I am trying to get an idea of the numbers that can be contributed by the NFL setup at JNPT. The number of samples is ~ 1 lakh as mentioned in the concall by some participants and not refuted by management.

This number is roughly there substantiated by the RFP floated by FSSAI

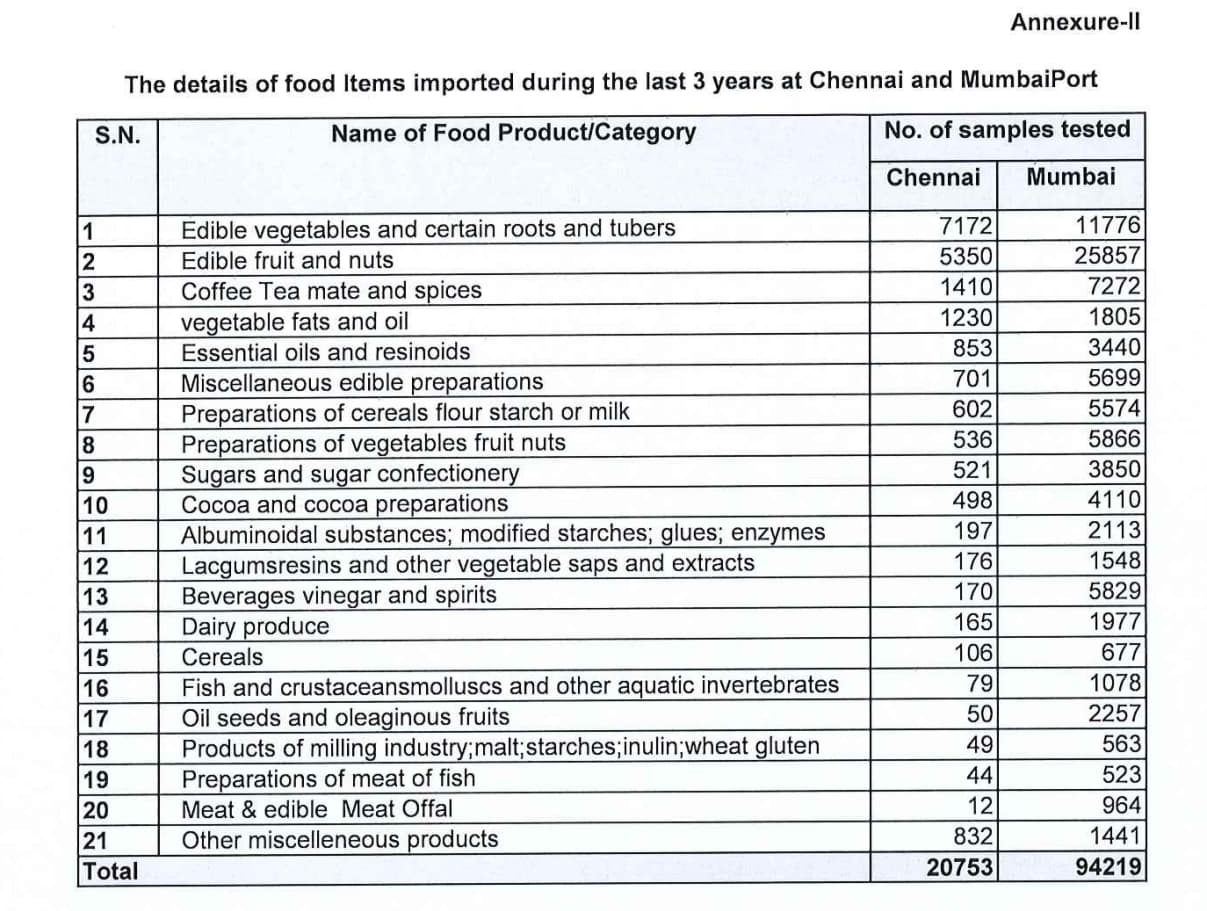

Annexure-II screenshot

But here it says “during the last 3 years”. Unsure if this is annualised or cumulative.

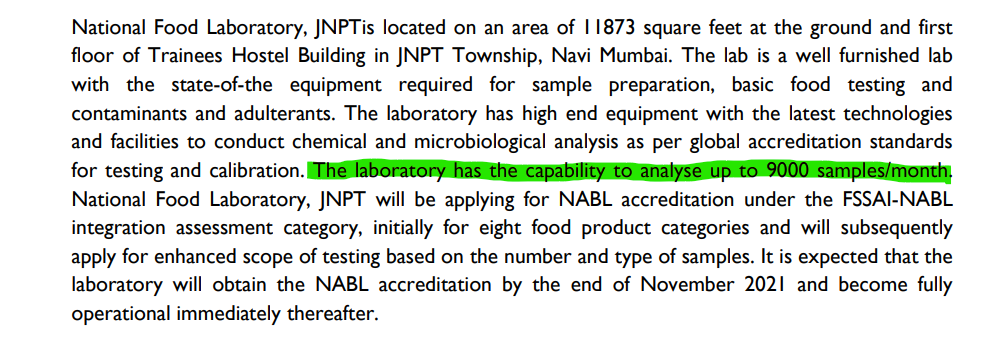

The FSSAI presser also talks of 9000 samples/month capacity (Why would they setup this much capacity if the expected run-rate is around 3000-4000/mo?)

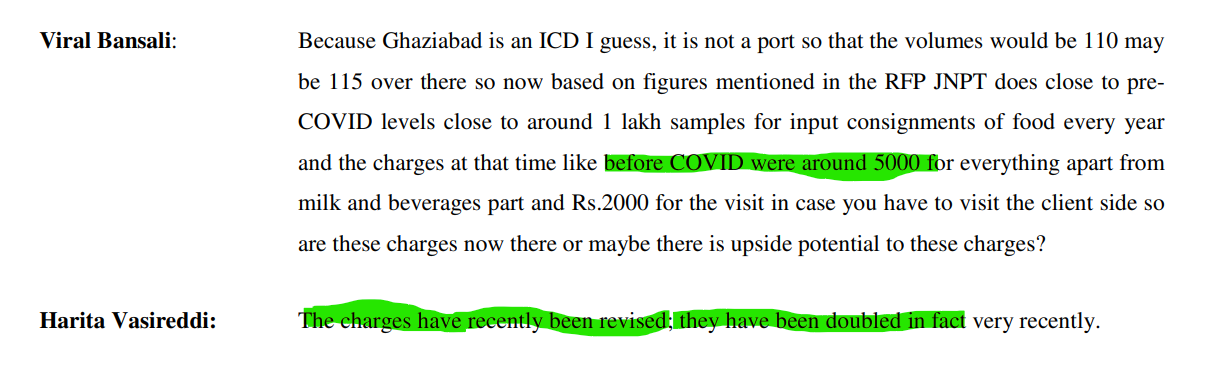

Now what is the rough/avg charge per sample. Here management is saying the charge is doubled from Rs.5000 - so should we assume Rs.10k/sample?

If that’s the case, does it mean a revenue potential of ~100 Cr from this lab? (Or is it much less, if we assume 1 lakh samples for 3 year period?)

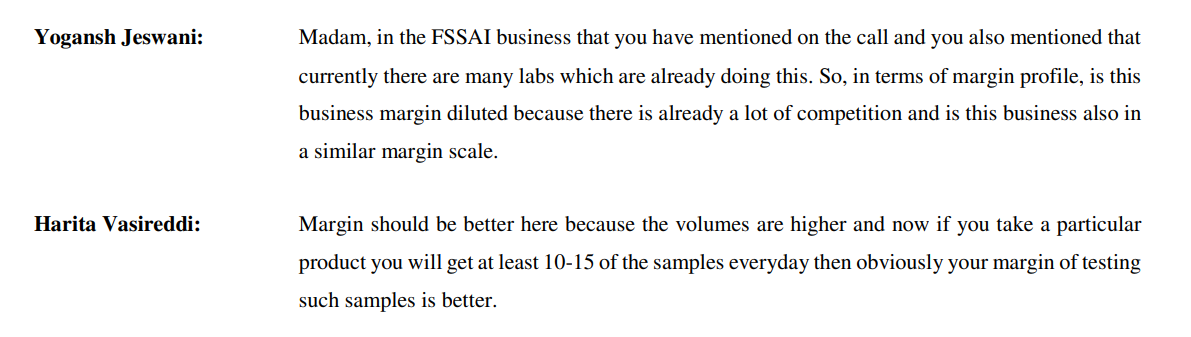

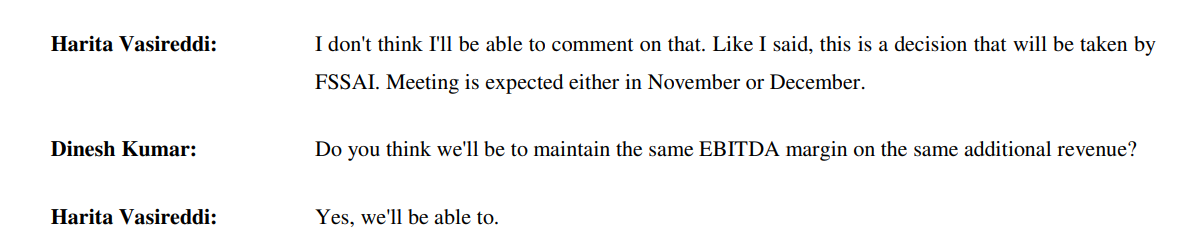

On the margin front, it looks like they can maintain or even improve company level margins as guided in diff concalls.

May concall

Oct concall

So if they can maintain the 32% margin post revenue sharing with FSSAI, perhaps they can make an EBITDA of 32 Cr from NFL alone when its fully functional?

It looks like NFL revenues are present in Q4, Q1 and Q2 as well but its not very easy to identify the quantum of it, but if we assume all of it is NFL related - then probably somewhere around 35-40 Cr is probably already coming from NFL for 9 months YoY. Considering they didn’t have accreditation for all, this number should only go up I think. Also seasonality is a big factor in food imports as mentioned by management as well.

Bulk of the Fresh fruit imports seems to happen in Dec quarter going by import data, so there’s a good possibility current quarter and Q4 numbers should be better now that there’s full accreditation towards last week of Oct (Assuming the joint steering committee is setup and volume of samples has increased as guided).

In addition to this, the E&E division has incurred a capex of 25 Cr. Unsure about how quickly they can ramp this up, but if they are able to achieve ~1.5x turns like the rest of the business, this can contribute ~40 Cr to topline as well in a normal year.

Management’s guidance of 500 Cr by FY25 doesn’t seem way off if its indeed 1 lakh samples/yr and also provided pharma and diagnostics can make up another 60-80 Cr growth

UPDATE: This part mentions it unambiguously that its 3000 avg/month for JNPT. So we should probably work with an estimate of 40 Cr or so I think at most. Have to see how FSSAI’s incentives are aligned since they have a revenue share in this lab, as well as growth in imports as the affluent population grows (this growth should be higher than GDP I think).