Disc: I have roughly 10% of direct stock PF invested in KEI.

Thanks for this great first post. In addition I will add the following:

Few Pros:

- I think of KEI as a B type company (definitions are in the ART of valuation thread) that is transforming itself into a type A company. The management understands the importance of retail, which is growing at a breath-taking pace.

- From the annual report " housing wires segment generates higher margins than conventional cables". So the management is able to recognize and understand the importance of moving into retail segment which is more granular, relatively less cyclical demand, higher margins. Towards this end, their spending on brand building is also increasing. From the annual report:

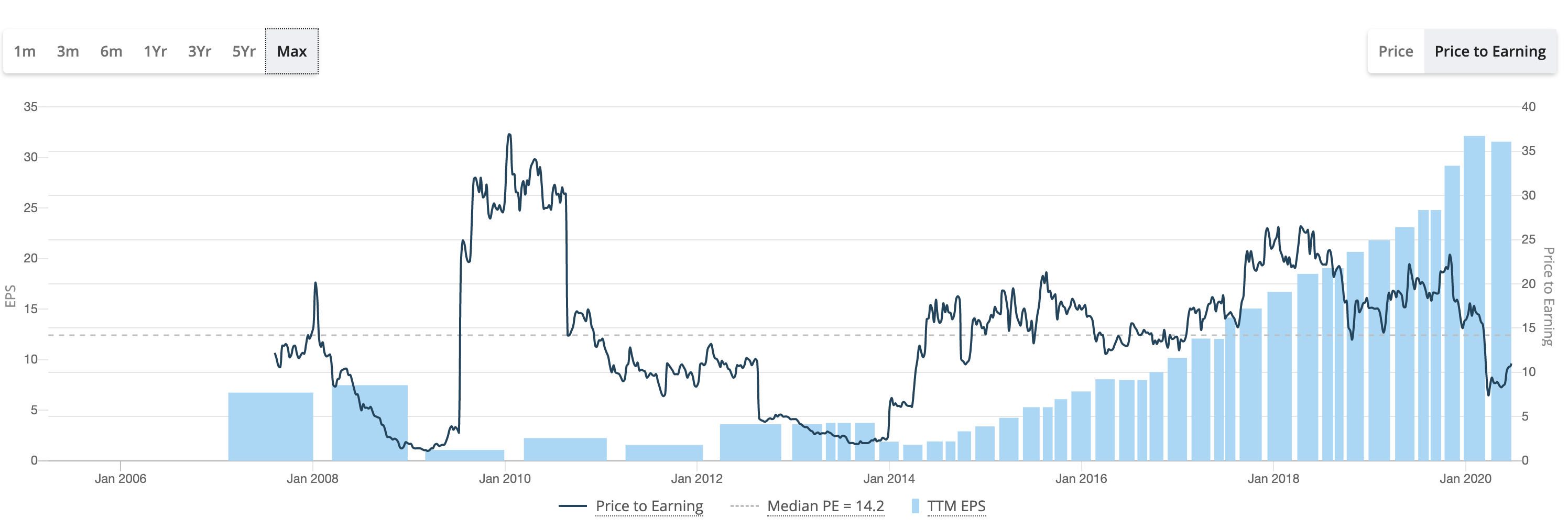

- Here is a visual representation of the company’s earnings from screener:

As we can see, earnings have been very consistent since last several years, which is quite fantastic given the overall growth slowdown in India in last 2 years. going over last few AR, IMO this has been possible due to the strength and diversity of the orderbook. - Current P/E multiples of 10-12 are quite low and possibly due to overall depressed state of midcaps and in general global equities.

Cons:

- KEI is a pureplay Wires business versus competitor polycab which has a small and growing FMEG business. KEI has its own version which is “retail wires”. Time will tell which strategy will prove to be better. I could not find a fine-grained break-up in polycab report for each type of client (for example, power sector, retail sector) for the wires segment which is still 90% of revenue for polycab. Having said that, I believe polycab will get higher multiples than KEI since market will tend to value it like a havell’s due to the FMEG segment which is higher up in the Value-Chain.

- KEI has a large dependence on cyclical industries such as Power, Auto sector. It is not very clear how long they will take to make Retail large part (80%+?) of the business (although that is the direction) but until they do, there is always a risk to their earnings.

PS1: I am not too worried about the trade payables and receivables: it seems to be high for all the companies in this sector.

PS2: I prefer KEI to polycab for 4 reasons:

(i) On some metrics like MarketCap/OCF or MarketCap/Sales KEI is 2x cheaper than polycab

(ii) It is smaller and hence larger room to grow

(ii) Retail is already ~50% of sales for KEI meaning it is well on its way to being a type-A consumer facing higher value-added company compared to polycab which only has 9% of its revenue coming from retail (which i could make out from 2019 AR page 15)

(iv) Much longer proven track record of growing earnings reliably for KEI (5-6 years) compared to polycab which has only been listed for 1 year publicly.