forward. [Link]

How do the best investors think about the right valuation for an emerging business (and therefore the gap) before consensus emerges about that business in the market?

)-----

Interesting thoughts, with very good insight.

I have no idea how good investors make their decisions because Iâm not yet there but I can say for myself. I have never penned my thoughts on this but when looking at emerging stocks, two things I mentally get a hang of are:

1.How does this company make money

2). What can go wrong for this business.

I will not discuss (2).

On (1), I sort of mentally slot where the stock belongs to - what I call as (A) Laborious stocks (B) Average stocks and © Smart stocks. The origin of doing so has something to do with school or hostel days where all of us have classmates of different types.

You have very studious and extremely hard-working guys who generally do well in a class directly proportional to their study hours, night-out effort and time. Rank toppers & gold medalists generally come from this segment. Most disciplined & regimented guys also come from here. Some of the dumbest guys are also placed here because of family & peer pressure etc. they keep slogging with poor results. All these areLaborious stocksâ Type A. They typically constitute 20-25% of the universe.

Then you have guys who are average studying types, will make same mistakes whenever faced with a googly question in the exam or viva. General tastes, fashion, fads etc. You wonât find any Sachin Tendulkars here. These areAverage stocksâ Type B that typically constitute 60% of the universe.

Then you have few who study little but are actually much sharp, fast grasping power, excellent subject understanding of fundas and output they deliver_in relation to the inputs gone in_. Iâm referring to only fair study means, no shortcuts or hanky panky stuff. These areSmart stocksâ Type C. They may not be rank toppers and sometimes they can even be laid back but my experience shows they have done fairly well in life (not always in conventional sense of the word). May be when you think back, youâll find some real life examples.

)----

__

It is this Type C â Smart stocks that I always look for when scanning emerging stocks that are yet to arrive (in terms of marketâs institutional discovery and consistency of results) but have some advantage. Scale up, Network effect and expanding of Moats are easier to achieve with this Type C stocks.

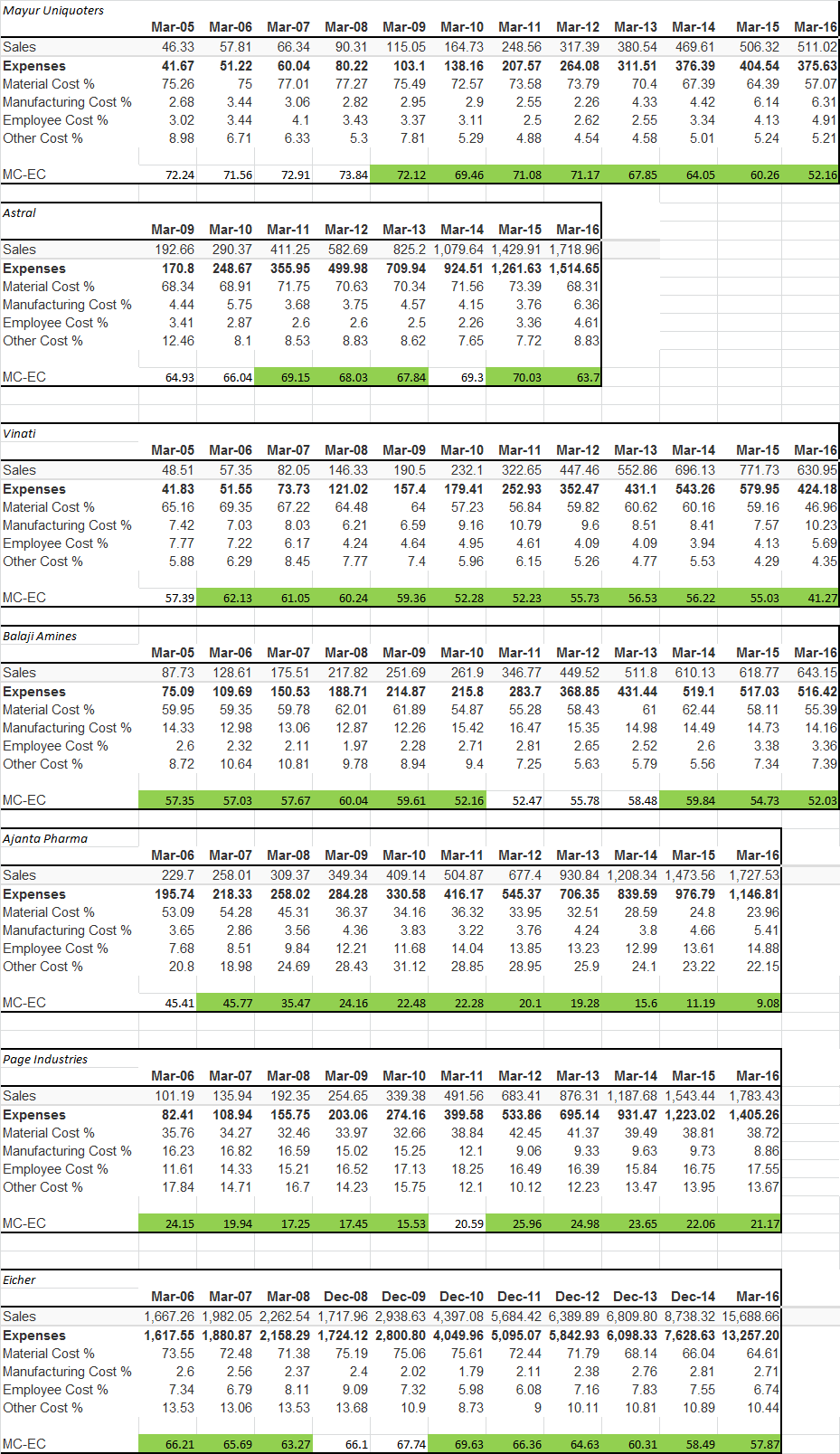

Pardon my saying but most of your ValuePickr stocks are the Laborious types including Manjushree, Vinati, Mayur, Balkrishna, GRP, Indag, Astral etc and even Kaveri that you are putting in A+ category. There is nothing wrong in being with laborious stocks and with right traits they make very good money so long as they preserve their traits just like gold medalists and most disciplined guys display. Mayur is a case in point. HDFC bank is a very laborious stock and very disciplined at that, so they can be really rewarding if you find them early and they themselves donât goof it up.

)----

__

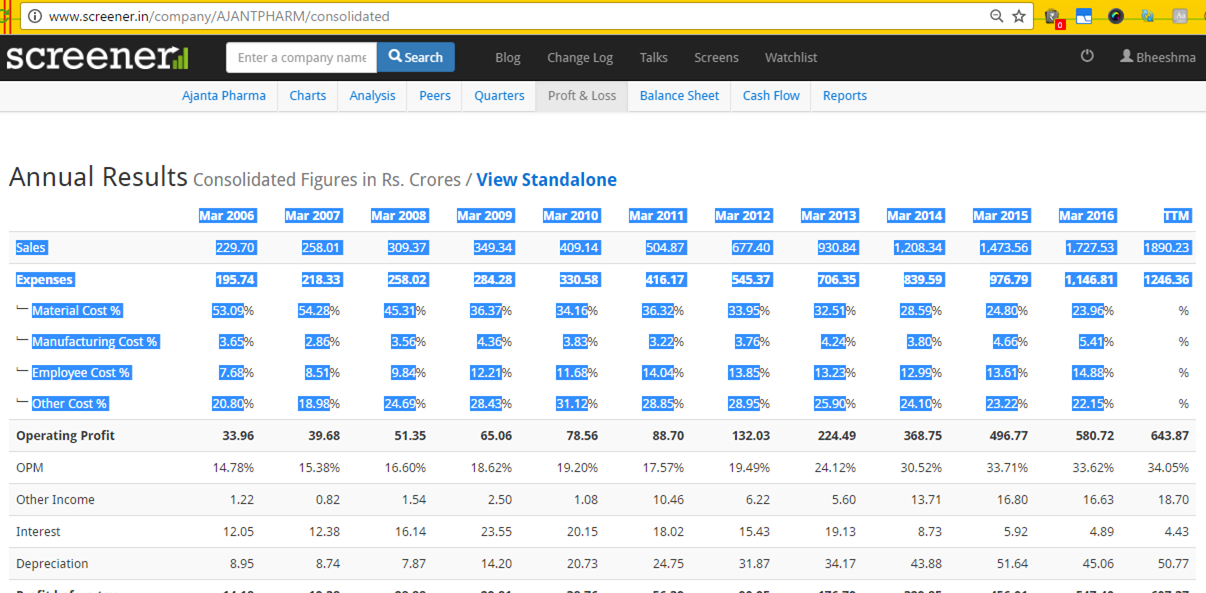

Ajanta Iâll not comment as I donât understand it well.

I can slot PI in Type C where results can be disproportionate.

Last year, Alembic was a very easy Type C and we made an easy kill there, doesnât always happen. Two Type C that Iâm betting on at the moment are JB Chemicals and Accelya Kale, though from much lower levels. One Type C where Iâve_probably_gone wrong is IL&FS Investment Managers.

While dealing with Type C Stocks, one important caveat is that management quality & integrity should not be suspect. Second is when analyzing such a stock, we should be looking at the outcome of big would-be picture. Third is we should have a handle on the right metric to value such a business, not necessarily the PE or PB.

)----

__

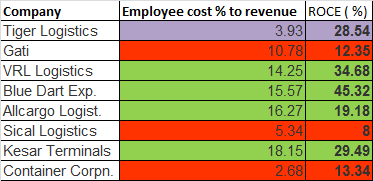

The term âProcessor stocksâ never occurred to me thus far, but itâs a nice way of looking at it and they are a subset of Laborious stocks.

Discl: I have no position in any of the stocks mentioned above,except for the last 4 named stocks.On Laborious stocks, to take the cricket analogy forward, I’m reminded of Australian fast bowler - Glen McGrath who can keep bowling the same outside the off stump nagging line to the batsmen the whole day - so disciplined and so immaculate. If VP stocks are those Glen McGrath,I don’t want to give an impression that these stocks will not be good vehicles to ride, as historic CAGR shows they have given superlative returns, and may continue to do so by all means.

- setting high expectations and inviting the risk of falling flat in delivery - but hey, we have always liked to stick our necks out - challenge and be challenged - in our bid to become more refined investors.

- setting high expectations and inviting the risk of falling flat in delivery - but hey, we have always liked to stick our necks out - challenge and be challenged - in our bid to become more refined investors. Remember Orkut, MySpace, Yahoo - companies which flattered to deceive? In response to your question on whether to invest fresh capital at 25PE, my personal take would be that I would not (would look at valuation metrics other than PE but if all/most metrices show its overvalued, I would pass).

Remember Orkut, MySpace, Yahoo - companies which flattered to deceive? In response to your question on whether to invest fresh capital at 25PE, my personal take would be that I would not (would look at valuation metrics other than PE but if all/most metrices show its overvalued, I would pass).

! amount, riskiness and timing of the future ofwhether thatthere

! amount, riskiness and timing of the future ofwhether thatthere