Added Shyam Metalliks while exiting Sparc/Vindya/RACL/FDC/Kovai

No of holdings now stand at 22 (including MF)

Avg MarketCap to Sales (for direct equity): 2.8

Net uptick: 25.81%

During the month some equities/bonds were getting sold at very low prices so I took entries with a short-term POV. However, have exited them now with some profit (ex: GS2052, AllCargo etc)

ALLOCATION

MCap/Sales

Names

Invested %

Net Returns

FPD > 1

PPFAS🔒

20.33%

20.60%

Yes

0.98

Godrej Agrovet🔒

8.68%

6.36%

1.51

Triveni Engg

6.95%

38.06%

0.70

BCL Industries

5.76%

11.29%

1.46

Exide Industries

5.25%

1.23%

2.25

Sansera Engineering🔒

5.02%

22.65%

7.23

Ami Organics

4.78%

8.18%

2.15

Gokaldas (GOKEK)

4.57%

103.58%

2.72

Greenpanel🔒

4.49%

4.30%

Yes

3.12

Max India Ltd🔒

4.34%

18.41%

3.00

Lupin

3.80%

33.80%

12.20

M.K.Ventures🔒

3.51%

5.82%

0.72

TATA Motors - DVR

3.46%

7.00%

5.19

Borosil Renewables

3.38%

-11.75%

2.18

L&T

3.25%

148.56%

Yes

2.89

Shyam Metallics

2.77%

0.08%

2.31

TIIL🔒

2.75%

59.94%

3.69

Ion Exchange

2.56%

73.04%

Yes

0.63

Cosmo First🔒

1.80%

2.83%

1.14

MMP Industries

1.18%

78.79%

5.36

Niyogin Fintech

1.01%

-11.38%

2.07

Banka Bioloo

0.37%

4.43%

FPD>1: First purchase date was 365 days ago. May have added more / sold some at a later time

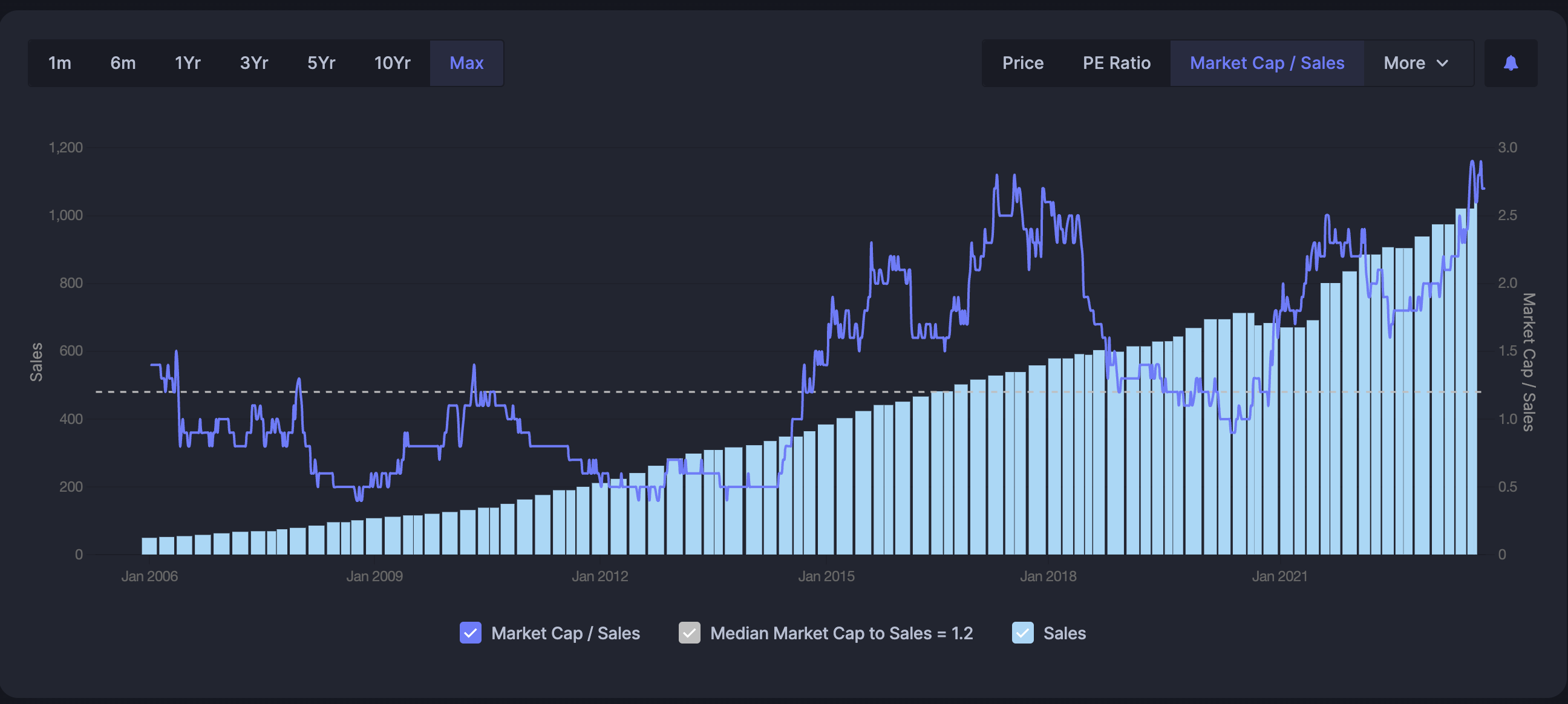

SHYAM METALICS: Needs a detailed post - will write later. (over the weekend hopefully)

RACL Geartech

Exited somewhere between 60% to 80% uptick (it was insignificant so didn’t care to remember). Bet size was getting insignificant with time (not comfortable adding at this valuation). Secondly, at 4 times Market Cap to Sales, chances of valuation re-rating were low (for comparison, Sansera is 2.2 times).

FDC (< 1year)

Exited at around 15% percent uptick. The re-rating could have limited upside from here onwards.

Vindhya Telelinks / Sparc Electrex

Bought them to study since they looked interesting - but - too many unknowns and unable to put the needed time.

Kovai Medical

Very consistently growing business but if I had to pay these valuations, why not target faster-growing companies? I still like this so maybe I’ll review at lower valuations.

Hi @ChotuKatappa Thanks for sharing your portfolio and the rationale behind the stocks. Did you get a chance to write about Shyam Metalics? I know its a recently listed company and i went through screener to check some of the basic things.

Found that profits and OPM% has got huge variations in last 3 years. What made you interested in the company?

I dont intend to criticize but this approach seems to be more academic and more suited to a storied Uniiversity Professor who wants to convince his students he has theory with all postulates and assumptions adding up…

I prefer a little more free flowing with focus on understanding the business and understandin g management better( they have bigger stake in the Business after all) and som etimes try to understand if there is a big trigger ( positive or negative ) which will impact the business. Believe me , this can be very cerebral and does not align itself to rules or framework.

About large caps it is a misconception that large caps dont give good returns , their returns are linked to risk in the business and cyclicality in business, These companies do benefit from the big economic trends affecting the country and these companies dont face existential challenge when economy slows down. So you take your pick …

The business is quite cyclical and the margins are unlikely to be consistent. My understanding is that this cyclicality should reduce over the next few years. I haven’t been able to find time to document the thesis - broadly it revolves around the following points:

Expectations

Capex: The company has been investing in massive capex / backward integration. I like how most of this comes through the cash generated/non-debt. Here’s what happened in FY22

This ppt would give a better idea of where’s this capex is going. Is the management skilled enough to use this capacity? If things turn out as per my expectations, it could drive higher profitability.

I also find it interesting how the company has been trying to diversify different segments such as aluminum foils (~EV battery) - I believe they have a collaboration with Achenbach - but that’s a different story. [Source]

Debt: High debt is something that always has made me avoid steel companies. However, Shyam doesn’t have much debt at present. Management doesn’t look like they’ll go crazy over here which makes me interested.

Looking at the team, one might feel good about corporate governance. I have mixed opinions. However, the management broadly has been consistent with their words so I got intrigued. Here's what the management claims/expects:

There are things I do not like about this investment:

Investing in companies where timing is crucial, isn’t something that I prefer. I do not think i’ll hold this stock for the long term. Management commentary proved my understanding here. Let’s see how the plan goes.

I still haven’t completely analyzed through their pre-IPO journey which is a serious risk on this investment.

A lot of unanticipated things can go wrong in such business

This is all I could write due to time constraints. In my opinion, before analyzing this business, one may want to look at GPIL.

I hope I was able to give you a direction.

Disclaimer: Invested and biased. Not a buy/sell recommendation. I am often wrong and change my views. Further, I may buy/sell stocks without informing anyone.

Hi @Malolan_R, I am quite open to criticism so feel free to add.

Can you please elaborate on your understanding of my approach?

“good” here is relative so I will not comment on it. But, I do not think I have ever said that large caps do not give returns. I try to avoid stocks that are being chased/covered by every analyst as the chances of valuation re-rating are often low. This is higher for large caps as compared to small/mid caps.

Secondly, large caps are all about providing stability to the portfolio by protecting the downside.

My thought has always been - “If I have to protect the downside, I would rather hold it through a fund that doesn’t have large drawdowns while beating the large-cap index”

Once in a while, a large cap may offer good risk-to-reward, at which time, I do evaluate the opportunity.

Ex: Invested in TATA motors / L&T

What happen to your VA Wabag holding? You sais, you added it, as it was a better option for you, considering the risk vs rewards.

Then suddenly it was gone from your portfolio w/o mentioning anything about the exist. What made you to exist this stock? I think its still a good opportunity and it is one of my highest allocation.

Would like to know your view if you don’t mind.

Thanks much.

Valuation seemed quite favorable. Further, the probability of a significant downside was on the lower side (not zero though).

Why I don't like Wabag

I do not see it as a long-term stock and wouldn't like to hold it during a down cycle. Here's why:

There are usually 2 reasons for undervaluation when a stock is undervalued (there can be other reasons too but for the sake of this discussion I’ll focus on the following):

Concerns at an industry/sector level: everyone performs poor

Concerns about a particular stock: a specific company performs poorly while peers are doing okay

If it’s the first one, often management can’t be singled out.

If it’s the second reason then I like to be cautious. In the case of Wabag, I have concerns about the management’s decision-making and vision during the last down cycle. I think the comparison below expresses what I mean:

I was getting into Wabag with a rationale to exit in 2-3 years. Midway, I realized that I’ll not be able to exit in time due to personal commitments. So, I decided to stick with Ion Ex.

My complete set of actions was: Bought Wabag → Sold Wabag → Add Ion Ex. (Last addition on 09/08/23) .

Disclaimer: I am not a SEBI registered advisor or analyst. This is my personal view and not a recommendation. I am often wrong and do change my views without being able to inform anyone.

I like your way of seing companies. Could you elaborate what concerns you had about management decisions like which decisions etc and also which lack of vision?

Yes … I am ex L & T so I may be biased . Its only after 10 plus years market is realizing the worth of L & T …

About large caps many large caps benefit from the growing economy … we need to compare with equivalent listed companies in same industry in developed markets …

Whats the thesis behind 5% in Greenpanel. MDF usage is struggling in India . and companies need to deal with lower priced imports from Middle East or East or SE Asia ??

Even current valuation dosent reflect this downside

Difficult to answer since there is no direct statement that I can quote but let me try.

Before covid, they had a goal of 1 billion euro. From being the top player in water purification to changing its EPC business model, management has set multiple targets in the past. I do not see them achieving most of them. When I go back to the 2016 - 2020 period and compare peers, I see much better ambitions/actions. For example: Thermax diversified their business during the period while Wabag was sleeping.

Money is made for an investor when either the company becomes the leader in one industry OR, the company expands in different industries until it becomes a leader in one. I do not see Wabag doing any of this in the near future (mid-term).

In other words, having a big dream, working on it, and finally achieving it are three different things. I do not see Wabag doing enough for the first two itself.

Okay firstly, I have sold Greenpanel after the last update - HERE. I needed cash and I sacrificed Greenpanel because I don’t see their earnings growing significantly in the next few months. If I have cash in the future & valuation is good, I’ll review the space for entry.

Now coming to your question.

What you’re saying are short-term challenges (which usually happen in every sector). I would be happy if these hiccups get so intense that it eliminates some competition. My views about the long-term trends of MDF are positive and I like GP’s management much more than peers. Certainly, the valuation is not cheap but I do not think it’s crazy enough to make me sell (which is ironic because i sold - but my reason was something else which I explained earlier).

Hi Sir, Any specific reasons sell off Max India (other than you have bought at lower price)? I’m keeping a tab on Max Ind for last few months, but waiting for some corrections to have in long term basket.

I bought it at a lower price but added it at a higher price. At the time of exit, I was around 20% up in total.

I don’t have anything against Max India. The business has a lot of potential and I continue to like it.

I sold it because there are a few other businesses that seem attractive and I would like to invest there so I needed cash. I am not expecting Max’s earnings to shoot up in the short term and felt comfortable to exit.

Not to forget that the business hasn’t been generating profits but the valuation is 3/4 times market cap to sales. Should a business that is unlikely to grow 20/25% consistently for the next 2-3 years be valued so high? Imo, it shouldn’t sustain unless growth kicks in

I started buying ~120-130 in smaller chunks. But suddenly went upto ~220, so not adding now. I’ll wait for this to correct for fresh buy. This is my long term micro cap bet, no path to profitability atleast for next 3-4 years until all capex is done. All my other investments are in stable ones, so ok to take this bet. I dont have good stock picking skills , so doing direct investments either during heavy correction or fmcg/companies having business that any layman can understand.