Using this post to document my thesis for holding TaMO - DVR

(Other people have already written quality quantitative posts under this thread (eg: this one by @GourabPaul) - by repeating information I will pollute the thread and not add any value. Instead, I’ll write something that is not talked about a lot on this thread)

My reason: Value (even in this market).

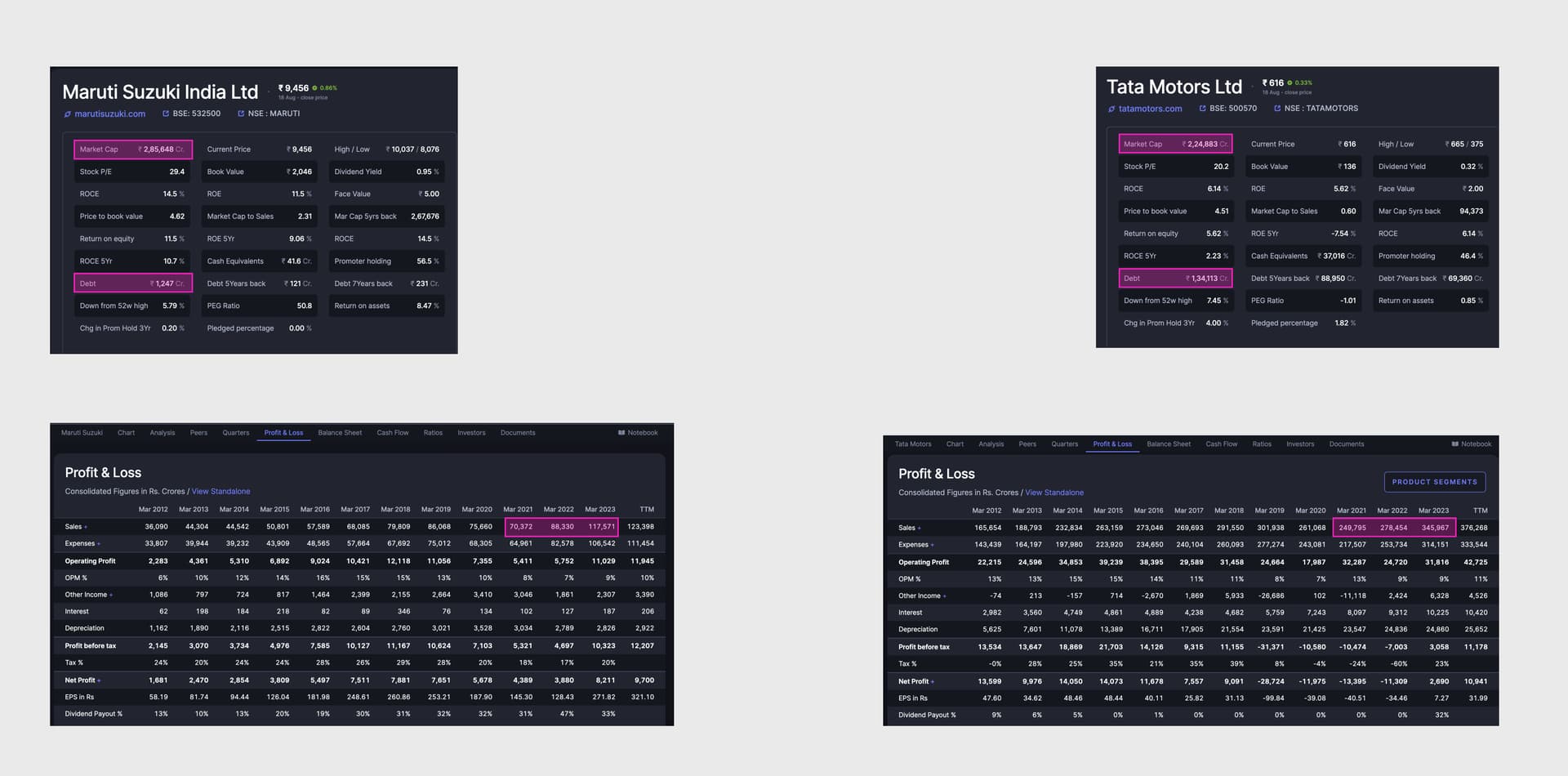

a) TaMo does more than 2x sales as Maruti but has a lower Market cap (+20k for DVR). It does more sales every year than it’s Mcap.

b) Imo, if the debt were to go off, the real numbers would surprise everyone. Can the debt go off? I believe they are doing the right things and the trajectory is in the right direction (again, not going to repeat quantitative information since there is enough of it in this thread).

Risks:

1. Hydrogen-powered v/s EVs: If somehow Hydrogen vehicle scales up, I believe that government would prefer/push Hydrogen over EVs (especially how China’s dominance in the EV value chain is). I am unsure how long can I hold TaMo <I’ll use this space to expand more as I find hard evidences (or) frame my mind>

2. Is another pricing war coming?: There are new manufacturers coming up (and most likely more will come up for EVs) which could eventually cause a margin erosion. Be it pricing wars in telecom or making the world’s cheapest car, the group’s history of failing at “good ideas” is not unknown. So once again, I have doubts about how long I will hold TaMo.