There is already a separate thread on Vertoz:

Super results by Creative last week and management sounded very honest about their plans for future. Key highlights:-

-

Q1 FY22 impacted by lockdown and represents around 2 months of sales. They did 69crs and 70crs of biz in June and July 21 - best performing months in the history of company

-

Console margins are depressed because Honeywell expenses have started flowing but revenue is yet to kick in. The management has guided for a launch in middle of September for Honeywell products and are sticking to 80 to 100cr revenue guidance for FY22. That makes INR 17cr EBITDA just from the Honeywell licensing business. Rest of the INR 600crs (conservative number) business could contribute another 5% EBITDA margin so another 30crs. So a total of 47crs EBITDA expected in FY22.

-

Ckart - Independent director on board from IIM who teaches platforms and social networks. So they’re seeking guidance from the board in terms of the skillset, direction and how to play this business. Tentative plans would be revealed in the next 2 months. Could include a demerger of ckart too.

-

Guidance for Honeywell business - INR 200/250 crores by FY23. The agreement is till FY25 and they’re in very early stage talks with other brands as well for licensing business.

-

Numbers: INR 135cr revenue; 4cr EBITDA and 1.23cr profit.

Per the guidance by management, Honeywell business should contribute ~35cr EBITDA by next year and rest of the business could contribute a similar amount. Overall 70cr EBITDA in FY23.

Currently the stock is trading at a mcap of around 315cr which is 4.5x FY23 EBITDA.

5 Likes

Is anyone tracking Libas Consumer products?

This issue was spoken of in the Q1FY22 con-call and I have myself been critical of the move but here’s the perspective of management:-

- We were talks with these for last 1/2 years;

- Not sure if the rights would have been subscribed (management sounded skeptical)

- Said they’ll consider rights in future fund raising requirements

- No further immediate funding requirements, so no further dilution.

And yes, the pricing is as per SEBI norms, it looks very low because the stock had a sharp upmove from 130 levels.

Not very satisfied, but then, not every thing is perfect. One has to weigh risks / rewards here.

2 Likes

Is anyone tracking Auro Labs now? @crazymama @cabunny There is a closed thread:

A couple of questions:

- @cabunny Did the company give the answers to your questions, particularly related to the capacity?

- What are the reasons behind the ongoing correction?

Disclosure: Not invested.

Add shop e Retail…

Expansion is going on.

2 Likes

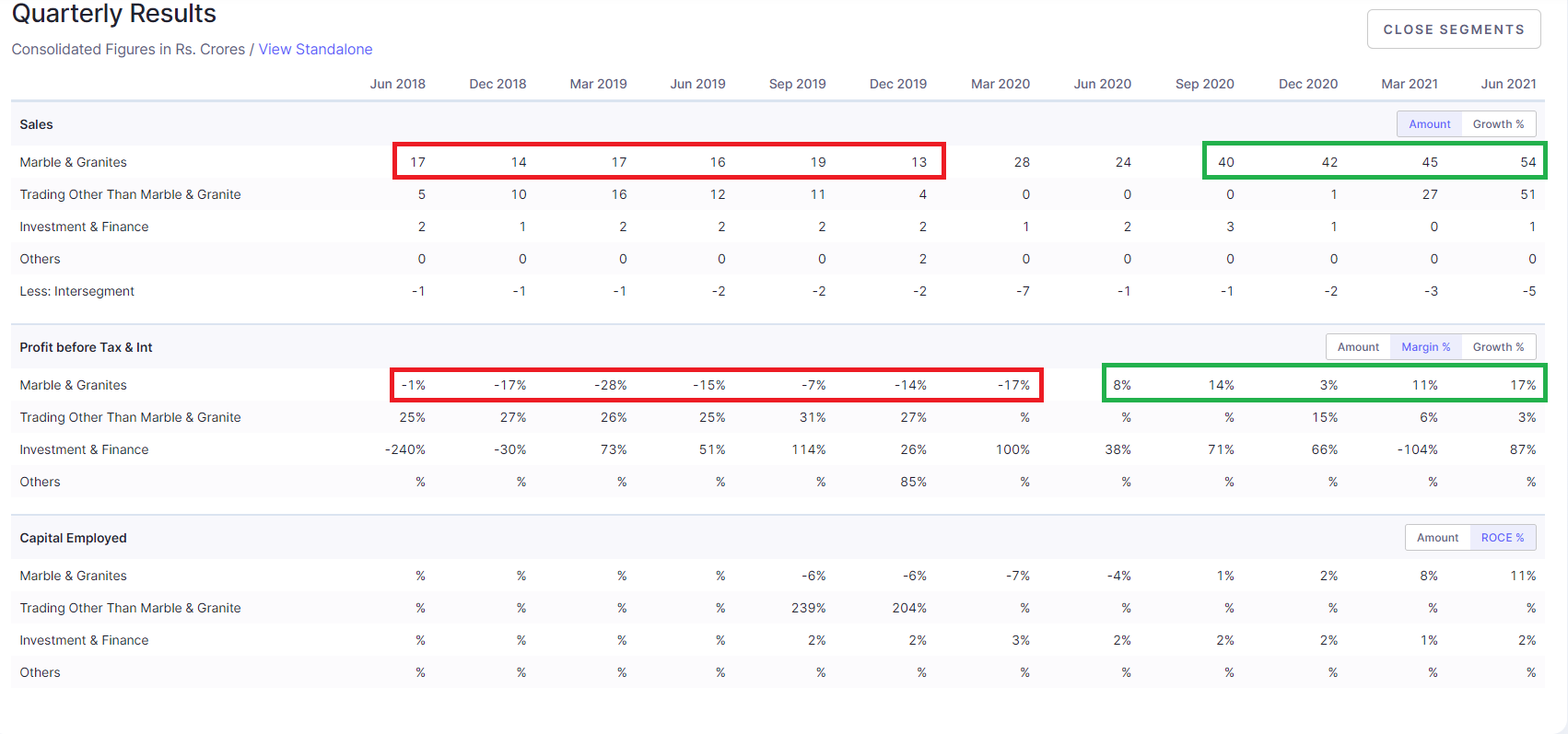

Pacific Industries Ltd ( BSE: 523483 )

Market Cap ₹ 123 Cr.

Promoter holding 74.0 % ( Good )

Debt ₹ 42.3 Cr ( Concern )

Listed Peers: Pokarna

Pacific Industries Limited is an India-based company, which manufactures and deals in marble and granites, and allied products. The Company is engaged in mining and quarrying.

https://www.pacificindustriesltd.com/

Recent Result Trends :

If anyone is tracking this space, please do share more information.

Regards

Gaurang

1 Like

Is there anything specific in Add-Shop E-Retail, continuous UCs from few days?.

Please go through its business model. U will get answers. This script is upcoming FMCG player.

@ Add shop e retail.

d9005d3f-6017-4157-99a6-d339b852d6d2.pdf (541.7 KB)

MY be after pref share allotment to this PE fund, a lot of buying is happening in the stock

I got some product review directly from people who have used the product and they were great.

All the online reviews are also good.

The very high receivables is a worry. company’s relationship with Dada organics (another company of the chariman) is suspicious. However there is PE fund investing in the company and the chairman also has a very good reputation.

disc: small percentage of my pf.

Sir

We do not have any thread on Add-Shop. Can we make one for better understanding and follow up.promoter seems very honest. A blind person with high visions.

Disc. Invested recently.

2 Likes

Apologies if this questions seems naive as I have not studied this business, but what’s stopping giants like Amazon and Flipkart to kill Add-shop? Trying to understand their competitive advantage and what makes them stand out in this space?

Curious to get some thoughts here. Thank you!

3 Likes

161b73ac-97ee-48dc-8c90-e734babfac08.pdf (590.2 KB)

Previous Auditor Resigned and new Auditor appointed in place. is it just a routine or any thing suspicious? Why any auditor will resign without ant reason?

1 Like

I have also noted few minor observations on Add-Shop E-Retail.

- MD is signing himself on all the disclosures submitted to exchange despite he is partially disabled. CS is not signing any documents.

2.Company is not having any proper designed letter head. Currently they use word header letter heads.

1 Like

This time CS has signed the letter. And using word based latter head is not an issue. Yes company should use companys logo in all the communications.

Promoter is the competitive advantage. He personally has addressed highest no of panchayats and made a world record. And thst feeds bsck customer stickiness and networks effect in buyers. Snd its a sustainable advantage which online players can not even dent.

That is because Dolly Khanna recommended it on 1st oct.