The rebound played out nicely last week in pretty much everything. I think sometimes having a fundamental view can reduce macro and technical noise which a lot more participants herd around and participate (nothing wrong with it). Technicals based on daily charts change very fast but our mind is incapable of drastic shifts in view within a week (we are not George Soros). We must be careful not to form strong opinions or celebrate victories, for there are none in small timeframes.

The fall was nice to shop in some cheap names.

Dynemic Products, Weekly - The stock has been very well covered in its own thread. The company has perhaps bitten more than it can chew in its capex. I suspect pretty much everyone has thrown in the towel by now as the price is now at around pre-breakout level of 2020. The numbers are showing some improvement in the topline and the PnL is hit due to the massive depreciation. The margins are perhaps hit due to the poor utilisation and bad operating leverage that results from it. I think even the gross margins should improve from here without commodity price pressures. So there is a possiblity in my mind that a large GM, OPM improvement and a big multiple expansion is also possible from here whenever things go right. It could be a year or two but at current price, there is perhaps value around 250-300 levels

Honda Power, Weekly - So this did re-test 2200 levels as I thought it might. There is a gap in the daily charts around 1850-2000 levels as well which may or may not be tested. It still looks dicey but any re-test could be fantastic levels for a value investor. Fundamentals in the previous post in this thread.

There is a secular theme that’s underway in the power sector capex, especially in the grid spends. It doesn’t seem to be a theme that’s just domestic but its international as well, with US readying $13b to upgrade their power transmission infra and Europe doing the same and Ukraine at some point going to need a massive overhaul as well. EVs aren’t going to be able to use the existing power grid infra when the sales scale up. It will need a better transmission infra and also last-mile connectivity (US wants charging infra every 50kms). Renewable power generation also needs more power infra with substations and additional wiring in the wind turbines and solar panels. So this appears to be a multi-year theme as we move from dense fossil fuels to energy which is going to be synonymous with “power”.

There are multiple ways to play this theme, in conductors, transformers, transformer oils, T&D structures, cables.

Apar Industries, Weekly - When looking for players in this theme that were fundamentally strong, growing well domestically as well as international, with a strong chart, I came across this. Perfect upward channel since mid August.

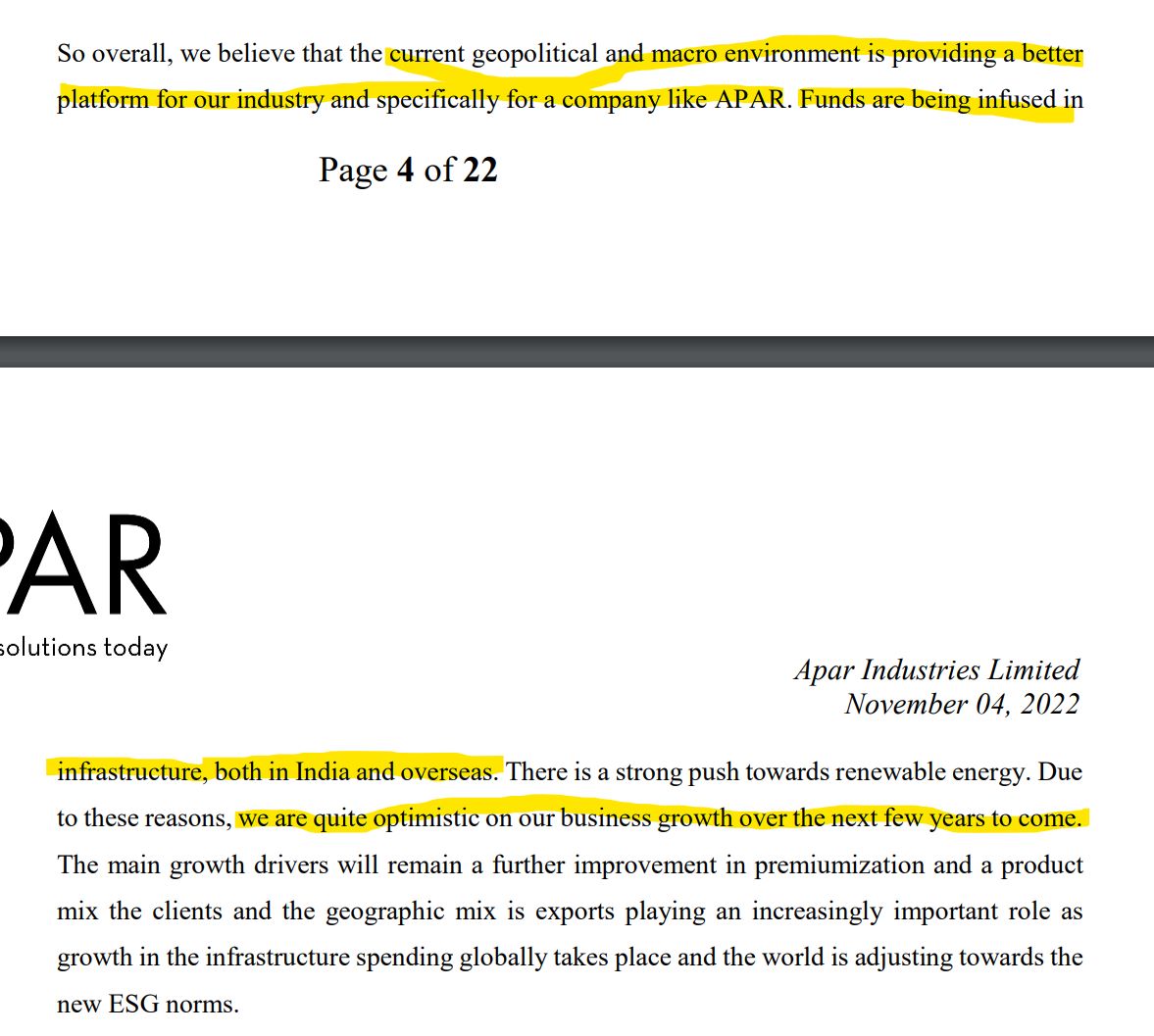

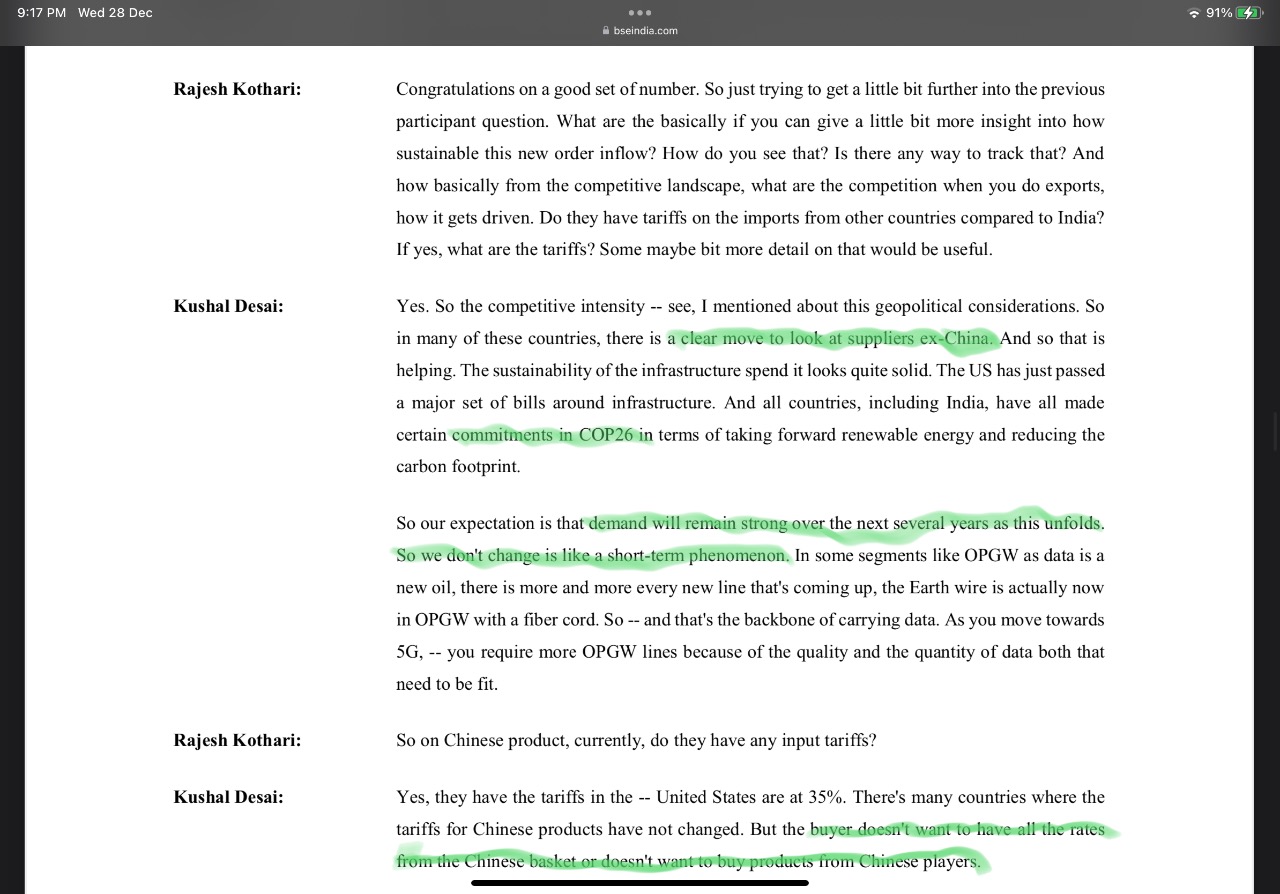

Fundamentally, Rev up 55%, EBITDA 77%, PAT 89% YoY - Very strong growth in H1 and H2 should be equally strong as well as per guidance. Exports revenue - up 85% for Q2 and 65% for H1 (clearly exports driven growth and rate of change of growth is phenomenal). Export mix was 47% in Q2 vs 36% Q2 last year (Skipper as well has very good export growth). Exports of Cables (22% of sales) and Conductors (42% of sales) are growing at 206% and 97% - So bulk of the portfolio (64%) is experiencing significant volume-led growth. The investor presentation and the concall has a lot of details needed to understand the business. All products are listed on their site if you want to visualise.

Fundamental thesis for investment is inline - grid spends are driving numbers

Businesses moving away from China and COP26 driving demand (incidentally Techno Electric also talks about COP26 driving FGD demand in thermal plants. Same is confirmed in Hitachi Energy and GE Power concalls as well - and the fact that a player like Power Mech is bagging orders worth thousands of crores)

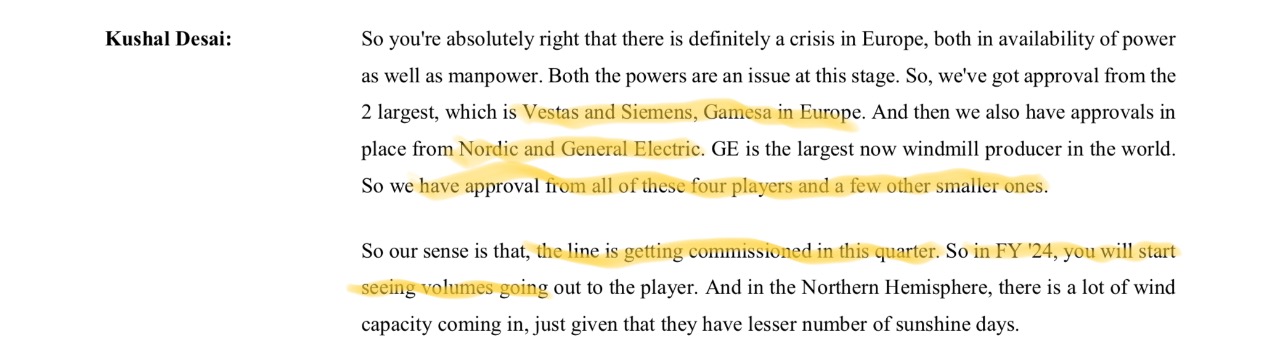

They have approvals from big 4 renewable players in Europe and this should contribute to sales going forward (70% market share in wind domestically)

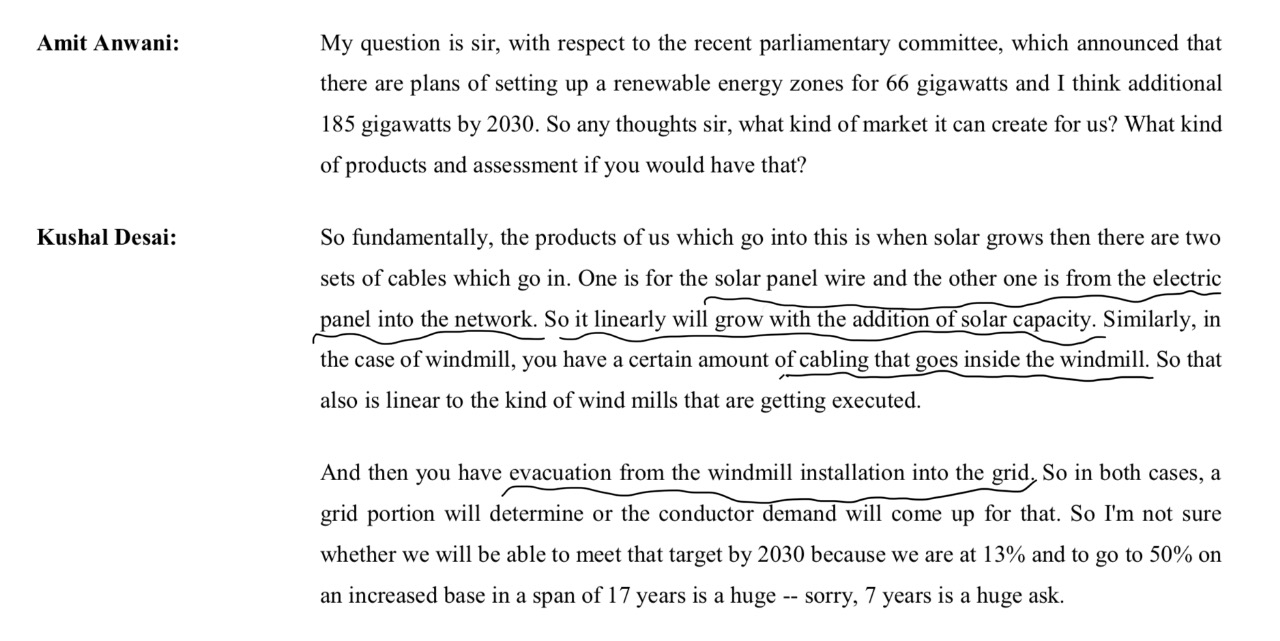

This is how they participate in the renewables space

They hedge Copper and Aluminium prices at LME soon as they bag an order which is why they haven’t made a loss in 10+ years and have retained margins in the 6-8% range. In the Conductor and Cables business at least volatility is low. In the Oils business however there is some volatility across quarters (Q3 could be soft) but yearly its stable.

Please note that their RoCE isn’t as strong as reported since they pay interest on payable past 3 months - so interest should be seen just like you see power or employee expense for this business. RoE is a better indicator and thats around 14% - this is expected to go up to 18% in FY23.

Disc : Bought Dynemic around 290-300 and added to Honda power position around 2150-2200. Initiated positions in Apar around 1750 levels

2022 has been a very good year in the markets though I participated actively only in the second half. Hopefully '23 will be good too. Happy new year!