Some updates post earnings - (In short, I am still holding all the consumption names)

IDFC First Bank, Monthly - Poised near the resistance that it can bound over this month. Any close for this month around or above 64 can point to more follow-up gains next year (breakout from post-merger trendline). Fundamentally, the results have been very good and the story is playing out. I think book value could get closer towards 48-50 levels in a couple of years or so by which time this can even trade at 3x book (All the metrics including the Cost-to-Income should be better by then) which leaves considerable returns for the future.

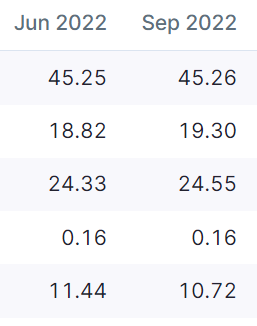

Metro Brands, Weekly - Around 820 levels should offer strong support which is about 64x TTM P/E. The numbers continue to be good with 47% topline growth and 42% bottomline growth YoY. QoQ isn’t comparable for footwear businesses due to seasonality as contribution varies from 22% to 27% depending on quarter (Lot more pronounced in Bata). Q3 numbers should be strong with the wedding season and the festive season. With the valuation comfort and prospect of earnings growth led by volume growth, I have left this untouched. Metro has done phenomenally well due to its target market being unaffected by inflation (Crocs continues stellar growth and the 3000+ range is where business is experiencing highest growth) - strong wage growth has compensated, which was the fundamental thesis of choosing these stocks in the first place.

Varun Beverages, Daily - Probably the best performer of the lot, along with IDFC First Bank. Seems to be resuming uptrend after 6 weeks of consolidation. The numbers have been phenomenal with strong volume growth for a seasonally weak quarter which has beaten summer quarter last year YoY. Getting Cheetos, Doritos, Lays business in Morocco could be an indicator for further in-roads into PepsiCo’s foods business that they don’t usually give out. This is probably now a BIMARU play as well with Bihar, Rajasthan, MP etc. contributing a lot to the growth. Despite the already high allocations (#1), I am always tempted to allocate more here - such has been the prospects and performance. With strong utility, cheap price points, smaller packs, I expect per capita beverage consumption to go up strongly and lead domestic consumption from the front.

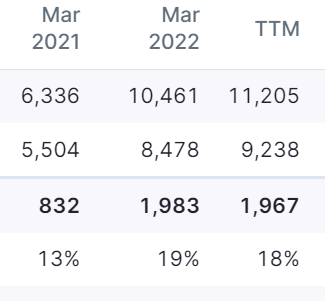

Devyani, Weekly - Around 180-185 levels have been strong support and currently its trading around those levels (Also 20 WMA). Business performance has been very good here as well for a seasonally weak quarter with 45% topline growth and 21% bottomline growth (One off currency loss in Nigerian subsidiary skewing bottomline. EBITDA still highest ever across quarters, though this is a seasonally weak quarter). Store addition is the strongest with 88 stores added in the quarter which is the highest. I assumed the margin decrease was due to newly added stores but looks like there is gross margin compression as well due to inflation (confirmed in concall). Most of the RM prices from chicken, oil, gas prices though are moderating as per management so margins should come back. The topline is the highest ever which isn’t bad for a seasonally weak quarter. When margins come back, bottomline should shine as well (However tax rates might be 25% from next year)

While Metro and Devyani appear weak on the charts, so was the case with VBL and IDFC First after September and now they are the best performing, so have decided to exercise some patience since fundamentally numbers are good.

Manyavar is yet to announce results. N R Agarwal and HBL are coming soon. Haven’t seen a reason to sell any of these, so have held on as prospects are good.

Some new additions

Permanent Magnets, Weekly - Broke out of 1 year resistance, re-tested and formed a triangle from which it could be breaking out. Volumes are slim so good luck buying this.  The investor presentations of 2022 and 2021 and the AR offer great insights to the business. The numbers don’t seem as good as they should be due to reduction in gas meters contribution. However the contribution of EVs has been going up considerably and the vision of the business seems very promising (While they are also into current sensing and BMS, smart meters and similar space as Shivalik bi-metal, they seem like a slightly differentiated play)

The investor presentations of 2022 and 2021 and the AR offer great insights to the business. The numbers don’t seem as good as they should be due to reduction in gas meters contribution. However the contribution of EVs has been going up considerably and the vision of the business seems very promising (While they are also into current sensing and BMS, smart meters and similar space as Shivalik bi-metal, they seem like a slightly differentiated play)

Gufic, Weekly - Seems to be breaking out of the downward trendline on the weekly. I was interested in this fundamentally after going through the VP thread. Consumer focused branded pharma play, especially in the vanity space sounded like a good thing to me. Valuations weren’t demanding so took a position

Disc: Have positions in IDFC First, VBL, Devyani, Metro and Manyavar from early July or so. No trades since. Have positions in Permanent Magnets between 540-550 levels and Gufic from 220 levels. Not SEBI registered and none of this is advice. I write to make things clear to myself more than anything