SHALIL-SHASHIKUMAR-SHROFF-MD-@-Punjab-Chemicals.pdf (1.7 MB)

4 Likes

I believe it’s due to technical reason. most chemical companies are correcting after giving spectacular return in last bull market. Leaders of last bull market hardly give any return in short term like 1-1.5 years. Here is a weekly chart indicating it.

If eps growth is strong then this downward trend must be broken.

2 Likes

There is nothing called hydrogen hydride. It is hydrazine hydrate. It was a typo while creating transcript of the concall.

Punjab came up with very good sales growth of 33%, but margins were stressed due to RM inflation and higher power costs. Management remains confident of strong growth and are guiding for 1100-1150 cr. of sales in FY23, and 1500 cr. in FY24. My concall notes are below.

FY23Q2

- Headwinds in business environment, have adopted flexible approach in product pricing (to increase market share) and are focusing on new geographies such as South America

-

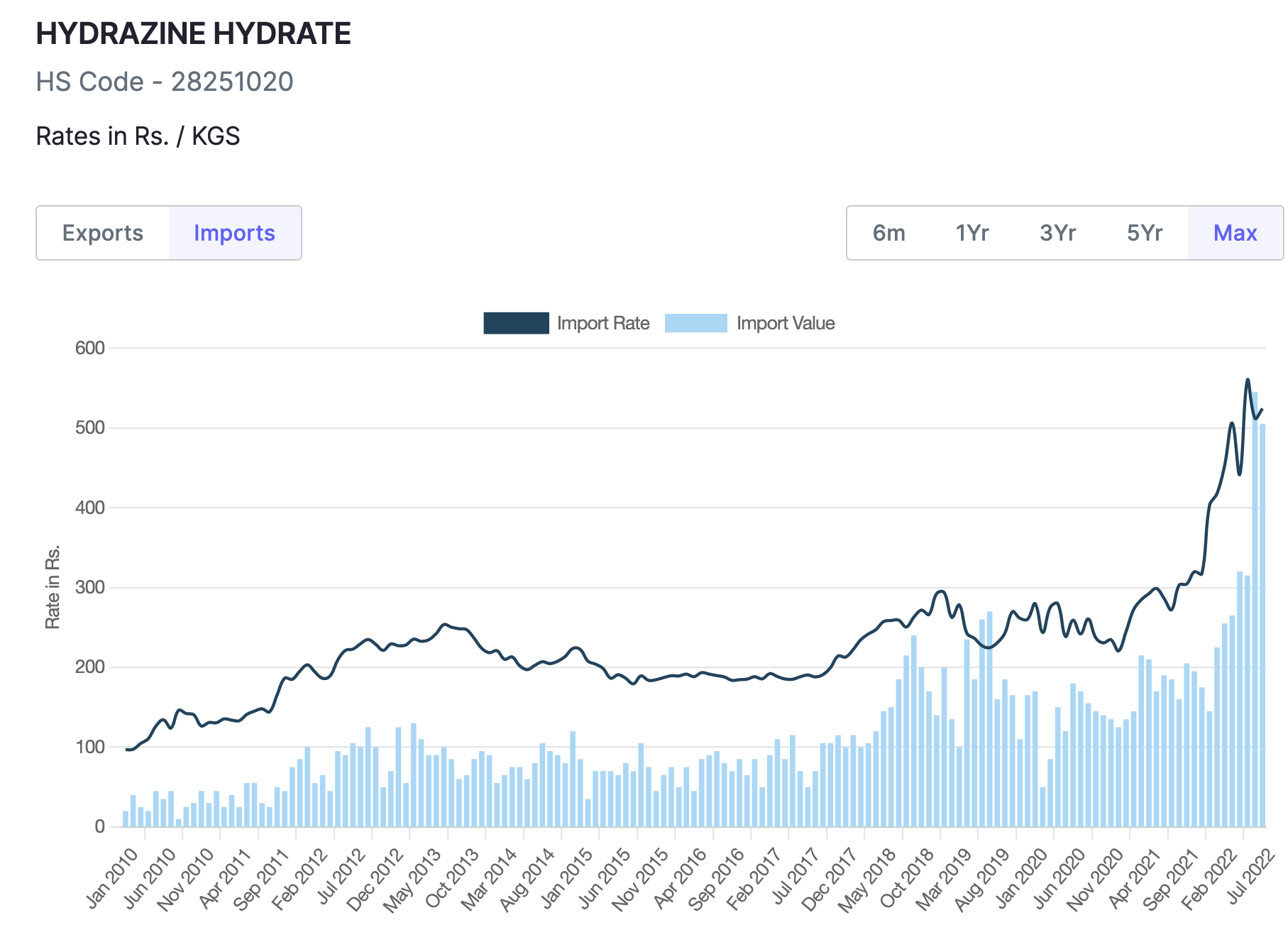

Margins: pricing pressure, product mix, carry over of high cost inventory from earlier periods (mainly hydrazine hydrate). Energy, fuel (rice husk; gone up) and freight costs impact other expense. Will be able to pass on cost pressures by Q4 and revert to 14-15% EBITDA margin

- Hydrazine hydrate prices have started tapering off

- Power costs (60 cr. in FY22 vs 32/33 cr. for IPL/Bharat Rasayan): Products (herbicides) are more power intensive + due to farm law changes in last couple of years, availability of rice husk has become a challenge

- Investing in renewing assets that are 30-40 years old (should have replacement capex of 30-40 cr. over 2-years)

- Lalru: facing raw material problems resulting in lower production and delay in registration. Hope to come back to 70%+ utilization in Q3/Q4. Large part of CRAMS business comes from Lalru, and majority of expansion will also happen here

- Derabassi: mature products, debottlenecking

- Order book: has increased from 1500 cr. to 2500 cr.

- Looking for a new site in Maharashtra or Gujarat and should finalize by end of FY23

- Lot of customer visits happening from multiple geographies (Japan, Israel, etc.)

- Phosphorus derivative: Faced pressure in this division due to pressure from Chinese suppliers. Have seen large margin drop, should see it come back to 16-18% next year

- Have seen some slowdown in demand from domestic market

- Agri segment has seen significant growth in South America

- 15%+ volume growth. Maintain 1500cr. revenue by FY24

- Thiocyclam: Full potential of this product has been delayed due to registration an should be realized in FY24

- Singapore customer molecule (most likely prosulfocarb): Registration has been delayed and growth should come in FY24

- Capex: 120-150 cr. over next 2 years

- CRAMS: 65%; 40% from generic molecules + 25% from tech transfer of 2 molecules from Japanese customers + 1 more. Are either first or secondary supplier in CRAMS business. Have quarterly review on forex adjustements

- FY23 sales will be 1100-1150 cr.

- 60-65% CRAMS + 15% specialty chemicals + 15-20% intermediate & fine chemicals. On spot basis, sales are very low (maybe 5%)

- 2 new products coming in agro + 1 in specialty chemical in FY24

- Making intermediates for Israeli company specializing in fermentation space (most likely NextFerm Technologies). It’s a small high margin business

Disclosure: Invested (position size here, bought shares in last-30 days)

19 Likes

This product is sold by UPL in Srilankan Market (Looks in-license agreement from Nippon Kayaku )

Possible reasons for high power costs are due to very old equipment (30-40 years old and they are spending about 30-40 cr to upgrade)

Reasons for low Margins

- Increase in RM costs (Hydrazine hydrate)

- High Power Costs

- To maintain the customer relationship unable to pass on the RM costs

Growth Guidance

- FY23 Target of 1100 Crores (550 Crores of that is achieved in H1 FY23 , they should do another 550 in another two quarters of FY23)

- FY 24 Target is 1500 crore

- Aiming to achieve 14-15% EBIDTA

- By end of FY23 few of the products will be approved in Brazil market

- Lalru’s utilization (where most of the CRAMS stuff happens) is low at the moment, aiming to reach to 75% utilization

- Beyond FY24 guidance will be announced soon (by Q3 or Q4 of FY23)

- Focussing more on inhouse R&D to capture market share of molecules that are going to off patent in couple of years from now

- Margins will be better in Q3 onwards (This is product that they are making exclusively Nippon Kayaku and one more product for a Singapore Customer - Syngenta? )

- Enough land at Lalru (6 acres ) to address the growth beyond FY25

- Also looking for a site in Gujrat / Maharashtra

- Growth Capex is between 120-150 Cr (At Derabassi it is mostly debottlenecking )

Management View on Generic molecules

19 Likes

Punjab came with muted nos, with sales being flat YOY. Margins have started reviving but next quarter will also be soft. Management is guiding for resumption of growth starting Q1FY24 and a 30-35% jump in revenues in FY24. Concall notes below

FY23Q3

- Shifted guidance of 1500 cr. revenues to FY25 from FY24. Will probably see 30-35% growth in FY24 and there will be a shortfall in reaching 1500 cr. in FY24. Will get projections from customers in February

- Gross margins impacted due to high cost inventory, pricing pressure from certain markets and higher energy prices. This will persist in Q4 which will be a flat quarter. Gross margins will revive in Q1FY24, if energy prices are still high then EBITDA margins can be under pressure

- All existing contracts renewed, none of their products are in red category

- Industry is into stock liquidation mode to reduce high cost inventory

- CRAMS contracts over last 2-years have ramped up well, have started reaching volume projection for the Japanese customers. 1 molecule projection has been surpassed, one is in-line, and one is lagging due to registrations

- Lalru: Expecting 1 product registration in early FY24 from Europe. Capacity utilization will increase significantly after that as there is a dedicated capacity

- Building new chemistry capabilities in line with newer demand from CRAMS customers

- Have commercialized 1 new product this year, 1 more product was supplied in small batches for registration purposes. Will start contributing in Q3/Q4FY24 and major contribution will flow in FY25

- In most CRAMS relationships, have exclusive relationship. In few molecules, there is a second supplier

- Have been able to develop local vendors for 3-4 intermediates in last few years

- Export margins are higher than domestic

- Volume has grown 8-10% in 9M FY23

- Capex: Will spend 100-150 cr. in next 2-years

Disclosure: Invested (position size here, no transactions in last-30 days)

22 Likes

A good video summarizing business model and history of Punjab Chemicals.

10 Likes

PUNJAB CHEMICALS

Innovative CRAMS - active ingredients (similar as API in pharma) - capex funded by clients (partially)

ROCE 30%

Food grade Phosphoric acid goes to Pepsi and Coca cola (clients since 20Y). Bet on CEO Vinod G (IIT Bombay Chemicals )

Rev : 48% India 39% Europe 10% Japan

Metamitron (hemani group is competitor along with best crop science)

Metconazole (Anupam rasayan, Astec lifesciences, meghmani and rallis are competitors)

Major client - UPL (client concentration risk)

What i feel they have good management barring the past acquisitions to enter US and other regulated market. (2003-2009) + Fire impacted in major products plant

We can think that the company came out of all this major liquidity problem. But that should be taken with a pinch of salt.

Debt/Equity has come down from high levels of 18 in FY11 to 0.3 in FY23 - CRAMS impact - innovator or not one needs to judge on its own.

I also think they are not doing innovator molecules (personal view) - one can think of this as a turn around story where a bet is on the management and no hoax narratives like innovators.

Rev breakup

40% - Generic CRAMS

25% - innovative molecules

valuation comfort in agro space imo. Rest cut the narrative floating around. Invest with due diligence and special care on position sizing.

4 Likes

Dear Sir your analysis is extremely mindful. Based on my personal opinion adding this stock to core portfolio seems unlikely. Here are few factors -

Promoters holding

Working capital days

Cash conversion cycle

Borrowings and other liabilities > reserves vis a vis fixed assets and gross block

OPM too thin and Interest increase.

The sector has a lot of hurdles. I personally will wait for it to showcase a better performance.

Many thanks

(For educational purposes)

1 Like

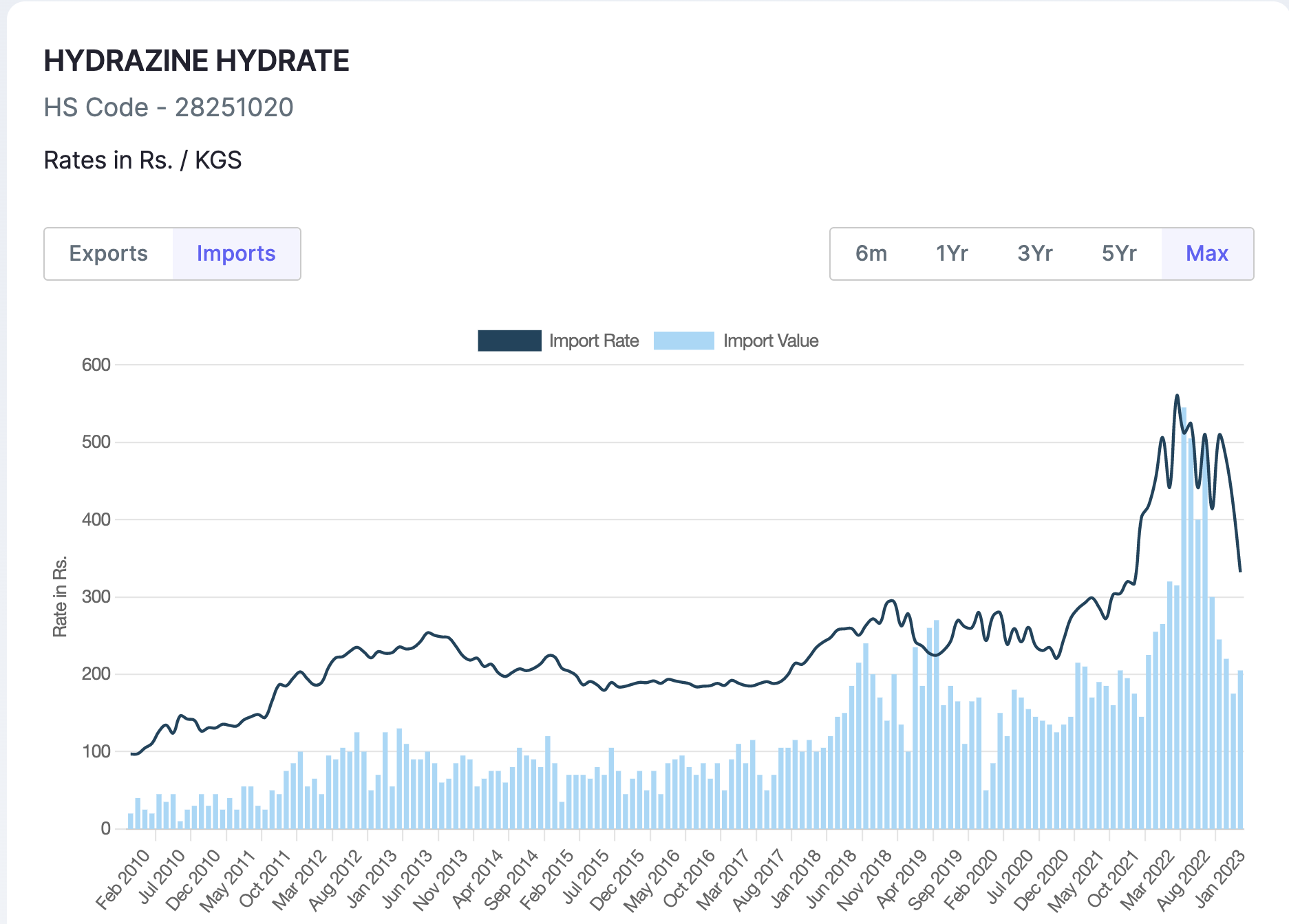

Hi Harsh,

Could you please share latest price chart of Hydrazine Hydrate.

Also, could you please inform the source to get the price chart.

regards

narendra

Horror set by Punjab chem:- Seems generic Agchem restocking is similar to what happened to API’s last year.

First Astec and now this. Innovator CMO’s will stand apart. We will get to know true product mix by strength of margins in headwinds.

Disc: not invested. Tracking the sector.

8 Likes

market knew in advance so stock corrected more than 50% inspite posting okayish result till now !

7 Likes

All generic cos are in stage 4… Agchem prices have been correcting for last 6months. Smart hands track this data ![]()

12 Likes

I’d like to believe a lot of this is in the price though. The stocks been correcting for months on not so horrible numbers. It is in stage 4 and no way of knowing where the base will be, but seems not too far away from the bottom of the business cycle. Pretty close to trough business cycle and trough margin. The call will tell us more.

Disclosure: Took a small position very recently at about 800. Not great timing I guess ![]() Looking to add once base forms.

Looking to add once base forms.

6 Likes

What’s your view on the results? @harsh.beria93. Would love to know your take on the results too. Also do you think that rise in raw material costs is the only factor for their margin depletion?

1 Like

These are some of the notes I could jot down during today’s conference call.

- Company aims to develop molecules which can offer them a revenue visibility for at least 15- 20 years.

- Potential targeted revenue still stands at1500Cr, no timeline given this time. This number includes revenues from both existing products and products in the pipeline.

- Company wants to invest in energy to save on costs.

- Reasons for lower revenue in FY23 include domestic demand slowdown and inventory correction.

- One important product running at full capacity, while the other will have similar or higher volumes in the coming year.

- Capacity addition through debottlenecking at Derabassi (2000 tonnes) and Laluru plants(1000 tonnes)

- Company expects margins to return to last year’s levels in FY24.

- Focus on R&D to increase product profile.

- Inventory correction is industry-wide, not just for the company.

- Product movement has started, and company expects better margins with lower raw material costs.

Altogether I could not really find clarity in the company’s statements in terms of capacity utilization and domestic demand. Also wanted to understand deeply as to how much of the revenue levels were disturbed due to “adverse climate”. I would be closely tracking the upcoming quarters for a better understanding.

7 Likes

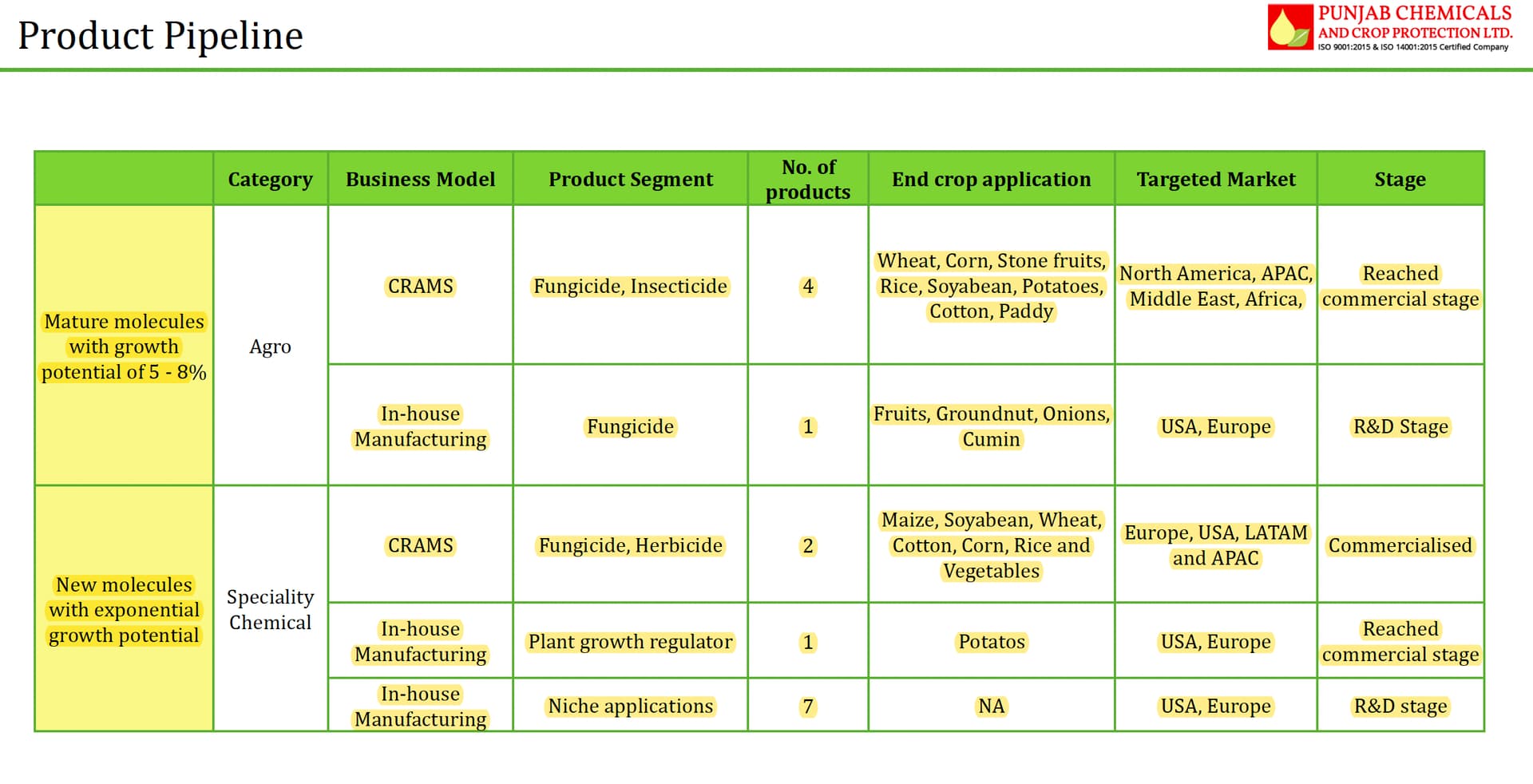

Company came out with a howler. Although nos look really bad, there were some interesting insights in this call and presentation. For the first time, thay talked about their product portfolio in the presentation.

They also talked about their recent hirings and how they are trying to professionalize the company with hires from large agchem cos (have highlighted relevant details).

Another interesting development was installation of MVRE plant this year. Although, this doesn’t add to production capacity, its very important for the kind of business model Punjab is targetting.

Now coming to the reasons behind such a howler in sales and why there were lots of questions around Metamitron: There are 2 companies from India who make Metamitron at scale, Punjab Chemicals and Hemani. Punjab controls 65% of market and Hemani controls the remainder (talking about technical market). The main difference between the two is that Punjab supplies to ADAMA and UPL on a contractual basis (ADAMA/UPL control the end formulation market), whereas Hemani supplies on spot basis. In past few months, it seems Punjab hasn’t been able supply this molecule and people have been worried if Hemani got into some contract relationship and displaced Punjab. Management categorically denied this on the call and attributed low sales to large inventory pileup at UPL/ADAMA’s end which is getting liquidated. Additionally, they guided that Metamitron volumes in FY24 will be equivalent (or maybe more) vs FY23. This molecule is the largest contributor to Punjab and thats why its so important.

If we remove Metamitron, Punjab has done very well in all their other export molecules, which is why exports only showed a 15% decline (vs 35% decline in domestic sales) .

More interestingly, Punjab has been able to gain market share in Diflufenican in LATAM, and are now expanding capacity from 300 tons to 800 tons. This is the molecule where they were facing stiff competition from Chinese peers and had to drop prices to gain market share.

In terms of importance, Metamitron, Metconazole and Diflufenican are the 3 main molecules for Punjab and contribute almost 50% to their sales.

One major negative for me was order book reduction to 1200 cr. In FY23Q2, they had mentioned that order book had increased to 2500 cr, but it seems to have been reduced by half. My concall notes are below:

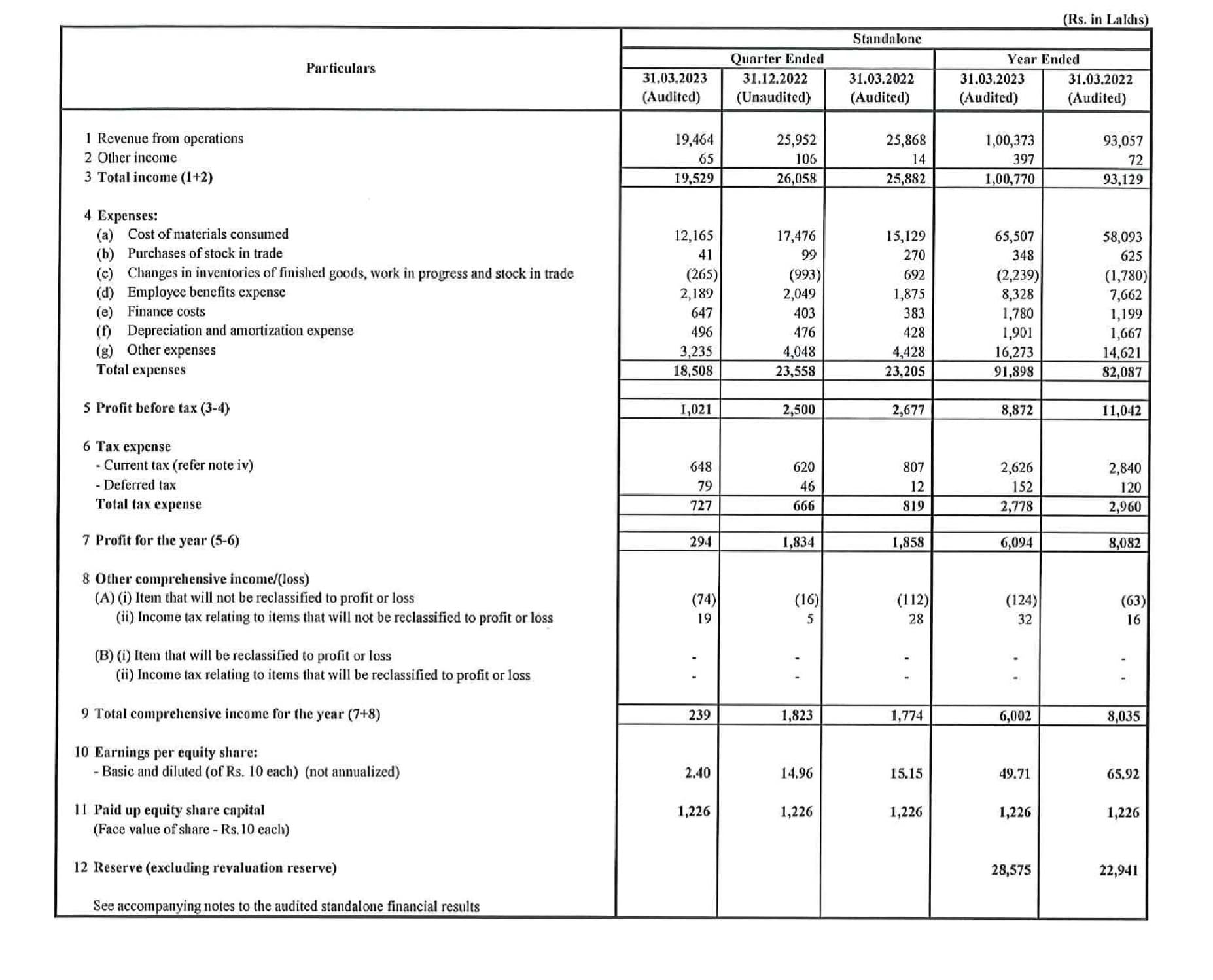

FY23Q4

- 20% volume growth in FY22 and no volume growth in FY23

- Overall drop in sales is because of lower domestic demand + inventory correction in Europe

- Indian sales will recover in Q1FY24 and Europe will recover by Q2FY24

- Industrial chemical performance has been very steady

- Have seen demand slowdown in pharma business. Pharma intermediate hasn’t been commercialized due to inventory correction at customer end

- Energy prices have been high (high rice husk prices), have started investing in alternative sources of energy

- Herbicide: have got approval for Australia + certain countries in Europe (should get full approval by January 2024) – is this prosulfocarb?

- 4 products: 1 KSM commercialized, 1 agchem for Brazil will be commercialized in September, 1 will take time and 4th one (intermediate) is delayed

- LATAM product (Diflufenican): Have reached 55-60% market share in Argentina. Main competitor is Chinese

- Metconazole: Capacity is fully utilized

- Metamitron: Inventory correction is getting over, similar or higher volumes in FY24

- Added one fungicide (12 step process). Delivered 20 tons to market and it has potential to ramp up to 200-300 tons

- New products have at least 5-7 step process

- Focusing on bromination chemistry (azole range of products)

- Order book tapered down to 1200-1300 cr. but will increase by 1500 cr.

-

Capex:

o Capacity addition is mainly for a herbicide (probably Diflufenican; from 300 tons to 800 tons/year). Hoping to double sales this year

o Capacity addition: Derabassi: 2000 tons/year, Lalru: 1000 tons (for an intermediate) - 18-20% EBITDA margin will be achieved after FY25 with ramp up of newer products, target for FY24 is 14-15% EBITDA margin

- Complete leadership team has been built in last 2-years, EHS processes have been strengthened and investing more in R&D

- Dr. Vijay Kaushik (ex Bayer, Meghmani, PI) has recently joined as head of R&D

- Receivables look high because there was large sales booked in March

Disclosure: Invested (position size here, no transactions in last-30 days)

36 Likes

AR23 notes

Quick summary:

- Top two customers account for 55% of sales (vs 62% in FY22)

- They have lost a major contract due to registration issues (more in description below)

- Management is investing in team + capabilities to grow business

AR23 notes

Miscellaneous

- Portfolio of 12 products (vs 10+ in FY22) in contract manufacturing for MNCs and Indian companies

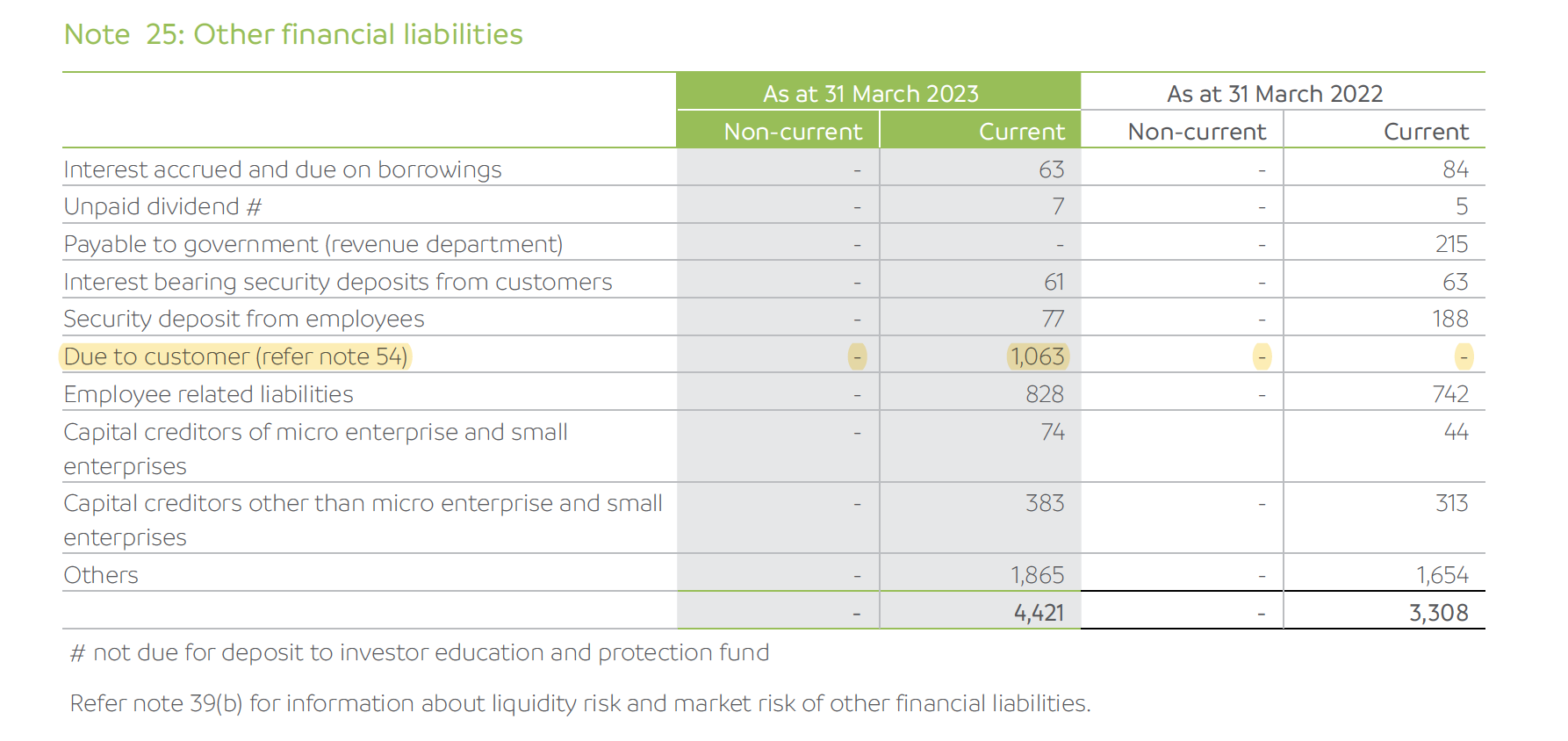

- Had an item called “due to customer” of 10.63 cr. This is relation with an overseas customer and loss of contract due to registration issues . During FY23, as a result of product registration regulatory issues faced by the customer , the Company and the customer have preferred to enter into a settlement arrangement pursuant to which the original contract for supply of goods now stands terminated. Company has recognized 2.84 cr. as settlement income (net of certain expenses aggregating to 2.25 already incurred pursuant to the original contract of supply)

- During last two years, have invested in building new managerial positions, inducting professional talent and investing in research. Widened capabilities across more chemistries

- Enhanced process yield, decline in energy consumption per unit of output. Looking to use new hybrid technology to moderate power and fuel costs.

- Used idle manufacturing capacity for new product development in existing and adjacent product spaces . These products are awaiting customer approval while some others are at a pilot production stage

- Looking to double proportion of revenues from new products

- Continued to transform its approach from product sales to being solution providers

- Macro issues: floods, droughts, increased power, fuel and freight costs, geopolitical challenges

- Has approved Effluent Treatment Plants with incinerators to treat the waste materials in Derabassi and Lalru. For disposal of solid waste, it has a tie-up with Common Effluent Treatment Plants close to manufacturing sites. Both are zero liquid discharge facilities

- Installed MVRE (Mechanical Vapor Recompression Evaporation technology) to ensure zero liquid discharge. Installed scrubbers in its boilers to control emissions. Undertook asset upgradations, such as installation of multi-effect evaporator for water treatment

- CSR : Spent 1.33 cr. (vs 75.94 lakhs in FY22)

- Employees : 1228 (vs 1213 in FY22) + 530 (vs 867 in FY22) on contractual basis

- Share price (low): 821.7, (high): 1597.95

- Shareholders : 21’029 (vs 19’419 in FY22)

- Average increase in employee salaries (ex-managerial) was 12.46% (vs 10.34% in FY22) and managerial remuneration decreased by (-18.96%) (vs 43.65% increase in FY22). Managerial remuneration decreased due to superannuation of some KMPs

- Management remuneration : 6.94 cr. (vs 6.04 cr. in FY22) (1.18 cr. was commission vs 2.26 cr. in FY22)

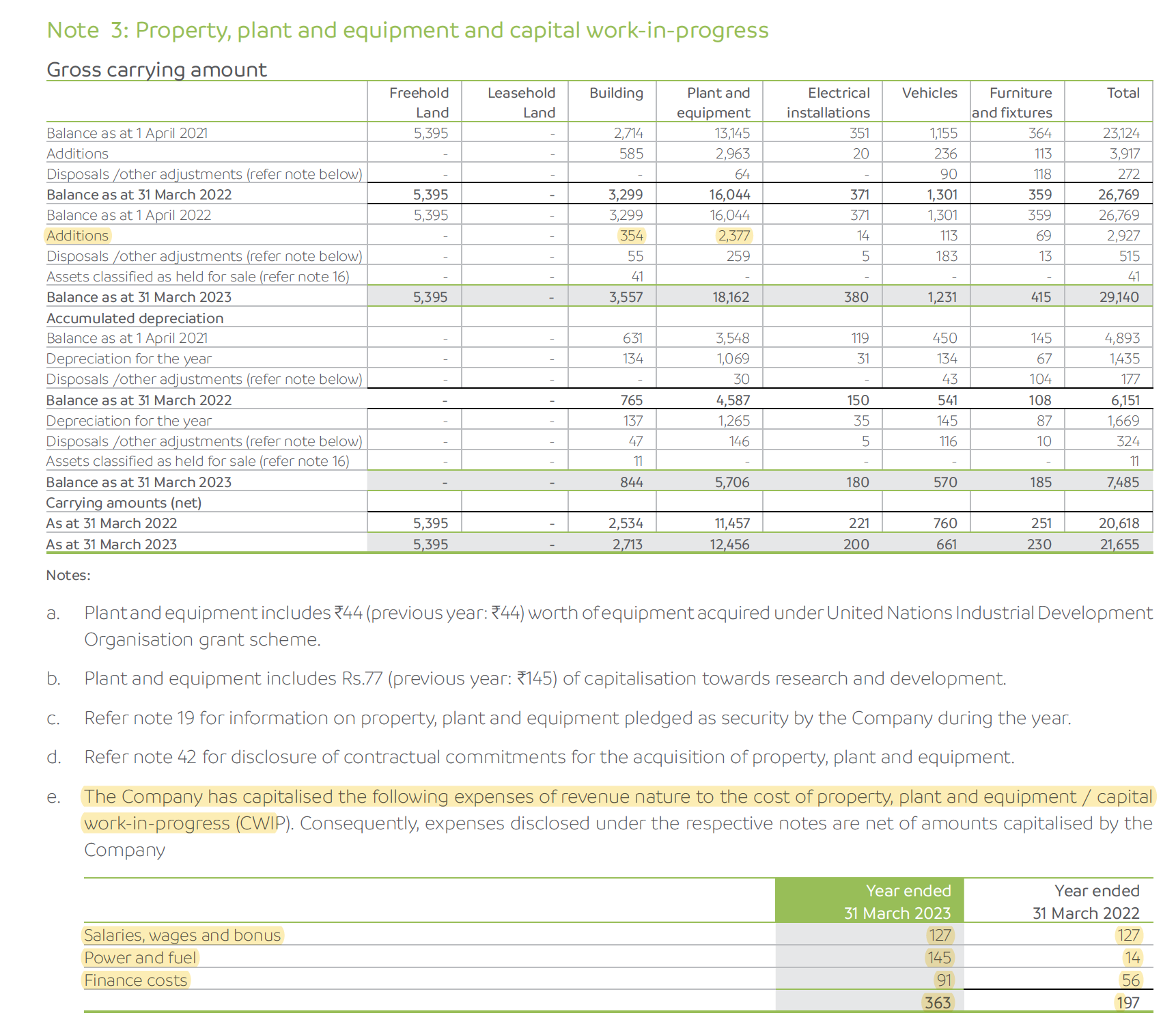

- R&D : 3.01 cr. (vs 3.3 cr. in FY22). Out of this, 0.77 cr. was capitalized (vs 1.45 cr. in FY22)

-

Capex: capitalized certain part of operating expenses in CWIP

- Did not hedge commodity or foreign exchange in FY23

-

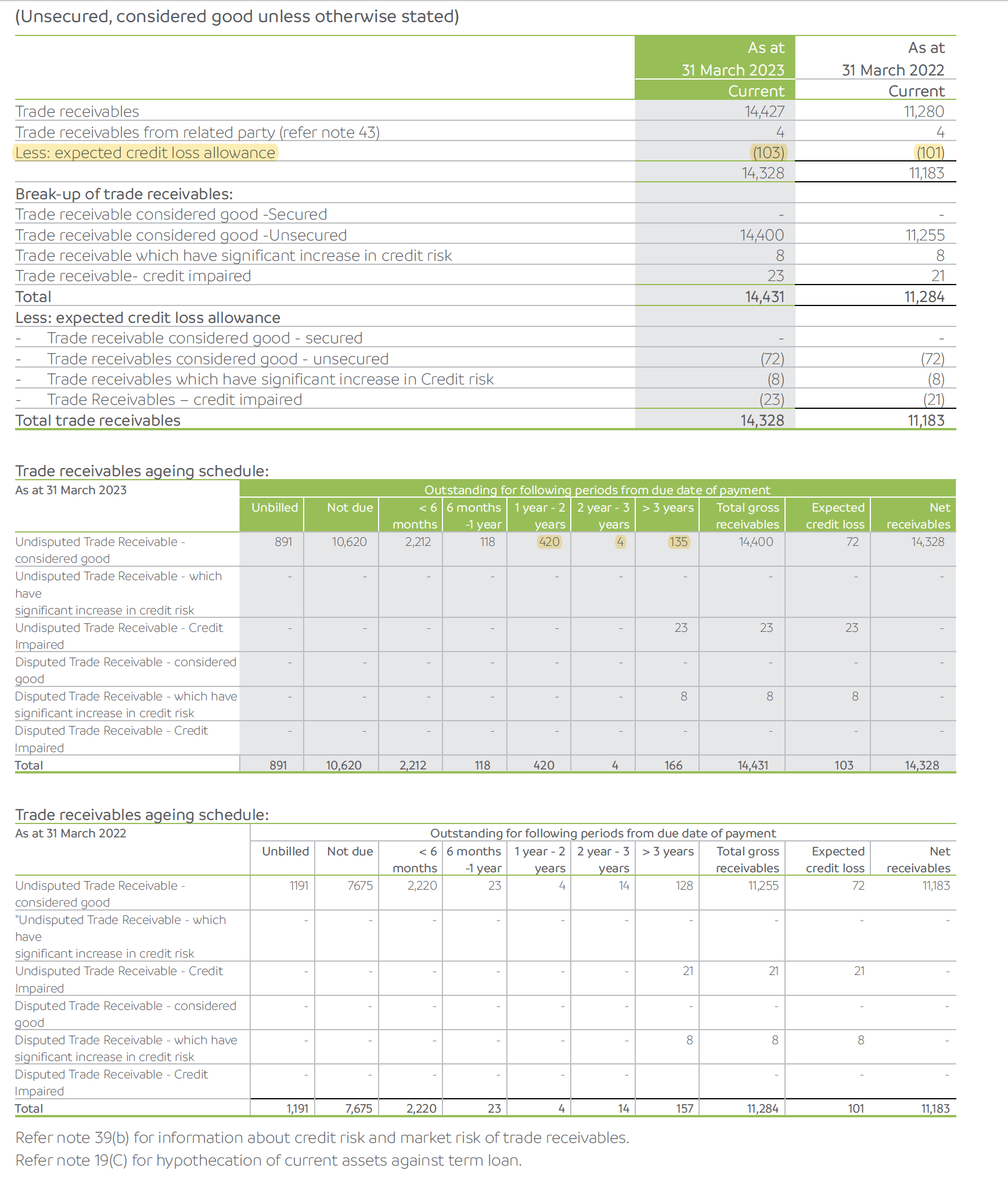

Receivables : Provisioned 1.03 cr. (vs 1.01 cr. in FY22). >1 year receivables increased to 4.6 cr. (vs 1.46 cr. in FY22)

- Customer advances : 6.96 cr. (vs 18.6 cr. in FY22)

- Revenue from top 2 customers was 414.44 cr. (vs 503.71 cr. in FY22) and 138.68 cr. (vs 75.83 cr. in FY22)

- Contingent liabilities : 22.86 cr. (vs 13.41 cr. in FY22). All are tax related

- Auditor remuneration : 38 lakh (vs 34 lakh in FY22)

- Foreign outgo : 139.58 cr. (vs 114.58 cr. in FY22); translates to 13.87% of sales vs 12.27% in FY22

Revenue breakup:

- Agrochemical division Derabassi: 739 cr. (vs 664 cr. in FY22)

- Specialty chemical division Lalru: 153 cr. (vs 156 in FY22)

- Industrial chemical division Pune: 116 cr. (vs 111 cr. in FY22)

Geographical revenue breakup:

- India: 395.42 cr. (vs 426.96 cr. in FY22). In domestic revenues, sale of services was 97.36 cr. (vs 126.11 cr. in FY22)

- EU (including UK): 414.47 cr. (vs 360.71 cr. in FY22)

- Japan: 54.33 cr. (vs 89.8 cr in FY22)

- Israel: 40.03 cr. (vs 10.48 cr. in FY22)

- USA: 29.36 cr. (vs 1.81 cr. in FY22)

- LATAM: 27.22 cr. (vs 4.9 cr. in FY22)

- Others: 17.85 cr. (vs 22.4 cr. in FY22)

- Exports go to 29 countries

Banking relationships

- Term loan from RBL bank at 11.25% interest rate is repaid fully (vs 4.96 cr. in FY22)

- Term loan from SVC Cooperative bank is at 10.85% (vs 9.7% in FY22) (36.94 cr. vs 44.58 cr. in FY22)

- On 20 April 2023, availed working capital term loan under ECLGS scheme from SVC Co-operative Bank Ltd. for 15 cr. (0 in FY22) at 9.25% interest rate. Loan has a moratorium of 2 years from the date of first disbursement and is thereafter repayable in 48 equal monthly installments

- ICDs were 15.85 cr. (same in FY22) at 12.75-16.50% interest rate

Total income of SD Agchem (Europe) NV was 17.52 cr. (vs 12.58 cr. in FY22) with profit after tax of 0 cr. (vs 2.89 cr. in FY22)

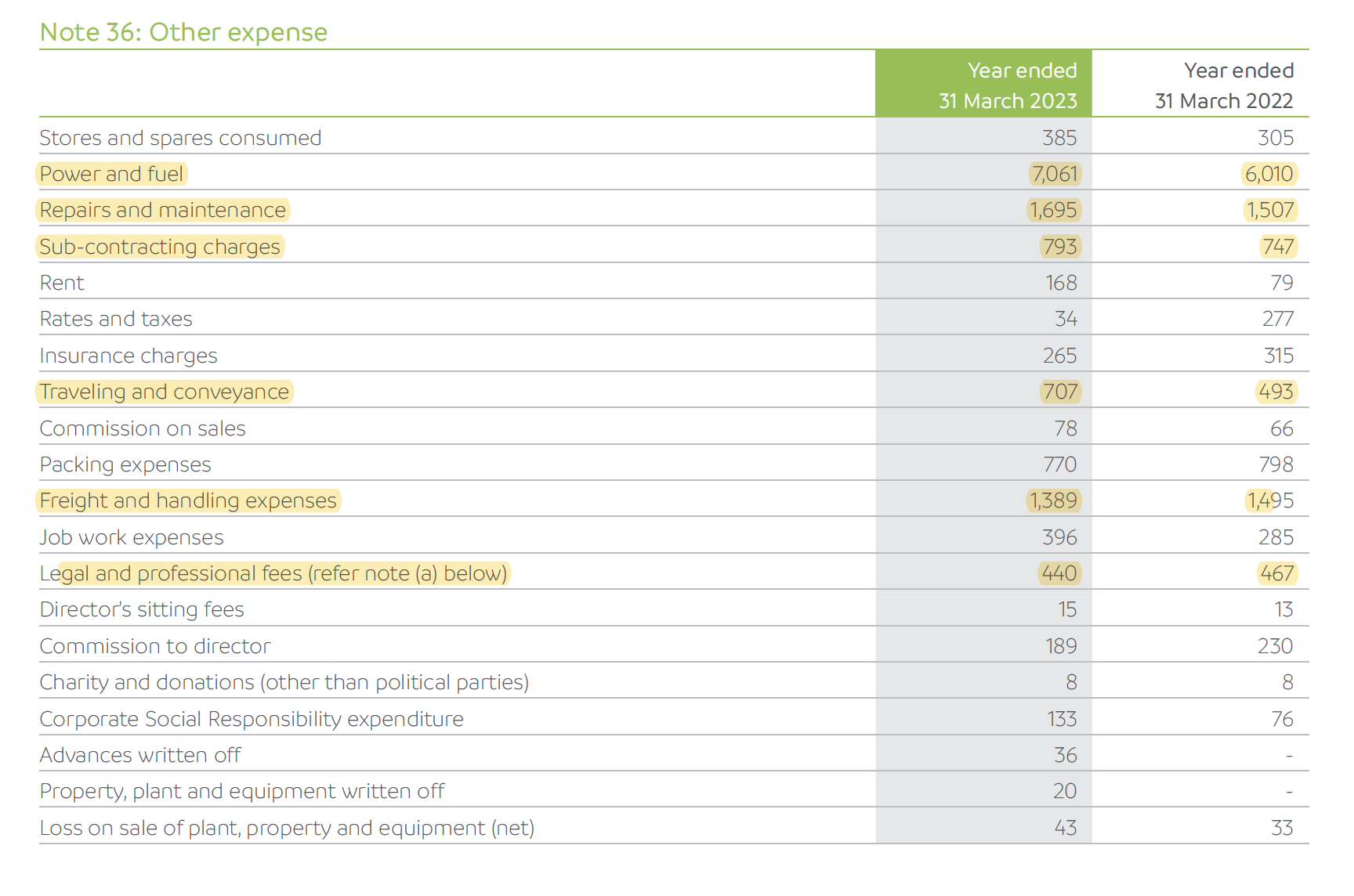

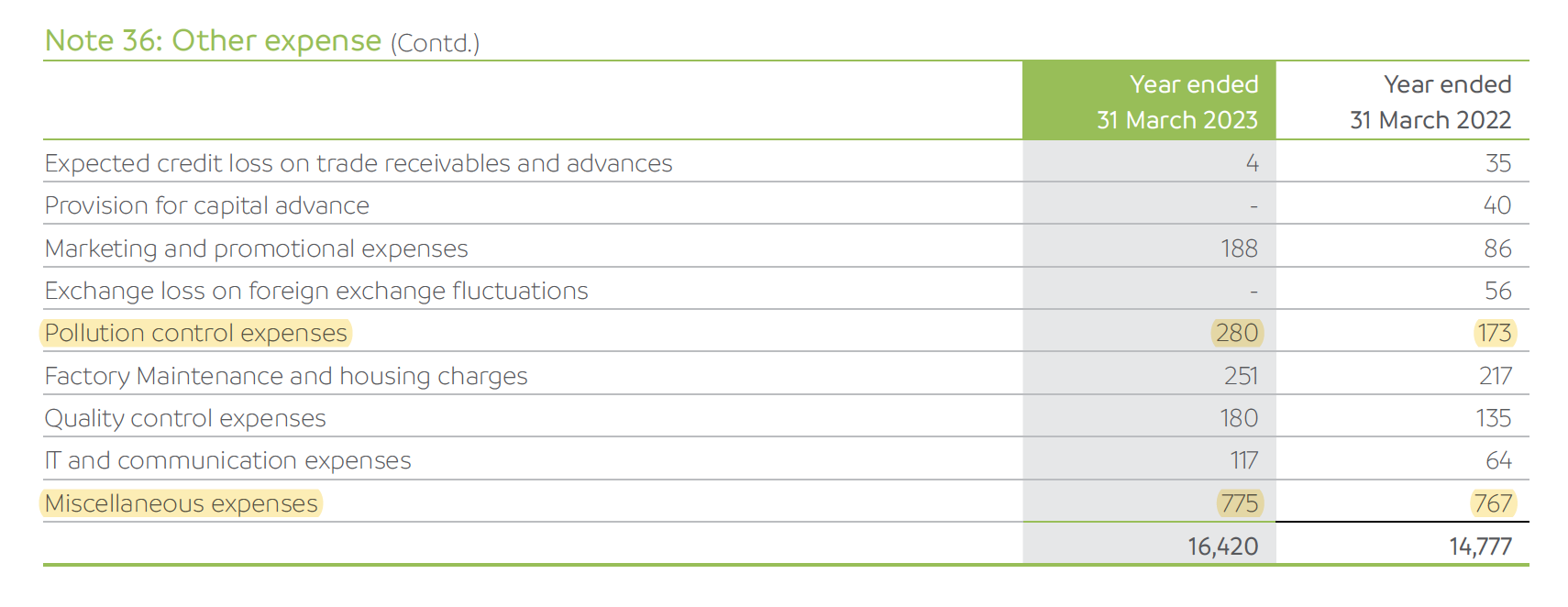

Other expenses breakup

Disclosure: Invested (position size here, no transactions in last-30 days)

22 Likes