About

40+ years old manufacturing company that makes precision engineering components for automobile and non-auto industries.

In automobiles: Serves almost all major OEMs

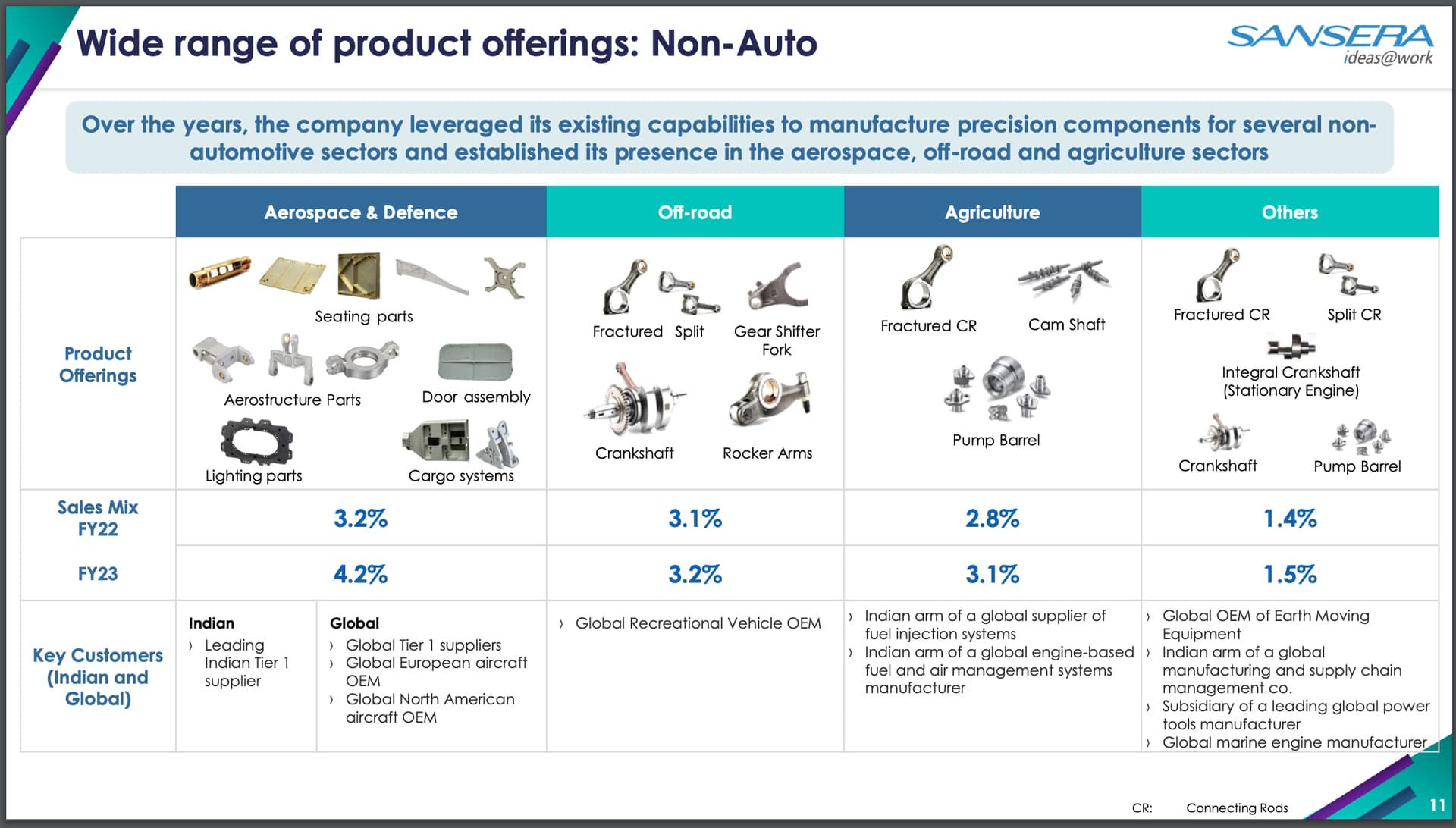

In non-auto: Serves defense and aerospace industry - working on entering electronic sub-systems

Promotor: Mr. Sekhar Vasan - IIT / IIM Alumni (read here)

CEO: Mr. B. R. Preetham (has always been here - LinkedIn)

What’s interesting about Sansera

-

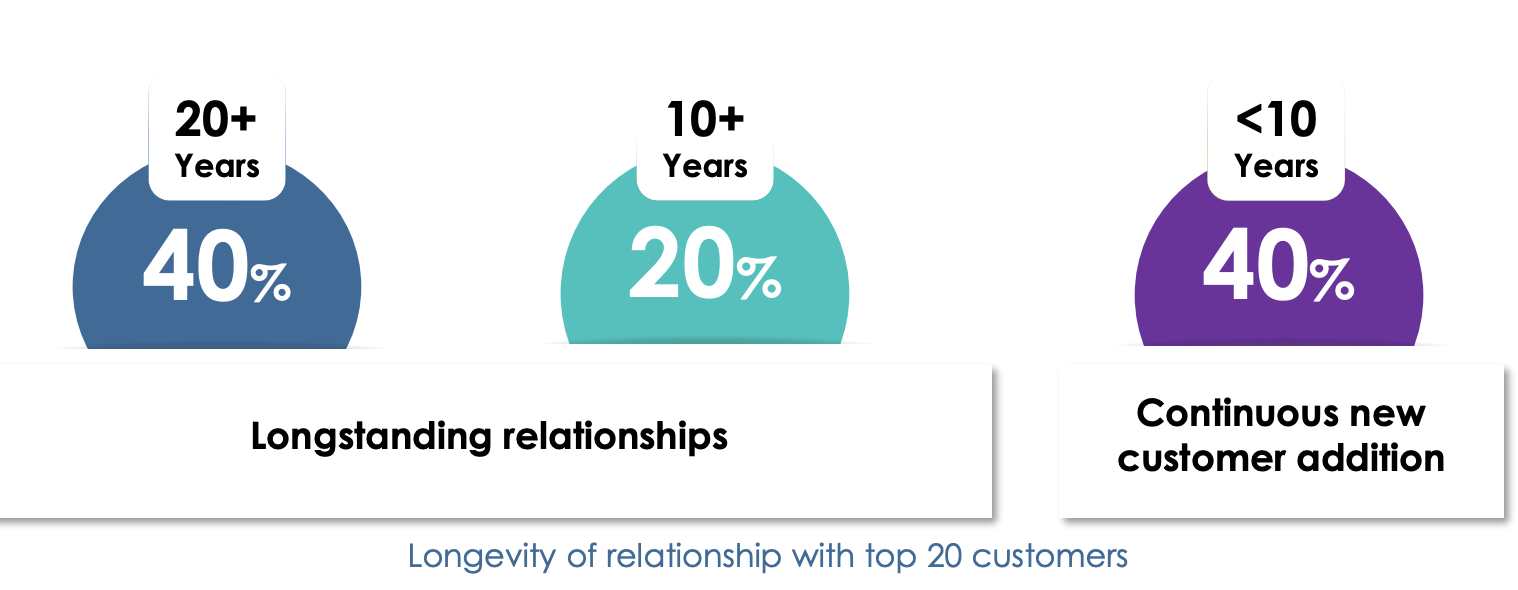

Stickiness of customers: They have been working with almost all major OEMs. Interestingly these relationships last quite long.

a) In 2W segment: Over 18 years of relationships with leading 2W players such as Bajaj Auto Limited, Honda Motorcycle, and Yamaha Motor India.

b) With Maruti Suzuki India Limited for 30+ years, and with Fiat Chrysler Automobiles for 10+ years

-

Largest domestic supplier of connecting rods: Has a market share of 2% to 3% for connecting rods for light vehicles (PVs dominantly) and CVs globally.

-

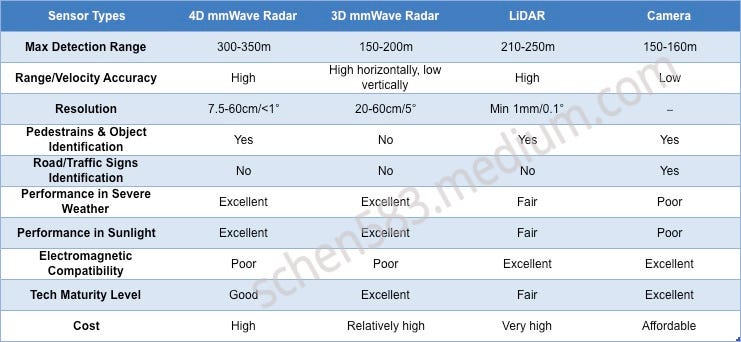

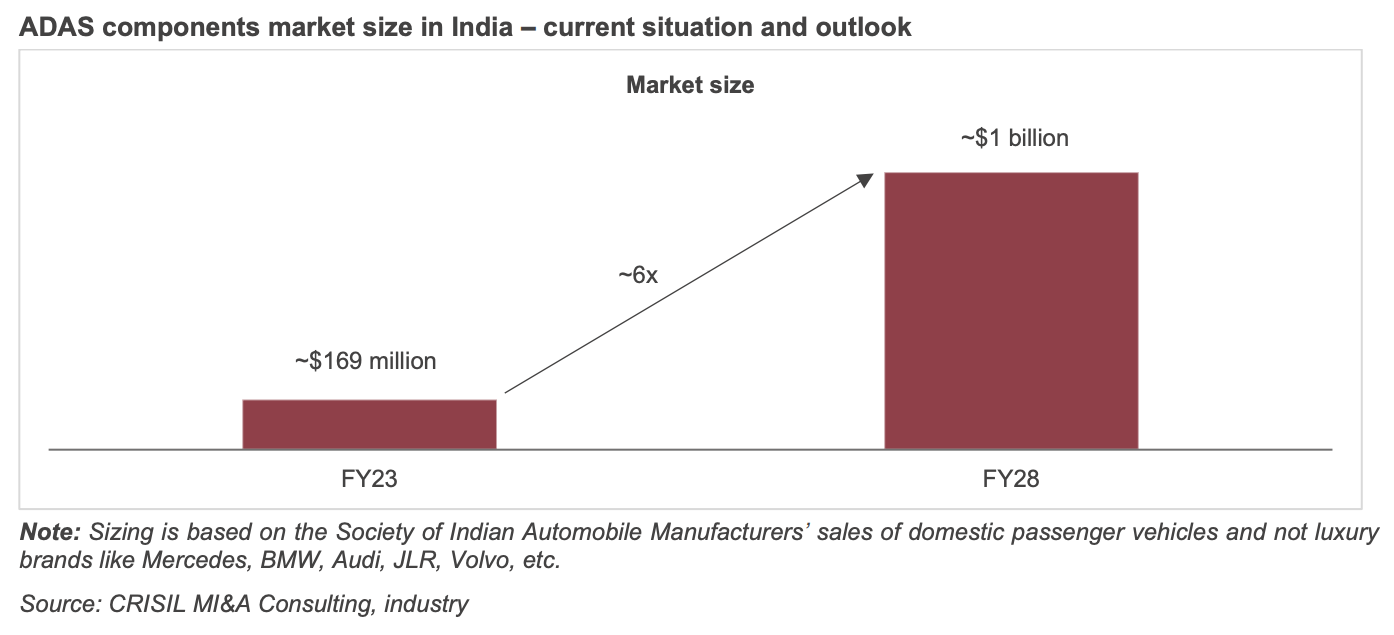

Strategic Investments and Capex: Company has been doing significant capex. Also, exploring opportunities in electronic systems and autonomous driving sub-systems.

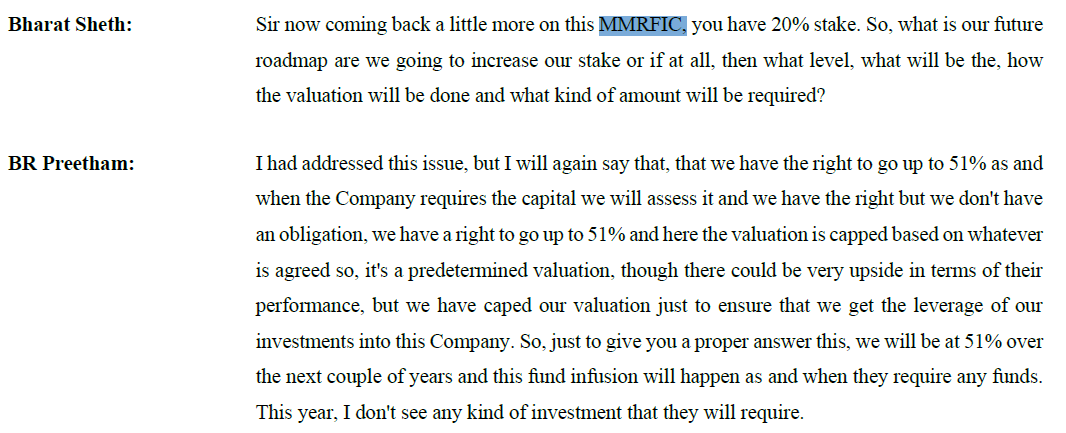

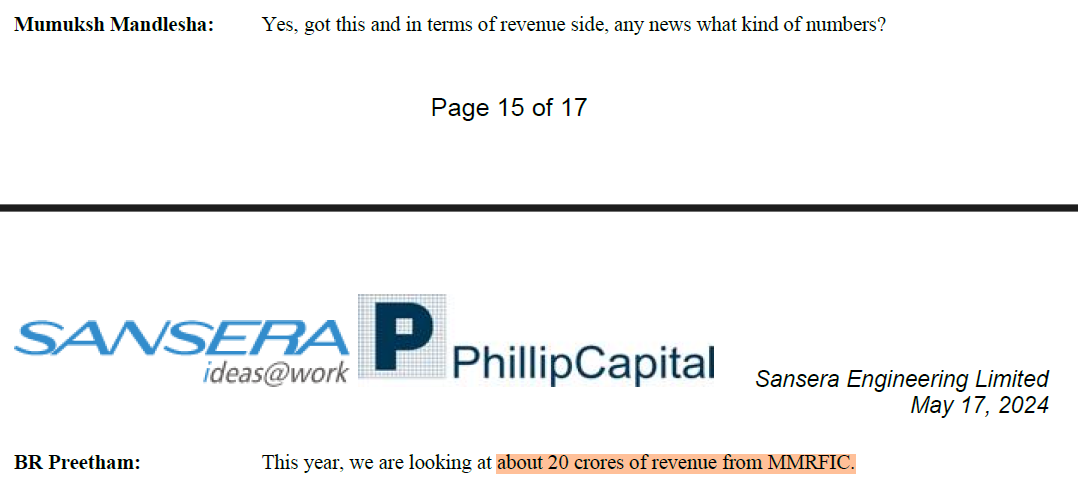

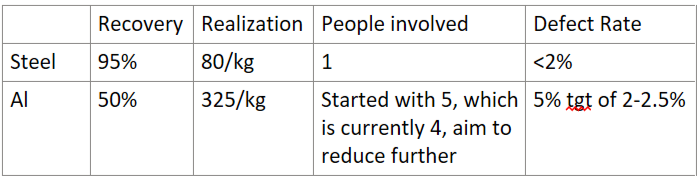

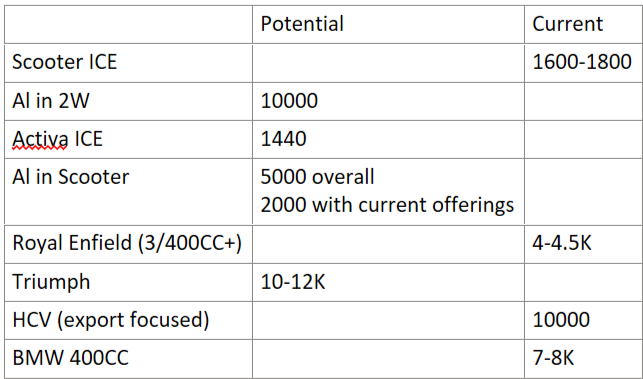

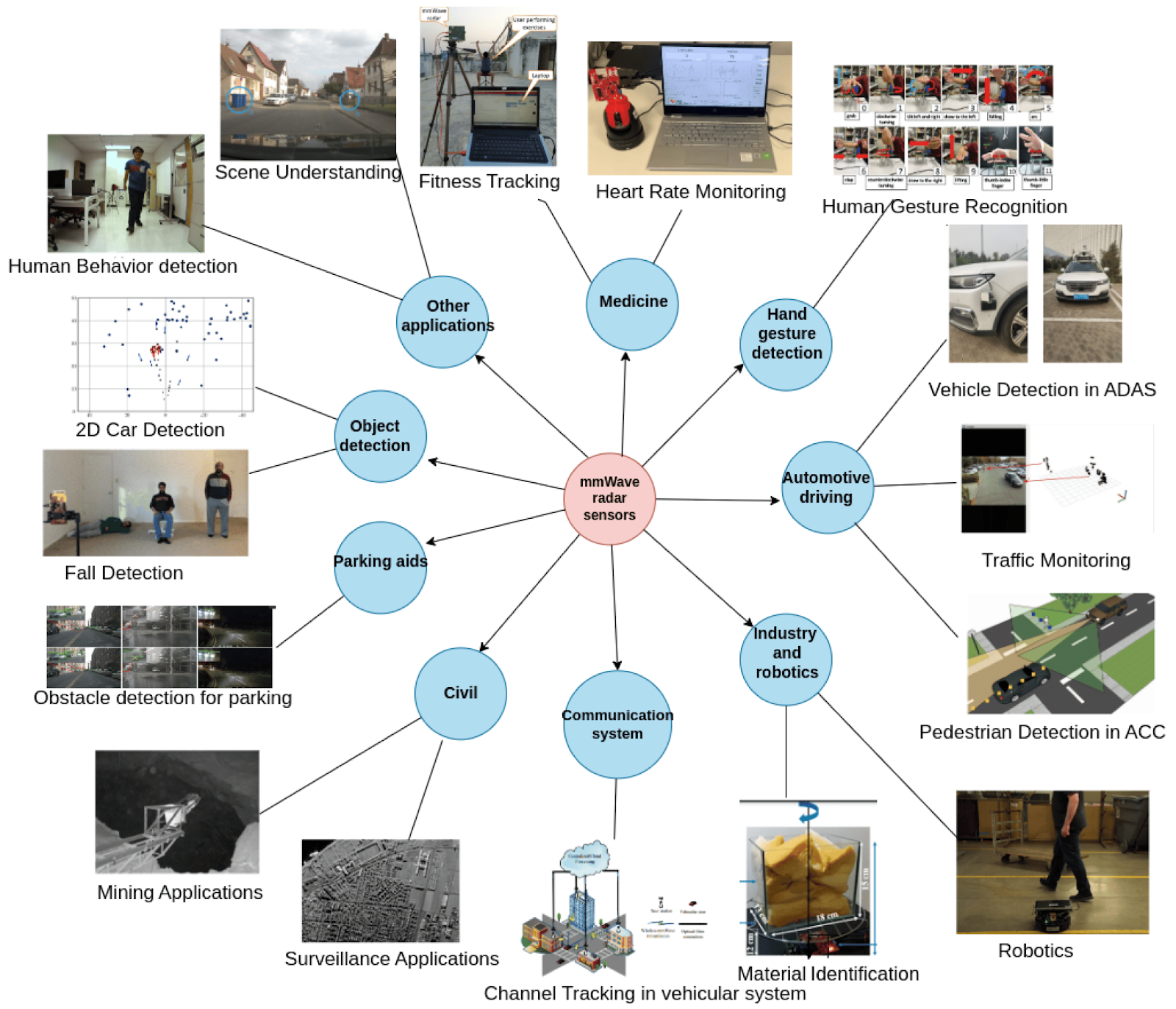

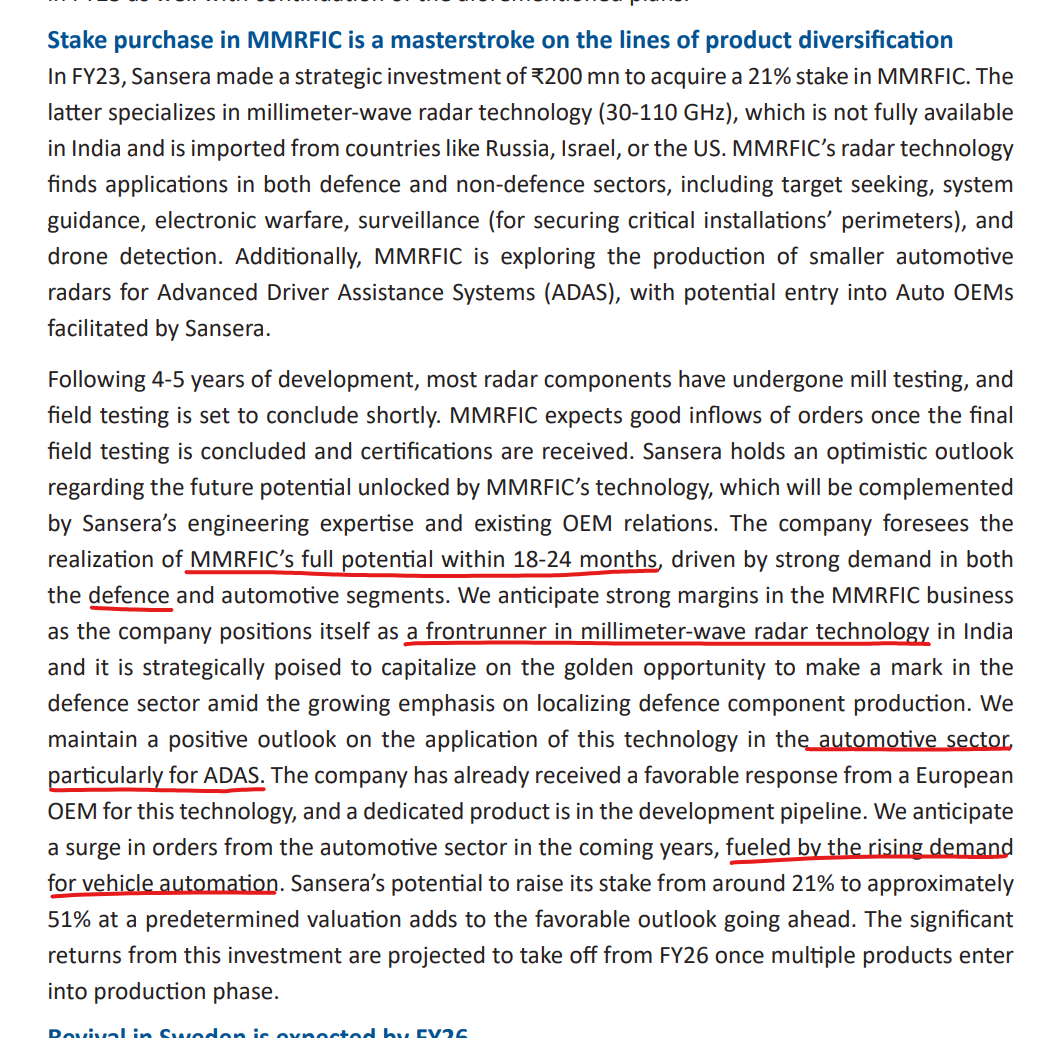

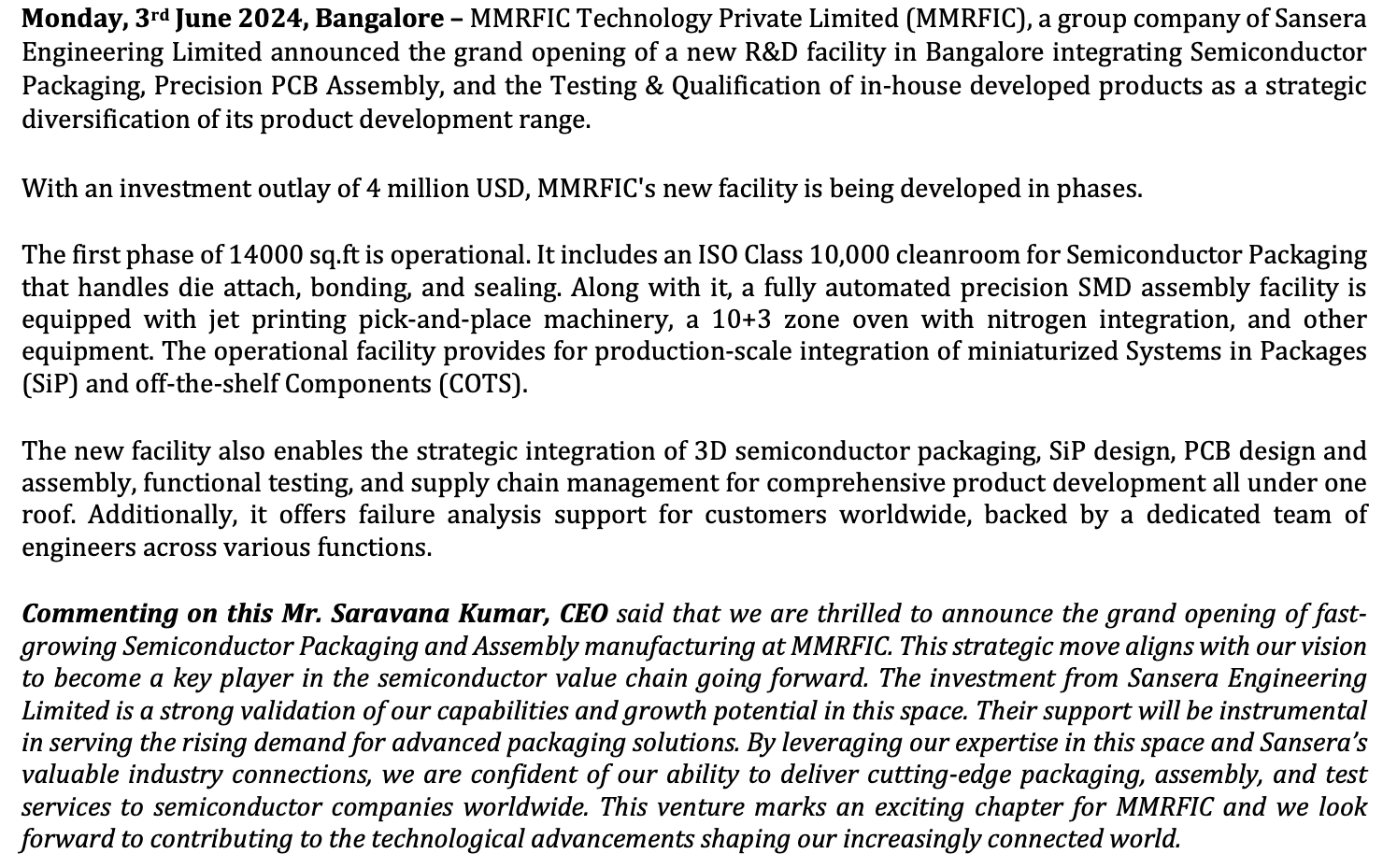

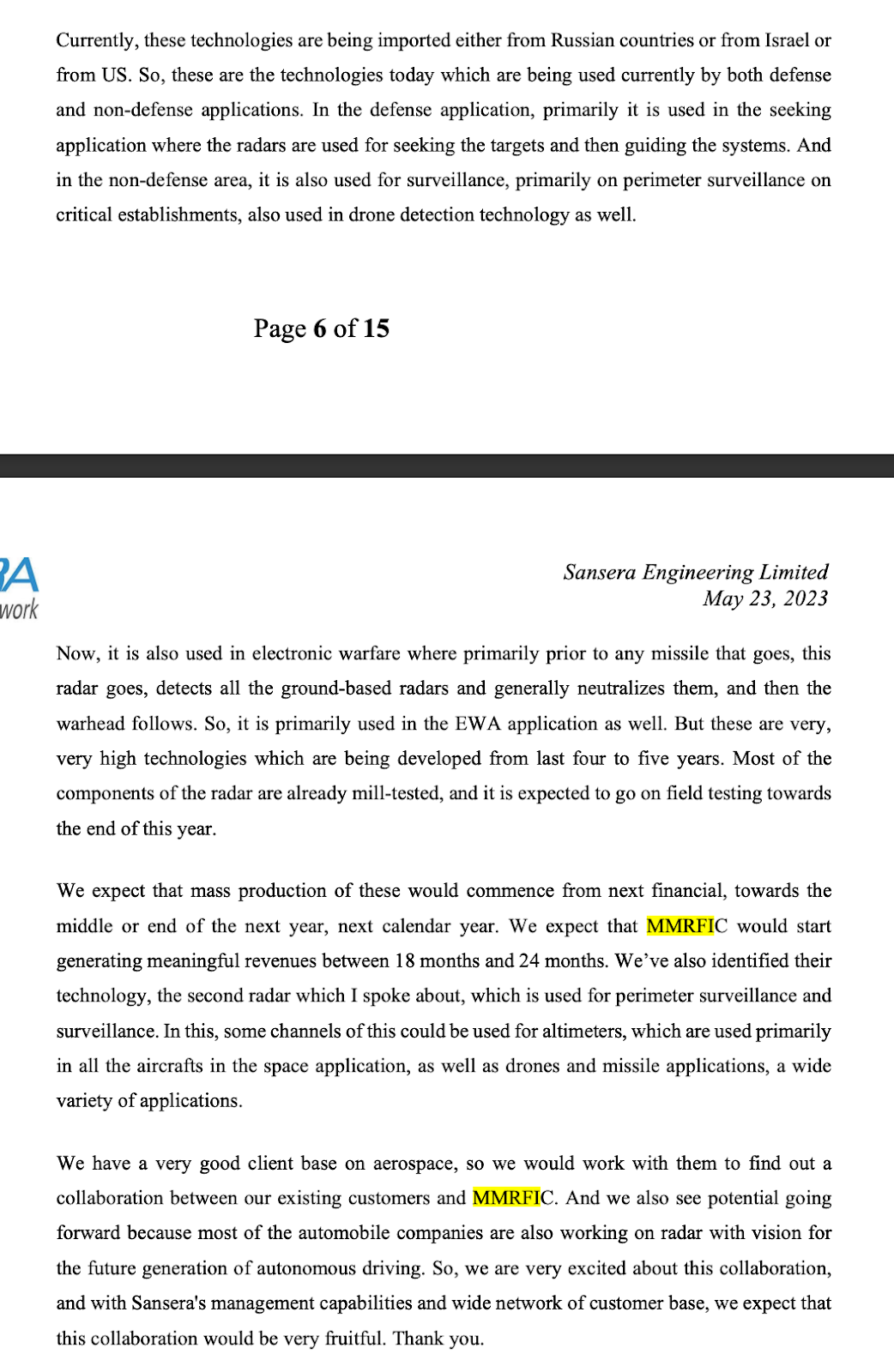

a) Investment in MMRFIC Tech Pvt Ltd. This company is being by ex-Texas Instruments engineers. This company seems to be involved in making electronic subsystems used in defense/telecom/security. (source: employee profile)

b) Company has setup a new facility for aerospace and defense. This should start showing results from FY24. Management expects a CAGR growth of about 25% to 30% in aerospace for the next three years. This facility was built much before the time management initially quoted

-

Trackers: Company expects to diversify topline-> auto v/s rest in 60% to 40% ratio.

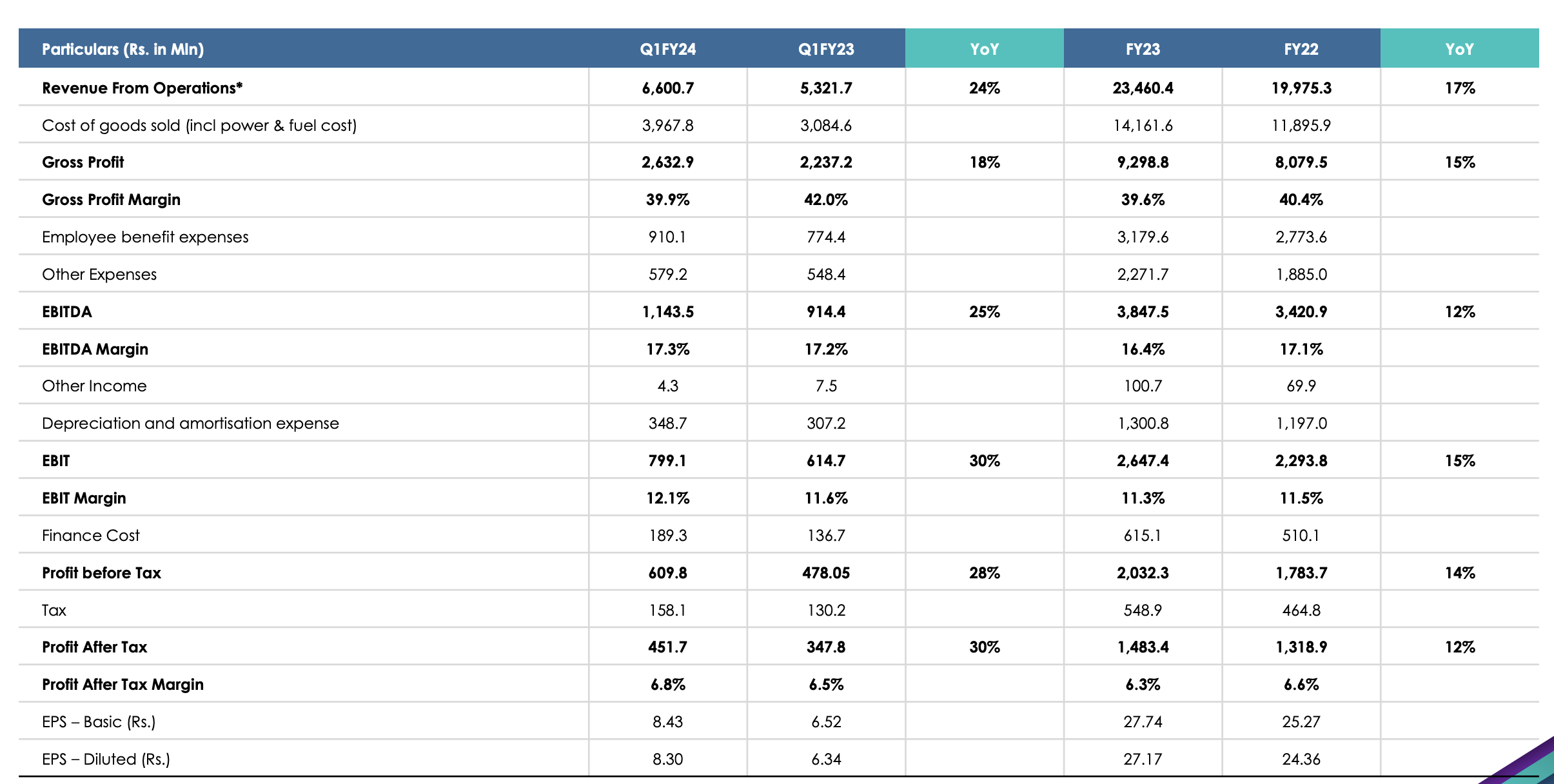

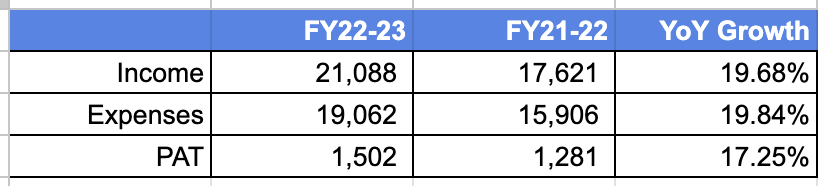

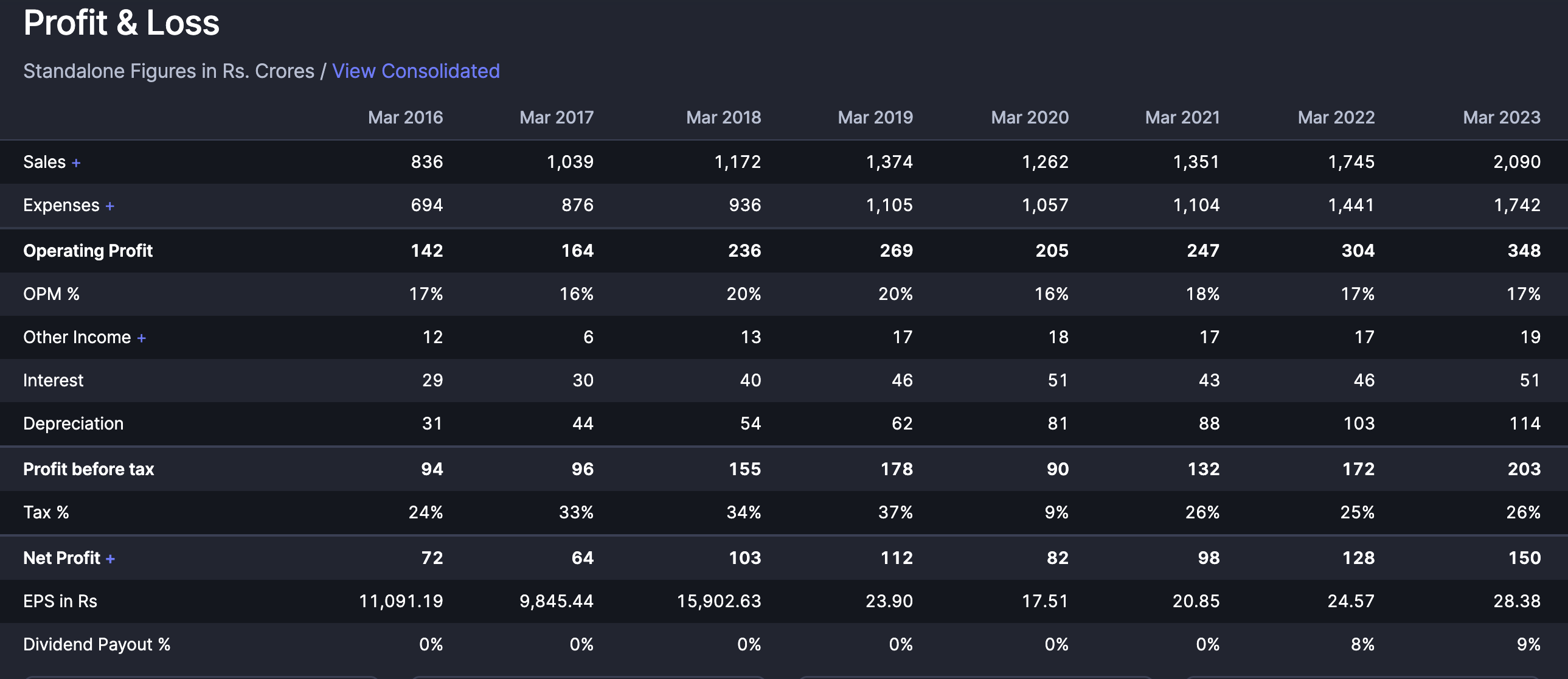

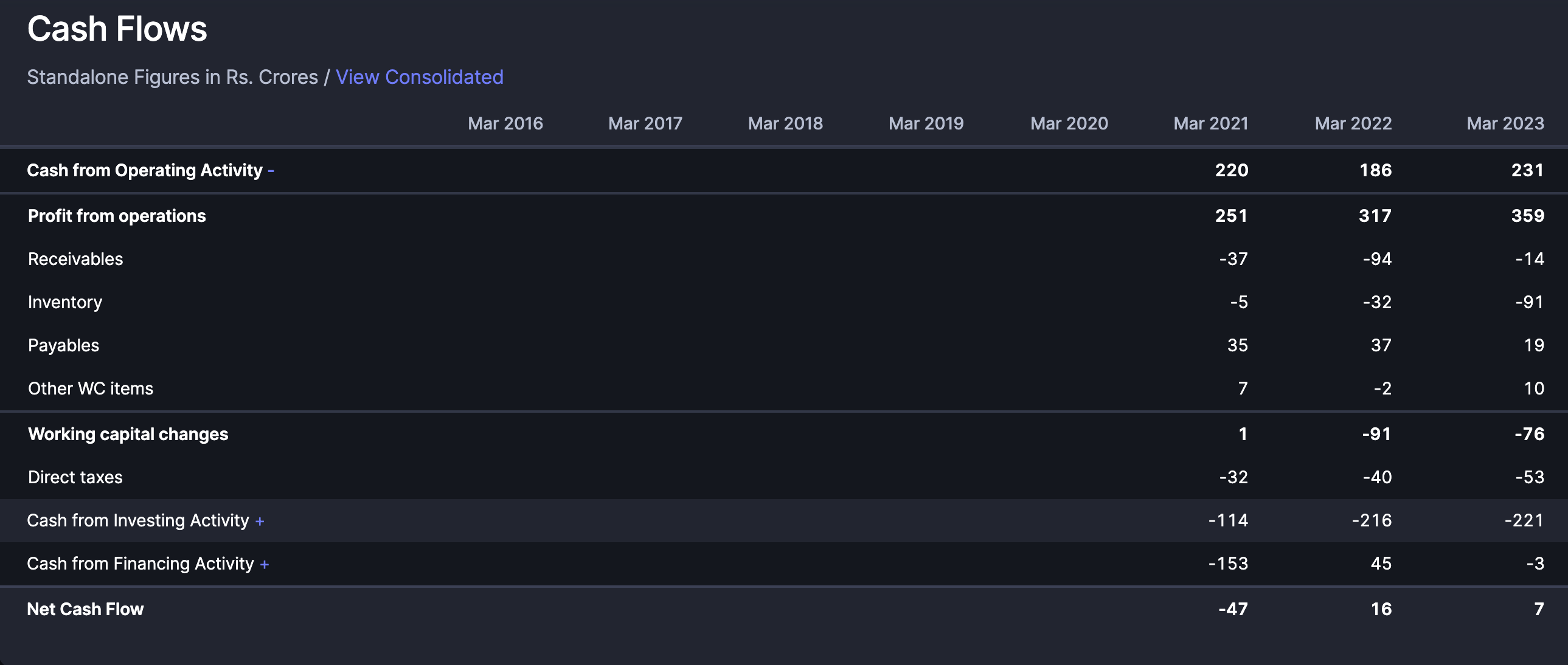

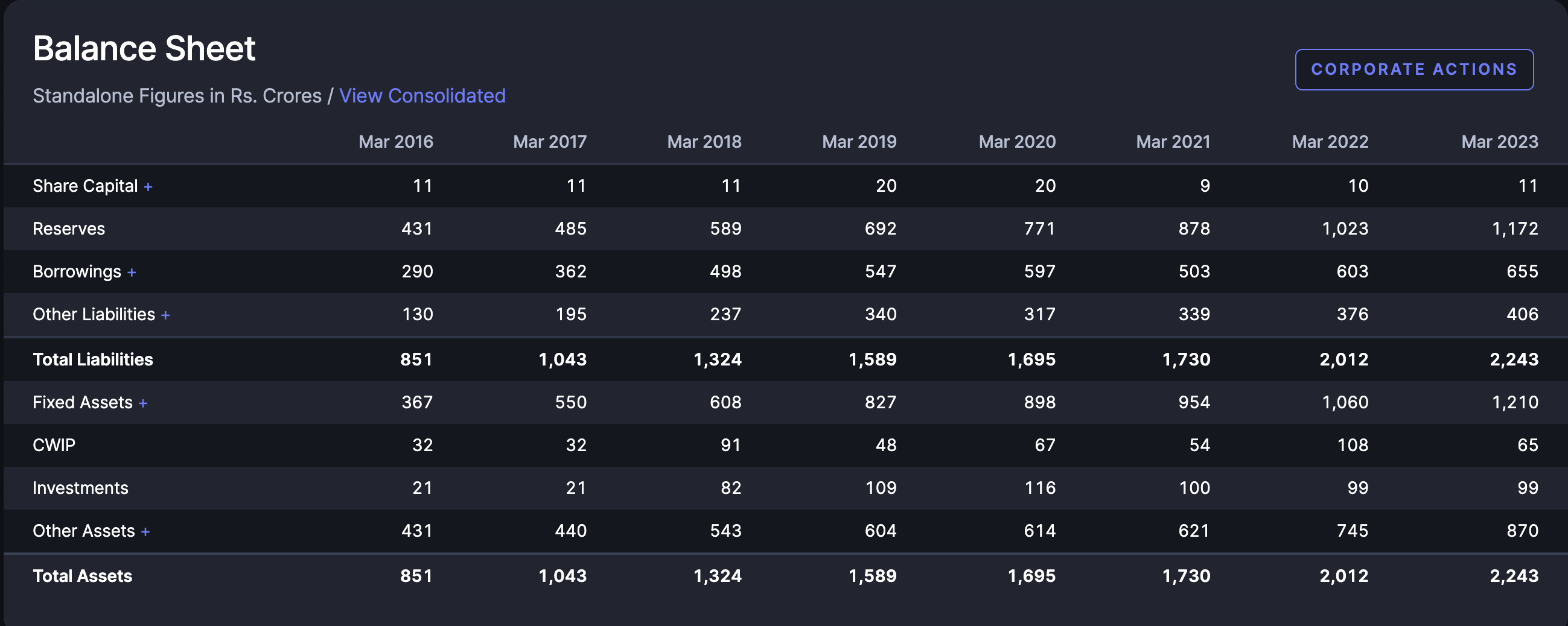

Financials

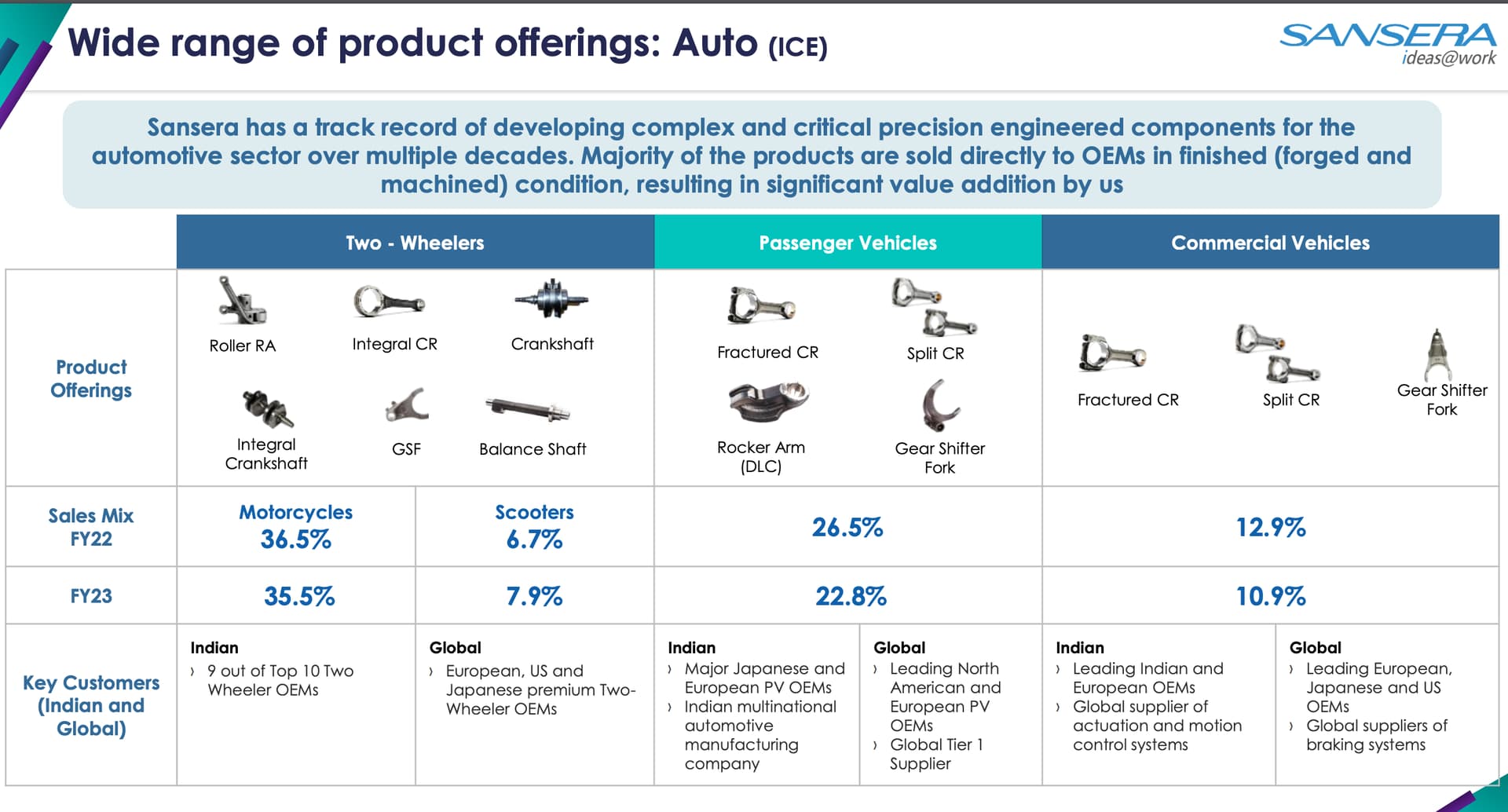

Company’s Products

Risks:

- Client Concentration: Top 5 customers used to contribute over 50% to its topline during 1HFY22. However, the company has been diversifying this and it has fallen from over 70% in the last 7-8 years.

- Accounting Red Flags: I haven’t checked. I liked the management and betting on my instincts for their honesty so far

Relevant Links:

Disclaimer:

- I am Invested from quite low levels (PF sizing here). Safe to assume, I have interests here.

- This is not a recommendation advice. Please do your own research.