Flattish results for Q1FY24 compared to Q1FY23 (with minor improvements)

1 Like

Given the context of headwinds for the agrochem and chemical sector, the results are rather taken positively by the market. Some of the pointers from the conference call.

- Revenue guidance for FY24, 1,200-1,250 Cr. (current market cap 1,203 Cr).

Margin guidance provided as 13.5-14.5% - Market conditions are challenging

- Product samples for a couple of their new products are approved. However, they expect delay of 1-2 quarters for shipping those products

- Management suggesting that they have exciting new products pipeline

- Utilization level to go to 70-75% in next 2-3 quarters. Company to take a call on capacity expansion in Q3/Q4 of current FY

- Expect second of the year to be better

3 Likes

Company came out with flattish set of nos, when the entire industry is going through a lot of pain. They have been able to get their volumes back, and are focusing on their new molecule pipeline. Concall notes below

FY24Q1

- Industrial division is performing well and is expected to do well in FY24. Phosphorus and derivatives business is specially doing well and UPL family is very strong in this

- Next few quarters will be challenging due to inventory positioning of different companies. They are maintaining low inventories and working on just in time model to ensure sustainability of margins

- Hope to improve margins by 50-100 bps in rest of FY24

- Slight dip in gross margins was due to change in product mix

- Aggressively going for new business opportunities

- FY24 capex: 40 cr. (spent 9.5 cr. in Q1). Have replaced older reactors with new ones which increased reactor capacity to 2000 KL (vs 1300 KL in FY23Q4)

- NextFerm: Pharma has been slow and this ramp up has been delayed, contribution will only come next year

- Prosulforcarb: did not lose the contract, but registration in Australia was delayed during COVID. Their consultant has guided that they should get registration in Europe by September 2023 and they are expecting to have revenues in Q3FY24

- Greenfield expansion: Looking aggressively for land in Gujarat/Maharashtra

Disclosure: Invested (position size here, no transactions in last-30 days)

14 Likes

Listened to concall, your question on reactor capacity and contract, I am currently invested in Dharmaj, thinking whether to switch or not

Just noticed that in the balance sheet, trade receivables have gone up by 28% in FY23 when sales increased by 8%.

Any idea why that would be so?

Company came out with flattish results, with sales declining by 13% and EPS being flat YOY. While results were subdued, if compared with peers (likes of Astec, Sharda, Rallis, NACL, etc.) they were quite good as the industry is going through a massive destocking cycle with Chinese driving down the technical prices. My concall notes below

FY24Q2

- Witnessed drop in volumes (due to inventory overstocking) and prices (due to entry of Chinese peers)

- Margins were higher due to focus on better product mix, better cost management, process efficiencies, R&D focus on new products leading to improved process efficiencies, and better customer support leading to better demand and pricing

- There was a one-time 2 cr. interest cost in this quarter (due to some Supreme Court judgement). This wont repeat

- Australia product has huge inventory in market

- 4 new product registrations: 2 secured + 2 under process. Full potential for approved products will be realized in 12-18 months

- Efforts on LATAM has yielded good results in last year, main problem with that market is that registrations require 3-6 years

- Receivables: generally 50-60 days. In this quarter, percentage of sales in domestic market was higher where credit period is higher

- Lalru: pharma + specialty chemicals products (no agchem products).

- Derabassi: Debottlenecking to improve capacity, will migrate towards higher realization products. Capacity will not be a challenge for growth

- The pharma intermediate products are still under approval, its generally longer cycle compared to agchem

Disclosure: Invested (position size here)

13 Likes

Q2FY24 Results

Industry Headwinds

-

Revenues impacted due to high channel inventory

-

Price erosion due to heavy dumping by China

-

Demand continuous to be sluggish

-

Price pressure is as intense as ever

-

Margins improved due to efficiencies in the processes (investment on equipment upgrade helped ), new products with better margins

Factors that impacted this are broadly due to below

- Product Mix (Promoted products that are more profitable )

- Cost Management ( Logistics, Fuel, People )

- Productivity and Efficiency ( Investment in R&D, process efficiencies , reduced waste)

- Innovation and R&D ( Added more people )

- Customer centric Approach - Helped to understand current market conditions and understand customer requirements

-

Revenue Mix - Domestic 48%

Margins

Gross Margins 40.6% ( vs 35.5% same period last year )

EBIDTA Margins 14.6% (vs 12.1% same period last year )

PAT Margins 7.5% ( vs 6.9% same period last year )

- One time interest cost of 1.98 crore

- Added 27crore worth of fixed assets

- Focusing more on data driven decision making, to achieve this, we are in the process of implementing S/4 Hana

- Working Capital days increased from 63 to 72 days (this is due to more domestic sale and that is the nature of domestic market, but sill Punjab is best when compare to peers )

- New molecules commercial supplies will pick in H2

- 40% of the new enquires are from non agchem space

- Expecting few registrations from Europe (very soon )

- Metconazole , capacities are fully utilized

- Lalru facility is mainly for Pharma and Specialty products (Current utilization is 55% )

- Looking for new site for Agchem products

Growth / Margin Guidance

18 - 20% Revenue growth

Aiming to achieve 18% EBIDTA Margins

13 Likes

Summary notes from conference call Q3’24

Volume Growth Issues - Because of inventory delays the guidance of 20% growth will not be feasible during FY24.

Improvement gross margins - attributed to Improvement in processes for raw material optimization, product mix. The efforts are to sustain at 41%

Challenging Times: Global challenging time for Agrochem to continue until Q3’25.

FY25 Guidance: 10-15% improvement in FY25 for existing product. New products would contribute ~ 200 Cr.

4 Likes

Punjab came with very subdued results (-18% sales decline, -44% EPS decline). However, these nos were much better than most other technical manufacturers and they have only witnessed 8-9% price decline vs most generic cos facing 40-70% price decline. This has meant that they actually improved gross margins this quarter.

They seem to have invested quite a bit in new product development and are confident of scaling up 7-8 new molecules + intermediates in the next few quarters. Concall notes below.

FY24Q3

-

Export demand is subdued (high channel inventories, adverse weather, customers building inventory closer to season). Expect revival by Q3 of FY25 (so about a year)

-

Gross margin improvement is due to process re-engineering leading to better raw material efficiency + product mix. Make higher margins in specialty intermediates for pharma

-

Of the 3 planned launches this quarter, have got registration for 1 product in EU (different from Australian product; prosulfocarb) and started supplying commercial quantities. Other 2 registrations are expected in 2024 and commercial supplies should begin in Q3/Q4FY25. Total business from these 3 products are 100-150 cr. once all registrations are done

-

Intermediates: Supplies have started for 1 pharma intermediate (currently for EU market, high value, should get US registrations in 1-2 years). 2 other samples have been approved and commercial quantities will start in Q3FY25. These 3 intermediates (2 pharma + 1 agchem) will contribute 150 cr. in 1-2 years

-

So 100-150 from agchem + 150 from intermediate ~ 300 cr. from products being commercialized now

-

Have got into a long-term agreement with agchem customer for 1 agro product which will be launched in beginning of 2025

-

In 9MFY24, have not seen major volume decline. So probably 8-9% price decline (which is quite good compared to generic technical that have seen 40-70% decline)

-

FY25: Existing products should see 10-15% volume growth as volume have reduced in FY24 due to high channel inventory + there will be new product contribution in range of 200-250 cr.

-

Expect 10-15% growth in near term which will then ramp up to 25-30% in 3-5 years

-

In current portfolio, 2 products are patented by Japanese innovator, 4-5 other products are generic but in a couple of them, Punjab has 80-90% of market share

-

Will start working on a new production block in Derabassi in April/May 2024

-

Hydrogenation added to capability

Disclosure: Invested (position size here, no transactions in last-30 days)

7 Likes

@harsh.beria93 can you share references of 40-70% price decline in case of peers.? And whats the reason for better pricing given destocking and subdued export is faced by all downstream player including UPL.

1 Like

You can read commentary of Sharda Cropchem or Meghmani Organics

Product basket for Punjab has much lower competition, that’s why price cut has not been so severe.

1 Like

Notes from Arihant Conference April '24

History

- MD: Shalil Shroff

- CEO: Mr. Vinod Kumar Gupta; been with company for three years now.

- Agrochem (~60%) + Performance Chemical (~40%) Manufacturer (API + Industrial chem [18% of performance chem.])

Units

- Agchem division : Dera Bassi, Punjab (this is a 48 year old plant); 25acres & 6 production blocks. Has been upgraded recently in the last few years. Also houses the R&D facility for NPD. It has a freen effluent treatment steam generation unit which uses rice husk as a fuel.

- 2nd unit: Lalru, Punjab: acquired division; Performance Chem (API + API intermediate)

- 3rd unit: Pune, Maharashtra: Industrial Chemicals/Food additives (for Coke and Pepsi etc.)

- 4-5 decades old company

- Started as a partnership between Excel Industries Ltd. & Punjab State Industrial Development Corporation (PSIDC)

- 50-55% direct exports and rest domestic sales often are also mostly catering to exports.

- 1st product: Oxalic acid in 1970’s.

Recent History

- FY23 top line: 1000cr. topline

- Have turned around in last 3-4 years; almost doubled top line with EBIDTA margins in teens now.

- We did this by focussing on infra updates; upgrading talent pool across all deptts. Hence relatively newer team

- CEO Mr gupta has been for 3 years.

- Mainly into agchem. (be)

- Spec chem: Halogination, esterification, nitrogenation

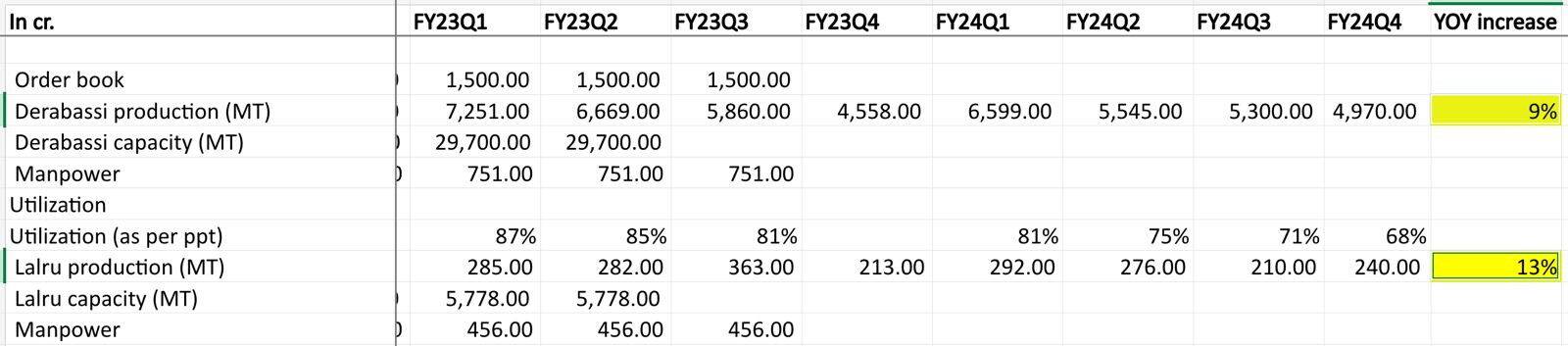

- Capacity utilisation: 9m24; DB over 70% (previously been 80-85%); Lalru - 49-50% (prev. ~70%); Pune 90% + utilisation

- Last 3-4 years have spent over 100cr in the last few years. From internal accruals.

- Has helped improve gross margins

- Clients: Laurus Labs, Lupin, Nippon Kayaku, Daichi Sankyo, UPL, Bayer, Pepsi Co., Coca Cola, Adama

- 55-60% is exports key is Europe; LATAM is growing fast

- Board: > 50% independent directors

Current Scenario & going ahead…

- Continue to focus on agchem

- Some products were launched in 24 although the sector is in turmoil due to heavy inventory

- Expecting some turnaround Q2FY25 onwards.

- Planning timeline according to this.

- Some existing and some new customers

- although from 10 years have clients in Japan however there are some new customers.

Had previously guided that has a 15 product pipeline and plans to launch 7 by H2FY24.

- Strengthened R&D, BD teams

- Some molecules that had been planned for H2FY24 have been postponed for FY25. Roughly 5 molecules for FY25.

- There are some other new molecules in pipeline and hope to launch 2-3 molecules each year.

- Volumes pick up over time and takes 2-3 years to reach peak capacity.

- Space to plan for one more line at DB or Lalru. If required beyond we will need another new site.

- Over the next 3-4 years 20-25% topline to come from new products. ==So maybe a topline of 200-250 cr topline possible from new molecules in 3-4 years.==. Had previously guided for a 1500cr. Top line in 3-4 years

- We are looking at molecules which have market size of 800-1000cr. Some of niche molecules could be lower for niche applications usually with tech transfer. We are typically looking for molecules which don’t have much competition and can be in the list of chemistries we could do.

- Seeing China + 1 but rather happening slow.

- Capex plans manufacturing block roughly costs 50cr. Which we are looking for in FY25 which we have space in DB. Further we would need new space primarily though internal accruals. Overall, capex 100-150cr. till FY26. Keeping both options open M&A (Brownfield in Pune or Gujarat) or a new site.

- Interest costs: due to some indirect tax that we have paid off in FY23-24. Going ahead depending on working capital we hope debt profile should be within limits.

- Asset turns are at 2.5 -3. (so a 50cr. could generate 150cr. Revenue). A new capacity takes 1.5-2 years to reach peak.

- What are we hearing from customers?: There was a huge channel build up while now it is mainly molecule specific. Till they are taken up there would be still challenges for the next 2 quarters. For us we have good visibility for FY25 and have good orders for Q1FY25 (reflective of good herbicide demand). We expect things to start improving from then. Pricing currently seems to be at lowest. KSM were 25% of usual price. For now its wait and watch mainly. Clients are saying to wait for few months to gain more clarity.

Management feels the challenges should last not more than a quarter or two.

- Vision: Aim to grow 15-18% annually in top line. Could also look at some inorganic route expansion if it comes our way.

- Credit cycle is a bit stretched a bit in the market right now however don’t see any red flags. Anticipate FY25 to be a turnaround year.

- Revenue Mix: How will this evolve?

- Mainly agchem business

- Key driver will be agchem only however planning to add spec chemicals.

- API or Performance chemicals; some promising products have been shortlisted for development in the next 3-4 years.

- Our Edge: some are hazardous chem. we are looking at that too large scale development.

- Margin profile: Has been fairly stable due to our upgradation of tech, product upgrades ie RM efficiency improvement which happens continuously in the last few years. Also, the new niche multistage molecules we are adding should lead to higher margin profile in the 3-4 years. Currently looking at 13-15% but hope it reaches to 18% in 3-4 years with new molecules.

Impression:

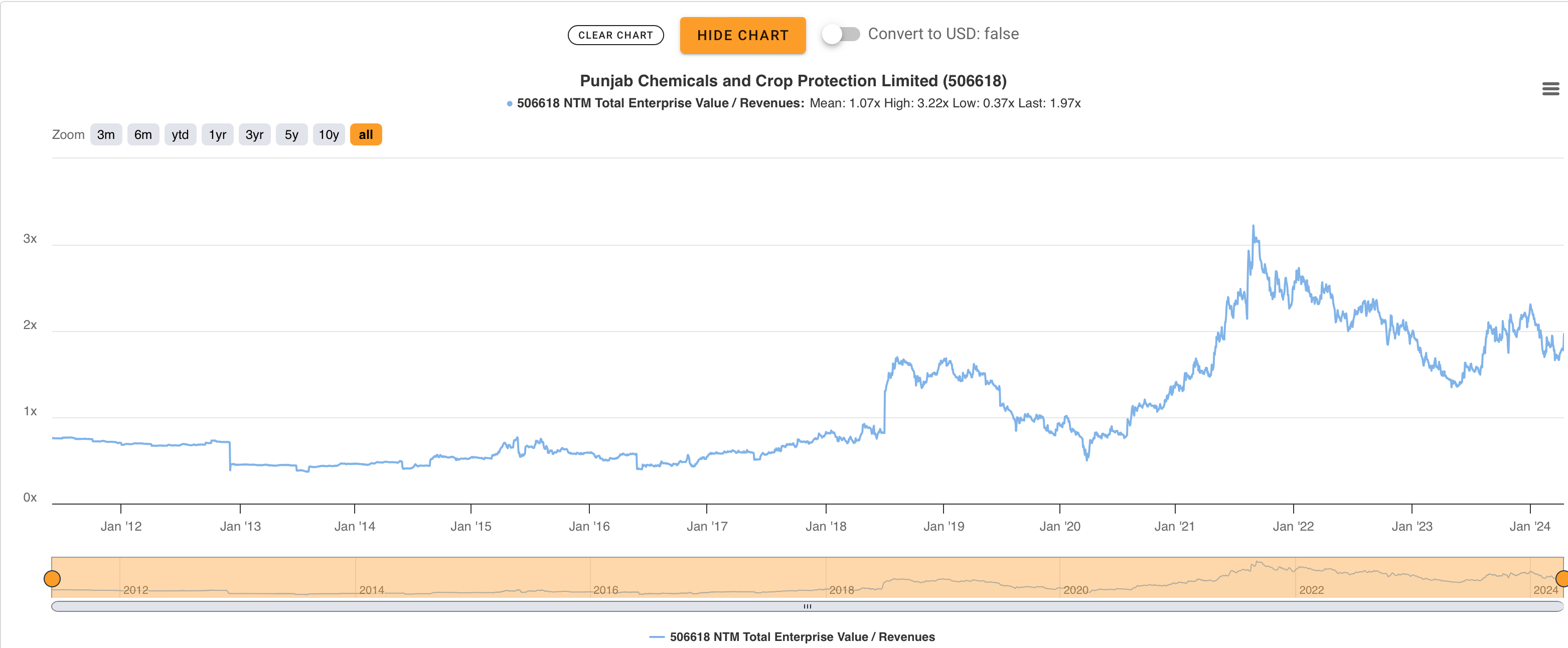

Company has made strides in the last few years as mentioned above (Tech and Infra upgrade, new team, improved financials) however as the company became ready to spread it’s wings it has coincided with a down cycle in the agchem and chemical sector. Hence, some of the recent plans stay in the wait and watch mode waiting to be executed as the demand scenario emerges and the cycle turns. The management is unable to give any clear timelines for the same as says that things are anticipated to improve by Q2 next year however has no order clarity yet. It’s in a wait and watch mode and so is the script. However, once the cycle turns, company probably has some interesting molecules it has been working on to look out for. All this being said the company is still not trading too cheap when compared to its recent past valuations.

[Discl: small tracking position]

11 Likes

Punjab came with flattish numbers (1% sales growth, -25% EPS decline). The good thing about FY25 was their numbers were way better than most other technical manufacturers, they improved gross margins while seeing margin decline in sales (-7% in FY24) in a very tough year.

Volume growth is coming back and they expect complete revival by H2FY25. Management is also guiding for doubling of sales in 1-3 years. Concall notes below.

FY24Q4

-

Seeing demand offshoots and expect recovery in second half of FY25

-

Freight costs have increased significantly for certain routes (e.g. Europe, USA). 1.2 cr. increase in freight + higher CSR costs + certain one-time costs which have resulted in EBITDA margin decline despite maintaining gross margins

-

Have received commercial orders for new molecules (both in agchem and specialty chemical)

-

Receivable increase is temporary and because of domestic receivables being stretched from 90-100 days to 120-130 days. This has started coming back to normal in May

-

Capex

-

FY25: 50 cr. in existing sites (1 new manufacturing block + maintenance)

-

Continue scouting for new production sites and want to time it to industry revival

-

Expect 1000-1200 cr. additional revenues in next 1-3 years. 10-15% of this will come from existing products and remaining from new products. This will require 250-300 cr. capex (3.5-4x asset turns) at existing sites and can be done from their existing plans

-

-

New products

-

New product contributed 7% to revenues

-

1 product has global sales potential of $100mn, another one has $20-25mn

-

Producing 2-3 products every 6 months, should commercialize 2-3 new intermediates in next 6-months

-

EU commercialized product should reflect in next 6 months because of high current inventory

-

-

Business mix: 70% Derabassi, 15-18% Lalru, 12-15% Pune

Disclosure: Invested (position size here, no transactions in last-30 days)

16 Likes

1 good point was: for multiple future looking questions, management didn’t commit any number and kept the answer open ended. In an uncertain market, it is good to be honest that we don’t how situation may unfold.

1 not so good point I observed management saying “its industry wide phenomena”. Yes everyone is affected but it can’t be repeatedly used as a shield to justify your own performance.

Another point is, they want to do Rs. 1000 - Rs. 1500 cr additional sale in next 1 - 3 yrs, for which they will need to do capex of ~ Rs. 200 cr. Since, they don’t have much of cash balance, large part of it will be debt funded, thereby stretching there D/E further.

Disclosure: already Invested and added further in today’s market meltdown.

1 Like

AR24 notes.

Miscellaneous

-

Settlement of SD Agchem (Europe) NV: have to pay 14.83 cr. to their ex- shareholders. Have paid 11.48 cr. in FY24 with 3.35 cr. to be remaining

-

“Due to customer” continued at 10.63 cr (same as FY23) has been largely settled now

-

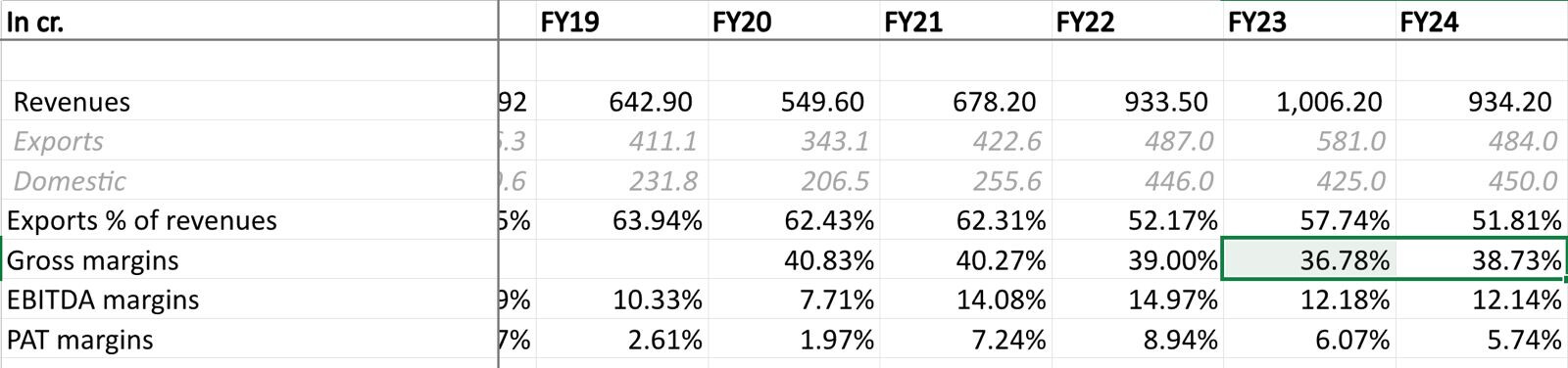

Gross margins improved from 36.8% to 38.7%, maintained market share in their products

-

Implemented new ERP software (SAP S4 Hana)

-

Lalru unit saw more product approvals from customers with new products being added. Expect Lalru utilisation to improve over the next few quarters

-

Recent product launches should mature expanding their market share and deepening relationship with their customers. They will introduce more new products for export markets during FY25

-

Faced erratic demand from critical markets and price corrections resulting in lower than expected demand. Exports continue to remain impacted due to lower prices, cautious approach by industry towards inventory and adverse weather condition. Channel destocking continues across the globe. The products with aggressive pricing from China and uncertainty around future pricing is compelling companies to delay buying decisions

-

CSR : Spent 1.81 cr. (vs 1.33 cr. in FY23)

-

# employees : 1215 (vs 1228 in FY23) + 559 (vs 530 in FY23) on contractual basis

-

Share price (low): 722.1, (high): 1391.95

-

# shareholders : 21’336 (vs 21’029 in FY23)

-

Average increase in employee salaries (ex-managerial) was 7.82% (vs 12.46% in FY23) and managerial remuneration decreased by (-)1.63% (vs (-)18.96% decrease in FY23)

-

Management remuneration : 6.16 cr. (vs 6.94 cr. in FY23) (1 cr. was commission vs 1.18 cr. in FY23)

-

R&D : 4.06 cr. (vs 3.01 cr. in FY23). Out of this, 0.18 cr. (vs 0.77 cr. in FY23) was capitalized

-

Did not hedge commodity or foreign exchange in FY23

-

Receivables : Provisioned 0.85 cr. (vs 1.03 cr. in FY23). >1 year receivables was 5.87 cr. (vs 5.9 cr. in FY23). Receivables from top customer was 83.74 cr. (vs 51.44 cr. in FY23)

-

Customer advances : 0.93 cr. (vs 6.96 cr. in FY23)

-

Revenue from top 2 customers was 384.69 cr. (vs 414.44 cr. in FY23) and 127.25 cr. (vs 138.68 cr. in FY23)

-

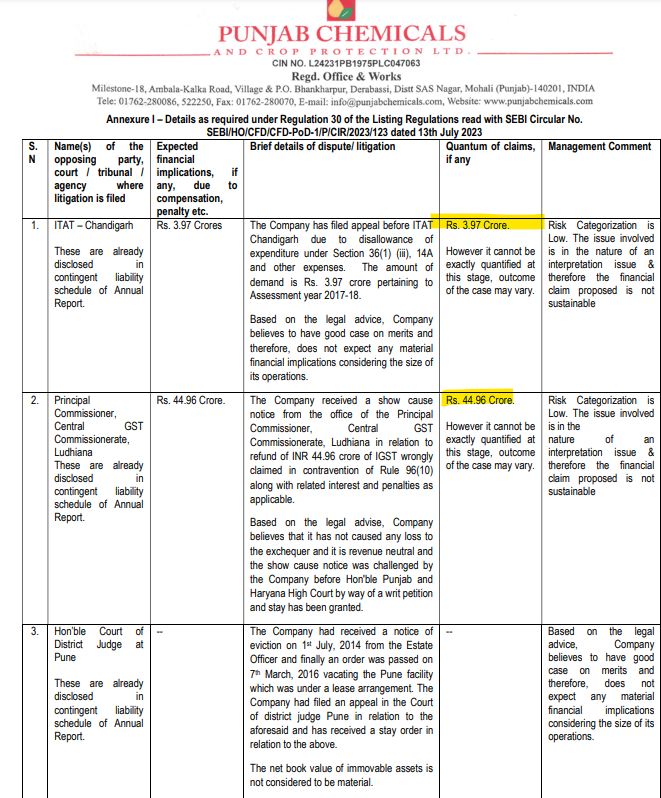

Contingent liabilities : 12.67 cr. (vs 22.86 cr. in FY23). All are tax related

-

Auditor remuneration : 42 lakhs (vs 38 lakh in FY23)

-

Foreign outgo : 129.27 cr. (vs 139.58 cr. in FY23); translates to 13.84% of sales vs 13.87% in FY23

Revenue breakup:

-

Agrochemical division Derabassi: 664 cr. (vs 739 cr. in FY23)

-

Specialty chemical division Lalru: 151 cr. (vs 153 cr. in FY23)

-

Industrial chemical division Pune: 118 cr. (vs 116 cr. in FY23)

Geographical revenue breakup:

-

India: 424.62 cr. (vs 395.42 cr. in FY23). In domestic revenues, sale of services was 34.61 cr. (vs 97.36 cr. in FY23)

-

EU (including UK): 344.79 cr. (vs 414.47 cr. in FY23)

-

Japan: 48 cr. (vs 54.33 cr. in FY23)

-

Israel: 44.03 cr. (vs 40.03 cr. in FY23)

-

USA: 3.79 cr. (vs 29.36 cr. in FY23)

-

LATAM: 26.1 cr. (vs 27.22 cr. in FY23)

-

Others: 21.19 cr. (vs 17.85 cr. in FY23)

-

Exports go to 26 countries (vs 29 in FY23)

-

Exports: 484 cr. (vs 581 cr. in FY23)

-

Europe (37% vs 41% in FY23), India (48% vs 42% in FY23), Japan (5% vs 5% in FY23), Israel (5% vs 4% in FY23), LATAM (3% vs 3% in FY23), Others (2% vs 2% in FY23)

Banking relationships

-

Working capital loan of 15.06 cr. from Yes bank (nil in FY23) at 8.85% interest rate

-

Term loan from SVC Cooperative bank is at 10.85% (same in FY23) (29.26 cr. vs 36.94 cr. in FY23)

-

Working capital loan from SVC Cooperative bank of 39.95 cr. (vs 19.16 cr. in FY23) at 9.9% interest rate (same as FY23)

-

Working capital term loan under ECLGS scheme from SVC Co-operative Bank Ltd. for 15 cr. (15 cr. in FY23) at 9.25% interest rate. Loan has a moratorium of 2 years from the date of first disbursement and is thereafter repayable in 48 equal monthly installments

-

ICDs were 16.32 cr. (vs 15.85 cr. in FY23) at 12.75-16.50% interest rate

Total income of SD Agchem (Europe) NV was 26.27 cr. (vs 17.52 cr. in FY23) with profit after tax of (-)0.8 cr. vs (0 cr. in FY23)

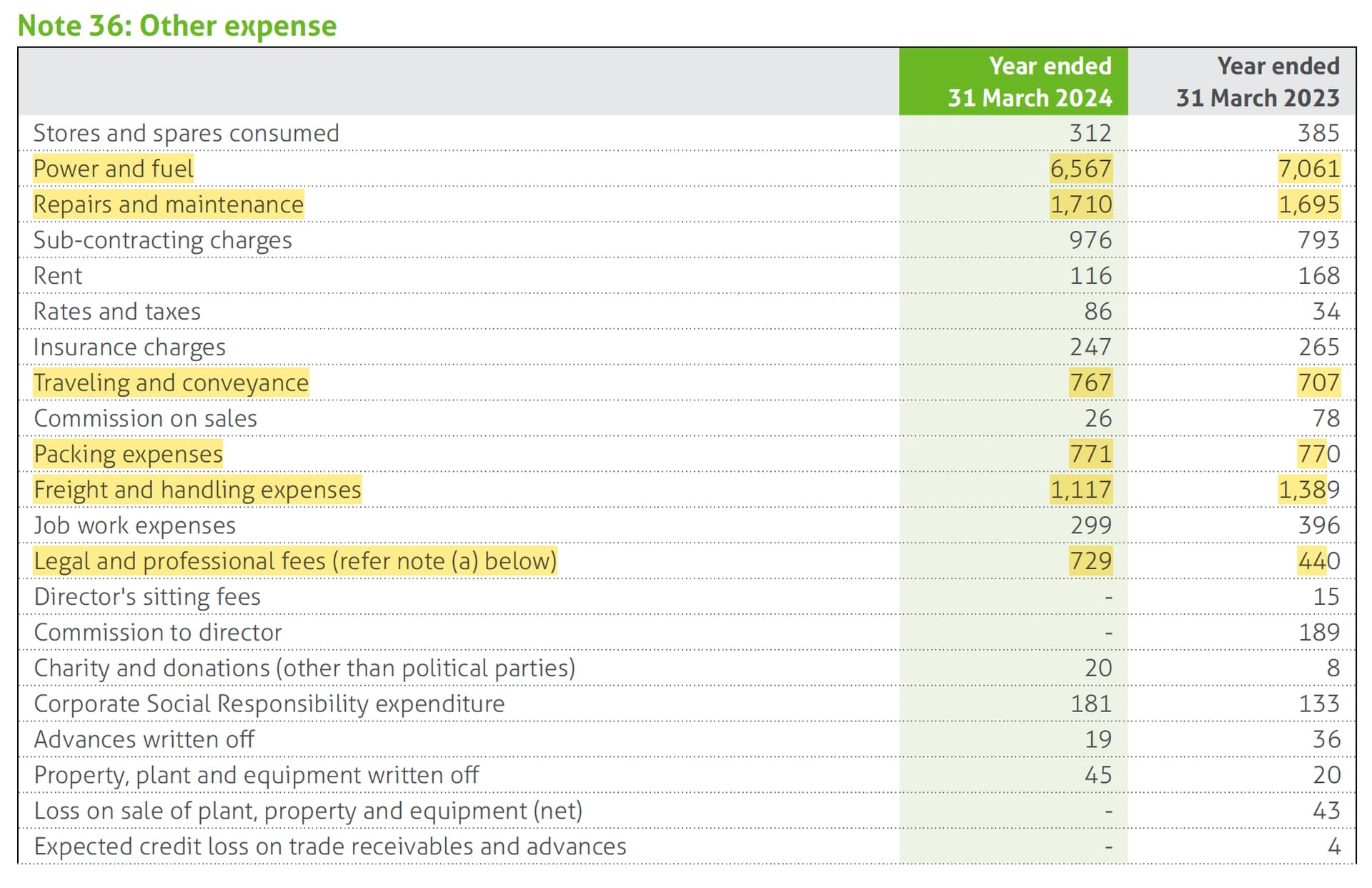

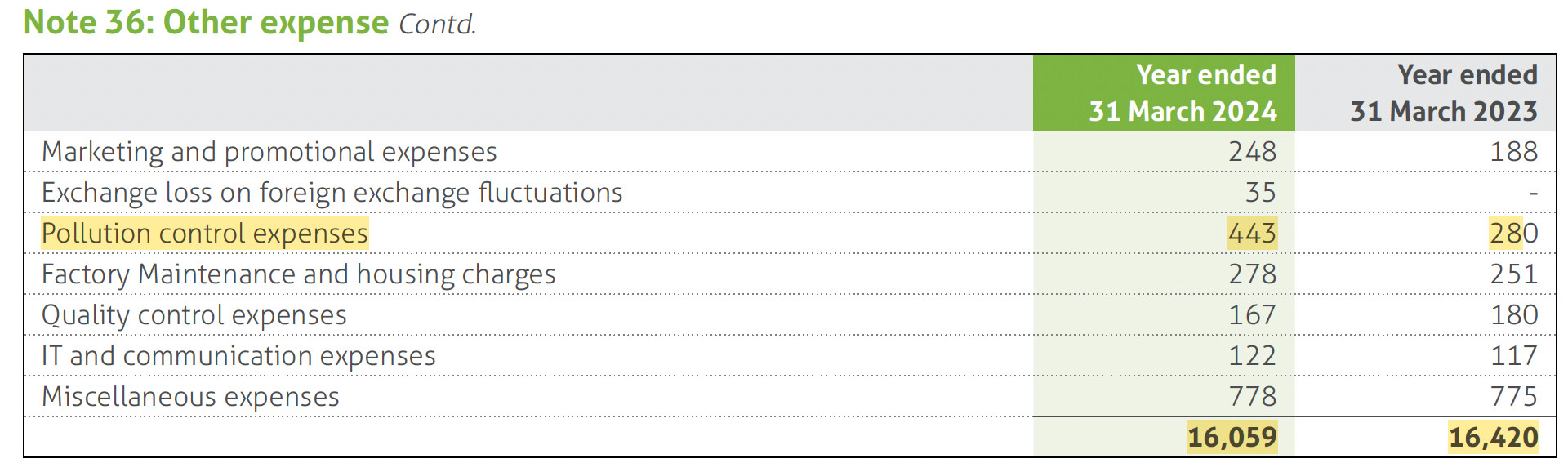

Other expenses breakup

Disclosure: Invested (bought shares in last-30 days)

12 Likes

Can see a good uptick in Sales and an even better PAT performance QoQ. Inventory expense also seems to be have come down by a big margin this quarter. Would be interesting to hear management commentary (or even from @harsh.beria93 ![]() ) about industry headwinds, china dumping and export prospects.

) about industry headwinds, china dumping and export prospects.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0b49aba1-fdbb-449f-9987-3594f4c23726.pdf

1 Like

Punjab saw 14% decline in sales which resulted in 39% decline in EPS. Demand still is sluggish and they are hoping it to turnaround this year. They have done well on gross margins and have been adding new chemistry capabilities during this downturn. Concall notes below

FY25Q1

-

Maintained volumes and marginal decline is due to lower prices. Inventory is still high in the market and demand is sluggish, expect revival by Q3FY25 along with pricing increase

-

Maintained 38%+ gross margins despite pricing pressure

-

Freight costs increased by 2.5-3 cr.

-

Commercialized 2 specialty chemical intermediate products, one shipped in Q4 and other in pilot plant stage. Lalru plant utilization will improve to ~65% in FY25

-

Derabassi is at 79% utilization, it can reach 82-85% (so not much headroom)

-

Added BASF and a new Japanese client as new customers

-

Newer molecules contributing 6-8% of revenues which should increase to 20% in next few years, these are higher priced molecules ($100/kg+). Most products are $150-250/kg priced with 40-80 tons/year demand

-

One of expenses and freight costs depressed EBITDA

-

New chemistries added: Freon reaction, cryogenic reaction, butyl-lithium reaction

-

Net working capital: 87 days (reduced from 98 days in Q4)

-

FY25 capex: 35-40 cr. maintenance. Will put growth capex after having signed contract

-

Current setup can generate 1300-1400 cr. sales

Disclosure: Invested (recently increased position size and bought shares in last-30 days)

19 Likes

Another muted quarter for Punjab (flat sales, 32% drop in EPS), demand is still subdued and lot of Chinese capacity idle. Recovery still looks far away. Concall notes below.

FY25Q2

- Channel inventory has been normalized, but supply chain is cautious (export still muted). Anticipating few more quarters before returning to normal levels. Lot of Chinese capacity is idle; Punjab is differentiating itself based on molecules

- US and Europe demand was good, Brazil is struggling

- Specialty chemical division sees higher production

- New product contribution (introduced in 2024) was 3-4% due to shifting of orders from Q2 to Q3. Products introduced in last 3 years contribute 15-20% to sales. 3 new products introduced should bring in good topline growth ($20-30/kg & 50-160 tons annual demand; meaning 8-40 cr.) – 3 new products on specialty chemical side (Lalru) to be introduced in FY25

- Product prices have reduced following raw material price drop

- Increase in other expenses was due to higher freight and repair costs

- Capex: 26 cr. in H1FY25 + 10-15 cr. expected in H2FY25 (primary capex is for infrastructure upgrade). Derabassi can have one more production block which will be commercialized once they see signs of demand revival (takes 6-9 months and 55-60 cr. with 3-3.5x asset turns)

- Adding more banks for working capital loans has reduced their finance costs

Disclosure: Invested (no transactions in last-30 days)

4 Likes