PART 1: ASSET ALLOCATION

20% Debt

80% Equity

0% Gold / silver / commodities

0% Real esate.

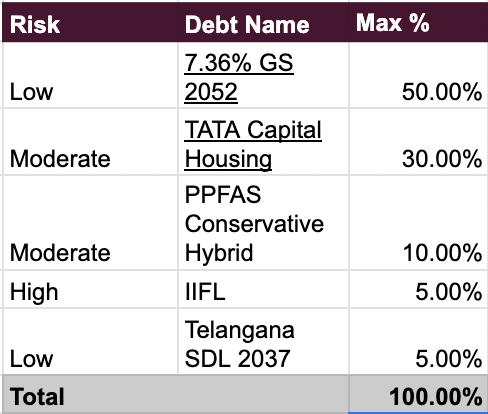

Part 2: Debt Allocation

- Given the prices at which I bought, I would be generating ~7.8% (pre-tax) yearly interest.

- I do have concerns over liquidity in debt instruments. The trading volumes are very low and my current strategy of buying NCDs directly is sustainable. Actively looking for suggestions here.

Part 3: Equity Allocation

My equity allocation is based upon the following points:

-

Following a framework of 1 - 25 - 5. This means that if a business is:

MicroCap → 1% Allocation of equity portfolio

SmallCap → 2.5% Allocation

MidCap/LargeCap → 5% Allocation

This removes personal biases and limits the number of companies I can choose from. -

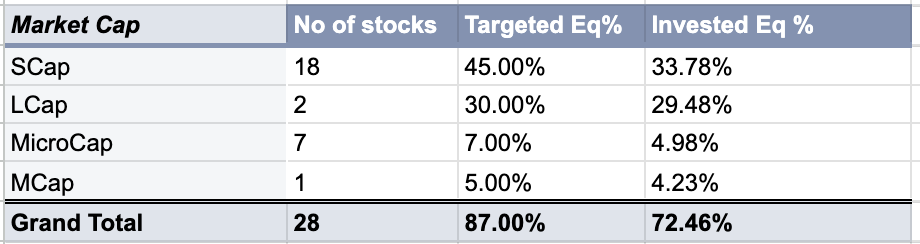

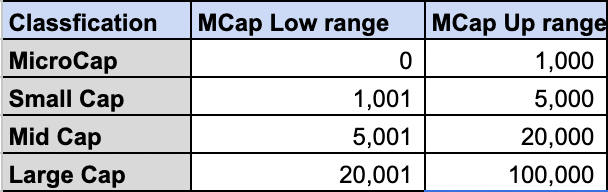

My classification of Micro v/s Small v/s Mid vs Large Caps

The reason I have put an upper range on LCaps is that I tend to avoid companies beyond a certain Market Cap. It’s better to just buy an index rather than buying a stock that is getting tracked by every analyst 24 x 7. -

Life is a mess and I have very limited time. Can keep a track of limited companies only (~20 to ~25)

-

Everyone is smart in hindsight. I’m going to make mistakes today only to realize tomorrow - what if I have no capital to come back into the markets?

-

No matter how many concalls / forums I track, I will likely be very late to learn about anything. ex: know some analysts who keep track of import/export data at a weekly level - can’t compete with them by just tracking quarterly concalls.

Also, makes me question myself if analyst actually can significantly higher return than me as a retail investor? -

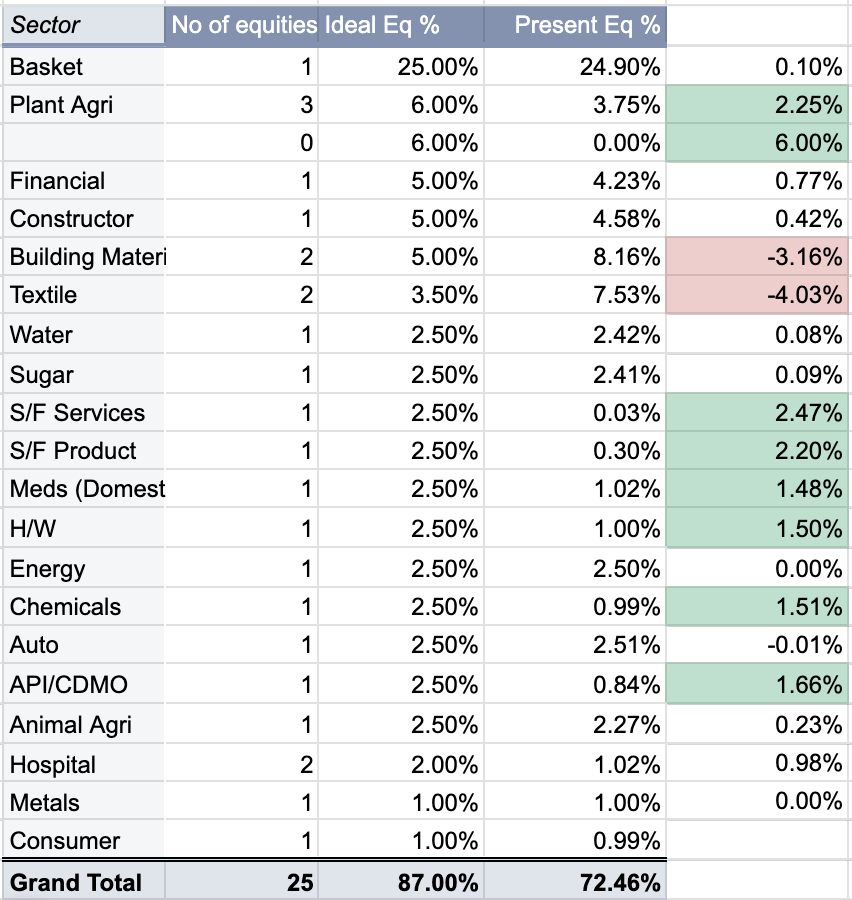

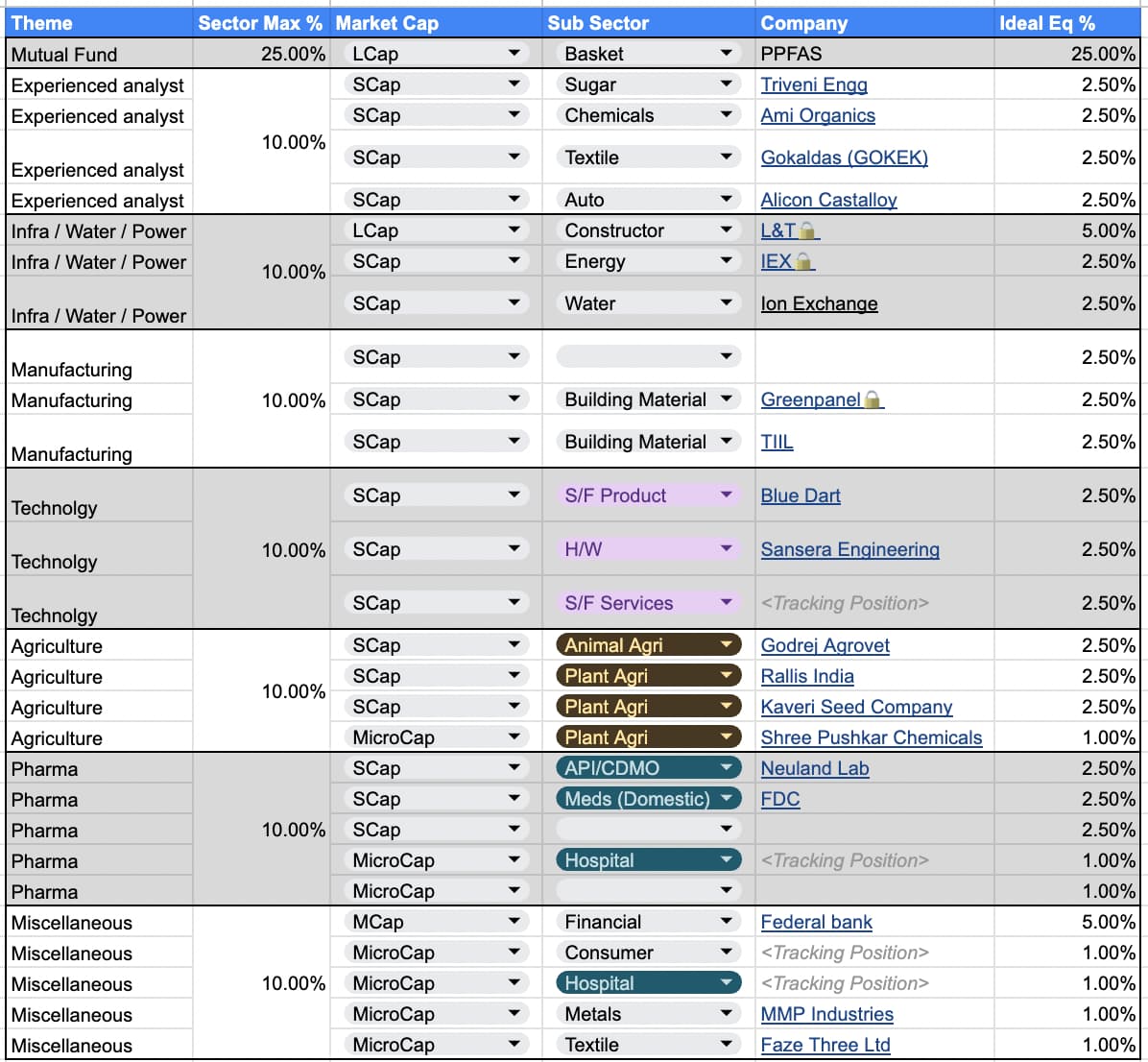

Past mistakes taught me that I was unintentionally bringing biases while investing. Now, I have been following a strict rule of not going beyond 10% in every theme/sector.

| Theme | % of Equity Portfolio | Rationale / Notes |

|---|---|---|

| Mutual Fund | 25% | Point 4 |

| Experienced analyst | 10% | Point 5 |

| Infra / Water / Power | 10% | - |

| Manufacturing | 10% | - |

| Technolgy | 10% | - |

| Agriculture | 10% | - |

| Pharma | 10% | - |

| Miscellaneous | 10% | - |

| Cash | 5% | - |

| Total | 100% | - |

8. Targets for this year:

- To move more and more towards passive investing / GTT based investing

- Reduce companies under 25 by year end. Do not have more than 4 companies in a theme.

- Increase allocation in IT and reduce allocation in API/CDMO.

Every investor and every company is doing capex in CDMO… There can be only one thing in future - enormous supply leading to possible pricing pressure