As of 2021, Add Shop E-Retail has 70% of assets in trade receivables, which seems very high. Working capital is getting stretched as well. Latest AR tells that they entered into a lot of RPTs as well. Not sure, if anybody has any view on this, but looks like a lot of red flags to me.

Not Invested, tracking and studying.

5 Likes

e2eb1311-7664-4f01-b156-e77bb02fb07e.pdf (1.3 MB)

Add-shop : Q2 FY22 Results seems very good. Can anybody analyse the results in depth?

Relevant suggestion by - humbleInvestor!

https://www.thedesiinvestor.in/?p=24

It does appear to be rather shady. The entire stock raw materials are being sourced from promoters, despite the IPO prospectus clearly stating that AddShop has an agreement with Marss Herbals for manufacturing.

The franchise and distributor numbers have changed in different filings it seems.

Also, the new investor Nexpact could be related to market operator Sanjay Dangi.

The blog has highlighted several other concerns as well.

4 Likes

Yes, I had already pointed out in my last post that the pace at which TRs have been increasing as compared to the revenues, clearly shows this company is basically incentivizing it’s distributors in some way to store the goods to their warehouses, and record them as sales. With a business model like theirs, it’s very easy to do so as there are thousands of distributors and it’s very hard to track, to how many of them the goods provided are actual sales and how many are just for the billing purposes. It’s a classic example of P&L manipulation.

What makes matter worse is that we don’t and can’t even know, how many of these transactions (customers and suppliers/manufactures) are related party transactions (RPTs), as the company has many times told the exchanges that they don’t fall under the bracket, where they have to report the RPTs to the investor community at large.

I don’t see any competitive advantage as well, and getting backward integrated by leasing out lands to produce the RM/finished goods is not a scalable option, as the organic farming for different agri produce can’t be done everywhere.

It’s a risky journey and I have decided to opt out of it, until they become more transparent, and/or I see improvement in their TRs/Inventory, and thus in the cash flows.

Disc: Not Invested. Tracking and studying.

4 Likes

Bonus share recommended in add shop e retail 7:10 fully paid.

Disc: invested and planning to add on dip.

1 Like

Hi, Here is my thesis about a closely tracked stock. I am looking for opinions if I am thinking in the right direction or not.

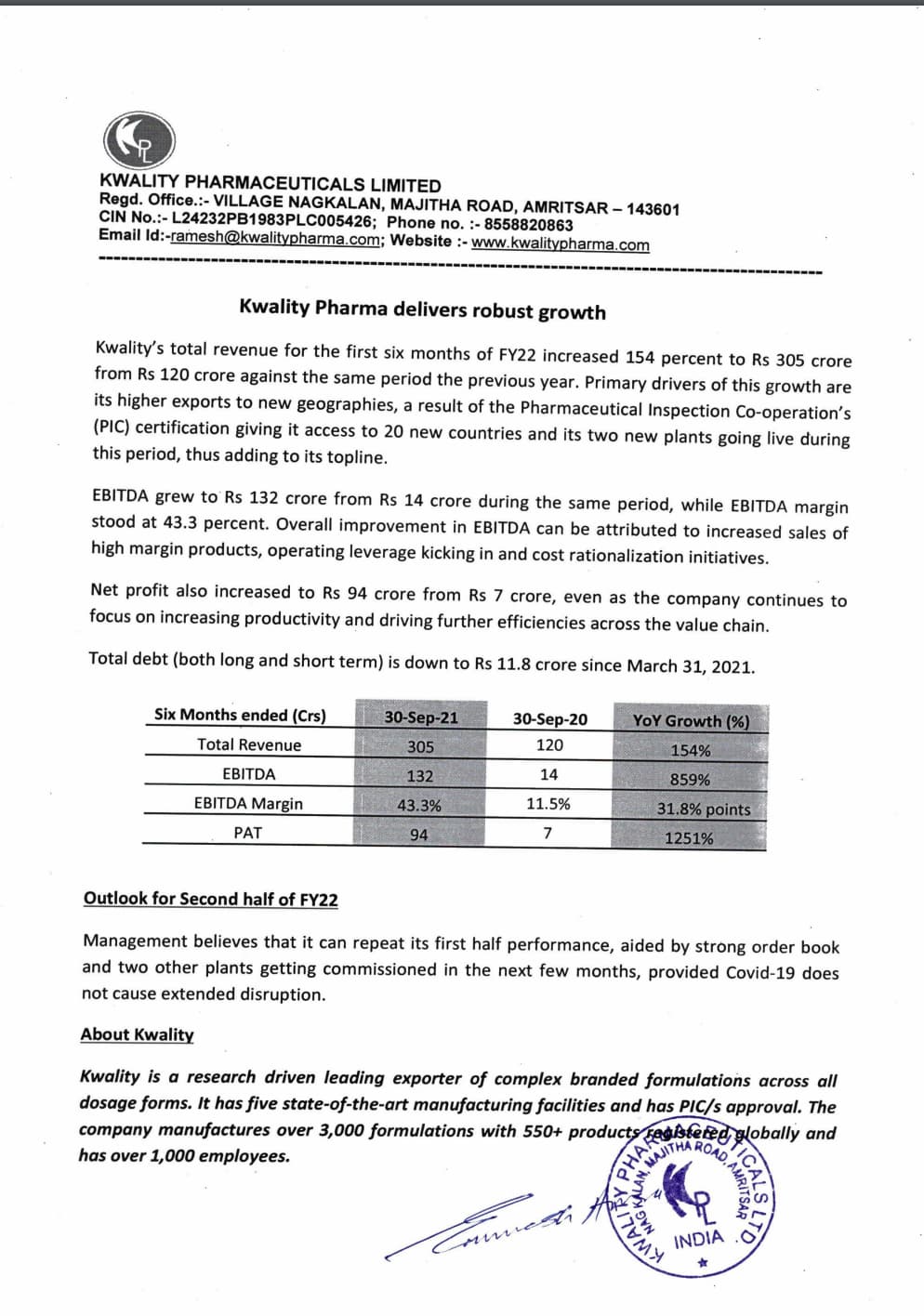

Kwality Pharmaceuticals Limited is an India-based holding company. The Company manufactures and exports pharmaceutical formulations in liquid orals, dry syrups, tablets, capsules, sterile powder for injections, small volume injectables, ointments, external preparations and oral rehydration solution (ORS)

While the Stock has run up from 100 rupees to 900 rupees according to the latest results:

Sales : 300 Crore

PAT : 94 Crore

I believe the remarkable performance by the company calls for a discussion.

Management has maintained it is able to repeat its first-half performance which means a PAT of FY PAT of 180cr+.

This translates into EPS of 180 and pe of 4.63 with an industry avg PE of 26 (Bulk Drugs).

Further 2 plants will get commissioned in next few months.

Company has also mentioned that due to Remdesivir and Propofol - it has gained a lot recognition in the international market and got a PHARMACEUTICAL INSPECTION CO-OPERATION certificate.

According to even basic calculations, this stock deserves a PE rerating because of

Stellar performance

Margin expansion

Confidence in repeating the performance for the coming years.

Hope to get your viewpoint on this situation.

5 Likes

Good stock

Invested

Usually due to upper circuits you can’t buy this stock but has retreated a bit due to market weakness allowing people to enter

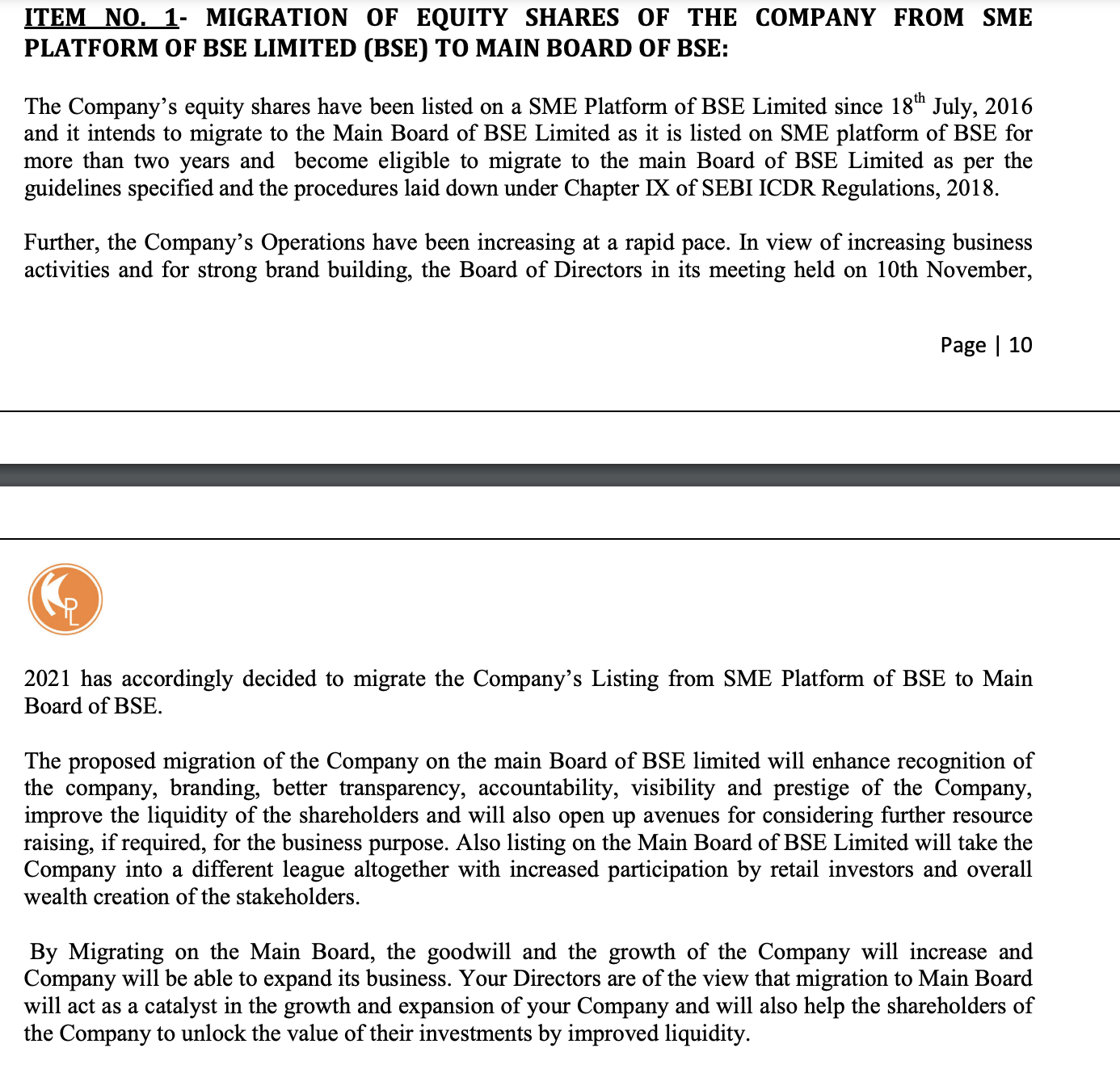

Also it’s going to try listing on main board that will bring more recognition and liquidity together with quarterly reporting

1 Like

What are reason you think it a good stock ? Would love to understand the rationale behind your thinking ?

1 Like

For similar reasons you mentioned

The business generates 25% of its market cap every year and is expected to increase it

Let’s say it does not increase any revenue or profit but maintains it, I’m happy even if price stays where it does

With new plants that have been lined up and with them being listed on the main board it’s only a matter of time before other investors will notice it

Many investors use screeners and not company filings to research their stocks, this stock is not on the screeners yet, but that doesn’t mean it’s value is lost

What suddenly changed for the company to double the top line and margin becomes 4 times.

did they just exploited the supply chain constraints.

Was there a change in business mix which caused such windfall.

What is the roadmap to sustain the topline and margin.

If we go by historic numbers and leave this one super quarter price seem fully priced in.

There was a increase of `~35% in fixed assets

Any thoughts on DCM Nouvelle? Company seems to be fairly priced. I have not seen any active discussion on VP on this co.

Kwality Pharma

Well, what changed was operating leverage kicked in and in times of uncertainty the company used its low cost of production and good quality products to gain global recognition - gain certifications - get its products registered and push its high margin products across new geographies.

I have vetted almost 100 companies this earning season especially in the pharma and chemical space. I didn’t come across a single company that expanded margins - revenue and positive commentary for the future like kwality pharma did. Plus it has the backing of investors like Ashish kochalia. Now the questions comes when will market realise this and price in the future growth as well. Do share your opinions guys. would love to hear some anti thesis pointers as well.

1 Like

The company shares very few details about the revenue from its various products. How much of the revenue is associated with Covid-19? The target markets can attract other companies owing to the high margins. What are the competitive strengths that will protect the margins? Any idea what is the sustainable revenue and margin next year onwards? The management seems to have provided guidance about the next half year but not beyond.

1 Like

I completely agree with you. In their recent updates about shifting to the BSE mainboard from the SME board, they mentioned that they want to unlock value and create better transparency for investors. so I hope they are able to do that. currently, the vote is underway.

Let’s say all of additional revenue is from Remdesivir. Other companies, one I was following was Everest organics, they couldn’t capitalise on this. Getting approval for Remdesivir from patent holder is a bit tricky and new approvals unlikely. In the heat of covid crises, they were more open to consider

South Africa has roughly 25% vaccine uptake

If they can maintain this revenue for another year and then say back to usual ebit of 2 crore, they would have enough free cash, almost equivalent to the current market cap

That amount of free cash gives you a lot of options provided management has foresight.

Their major revenue is Africa exports. A lot of companies are planing this sector, like Fredun pharma. Caplin did a good job expanding into Latin America

Not everything of course is guaranteed. Any stock comes with many ifs and buts otherwise anyone could fire up excel and come up with best stocks to invest for lasting wealth

Most of what the insiders know is unknown until it’s played out and many times the insiders are not even the management

I think the stock is at 50ema and many people know that, that level is when people get scared and dump. Smart money usually picks up here for next leg of movement. I’d wait for a week to see if 50 ema holds or falls. If it holds strongly during market weakness, then the normal pull back pattern would have played out and the stock likely will rise.

There has been a good level of buying support and reduced sellers at this level, even during market weakness and selloff yesterday.

2 Likes

Again I’m not counting new plant, new products, research plant etc

Back of envelope calculation without any of it looks good

2 Likes

Do anyone have any information on Siyaram Silk Mills regarding Dr Vivek Bindra hired as consultant?

Their latest note on the reason behind migration