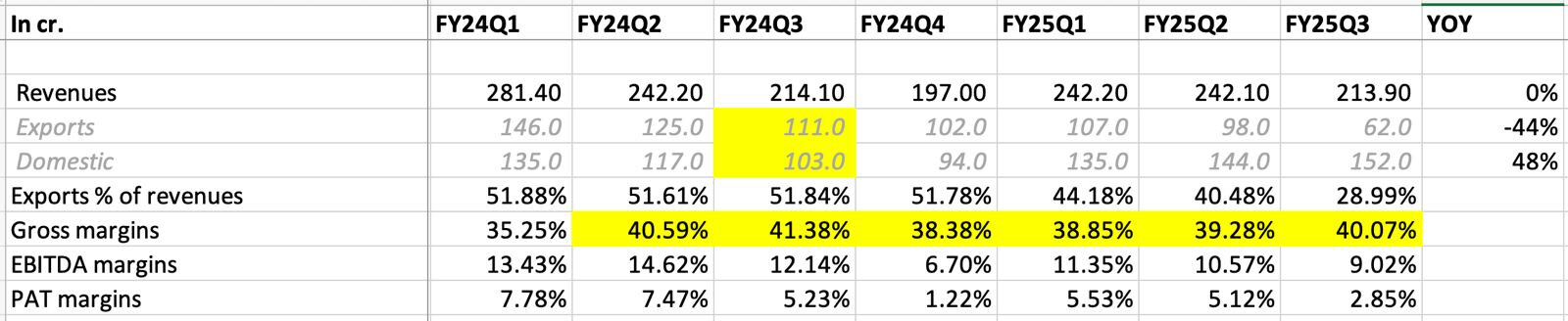

Another muted quarter for Punjab (flat sales, 46% drop in EPS). Exports took a huge drop which was countered by high domestic sales growth. Its impressive that during this entire downturn, they have maintained good gross margins, but have been hit on EBITDA/PAT margins. Concall notes below.

FY25Q3

- Prices have stabilized, export demand is subdued (higher supply, margin challenges in their patented molecules which have gone off-patent)

- EBITDA margins have been impacted due to higher freight costs and forex losses (2.3 cr.) despite 40% gross margins

- There has been delay in new product introduction for exports, they are expecting larger volumes in Q2/Q3 FY26

- Expect ~935 cr. revenues in FY25 and 12-14% growth in FY26

- Order book cycle has reduced to 2-3 quarters rather than longer cycles because customers do not want to hold high inventory

- Added new products for domestic market which has resulted in higher domestic sales (intermediates, specialty chemicals). New product portfolio contributed 15% to revenues

- Next few quarters are looking exciting, new product pipeline is exciting with higher margins

- Saw a big order in industrial chemicals from a beverage manufacturer to service their entire demand from their new upcoming facility in Gujarat. This can double the scale of their industrial division

- They will be investing in a new manufacturing unit parallelly with the customer and commercialization will only happen in late FY26 or early FY27. Exact capex commitments to be disclosed in Q2FY26

- Hindustan Coca-Cola is building a new facility in Rajkot, Gujarat to produce juice and carbonated drinks. The facility is expected to open in 2026

- They make 18-20% EBITDA margins in phosphoric acid division

- Took a 3-week maintenance shutdown at Lalru, presentation mentioned Lalru production numbers is incorrect

- 15-18 cr. is towards upgradation of existing facility in 9MFY25, majority of costs were in Q3

- Working capital cycle: 90 days for domestic, <60 days for international

Disclosure: Invested (no transactions in last-30 days)

5 Likes

Adding my notes from their Q4 call and recent rating report.

04.04.2025 Care

- Bank facilities increased to 105 cr. (vs 80 cr. earlier)

- Bank utilization: 81% for 12 months ending February 2025 (vs 79% for July 2024)

- PBILDT margin were lower at 10.69% in 9MFY25 (vs 13.83% in 9MFY24) resulting from decline in exports, higher employee expenses, exchange losses and higher freight costs

- In 9MFY25, exports declined to 38% (vs 52% in 9MFY24)

FY25Q4

- Environment remains tough especially exports (lower demand, more competition), most product prices down 25-50% from peak levels in 2022. Maintained market share in existing products and took price cuts to maintain share

- Commercialized four new products in FY25 in addition to five products commercialized in FY24, these contributed to 12% of FY25 sales (vs 7% in FY24). These are in Specialty Chemicals focused on India, Europe and Japan and are expected to grow at 15-20%

- Existing products saw 9% decline (70% from lower pricing, 30% from lower volume)

- Expect 18-20% growth in FY26 with improving margins, inventory level is very low in the channel

- Looking to commercialize 5 new products in FY26

- High inventory is because of increased production to improve asset utilization. Expect it to improve by Q2FY26

- Capacity utilization: Derabassi 71%, Lalru 64%, Pune at full utilization

- Reinitiated exploring establishment of new production facility (in Gujarat) expected to be operational by end of FY27, to be finalized in next few months and can double their topline. Will invest 250-300 cr. over a 4-year period and expect 2-2.2x asset turns conservatively and 2.5-3x if prices normalize

- Food grade phosphoric acid: Hindustan Coca-Cola Beverages transferring business to independent bottlers like Kandhari Global Beverages doesnt impact them as they get approval at the corporate level. Their new plant in Gujarat is expected to also house this division (120 cr. out of 250-300 cr. capex for this division)

- Chinese raw material dependency has reduced from 25-28% three years ago to 18-19% now

- R&D: have been spending 2-3% of total expenses. Team size increased to 30 (vs 28 earlier) and is expected to double in FY26

- Avg. Interest rate on debt was 9% in FY25 (vs 9.25% in FY24)

- Vikash Khanna appointed as their CFO

Disclosure: Invested (no transactions in last-30 days)

9 Likes