Honda India Power Products - Good breakout on the monthly chart across 6 years and an ATH. Breakouts like this don’t happen unless there’s a substantial business shift in the business. Unfortunately the company doesn’t do concalls or presentations, so the disclosures and ARs are what we have.

The business sells portable gensets, water pumps, general purpose engines, lawn mowers, brush cutters and tillers. Very recently they have also forayed into marine outboard motors (OBM).

There is substantial difference in the way the business is run from 2019 to now. Few that I noticed

-

Termination of JV with Usha International as of Apr 1, 2020 and appointment of Mr. Takahiro Ueda at the helm as President & CEO of Honda India Power Products (HIPP)

-

The above probably shows some change in direction from Honda Motor Co., Japan which is the holding company of HIPP. The way the business is structured and run has undergone a change where the company is getting lot more Export business, expanding its efforts towards localisation of components, introduction of new products, expansion of offline distribution and also building a digital and e-commerce presence (the new website was launched in July) etc.

-

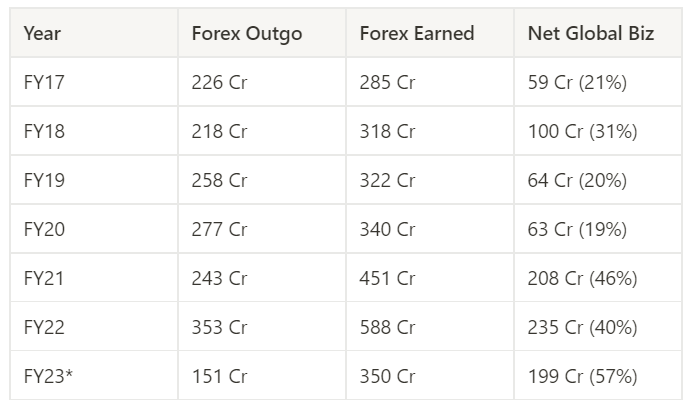

Exports business is one which has substantially changed. Here’s a quick table I made that captures the forex earned and outgo. (FY23 upto H1)

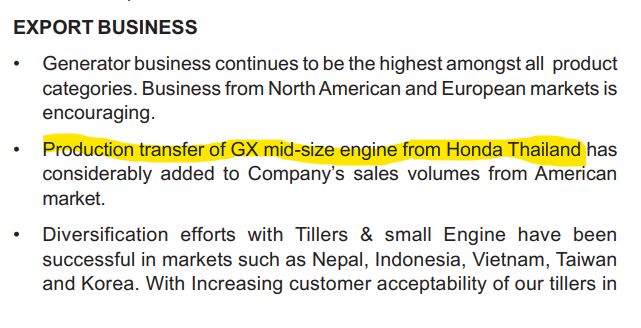

There’s a substantial increase in exports since FY20 (manufacturing shifting from Thailand as per FY20 AR)

and every year there’s an expansion of approved amount for exports (All exports are to related parties of Honda Motor Co. in Amerca, Canada, Europe, Australia etc.). Exports to US currently I think are mainly driven by the General Purpose Motors and the 7kVA gensets. Exports growing at a 25-30% CAGR since Mr. Ueda took over.

-

Important thing to notice is that the RPT for purchases from other Honda Motor Co. subsidiaries also is going up. However, there’s a great trajectory of improving value addition within our borders due to localisation (percentage of outgo is reducing). Outgo will never go to 0, since royalty (6%) and export commissions (8%) will be non-zero. This localisation effort has added 200 Cr net forex in H1 which is 85% of net from last year. My guess is that this could be helping in improving gross margins in the recent quarter where EBITDA margins were at a never before seen 14%.

-

The approval for royalty and commissions in approved RPT as of Nov, indicates topline around 1500 Cr based on approved royalty and commissions (In the past years they have achieved close to this number and in exports even overshot and took a revised approval in AGM for FY22. Approval was for 520 Cr but they did 570 Cr if am not mistaken)

-

I am unsure of market size of export opportunity but I think there’s a lot of cost arbitration to manufacture in India. The EU7000iS is the model we must be exporting to US and its sold there as EU70iS. The price differential is almost 2x. I believe the noise and emission norms there are different so there is perhaps more components that go into the US version but still there is probably a good cost arbitration in manufacturing here. Same is the case with the general purpose motors as well.

-

Its a strong domestic agri (water pumps, tillers, brush cutters) play as well. The marine business is currently dominated by Yamaha and Suzuki engines. The company wants to capture 15% market share in OBD market with their pollution and noise-free line-up of fuel-efficient 4-stroke engines. This could be a play on our rudimentary fisheries, coastguard and recreational boating market. They seem to have sales and service tie-up with Esmario marine to break into this market (YouTube launch video has some info on this)

So if they do manage a topline of 1500 Cr, I believe they could do an EBITDA of ~180 Cr and a PAT of ~120 Cr which could imply its trading at ~22x. Again these estimates could be off but if right, the upside could be substantial. (Also there’s cash of 426 Cr on the books)

Risks:

-

Royalty and export commissions has stayed at 6% and 8% respectively for sometime. Any increase in this could be hard for HIPP

-

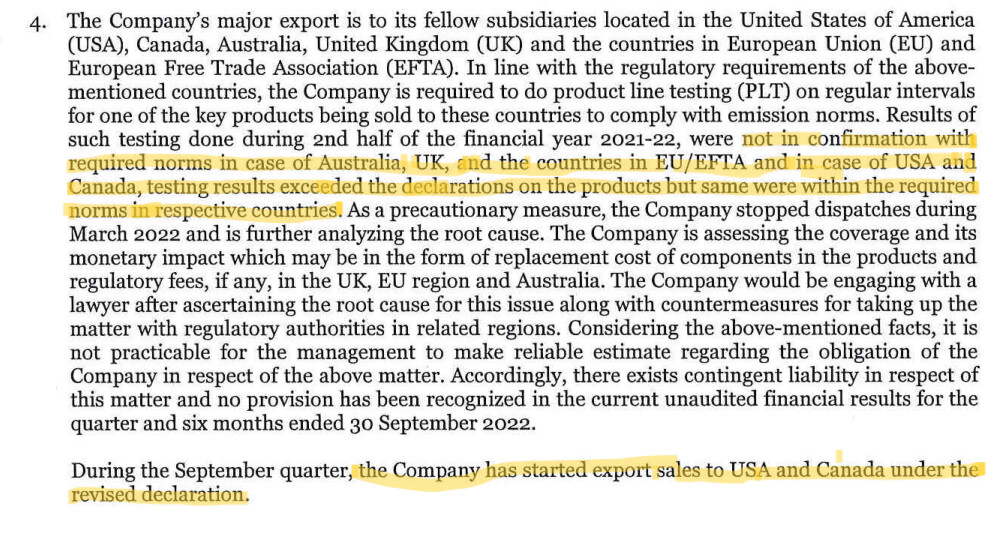

In Q1, some of the company’s exports were found to be not matching declared spec for emission norms. While it does sound big, the exports to US and Canada which are the major destinations (322 Cr of 350 Cr in H1) are unaffected and its only a matter of revising the spec since its still within environmental limits there and the company has already done that and is continuing exports. They seem to be working on the issue so they can restart exports to UK, EU and Aus. (Actual exports in H1 is only ~1.25 Cr to these countries, so they have proactively stopped)

-

RPTs and unlisted subsidiaries are a big problem with MNCs like this. Here too a lot of business is driven by RPTs but the company’s disclosures are stellar on the RPTs which is most of the info in this post has come from. However globally Honda Power Packs (swappable batteries for bikes, ricks) seems to be under Power Products division but in India its a separate subsidiary directly under the Holding Co. While they aren’t into a directly competing business line, merging this business under HIPP will make HIPP a much more valuable company perhaps

-

This company was trading at 1800 or less until last month. Now its almost 40% above that price. The price could go sideways or downwards towards 2200-2400 range which could be a worst case 15% drawdown from current levels. The upside though could be significant if the company executes well and the market sees this as a bit more than a dying gensets business as its perhaps currently viewed.

Disc: Have positions around current levels. I am not SEBI registered and could be very wrong with this thesis. Please do your own research.

UPDATES :

Few additional details on opportunity size.

Looks like Power Products world wide is at 6.2 million units/annum across products (As per Honda Global AR). Indian capacity is at 350k units/year whereas Thai unit is at 2.7 million units/year. That’s almost 8x difference in capacities though both Thai and Indian operation for Honda Power Products started in the mid 80s. Thailand has manufactured 45 million units while we have done only 5 million cumulatively.

Thailand exports 93% of its capacity. So their capacity is completely exports focused and since its 43% of worldwide demand, very likely this derisking of supply chain could go on for sometime and Indian exports could keep rising in the near future.