Respected Investors, My name is Raghav Agarwal and I am a final year management student. I have been reading a lot on this wonderful platform and am finally able to present everyone with my first thread on Punjab Chemicals and Crop Protection Limited. I am open to your wonderful suggestions and your subtle criticisms and I hope we can have a fruitful discussion of this excellent company on this extraordinary platform.

*Punjab Chemicals & Crop Protection Limited

Overview*

Punjab chemicals and crop protection limited (PCCPL) is an agrochemical manufacturing company based in Punjab. The company was founded in 1975 with a vision of being an integral part of the strategic supply chain both domestically and globally. It started its manufacturing facility by initially producing generic chemicals like oxalic acid. It now caters to agrochemicals, pharmaceuticals, intermediates and industrial and special chemicals and is now manufacturing various types of agrochemicals, for example, Metamitron Ethofumesate, Diflufenican, Lenacil and Cyanazine, with Metamitron and phosphorus acid being the major products.

The company owns two manufacturing units in Punjab and has leased one in Pune. The company also has a wholly-owned subsidiary in Belgium by the name of SD Agchem, which caters to the demands in the European market. Agrochemicals hold 80-85% of revenues which further breaks into 3 segments which are herbicides, contributing to 55%, fungicides contributing to 30% and insecticides contributing to 15% to the revenues. Out of these Agrochemicals, CRAMS contribute 60-65% to the revenues and this division is expected to grow 3-4x in the coming years. The pharmaceutical’s division provides Analytical reagents to pharma companies like divis labs and Laurus labs. The top five Analytical reagents contribute to 30-40 Cr.

Export- domestic sales breakup comprises 63% of the revenues generated from exports and 37% from the domestic market. The domestic market further breaks down into two parts

Agrochemicals amounting to 40% and Intermediates amounting to 60% to the domestic segment.

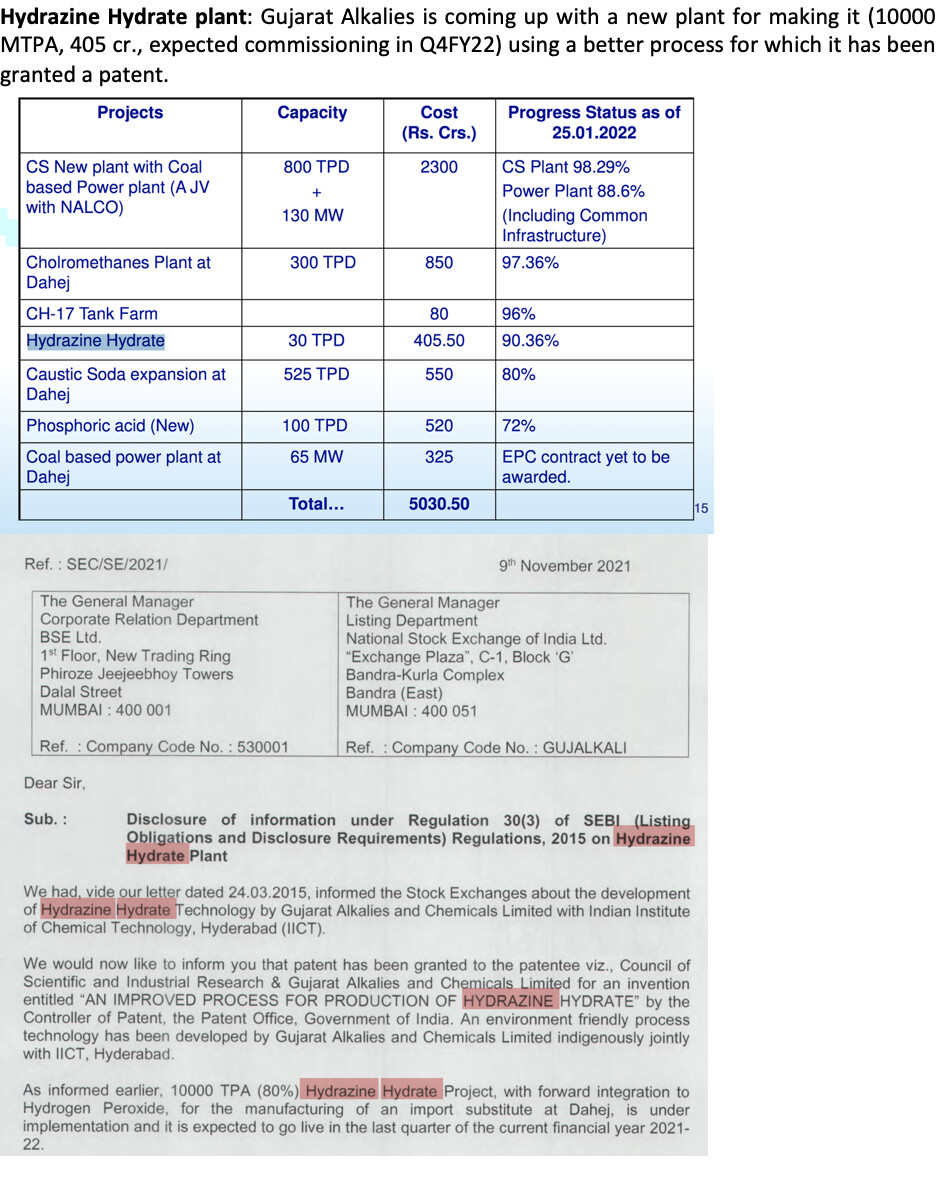

Location-Wise Revenue Breakup FY21

| Manufacturing Units | |||

|---|---|---|---|

| Derabassi, Punjab | Pimpri, Pune | Lalru, Punjab | |

| Size | 24Acres | 1.5 Acres | 23.5 Acres |

| Capacity | 29700MT | 3347 MT | 5778MT |

| Capacity Utilization | 80% | 95% | 73% |

| Certifications | ISO:14001 | FSSI | ISO:14001, ISO:9001 |

| Divisions | Agrochemical manufacturing | Industrial Division | Agrochemical manufacturing |

| Revenue Contribution | 60% | 5-10% | 30-35% |

Fundamentals

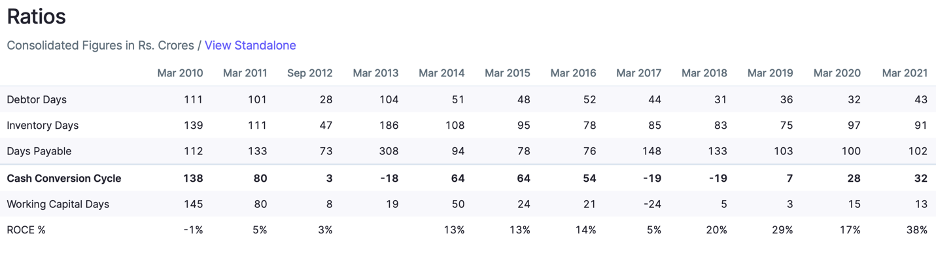

The company generated consolidated revenue of 678 Cr in the FY20-21 with an EBITDA of 97Cr and an EBITDA margin of 14.3%. The net profit was aggregated to 49.1Cr with a PAT margin of 7.2%. Punjab chemicals have an excellent ROEof 40% and ROCE of 32%, which showcases the excellent returns of the company on their equity as well as their capital employed.

| Q2FY21 | Change% | Q2FY22 | FY20 | Change% | FY21 | |

|---|---|---|---|---|---|---|

| Revenue | 164Cr | 27% | 209Cr | 550 | 23% | 678 |

| EBITDA | 23 Cr | 34% | 31Cr | 42 | 131% | 97 |

| EBITDA Margin | 13.8% | 1% | 14.8% | 7.6% | 6.7 | 14.3% |

| PAT | 12% | 6% | 18% | 11 | 345% | 49 |

| PAT Margin | 7.2% | 1.4% | 8.6% | 2% | 5.2% | 7.2% |

| Accounting Ratios | FY21 |

|---|---|

| Debt/Equity | 0.5 |

| ROE | 39.83% |

| ROCE | 38% |

| EPS | Rs.40 |

| P/E | 30.02 |

| Interest Converge Ratio | 10.3 |

| Current Ratio | 1.19 |

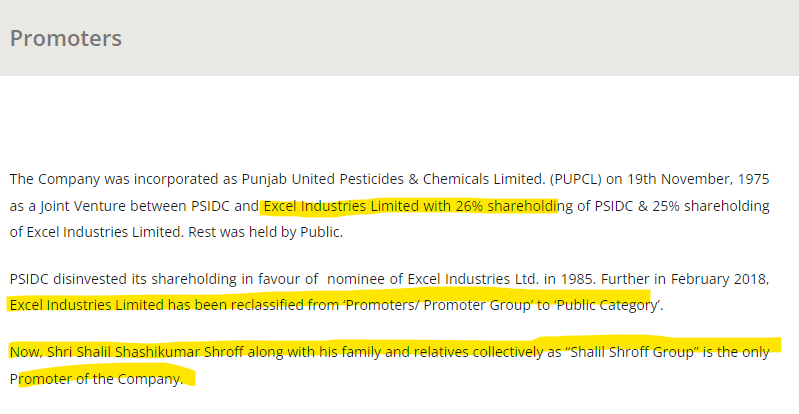

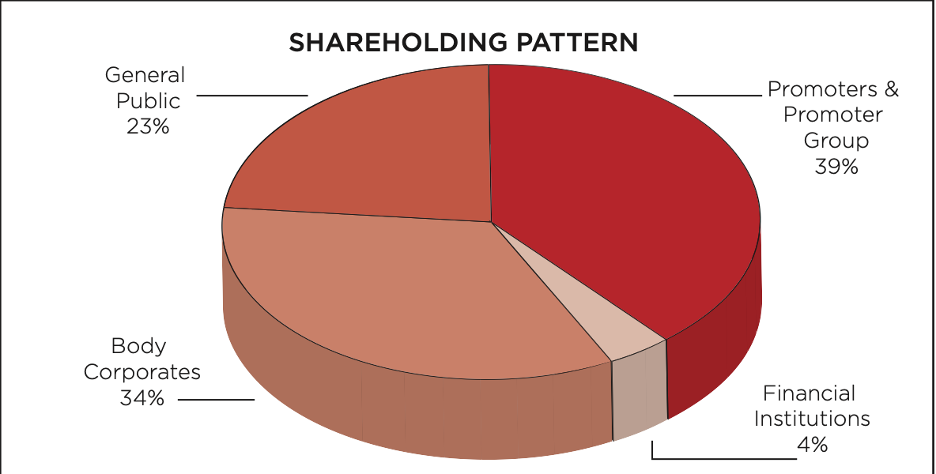

Promoter Holding

Image derived from Company’s Annual Report FY20-21

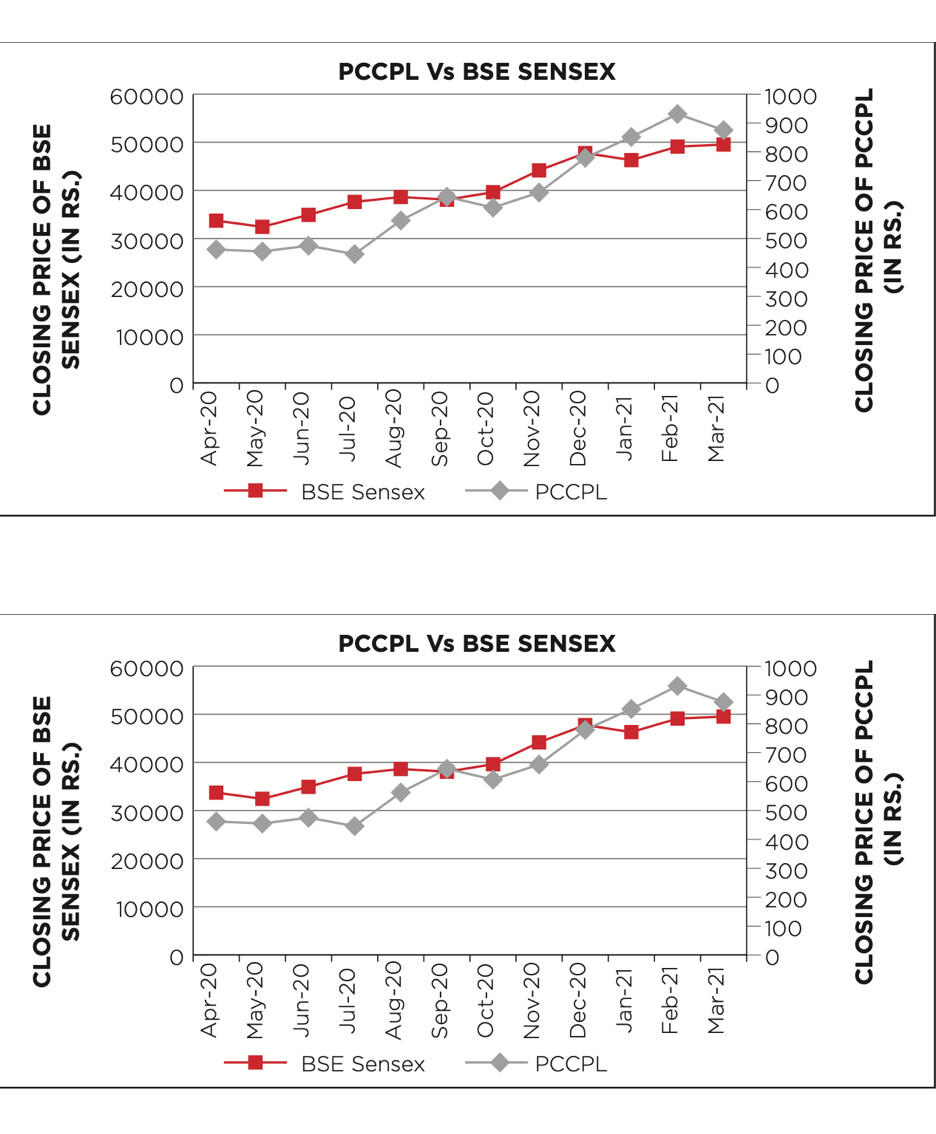

PCCPL VS Market Indices

Image derived from Company’s Annual Report FY20-21

Industrial Outlooks:

· Anticipated growth of the industry can be from $32 bn to $49 bn between 2021-2025 and grow at a CAGR of 6.3%.

· A big opportunity is created in the agrochemicals and speciality chemicals market because of the gaps in the supply chain that have been created because of the china plus one policy. This encourages the domestic producers to gain momentum in the production cycle and gain market share. This can be a big opportunity for a company like PCCPL which has a reputation for its contract manufacturing and its customer relationships. India imports 50% of the agrochemicals and keeping these will further boost low-cost manufacturing and will make India an important part of the supply chain.

· The export around agrochemicals in India is growing at a CAGR of 12% while domestic production is growing at a CAGR of 4%.

· India’s average per hectare consumption of agrochemicals is 1/10th of USA & UK and 1/20Th of Japan and China, this suggests that India’s demand for agrochemicals can still grow multifold and create robust demand for agrochemicals in the coming years. Food production is likely to increase in the coming years to cater the demands of the on a growing population. World food production is likely to increase by 70% by 2050.

· More than 100 agrochemical patents are getting expired by 2023. This will open up opportunities for CRAMS players and contract manufacturers and generic players including Punjab chemicals to manufacture new products for the excellent existing clientage as well as new players.

Key Growth and Profitability Drivers

The company aims to achieve a revenue of 1500 Cr within the next 3 years with the help of the following factors strengthening their objectives:

-

· Revenue Visibility: Punjab chemicals generated an order book of more than 1500 Crores for the FY21 with a stable EBITDA Margin of 12-14%. Improvement in the margins can be driven by better procurement, better efficiencies and cost savings and the company expects EBITDA margins to grow to 18-20% in the coming years.

-

· The management expects 2-3x growth in revenues from top customers which are UPL and ADAMA and which account for around 60% to revenues (35% and 25% respectively)

-

· Nippon Kayaku: The product that is being supplied to Nippon kayaku currently generates 10-12 Cr PA, with capacity utilisation of 80% for this particular product, The company believes that this product has the potential to generate 60-70 Cr to the revenue within12-18 months.

-

· Contracts with Singaporean MNC- The product that the company is manufacturing for the Singaporean company generates 12-15Crs to the revenue. The company aims to double that number in 2-3 years.

-

· The domestic formulation business is expected to grow 3-4 years, it currently contributes up to 50Cr to the top-line.

-

· Punjab chemicals is looking to increase revenues from its Industrial division because of the rise in demand for Phosphoric acid in pharmaceuticals as well as food and beverages. The company is already in talks with Coco cola to export phosphoric acid to their Korean and Singaporean factories. PCCPL already caters to the domestic needs of these companies and this segment adds around 50Cr to the topline. The management aims to double the segment revenue by next year.

Capex & Debt

· The company has planned a CAPEX of 150 Cr over the next 2-3 years and is planning to do a brownfield CAPEX at Lalru land where 6 acres are unutilized and available. The Asset turns from CAPEX of 150Cr will give out 3-4x returns and the total asset block will generate 200-300 Cr in the next 2-3 years.

- · Company is planning to expand its Pune facility by planning to acquire the adjoining plot, because of the rise in demand for industrial chemicals like phosphoric acid that the company is producing for MNC’s like Coca-Cola and Pepsi Co.

· The company has a debt of around 80Cr and have managed to reduce it by 13cr in the last year. The management aims to go debt free in 2 years.

Risks and Concerns & Key Monitorables

· Change in Government and Government policies: Government policies related to agriculture and any alterations in agro expenditure and incentives can directly affect the company’s order book.

· Adverse climate and weather conditions: weather conditions like rainfall and pests directly affects the revenues of the company.

· Exchange rate Fluctuations, Registration period, supply security and quality from domestic supply.

-

· Promoter holding is low and has decreased since the last year by 2.02% from 40.03% to 39.22%.

-

· Registration processes for new products and molecules take time for registration and formulation.

-

· 60% of the revenues are generated through the two MNC’s UPL (35%) and ADAMA which contributes 25% to the top line, having concentrated revenue generation can cause concern if any issues regarding these companies take place.

-

· Raw Material- Raw material contributes 60% of the expenses and vary time to time. Any changes in Raw material costing directly affects the topline as well as the bottom line of the company.

Company’s Plus points

· Excellent Clientage and Long-term contracts: Punjab Chemicals have excellent customer relations with excellent clientage which includes UPL, ADAMA, Corteva, Coco cola, Pepsi Co, Divi lab, Laurus labs, to name a few.

· PCCPL contract manufactures niche products for clients which include Nippon Soda, Nippon kayaku, Corteva, Syngeta, Bayer etc and also manufactures intermediates for Zydus, Cadila, Laurus labs, Divi labs etc.

Opportunity In The CRAMS Segment

Crams segment contributes 60% to the revenues by agrochemicals and its successful execution remains the key re-rating trigger for growth. The company has the advantage of being a go-to CRAMS player for both domestic and international companies by gaining market share as the industry expands. PCCPL is expected to use this as an opportunity to grow with the help of:

(a) concrete relationships with global agrochemical companies.

(b) expertise in the business led by an experienced management team

(c) integrating R&D team of both companies (PCCPL and the partner

company) to provide better products.

(d) renewed relationships with domestic formulators with a strong base in the domestic market;

(e) strong order book of INR15bn as of FY’21 (revenue visibility for the next 2-3 years).

The Company continues to focus on new and promising products either for CRAMS or for direct sales to improve its revenue and profitability. While they have been able to get new clients in the CRAMS business with lucrative long-term agreements signed with few MNC’s.

Capital Intensity:

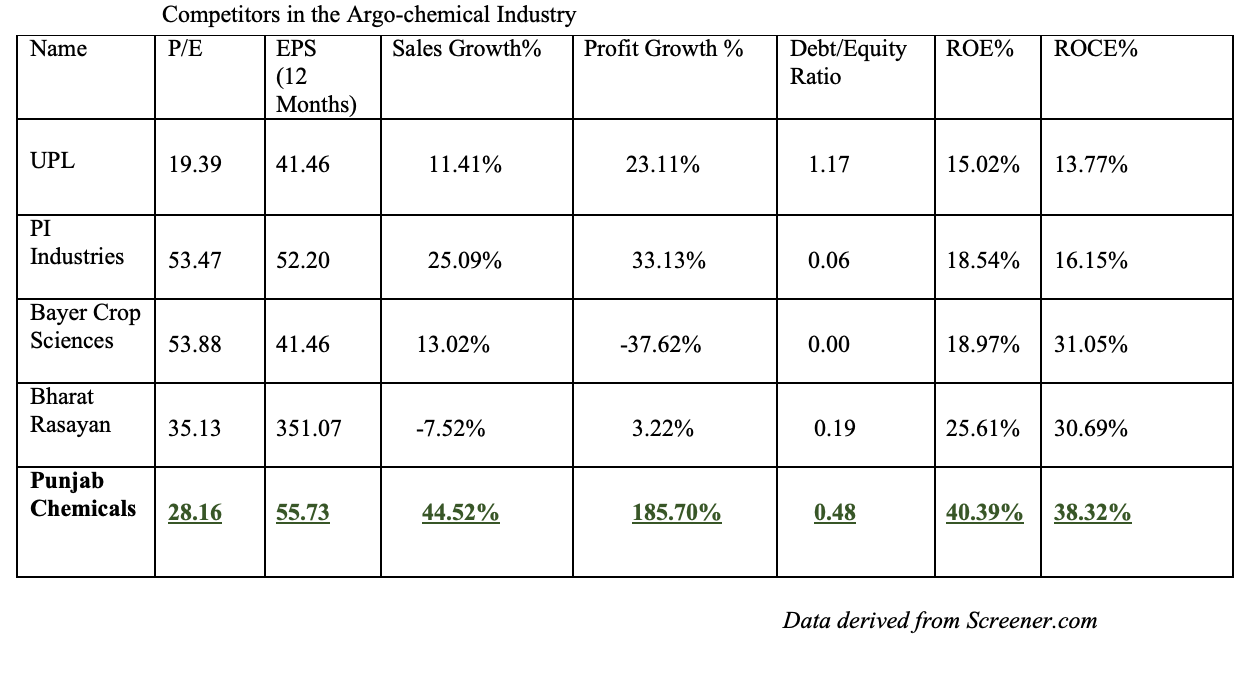

Company’s Competitors

Data derived from Screener.com

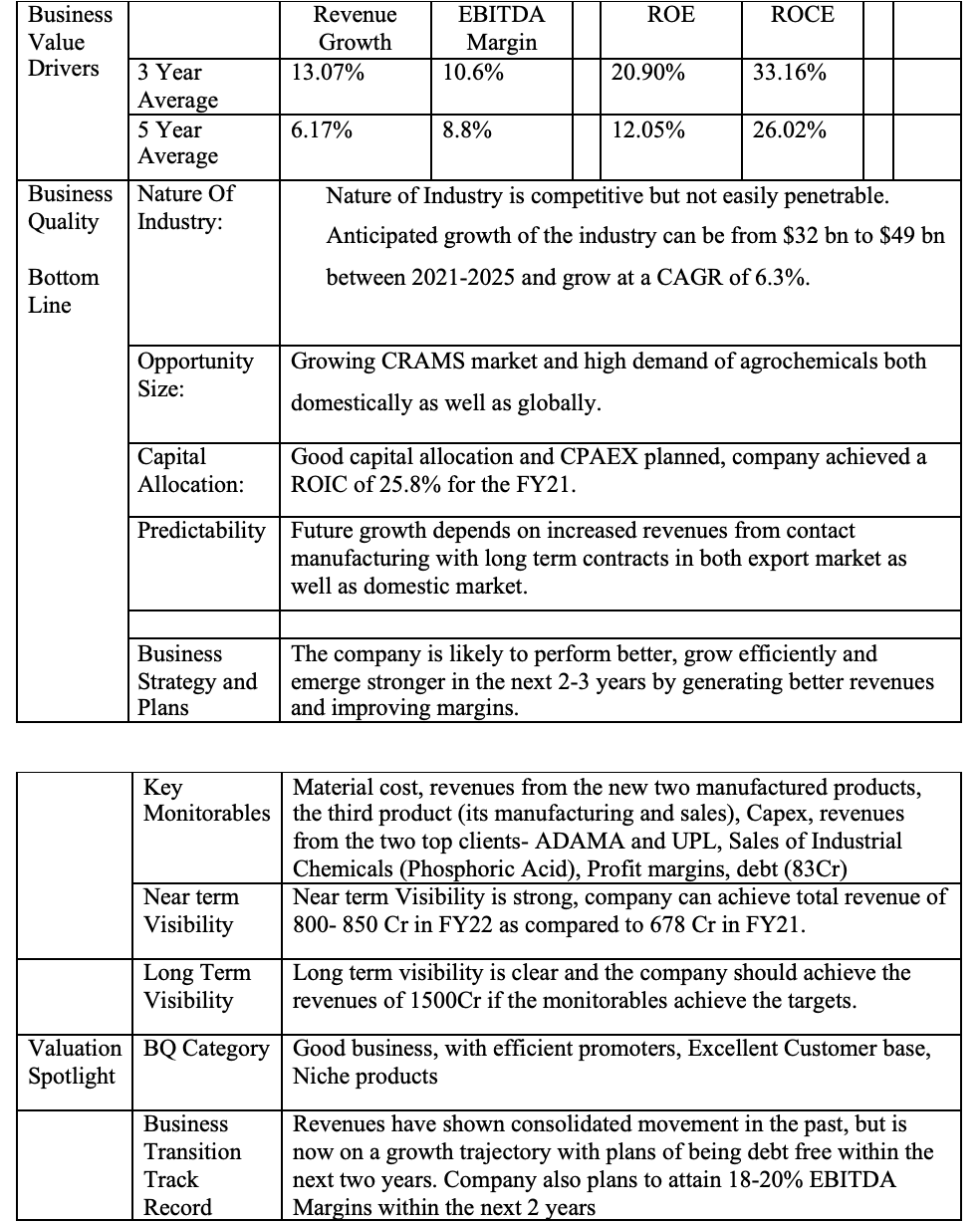

PCCPL Business Template

MY VIEWS

• The company can double its EPS from Rs 40 in FY21 to anywhere between Rs80-100 in FY22-23.

• The company can achieve a short-term target of achieving Rs 850-1000Cr Revenues in the FY22 and can double its PAT from 49.1 Cr to 100 Cr by the end of FY23.

• Punjab Chemicals and Crop protection limited is a great company with outstanding return ratios. I believe the company can achieve its revenue goal of Rs 1500Cr by FY23-24.

Disclosure-Invested

, infact seem likely to get an upgrade of Med term goals by mid FY 23.

, infact seem likely to get an upgrade of Med term goals by mid FY 23.