About the Company:

Dynemic Products (Mcap - Rs. 314 cr) is one of India’s leading manufacturer and exporter of a complete range of Synthetic Food colours, Lake colours, Blended colours, & Dye Intermediates.

Product Profile:

The company manufactures:

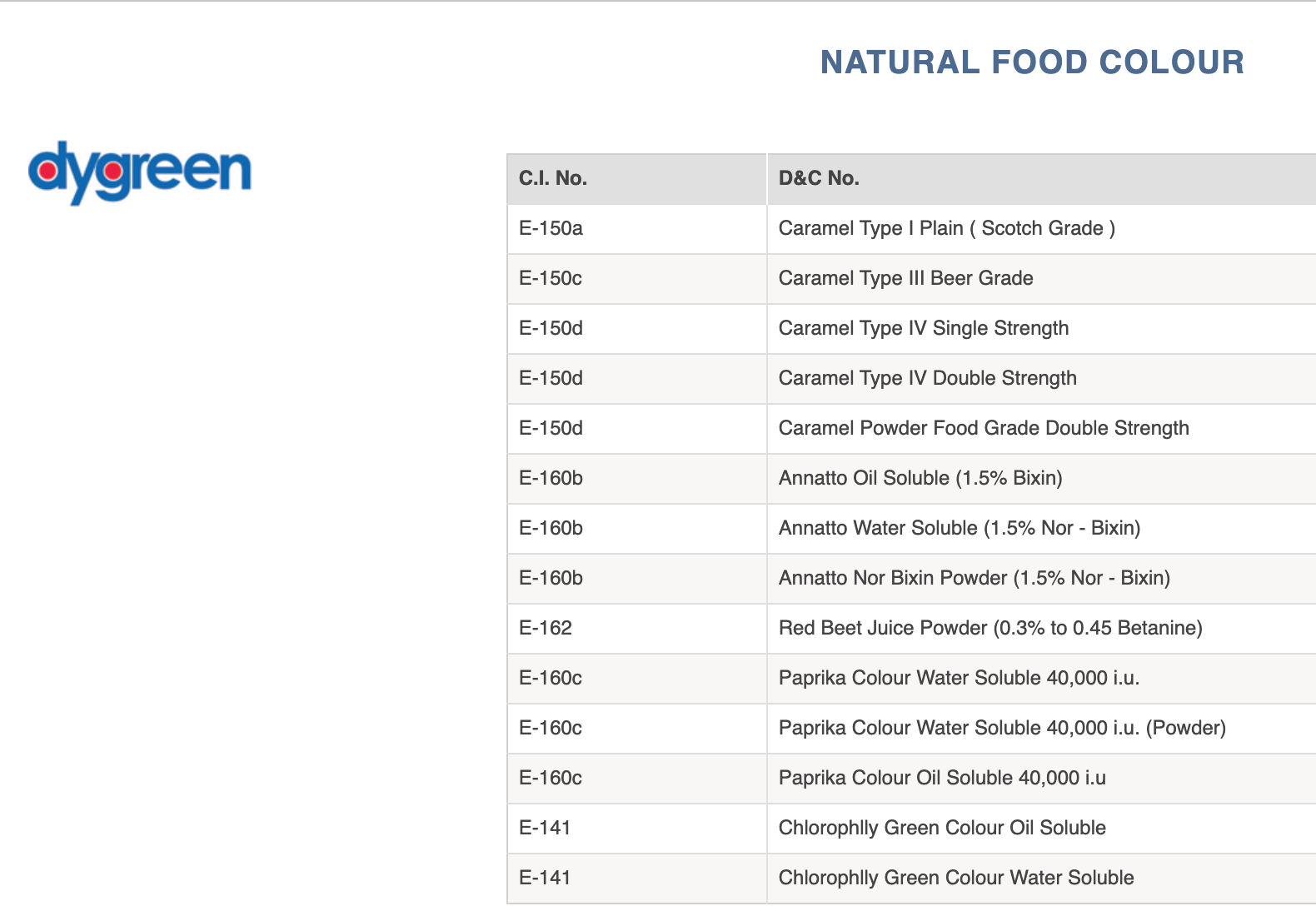

- Synthetic Food colours (used to enhance the original colours associated with a given product),

- Lake colours (more stable than water-soluble colours, so widely used in the cosmetic and pharma industry),

- D&C colours, Salt-free dyes, Dye intermediates which are used as an essential ingredient in the food, drug, cosmetic, personal care and FMCG industry.

Existing Capacity:

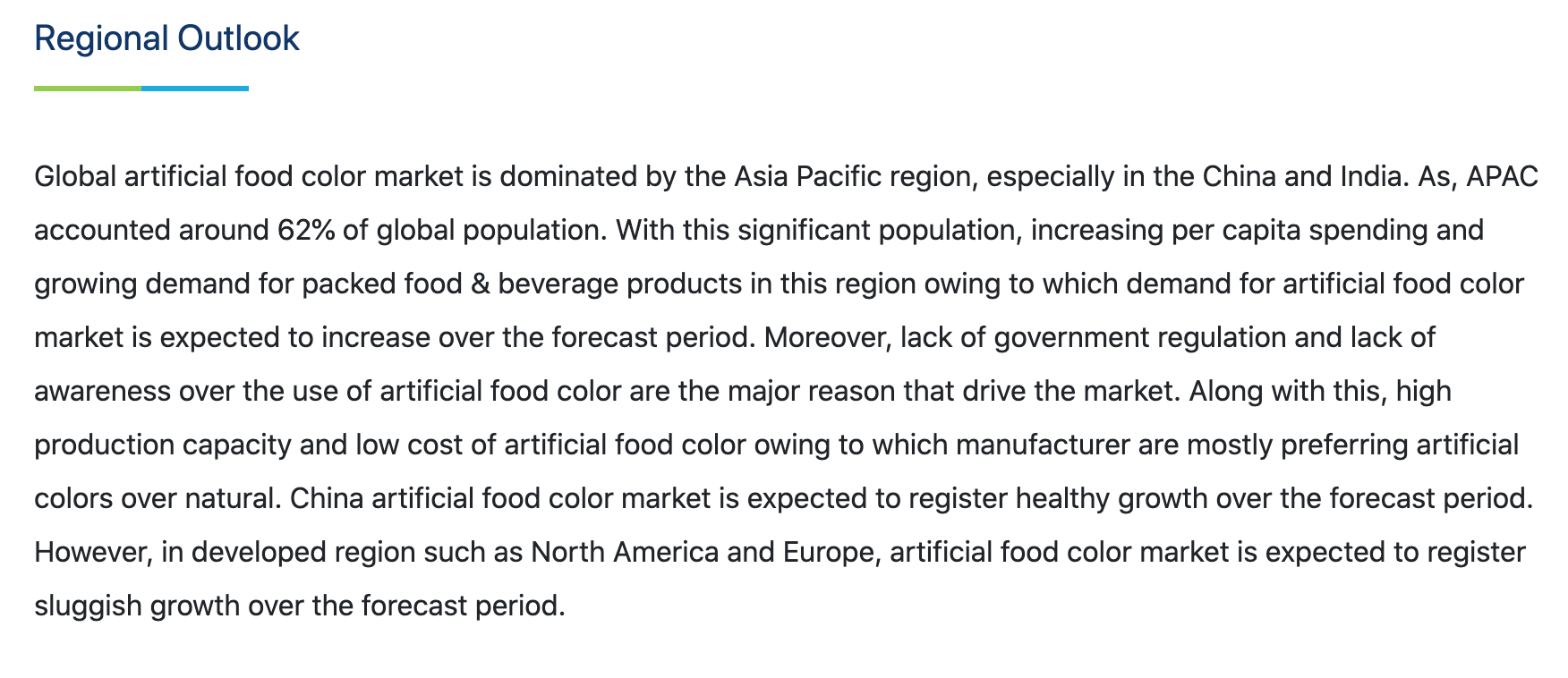

Industry:

- Global transition in the manufacturing base from developed countries to countries like India, China, Taiwan, etc. has taken place over the last 1-2 decades. Global players are not able to meet Indian peer in costing and hence, they are looking for Indian manufacturer to partner with for contract manufacturing.

- China is not interested in manufacturing food colours because of low volume and they are also unable to match the quality as the core focus is on dumping via high volume productions.

- US is the biggest market for food colours. Many large players in the US like Sensient buys intermediate from the market and produces food colour themselves.

- Europe is stringent regarding synthetic food colours but it’s not a very big market.

Size: The world market size for food colours is 50,000 MTPA growing at 8-10%.

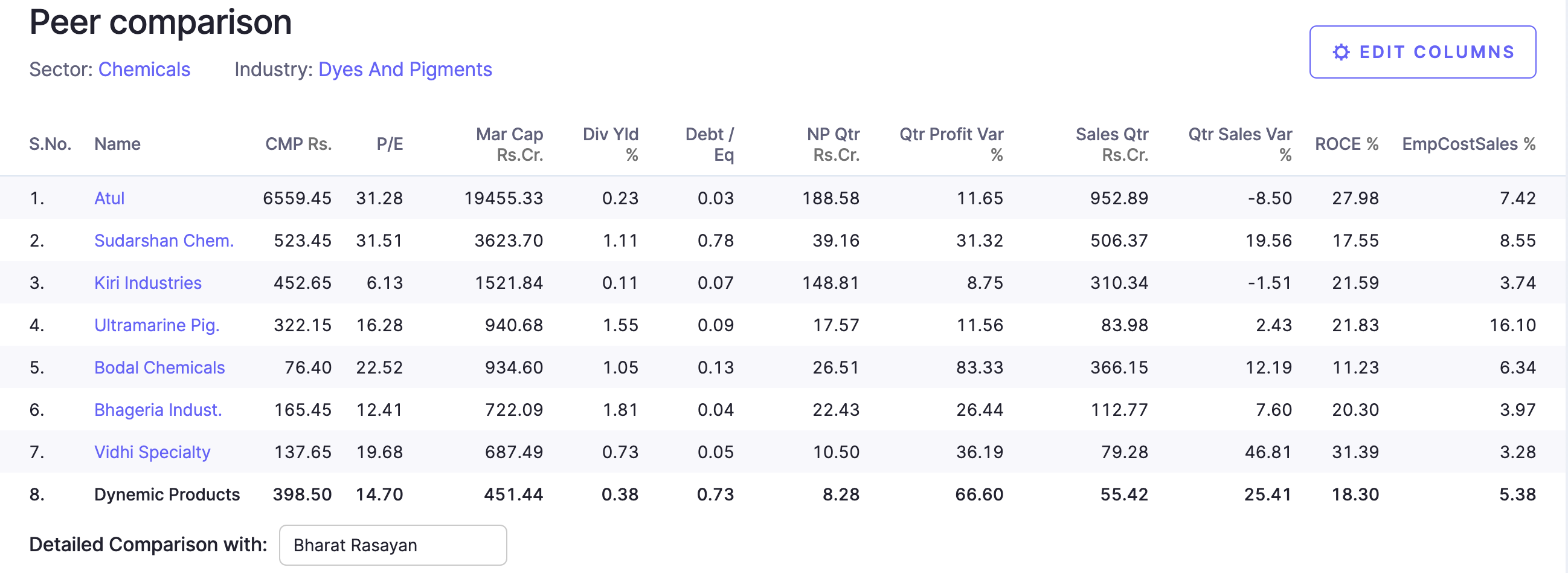

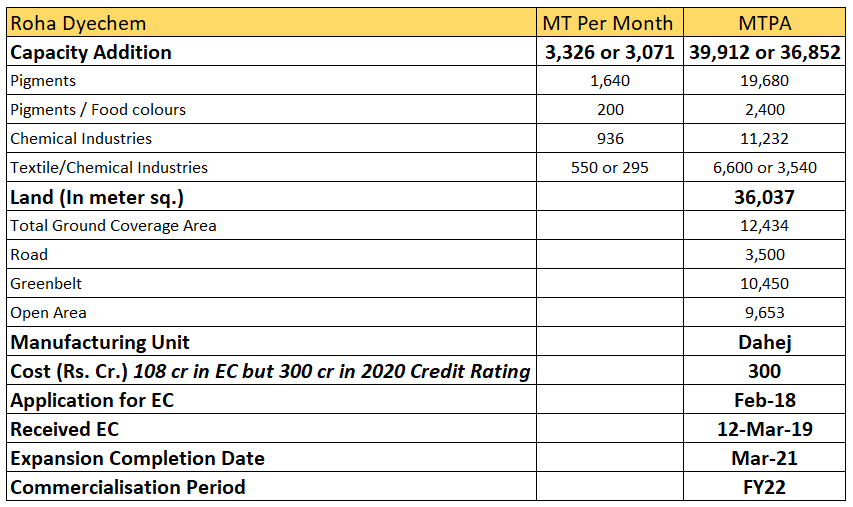

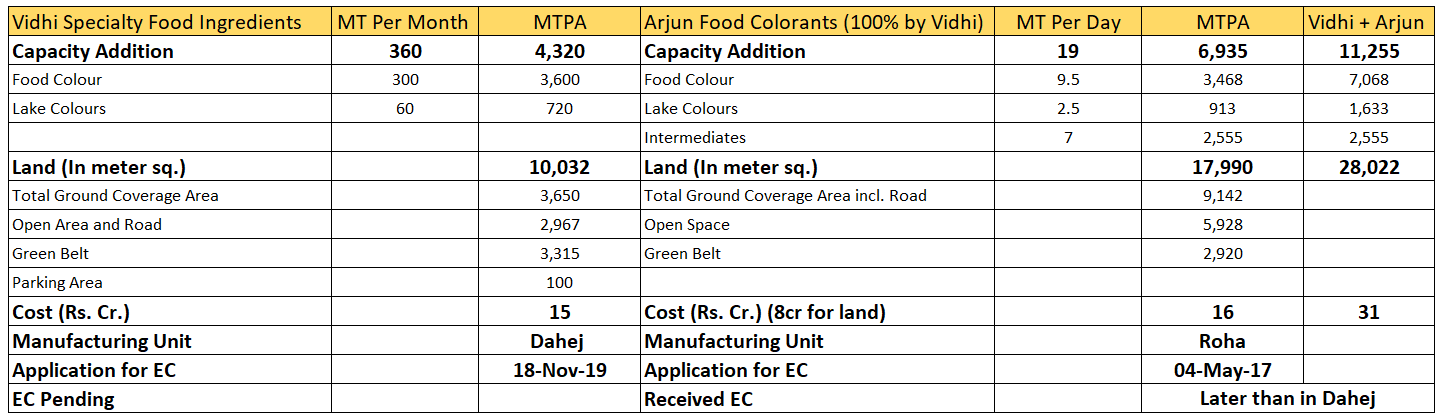

Oligopolistic nature: The industry has an oligopolistic structure wherein a few companies are in the lead with technical knowhow and quality control. Currently, India has three big players in food colours: Roha Dyechem (12,000 MTPA) followed by Vidhi Specialty Food Ingredients (>3,600 MTPA) and Dynemic Products (2,940 MTPA).

Export Oriented and Volume-based Model: Food Colours export market account for 80% of the sales for all three players. All the companies have established distributor networks in foreign countries to sell their products on tonnage basis.

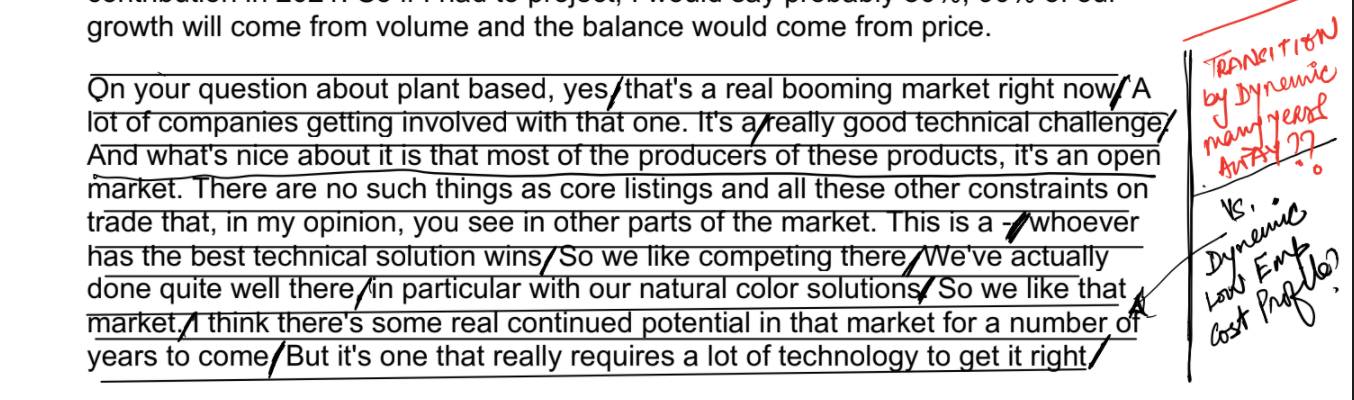

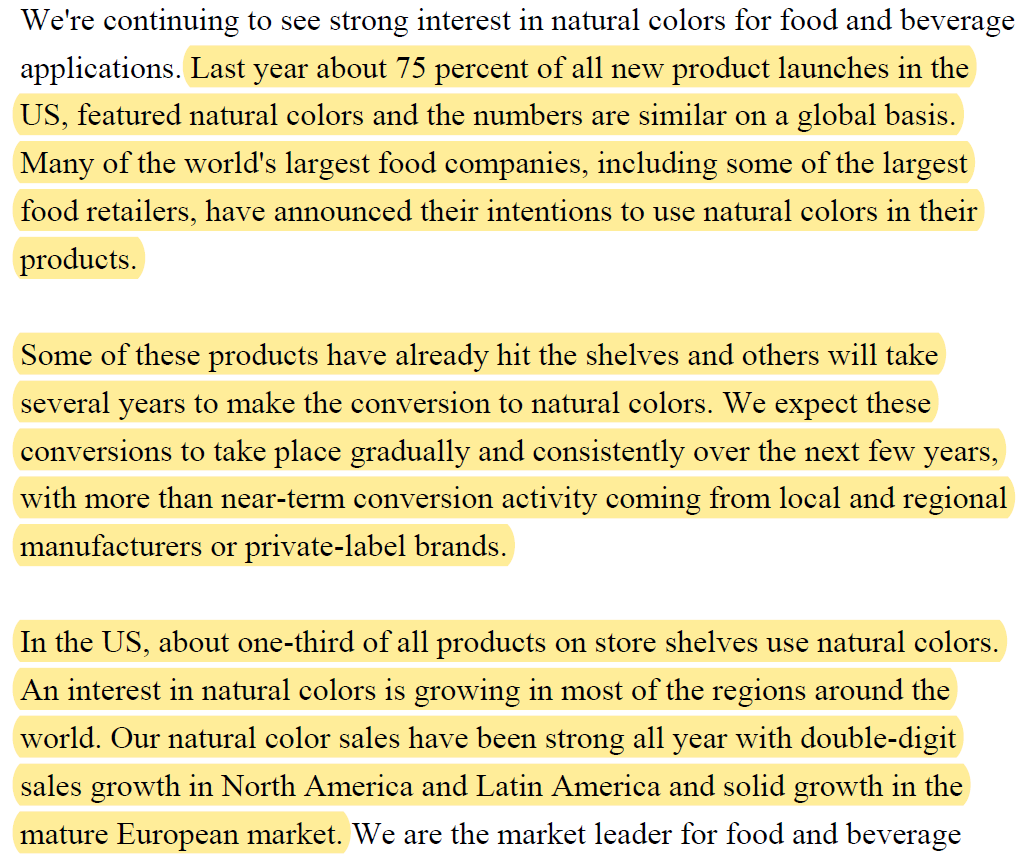

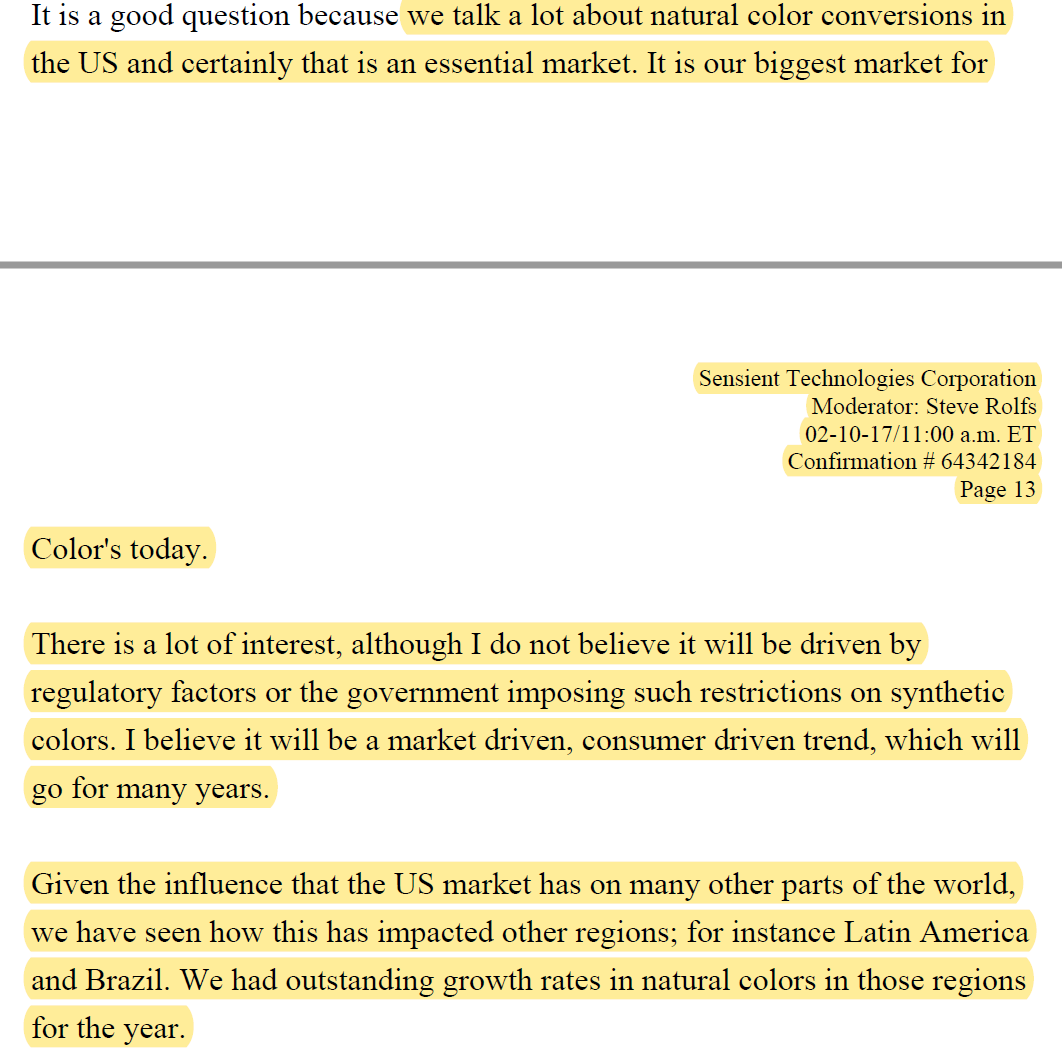

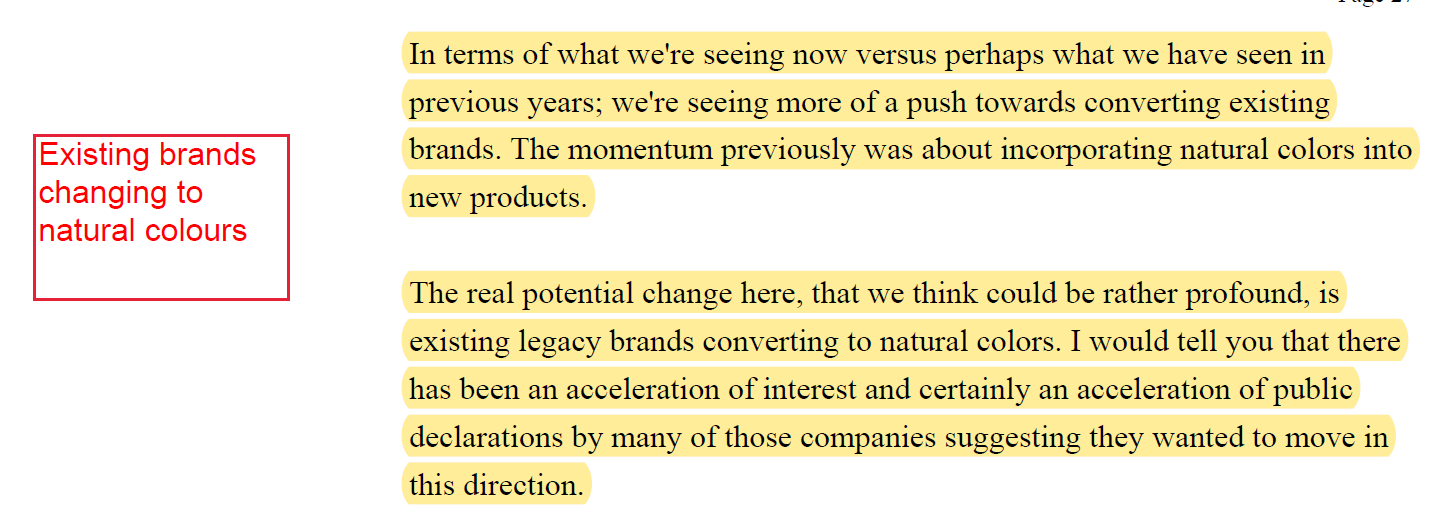

The misconception of Natural Food colours taking over Synthetic Food Colours: Synthetic Colours are perceived as harmful due to which there has been a notion that gradually, natural food colours would take over synthetic food colours.

However, there are certain disadvantages to natural food colours:

- Entire demand for synthetic colours can’t be replaced by natural colours as natural colours are 2-3x more expensive than food colours.

- Any customized colour could be made from a synthetic colour. In natural colours, very limited colour options are available.

- Natural colour doesn’t have stability- can’t last longer more than 6 months.

- As per the management’s experience and surveys, synthetic food colours market would expand rather than be replaced by natural colours. Many newer applications for synthetic food colours are coming which were not prevalent earlier. Hence, the management doesn’t see the synthetic market shrinking.

Promoters:

It is a family run business with founder and promoter Mr Bhagwan Das Patel as the Managing Director of the company. Other members of the family like Ramesh Patel and Dixit Patel are also involved in day-to-day affairs of the company and are whole time Executive Directors. Current promoter shareholding has decreased from 41.53% in June’20 to 35.81% in Sep-Dec’20. It’s because one of the partners, Dashrathbhai Patel decided to get out of the company in 2019 and has been selling shares slowly in the market, some of which has been bought by the promoters in 2020. Reputation of the promoters has been impeccable and they are known to be quite conservative people.

Drivers:

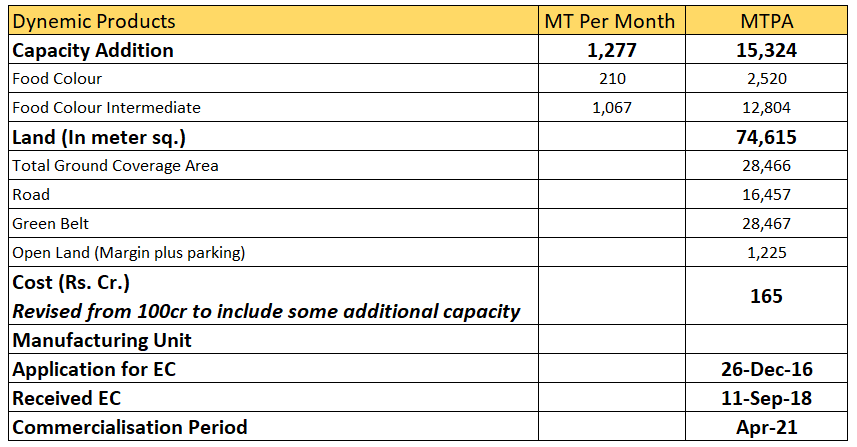

1.Capacity Expansion

The company has two manufacturing units in Ankleshwar, Gujarat and it intends to set up a 3rd unit in Dahej and will undertake expansion by setting up three plants. Dynemic had bought land at Dahej in Feb 2014 for capex of Rs. 9 crores. However, there was a delay in getting environmental clearance. It finally received EC in Sep 2018.

The company, like all industry players, was dependent entirely on China for RM supply. Majority of the capex is done on the backward integration side out of which 40% would be captively consumed and 60% would be sold commercially. Post capex, the company would be almost 100% backward integrated.

Peers like Vidhi and Roha are also doing capex. But, Vidhi’s capacity will take 1-2 years to come on stream and Roha’s capex is largely in pigments segment.

The company has spent Rs. 103 crores already from FY18 to Sep 2020. The total amount of capex up till FY19 AGM was Rs. 100 crores (80% Debt funded). But recently in FY20 AGM, the management has revised the cost upwards to Rs. 165 crores due to various reasons, including the increase in additional capacity, for which I could not get specific details.

The capex was planned to be 80% debt funded (80 cr out of 100 cr). After the increase in the capex, long-term debt is expected to increase from 80 cr to 120 cr. The interest cost is low, given that majority of it is either in foreign currency/ PCFC for bill discounting (acting as a natural hedge towards export sales).

Total potential revenue expected to be around Rs. 550-600 crores within 3-4 years with increased margins.

2.Increased Margins

The last 3-4 years have witnessed really good growth in operating margins ranging from 14-15% to 19-20% with TTM margins being 21%. The management expects an even further improvement and stability in margins due to backward integration.

3.Valuation Comfort

Even after the recent run-up since March 2020, the stock is trading at an EV/EBITDA of 10x with an EV of Rs. 407 crores. Assuming 500 crore sales in the next three years with an EBITDA margin of 22% (taking it this high as the management has always performed precisely to whatever they’ve said in their AGMs over the last 4-5 years) gives us EBITDA of 110 cr which at 9x would lead to Rs. 990 cr EV.

Risks:

1.The capex has already been delayed a lot – first due to consultants in 2015, and then due to Covid and late delivery of equipment in 2020. April-2021 is the timeline we have to track.

2.Dashrathbhai’s stake has been reduced from 12% to 6%. Supply of 6,92,050 shares is going to come in the market. Bhagwanbhai and Rameshbhai’s group bought a few shares in early 2020 but not considerable enough to absorb the selling. Due to this, the net shareholding has come down to 35.81% which is really low.

Queries:

1.Despite such a low promoter holding, the daily volume in the stock isn’t that high.

2.I could not get the specific answer from the company regarding what additional capacity will come on board after the revision in capex.

Disc.:

Even though I tried to make my research as fact-based as possible, I have been holding this stock for close to 2 years, so take my limited opinions with a pinch of salt.

Resources:

ARs – Dynemic and Vidhi

EC Docs – Dynemic, Vidhi, Roha

Credit Rating – all 3 cos.

AGM notes – Dynemic and Vidhi

Conversations with the management