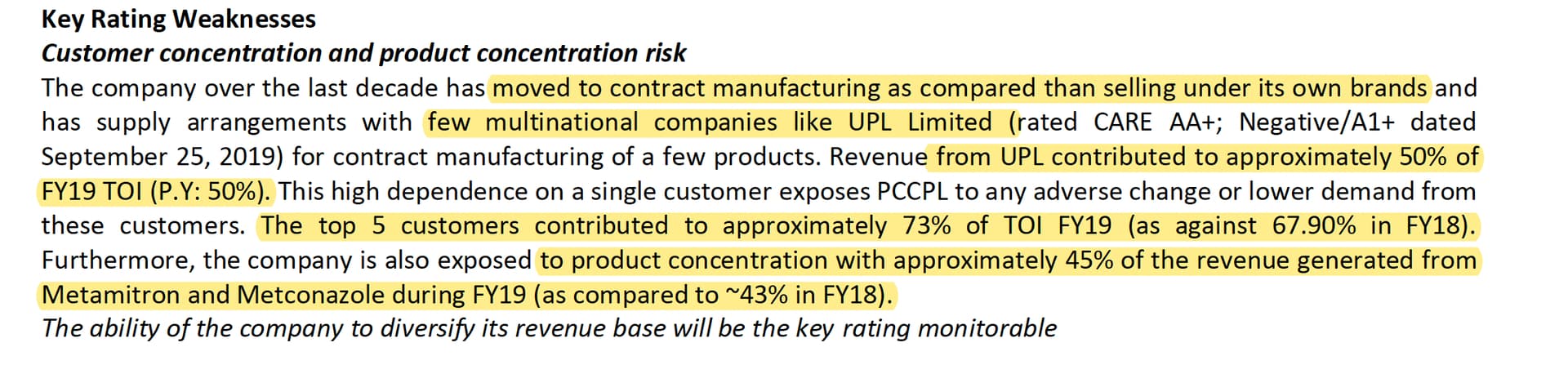

So far there are 2 key products which are driving close to 60%+ revenue for the company. Have spent some time understanding bit more about these two:

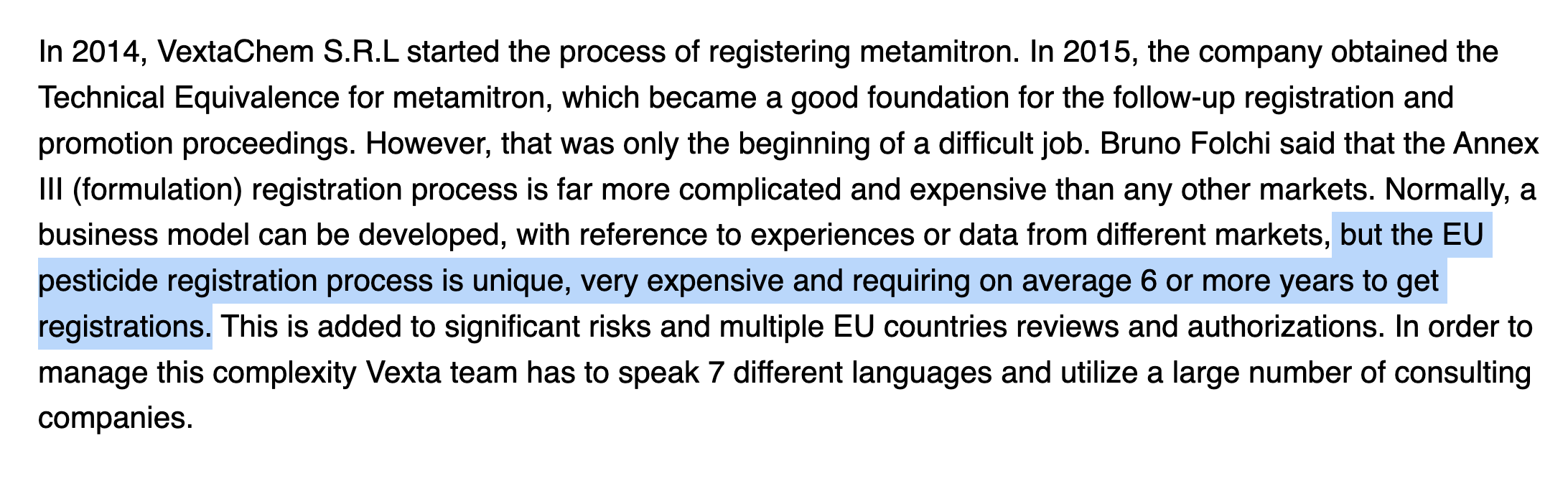

Metamitron:

- Triazinone Herbicide - Metamitron herbicide controls pre-emergent and post-emergent weeds. Key application in sugar and fodder beets.

- Developed by Byer Crop in 1975 and the patent has already expired.

- Global players are Bayer CropScience, ChemChina, Nufarm, SIPCAM-OXON Group, Ultra Group, Hutchinson Group, Shenda Chemical Industry, Nantong Reform Chemi

- As per one news feed, Its importance is increasing with the regulatory phase out of certain other competitor active substances ongoing in 2019 and 2020. (link)

- According to a report , global sales of metamitron in 2016 was $115 Million.

- UPL and Adama are significant players in European markets.

- In India, only Punjab Chemical has approval for Metamitron. Most importantly, it’s a 9(3) approval. - 9(3) approval is for first time indigenous manufacture of technical grade pesticide or formulation.

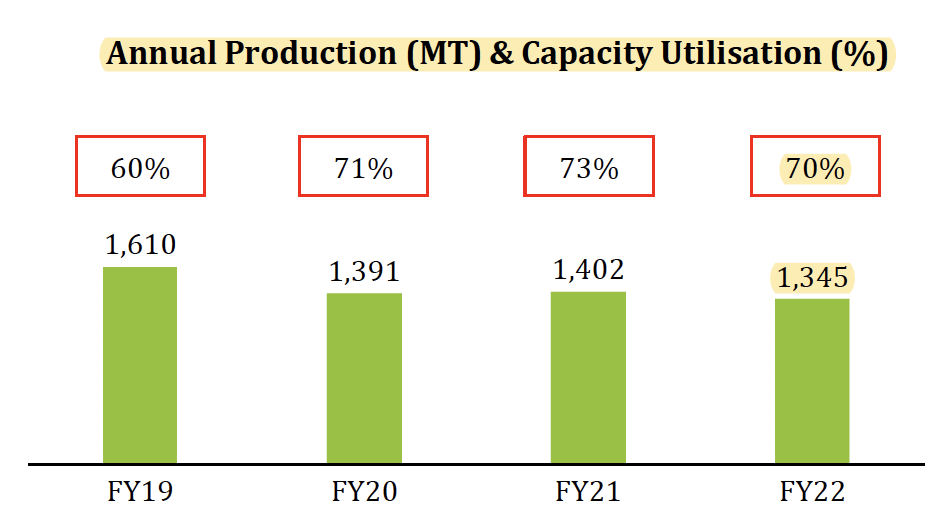

- Post capacity expansion, PCCL has capacity of 2700 (800 + 1900) MTPA.

- Interestingly, another player Himani Group has applied for Environment clearance (Link). Their proposed capacity is for 4800 MTPA. Close to 2x that of PCCL.

- Trivia - This Himani Industry had submitted a DRHP back in 2011. However, looks like the issue never came out. - Also, Best Crop has applied for a 9(4) (generic) application for Metamtiron in 2019. (link)

- As per Europian Pesticides Properties database, the dossier expiration date is 31/08/2022. What is the implication? (Link)

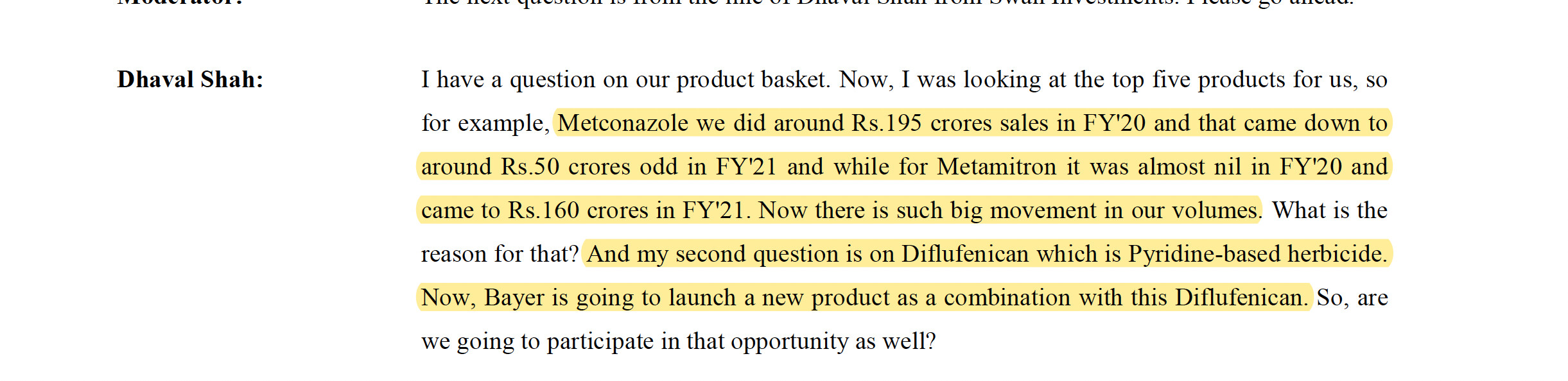

Metconazole (MCZ):

- Metconazole, was discovered by Kureha and initially co-developed with AgriShell (now BASF) to control a range of fungal infections cereals, canola, rice, maize, soybeans, sugar beet, cotton, stone fruit, nuts, peanuts, ornamentals, and turf.

- Kureha is a relatively small R&D-based company and has limited in-house marketing capabilities to cover all the major markets for metconazole and therefore entered into a number of collaborations with other companies. (Link).

- These collaboration has not only achieved wider geographical usage of metconazole but has also resulted in license companies developing mixture products and expanding metconazole’s use spectrum.

- In 2003 Rallis tied up with Kuhera for a 100% export oriented project on Metconazole.

- Rallis used to report Metconazole as one of the top three products till 2013.

- Even in the recent investor presentation and call etc, Rallis talks significantly about Metconazole supply to Kureha, just that the requirement may have changed and they are not required to explicitly call out top 3/5 products in AR.

- PCCL has current installed capacity of 240 MTPA for Metconazole.

- Meghamani has applied for Environment clearance for a capacity of 2400 MTPA. (link). 10X bigger capacity then what PCCL has today.

- Interestingly, Meghamani had applied for a 9(3) registration back in 2011 as well. They have gone through a lot in-between.

- Also, Astech has applied for Environment clearance (link) - proposed capacity is 240 MTPA (just what PCCL has today).

- Also, Anupam Rasayan has applied (Link) for environment clearance.

- Unlisted player Uma Organics also has applied for Metconazole capacity.

Some open questions/apprehensions that I have:

- Without any implied inference, they have very close working relationship with UPL - Infact a long standing one:

- Divesture of 4 subsidiaries to UPL in 2012-13 post the financial headwinds that PCCL was facing around that time. S D Agchem (Netherlands) I B.V., Agrichem B.V (Netherlands), N.V Agricultural Chemicals, Agrichem (Helvetia) GmbH.

- Biosar MIDC Plot lease right transfer in 2020.

- Customer funded (50%) capaex.

- Very remunerative supply of Metamitron piggybacking on UPL’s penetration in European market.

- Specifically on Metamitron, intrigued why this has been a monopoly situation for PCCP though the market size is decent enough and patent has already expired.

- Hemani with 2x capacity can be significant challenger in a level playing filed - if PCCLs proximity to UPL kept out of equation.

- On Metconazole, important to identify if the existing business shifted from Rallis to PCCL or PCCL was onboarded for incremental demand with an intent of supplier base diversification? Will be important to see Rallis historical capacity and growth thereon. Could be indicative if they have snatched business away from Rallis.

- Are we heading for a supply glut on Metconazole with Meghmani getting 10x capacity and other guys like Anupam and Astec getting in the fray?

- On the claim of 1500 Crs+ topline in next 2-3 years, current assets are close to 200 Crs. With proposed capex of 150 Crs. it will take ~4x to 5x asset turn for a top line of 1500 Crs. I think this point was discussed in Q2 concall as well. The explanation is not very convincing so far.

- On the claim of being significantly into CRAMS business, in context of the R&D capability etc. my impression is to look at this more as a contract manufacture. They claim to have 0.3% as R&D expenditure and have close to 55 people into R&D function. That gives a range of ~3 lac per employee/year as R&D personal salary.

- Overall Debtor days has impoved a lot and looks far better as compared to industry peers.

Thanks,

Tarun

Disc: No Investment