Hi Guys,

What a market we have had in the last few days.

First up @divygupta splendid work on Axtel Template. Every word of appreciation is thoroughly and richly deserved.

This whole thing looked to me as a complicated task, based on what pictures @Donald uploaded, however I got super excited reading your Axtel note. So Thanks again!

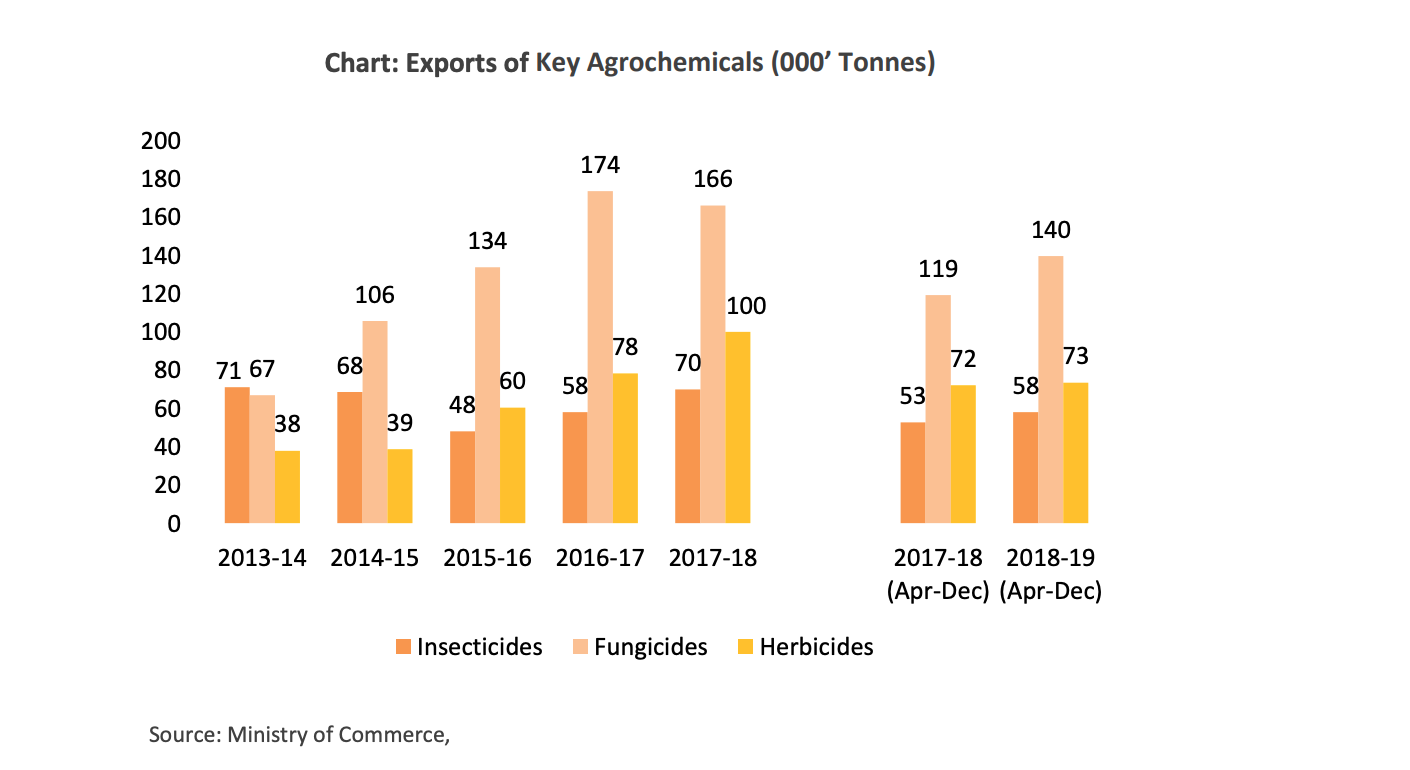

I have spent some time on Bharat Rasayan over the last few days, and I took it up a challenge to see if I can fill this up. I am not sure if I have captured all the nuances- a lot of the praise I hear from the existing investors who track the co is about the Dahej plant- I haven’t seen it myself - so the feel for me on that point is low.

One more point - before doing this exercise, I didn’t really feel the benefits of this as the story is usually clear in your head, but one thing I would say is that after filling up this sheet- I think it just makes it CLEARER. I usually write an Investment Note before my purchase and that is usually comprehensive, but this sheet sort of just cuts to the chase and focuses on the key points and you can be concise and focus on key points, which some-times may get lost in an investment note.

I would love to get feedback from @desaidhwanil, @ananth and @ankitgupta as they have been tracking the co for a long time and have posted copious notes from their interactions with the management . Big thanks to them!

Standard Disclaimer- I don’t own any shares in Bharat Rasayan. Bharat Rasayan_Deep Dive _ Template_Rohit Balakrishnan.docx (78.1 KB)