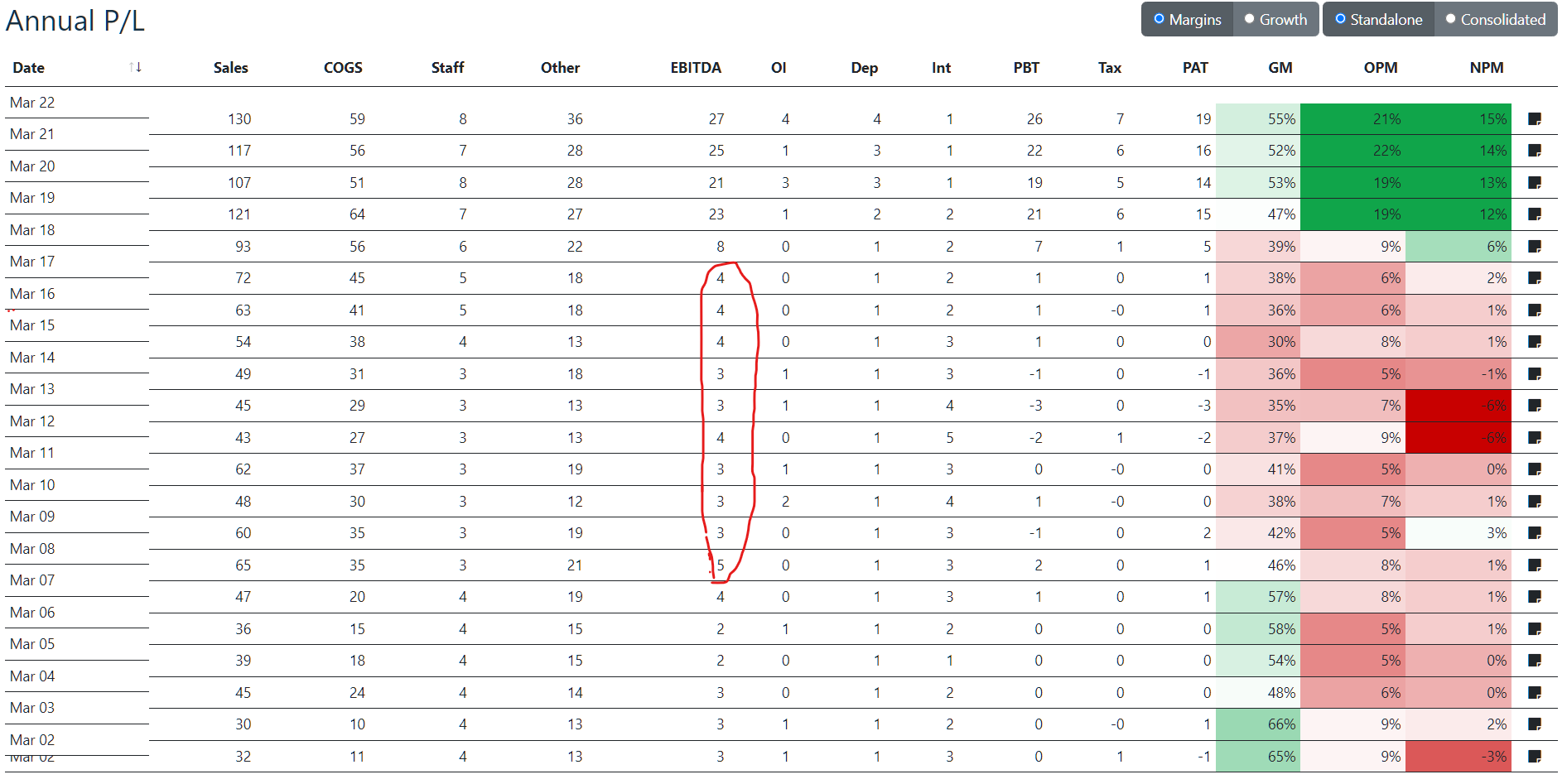

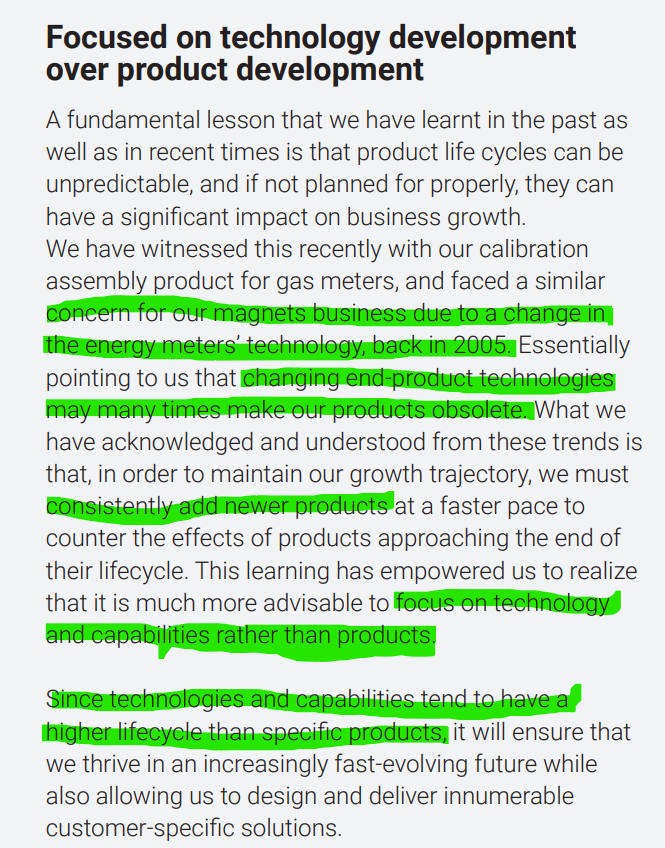

The business was incorporated in 1960 and has been around for decades. They were primarily into magnets and magnetic assemblies for a bulk of their existence (until 2005). When the energy meter technology changed, it led to a downturn in the magnets business, as reflected in the Annual PnL from FY08 to FY17 or so.

Since then the business has re-invented itself, especially post FY15 when the revenue mix shifted from magnets to Shunts and Hi-Perm.

Technology obsolescence is a clear risk in PML’s business as it happened in 2005 and also again with the Gas meters business in the recent past. To counter this, the business is focusing more on capabilities than specific products.

It is this specific change that is paying rich dividends to the company.

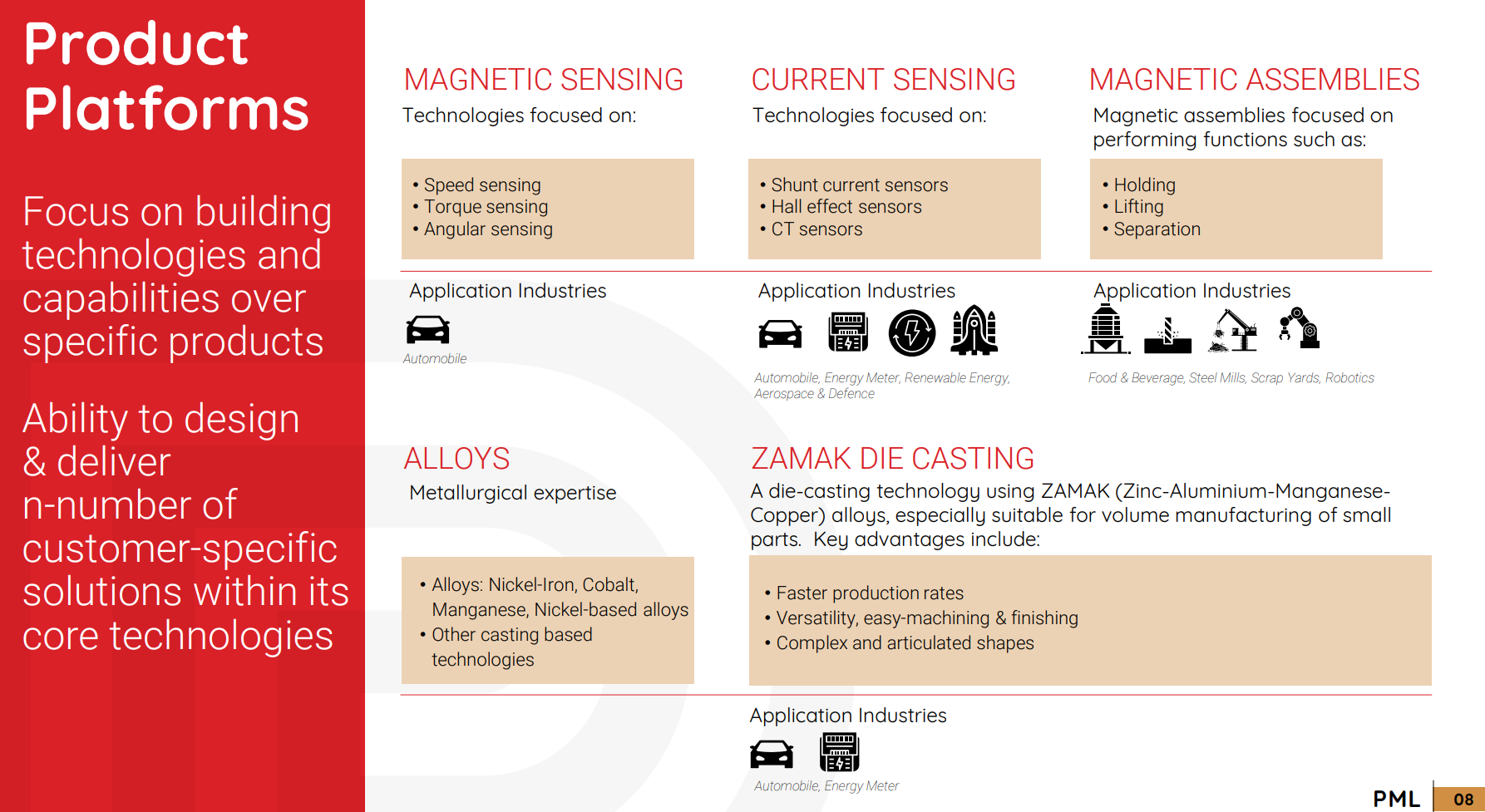

Now they have capabilities in metallurgy, mechanical, electrical and electronics engineering, along with melting, casting and heat treatment. This allows them to be the go-between for pure research and design companies and end-use industries to manufacture the product required that meets the specifications. They do customer-specific design prototyping and simulation (in collaboration with magLab).

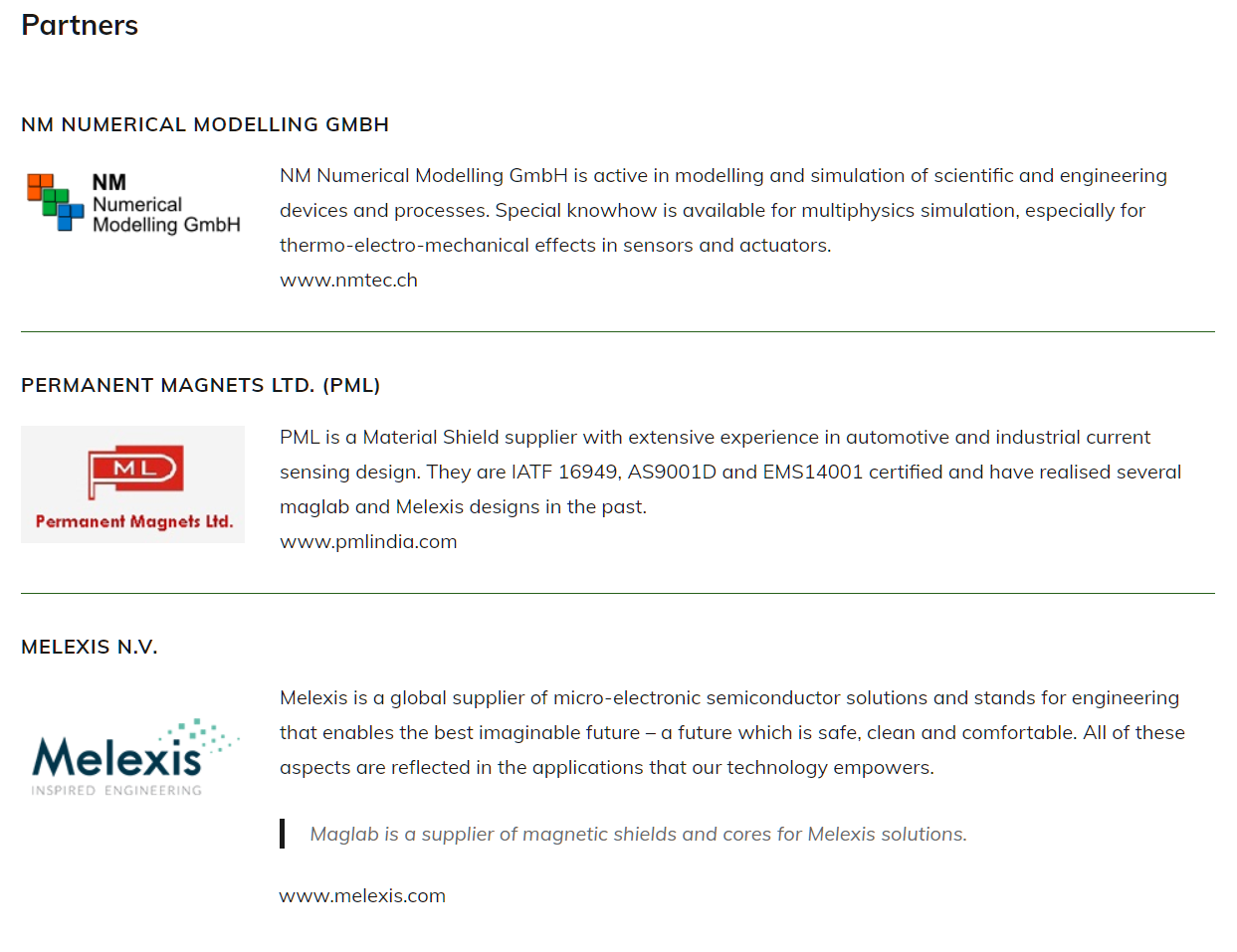

PML is one of the partners for magLab and an important one in the ecosystem. It looks like magLab does design & research, NM offers numerical modeling and simulations (testing materials for their electrical and thermal properties, without actually trying out lot of combinations), Melexis offers semi-conductors, sensors and industry knowhow and PML implements the solutions designed in collaboration with magLab and also supplies them at volumes.

Source: https://www.maglab.ch/partners/

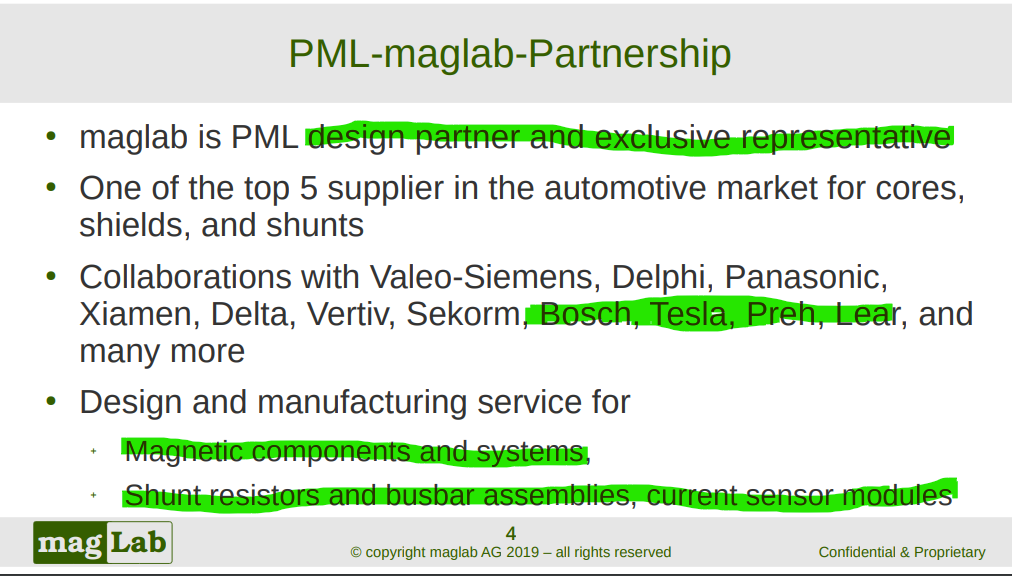

The corporate presentation of magLab as well lists themselves as PML’s design partner and exclusive representative (clearly PML’s fortunes are tied to magLab and Melexis) - Slides 3,4,5 and 10 substantiate.

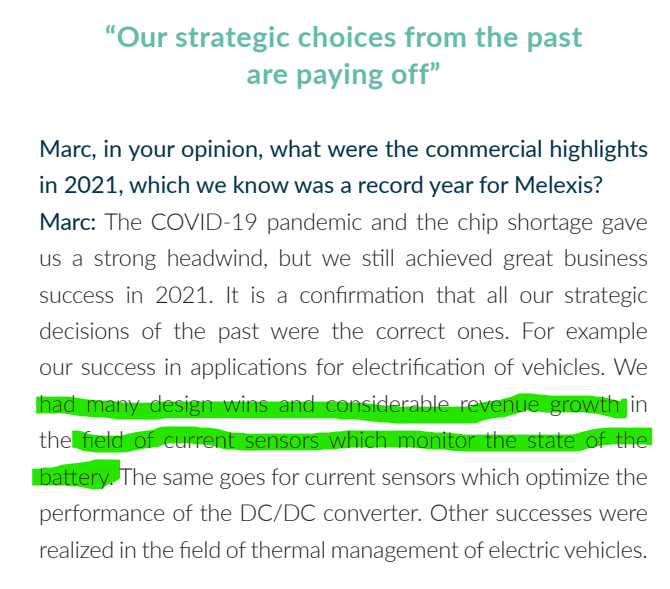

Melexis AR has lot of very useful info (It is a 3.36 billion EUR mcap business based out of Belgium). magLab and PML are crucial partners for Melexis as can be seen from this snippet.

Coming back to PML, the capabilities above tie into these platforms for which they have several products (~350 SKUs)

Source: https://www.bseindia.com/xml-data/corpfiling/AttachHis/96f94f2a-43b1-4024-8e09-0aafe0bc628f.pdf

Slides 9, 10 and 11 show the critical products in Automotive and Energy meters, as well their products in alloys and die-casting.

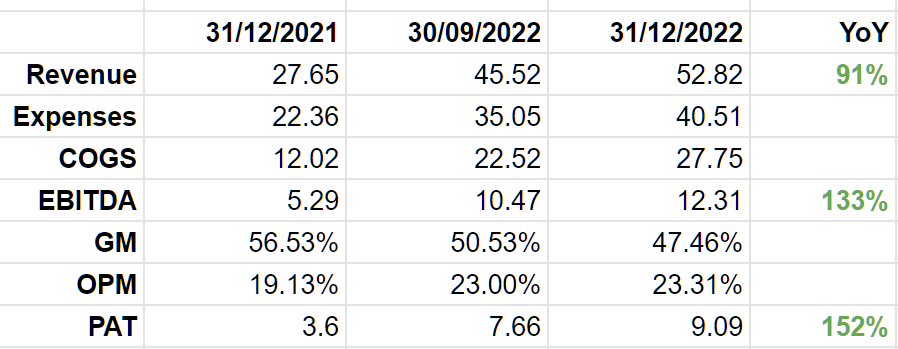

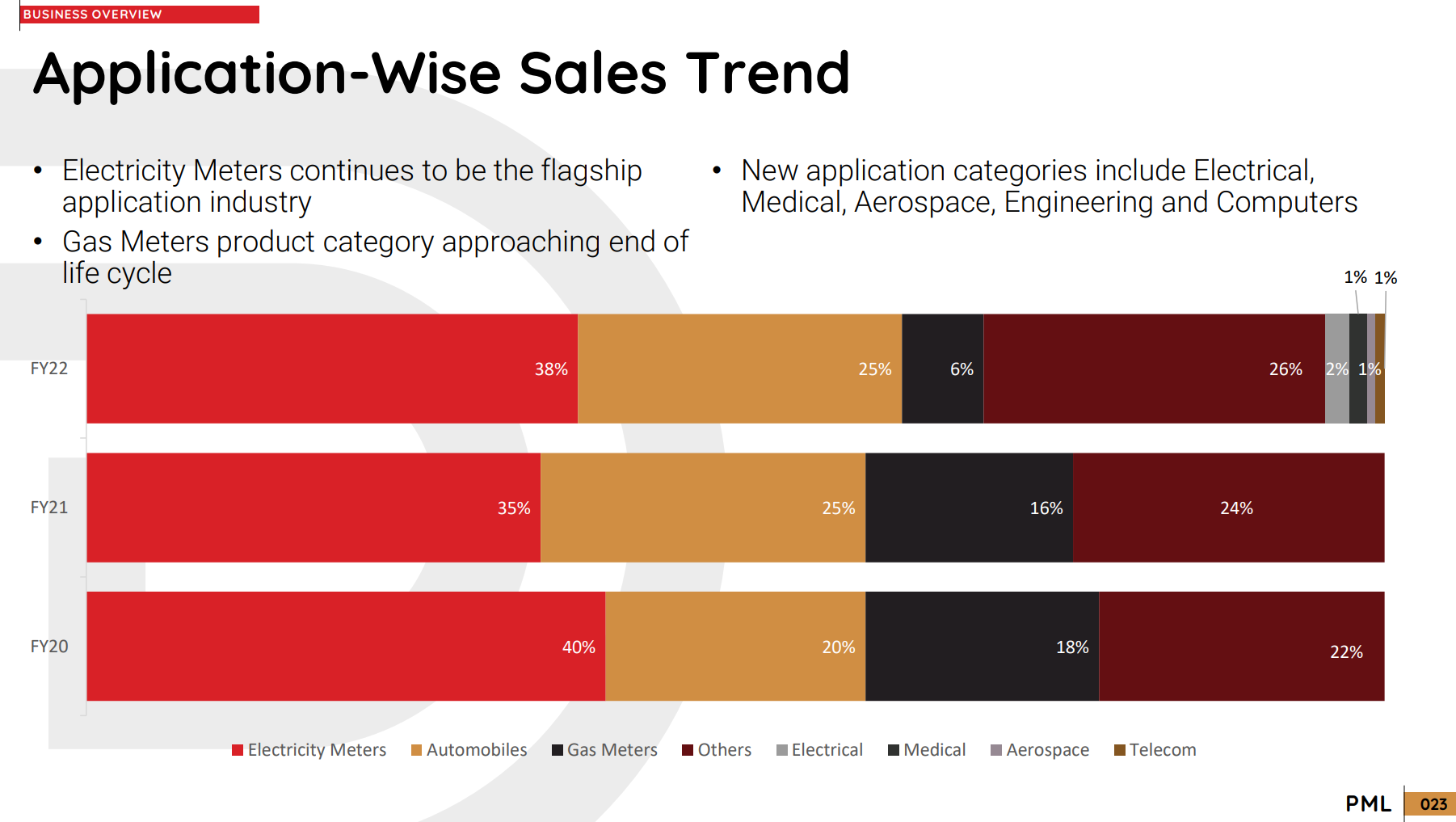

There is another interesting thing to note as well, which is the sales composition and the trends. Gas meters contribution is going down from 18% to 6% from FY20-FY22 (19 Cr to 8Cr) which sort of masks the actual growth in Automotive sector 21 Cr to 33 Cr, almost 50% growth and in TTM sales this is very likely to have grown further.

So the business reinventing itself and growing in a fast-growing segment with good technology partnerships is a great sign. What’s even greater is this

They are very likely at present in Stage 1 or stage 2 products but are working towards Stage 3 and Stage 4 products. After digging around a bit on magLab, my guess is that these are the stage 3 and stage 4 products they are talking about in the presentation.

https://www.maglab.ch/wp-content/uploads/2020/01/20200115_IoTCurrentVoltageSensor_rev005.pdf

https://cdn.shopify.com/s/files/1/0309/7625/files/CO-4-1.2-30-L.pdf?4839681362350308133

This could imply that the margins of the business could trend up if they find growth in these new products (Most have been conceived in FY20 going by the dates). They are also strategically integrating their manufacturing facilities under 1 roof which could also be margin accretive in the long run.

The PML FY22 AR is a very, very good read and has a lot of details on how the management is seeing the business prospects and is worth a read.

I noticed also that PML and magLab appear to have had a stall at Auto EV Expo this month in Bangalore. If anyone had been to it, would appreciate inputs.

Valuation: At 27x P/E and 17x EV/EBITDA, it is not cheap, however the business looks to be having good prospects but I doubt if any margin of safety exists at these prices around 700 levels. Around 550-600 levels, it could be a good buy though, if it gets there.

Risks

- Technology obsolescence is very high

- The contract payouts are almost 10% of revenue and could be the cost of manufacturing the shunts as they don’t appear to be manufacturing them in-house. Unsure how this will trend and who has the pricing power (Shivalik bi-metal could be manufacturing these shunts)

- Valuation isn’t cheap anymore. (It is discovered even by idiots like me due to the flashy AR and Presentation)

- Very highly illiquid stock - Please exercise a lot of caution executing trades here

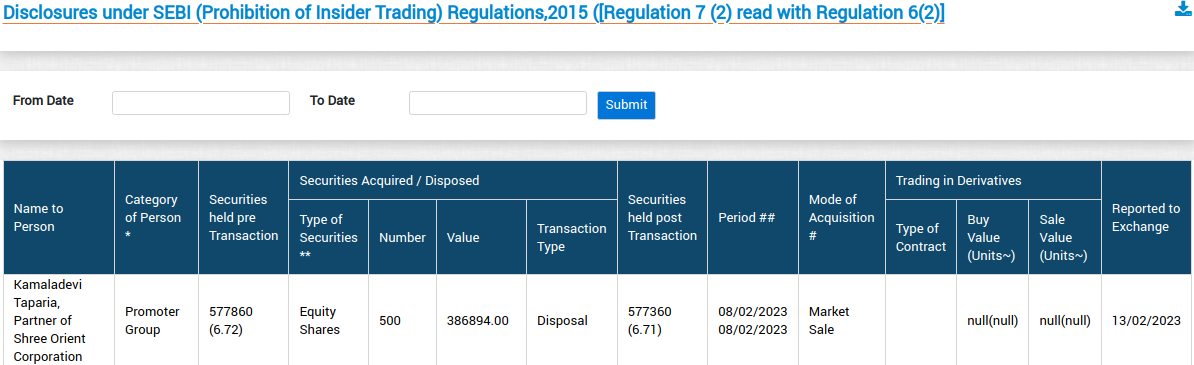

- Promoter stake has gone down from 70% to 58%

Disc: Invested from around 550 levels. Not SEBI registered and very much a novice. Please research on your own. The above is more or less a copy/paste from my notes with some clean-up and tweaks. Thought a thread would help bring in more perspectives since the existing thread is locked.