Linking another post on the comparison and capability of Bluejet vs Neuland in Bempedoic Acid.

2 Likes

I am not an expert at this but the mechnisms by which the two drugs work are different.

Its good to track the efficacy but few things to keep in mind are :

- Obicetrapib increased HDL-C, though this is considered as good cholestrol, however there is no clear indication if it improves cardiovascular health

- CETP based mechanism has historically been inconsistent

- Currently in investigational. For it to become commercial and be an alternate to BA would take at least 3-4 years .

8 Likes

Continuing with the work I’ve done here, here, here and here. Those posts were specifically about Bempedoic Acid. This one is about the Contrast Media side of the business.

BlueJet supplies contrast media intermediates to 3 of the top 4 CM majors that hold 75% market share (GE Healthcare, Bracco, Guerbet). Bulk of the revenues today though come from ABA HCl. However, the company is doing few things

- Backward integrating into APD

- Forward itnegrating to make Iodinated HCl

- Getting into Gadolinium based intermediates - for an NCE (Gadopiclenol) for Guerbet and also a base intermediate

The most detailed of reports I have seen on BlueJet is this from Sanjesh Jain which is phenomenal. I am going to be borrowing some of the data from this. Giving credit in advance.

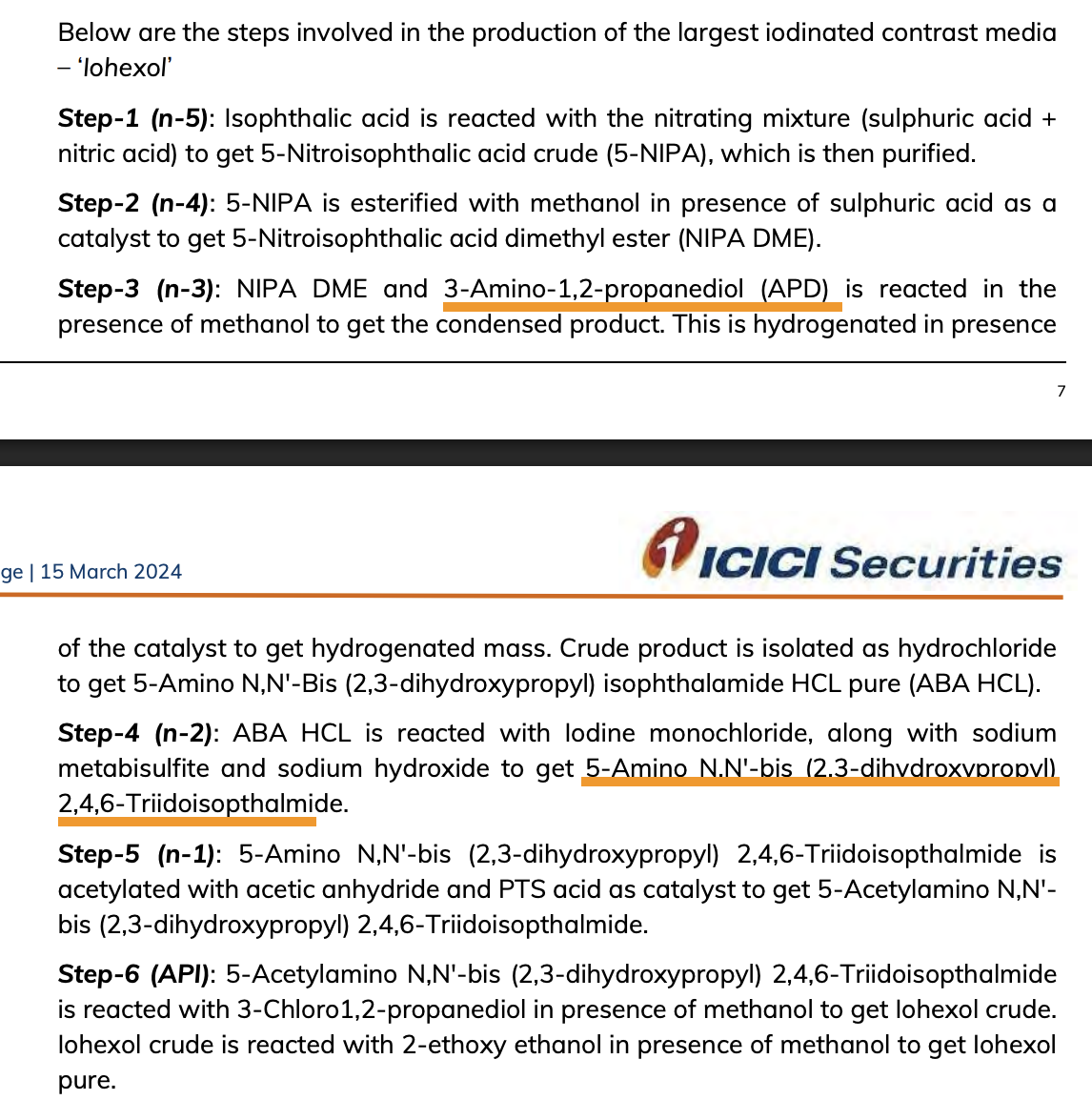

1& 2. ABA HCl (intermediate used in iodinated contrast media like iohexol) has contributed to bulk of the topline for BJ in the past. Still continues to be the case but its dramatically reducing in recent quarters as BA grows.

The quantity has remained more or less constant at around 3million MTPA. However, the use of most crucial RM used in the manufacture of ABA HCl, which is APD, has declined steadily over the years possibly due to improvements in yields - but the margins have been at the mercy of APD prices which vary between $7 to $9 or so roughly.

This is the entire value chain from the ICICI report

BJ does upto Step-3 at present. In this now, BlueJet is now backward integrating into APD which has been a pain for its margin stability and Iodinated ABA HCl which is one step ahead in the value chain.

How does this affect margins? This snippet gives a good idea

Imagine doing 16x value addition in-house! The other interesting thing I learnt is that iodine chemistry is very expensive due to Iodine prices and so if you manage to do it large scale, you get two advantages 1. You get to tie up with cheap supply of Iodine (BJ has tied up with SQM, a mining company in Chile) 2. You improve processes for recovery of Iodine which is better done on large scale. Both these make you very cost competetive in Iodinated ABA HCl (fwd integration). APD backward integration makes you unbeatable in ABA HCl. Combine both and you have the lowest cost producer catering to bulk of the world’s demand of the product to a niche industry dominated by a handful of players. (Divis is attempting to enter this business and has imported its first shipment of APD, just as BJ is backward integrating into APD).

- The Gadolinium intermediates (Cyclen and BGB) will cater to 24% of the total contrast media market. In this Cyclen is a basic building block of Gadolinium contrast media and will be supplied to the top 3 while BGB is used specifically in gadopiclenol and will be supplied to Bracco and Guerbet (they have a tie-up to market the product together under separate brands).

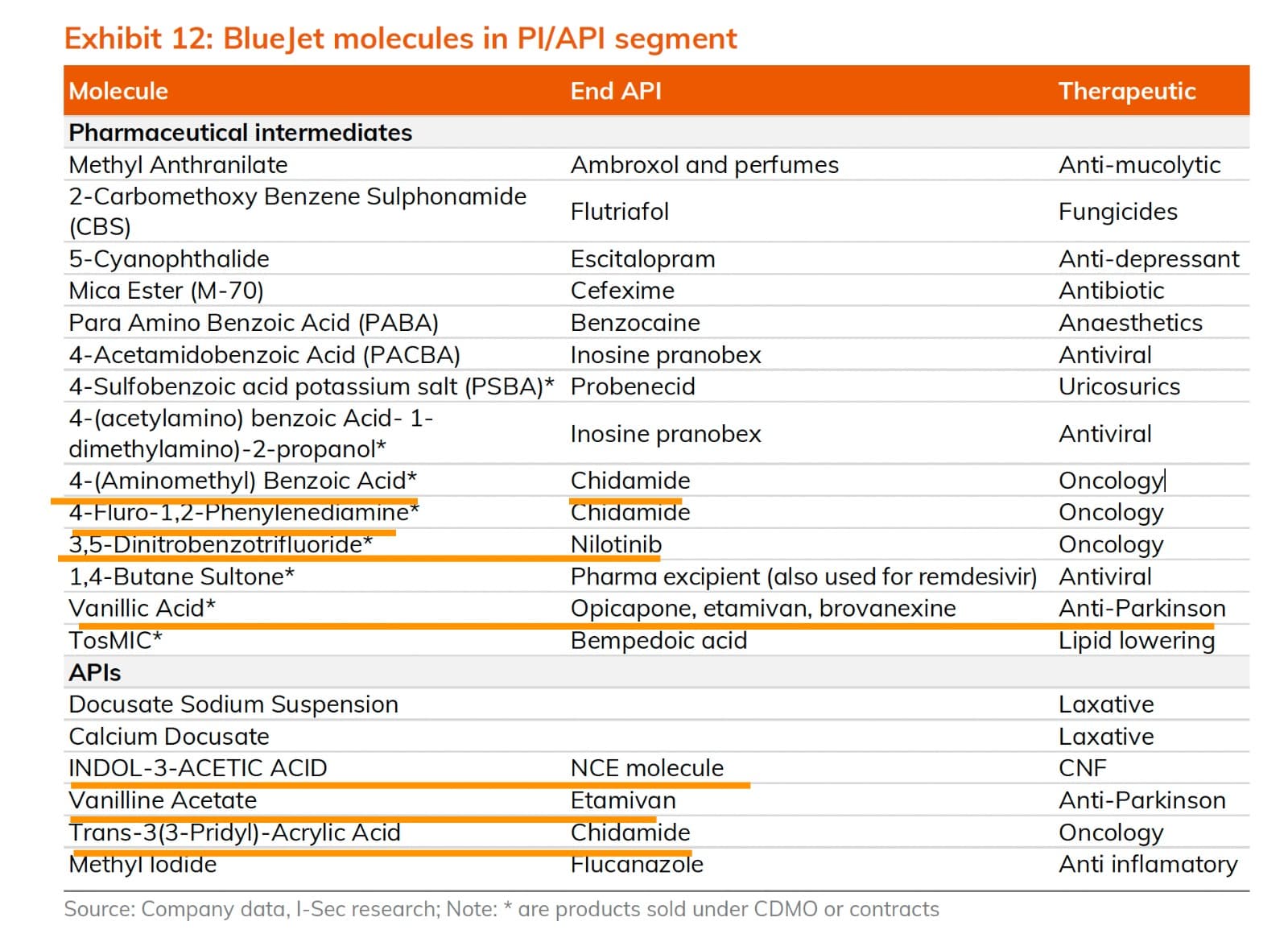

To me it looks like BJ does few things and does them really well. It will probably even do TosMIC backward integration when Bempedoic Acid volumes stagnate in the future (my speculation).

Other than the BA, there are few other pharma intermediates as well which sound promising - mainly the Nilotinib intermediate which is used in chemotherapy for Chronic Myeloid Leukemia (Novartis drug).

Like its expertise in 5-NIPA, they also seem to have an expertise in dealing with Vanillic Acid based intermediates which are mainly used in CNS therapies. IAA (Indol-3-Acetic-Acid) also appears to be a very high value molecule. Not sure what this NCE being referred to is. They seem to be shipping this to a subsidiary of Thermo-Fisher Scientific. Some of these might turn out big as well in the future but needs further work

Disc: Invested

55 Likes

I am trying to understand how the investors are viewing this company. Is this a trade where one can expect 2-3 good qtrs or is there a structural story that can play out here beyond a few quarters

-

The numbers that we are seeing right now is a function of inventory build by the innovator. Usually periods of such build up are followed by lesser procurement numbers. How are we asusming the sustainability of the exports we are witnessing right now?

-

Favera seems to be possibly beniffiting as NEulands capacity hasa peaked. I would assume NEuland is a primary supplier due to its old association with this product. Even if this isnt true, Neulands capacity ramp up by 3x should have some impact on bluejet as well?

-

What beyond? Sweetners is an avg business. While contrast media is decent margin , it will not grow exponentially, impact of peers coming in anyway has to be seen. What do they have beyond bempodoic and a few qtrs of growth after which base readjusts, neulands capacity comes in and inventory pile up normalises? How are we valuing a 450 odd cr PAT that may not be sustainable?

13 Likes

In my very humble amatuer opinion, I think it’s impossible to get more than maybe 1 FY future earnings visibility in the pharma businesses for Indian companies.

At least an innovator pharma company has a patent so there is some visibility on earnings till patent expiration. Plus, you can use the option pricing model to value the company’s pipeline of drugs under R&D using your own subjective judgements of probability and degree of success of each drug in the pipeline.

For CDMO companies, there are no patents and there are usually no long term contracts. Innovator companies can “shop” around every few years and this is field of fierce competition (as evidenced by Neuland and Favera coming up as competitors for BA and its intermediates, plus who knows who else).

To maintain high earnings over a longer term, say 7-8 years there are probably 3-4 cycles of where the pharma company finds its big earners ramp down and hope that a new big earner comes up. So really, investing long term into the pharma space is pretty much a bet on promoters. It’s more faith than analyses.

If there is any sort of strategy to be followed here, its probably to value the company at its core businesses only (for e.g. in Blue Jet, it would be sweeteners and contrast media) and invest whenever the price declines to close to that value.

For me, as tempting as the whole CDMO sector is - after lots of analyzing and thinking, I am staying clear.

Disc - Not invested

21 Likes

Two things I found recently. One on Gadopiclenol scope and another on TosMIC backward integration possibility.

Gadopiclenol (for which BlueJet supplies the intermediate BGB - or ButylBromoGlutarate) was approved for sales in US in Sept '22 and in Europe in Dec '23. It is sold by both Bracco (as Vueway) and Guerbet (as Elucirem). Currently Guerbet manufactures for both as per their agreement.

Bracco has already reached 1 million injections in the US alone.

The link also mentions that the Gadolinium dose is 0.05 mmol/kg. We can do some back of the envelope calculations. For an avg. person weighing 70 kgs, we would need

0.05 mmol/kg x 70 kg = 3.5 mmol of gado per MRI. Considering the molecular weight of 970.mg/mmol, this works out to

3.5 mmol x 970 mg/mmol = 3395 mg or 3.4 gms of API per adult per MRI.

In terms of formulation, the injection is available in different formulations

Very likely, something like the 3rd bottle would have ~3.5 gms of API and would be the one sold mostly.

The manufacturing process is patented (filed by Bracco). The first thing that comes to mind is that the amount of gadopiclenol at 3.5 gms is quite high (to compare, bempedoic acid as per earlier calculations was 5.4 gms for entire year!). So this is very high volume drug when compared to oral tablets. This also means the amount of intermediate used will be equally high (Not proficient enough to work that out from the patent doc). The value of BGB seems to be $50/kg. The current installed capacity (120 MTPA as per EC) should contribute to around 50 Cr per year (ABA HCl sales is ~400 Cr/yr, so this isn’t a bad start for a new NCE in year 1). The run rate as per exports is already at 6 MT per month.

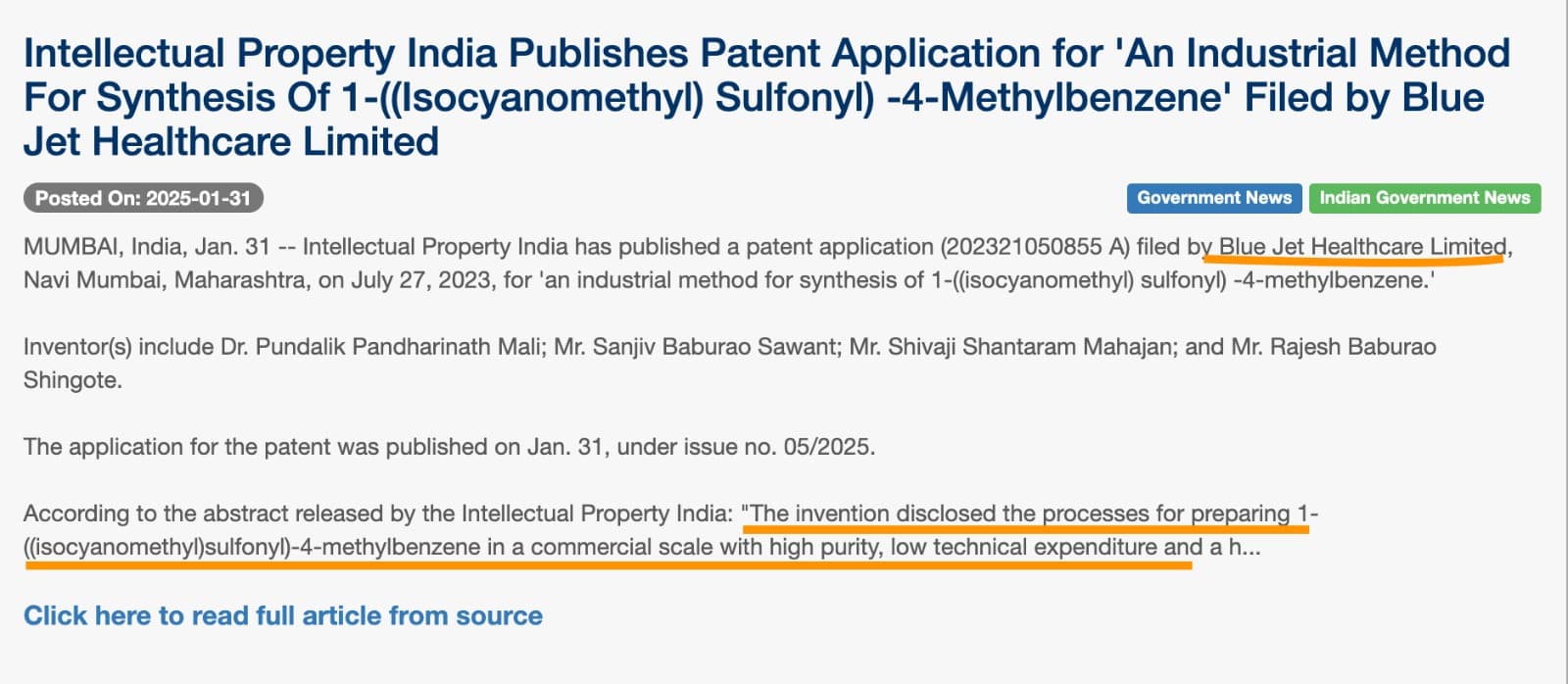

The second thing - @GourabPaul found a BlueJet patent on TosMIC manufacturing. I had speculated that this was a possibility in my previous post.

The patent seems to have been granted on 31st Jan '25 (filed in July '23)

TosMIC backward integration should be highly value accretive and should make BA very cost competetive for BlueJet and we should look out for any announcements of capex for the same.

Disc: Invested

56 Likes

i was researching about bempedoic acid and as per my understanding esperion has patent till 2031 right ?

how are so many generic companies making it ?

edit : figured it out , they have no patent in India

6 Likes

Few points from Emkay call:

- Bluejet is going to supply sacharine to Coke which can give 20% growth in the sweetner’s business

- The patent for TosMIC: the company used to manufacture the product, but they had fire incidents, and therefore it seems the company has taken a call to not manufacture, but buy it

- The US innovator: they received funding from a Canada fund (i think the analyst mention a that it was a Pension Fund), wherein the royalty income from Europe sales will be given to the Canada fund, and this in turn the funding solves for innovator’s financial situation

- Piramal Pharma currently manufactures the medicine, once Diachii takes over the manufacturing there is a risk in Bluejet’s earning from the Bempedoic Acid

Sharing the IC report of Emkay for everyone’s reference

BLUEJET IC emkay mar25.pdf (3.3 MB)

Disclosure: not invested

28 Likes

The UK has a government funded healthcare system which transparently publishes spends on all kinds of medication over the years. Using this dataset can be very rewarding to understand real life examples of how new treatments replace the old, how guidelines affect prescriptions, competition between different treatments, and growth trends for new molecules.

In the context of BlueJet and Neuland, this dataset gives insights into the growth and adoption of bempedoic acid, shows how sparingly the expensive PSCK9 inhibitors are used, and emphasizes just how important guideline revisions are for new age treatments.

The punchline is that Bempedoic acid has been growing in three digit CAGR, but satisfyingly, we also know why it is growing this fast, and what it means for the upcoming triple combo from Esperion.

Credits to @phreakv6 for all the charts made from the dataset.

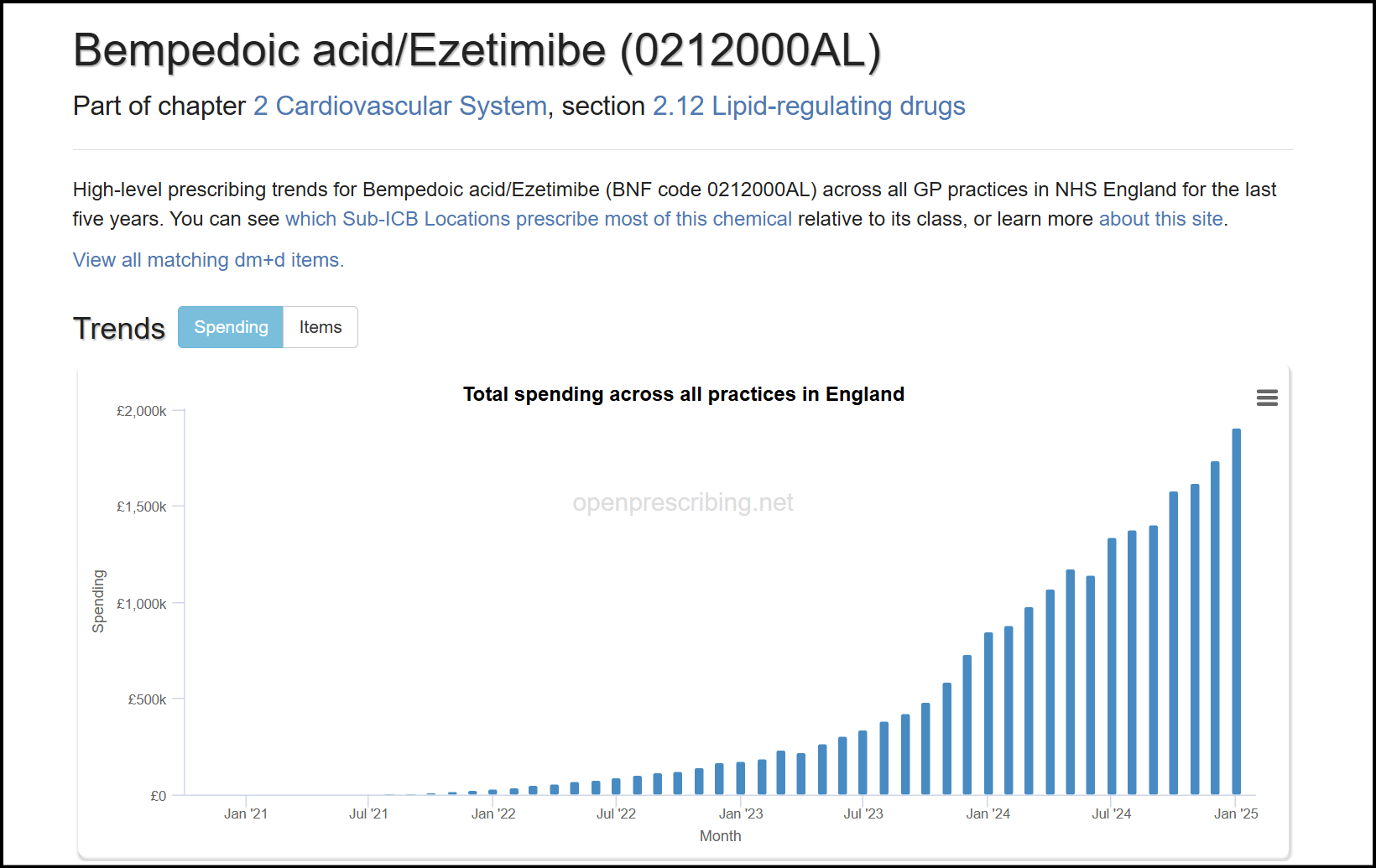

Statin Market and Ezetimibe Trend

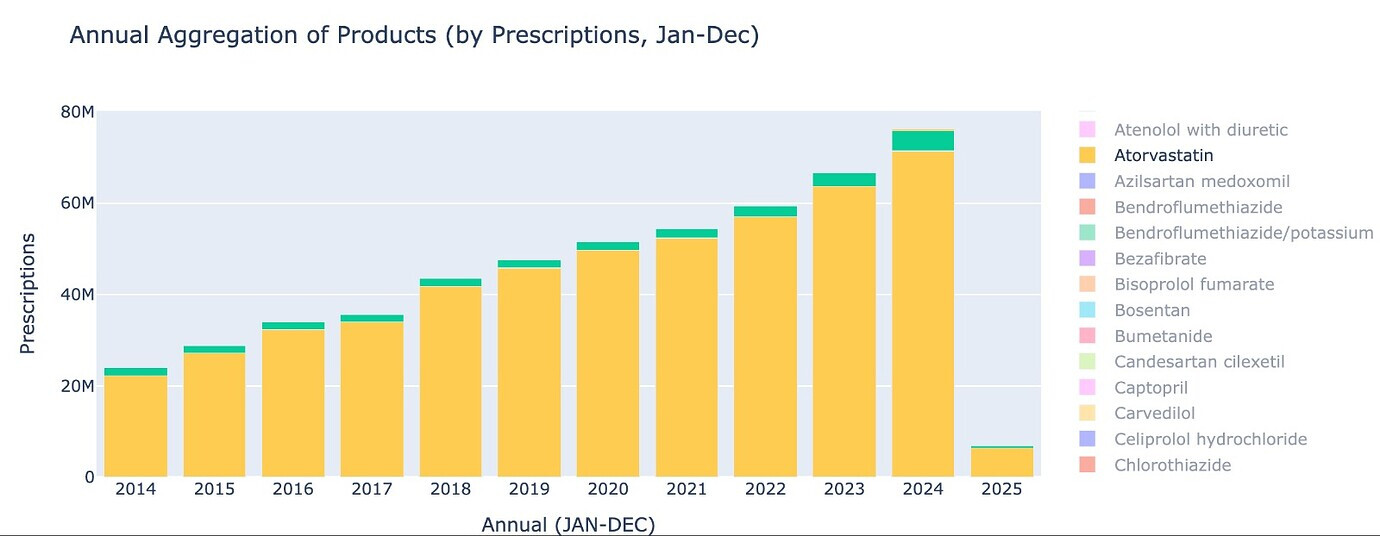

The primary cholesterol lowering treatment in the UK is Atorvastatin. As of Jan 2025, around 6.3 million prescriptions of Atorvastatin were dispensed, roughly ~10% of the population. This market is growing at around 10% CAGR, and Atorvastatin is the most prescribed drug in the UK.

Ezetimibe is a drug used often in combination with statins to lower cholesterol. The surprising find from the dataset is the sudden increase of Ezetimibe usage in 2023. From 2014-2022, there has barely been any growth in Ezetimibe usage, and then a sharp uptick in 2023 and 2024. It’s important to understand the role Ezetimibe plays to appreciate why Bempedoic Acid has scaled successfully.

This sudden growth is completely attributed to a revision in the UK’s NICE guidelines, and an updated stance on Cholesterol.

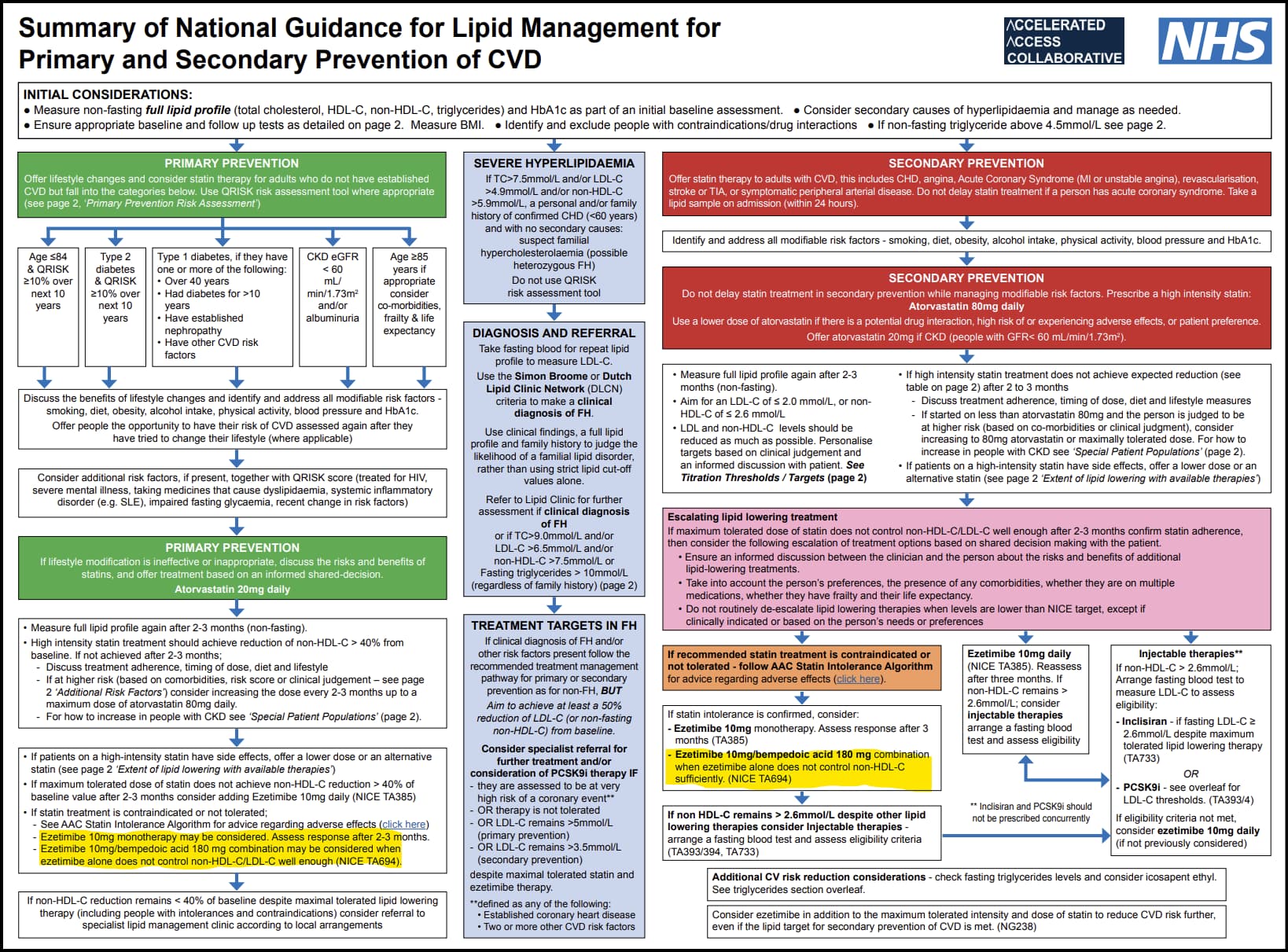

NICE Guideline Revision

Until 2023, the UK had been more lenient with cholesterol targets than peers in the EU, and this drastically changed in the 2023 guideline revision. The UK decided to treat cardiovascular disease more aggresively, and nip risks in the bud by managing targets in adults early.

This revision explains why Bempedoic Acid has picked up, when PCSK9 inhibitors are used instead, and the stronger stance on cholesterol lowering.

-

On Ezetimibe: The new guideline significantly broadened the scope of Ezetimibe, from being a second line treatment, to an addon treatment for people with cardiovascular disease. They also prioritised lowering cholesterol over cautious use due to cost. As a consequence, more frequent use of Ezetimibe.

-

On Bempedoic Acid: Instead of leaving treatment purely to the judgement of doctors, the guidelines clearly state that statins are the first line of treatment, and in cases where patients are statin intolerant (statins infamously have side effects of sickness, muscular pain, etc), prescribe Ezetimibe, and Bempedoic Acid + Ezetimibe when Ezetimibe alone does not lower cholesterol sufficiently. The corollary is that Nustendi (BA + Eze combo) should see faster growth, and more market share than BA alone. Sure enough,

Note Bempedoic acid and Ezetimibe are given both as primary prevention (those without CVD) and secondary prevention (those with CVD).

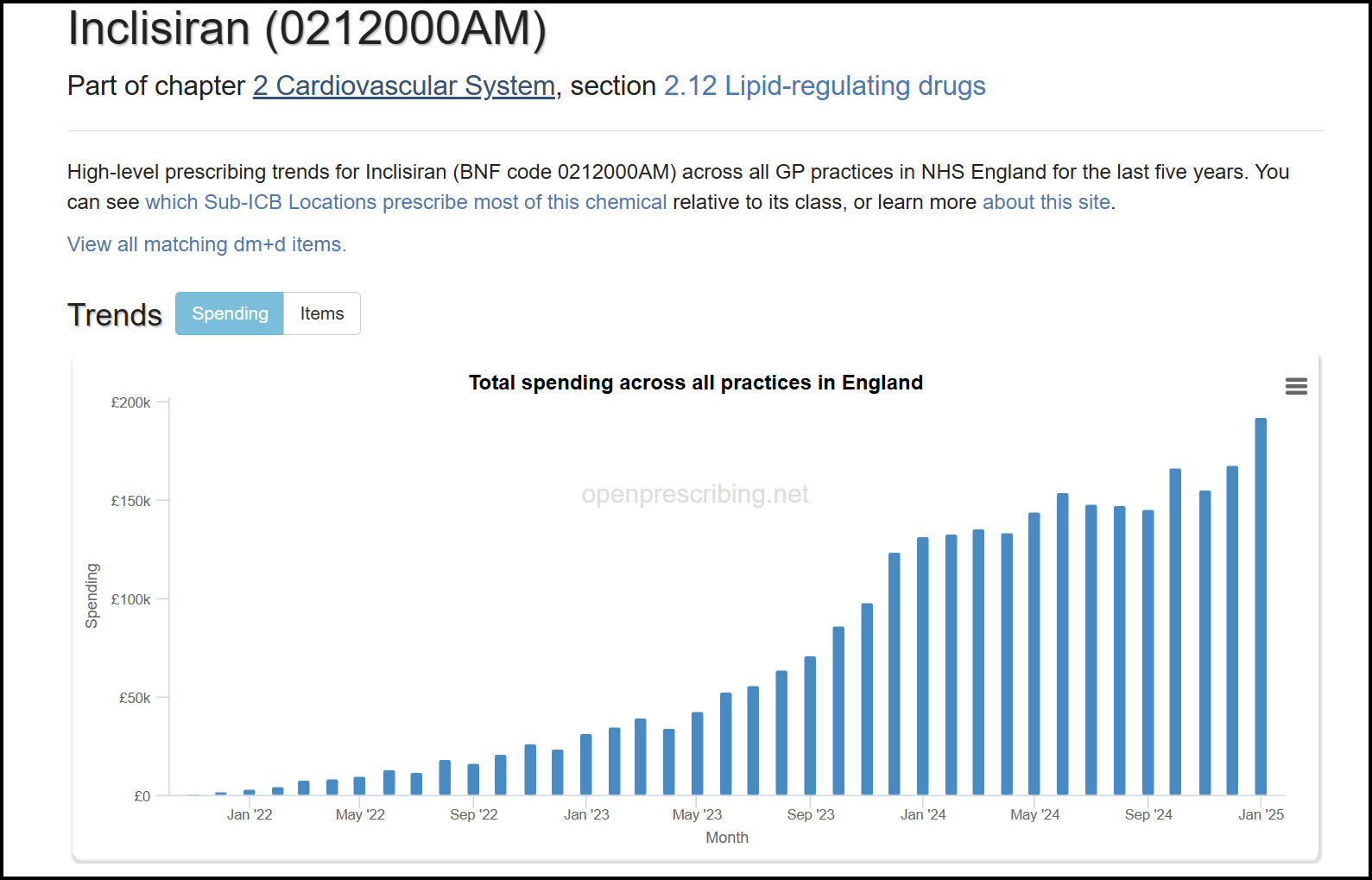

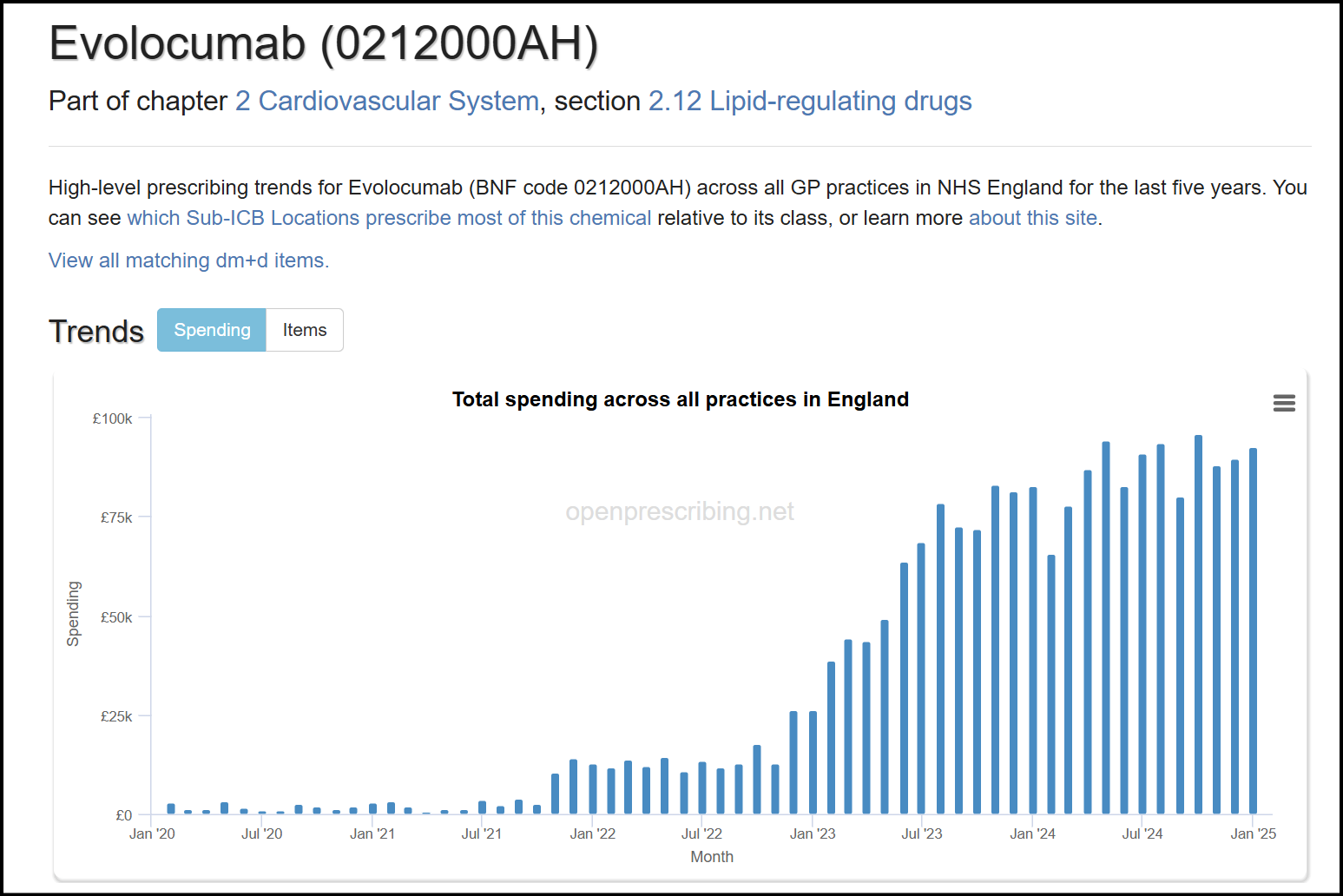

- On PCSK9 inhibitors / Inclisiran - these are injectables that can lower cholesterol, and are competitors to bempedoic acid. From the guidelines, it is clear these are the last line of treatment, when all else fails. Guidelines also state the use of PCSK9 explicity only for secondary treatment So only if patients are on the highest dose of statins / Eze / BA + Eze and still don’t meet cholesterol targets, then they are eligible for PCSK9 / Inclisiran. From this, the market share of PCSK9 inhibitors / Inclisiran should be the lowest among the molecules discussed.

Sure enough, by value, Inclisiran is 10% of the BA/Eze spend:

The PCSK9 inhibitors are even lower:

- The data also tells us that all statin intolerant people have taken Ezetimibe (but not all people on Ezetimibe are statin intolerant). Therefore, if you divide the number of people on Ezetimibe by the number of statin users, this is an upper bound for statin intolerant patients. Based on the UK data, the upper bound is 6.6% of statin users are intolerant. Bempedoic Acid has around 30,000 monthly prescriptions in the UK, compared to around 450k Ezetimibe prescriptions, and can further eat into this market.

Looking Ahead

-

In the US, the American Heart Association have updated guidelines in 2025, and mention BA as an option for statin intolerant people. Real world learnings from UK data tell us that guidelines significantly affect prescription behaviour, and an inclusion in AHA guidelines means more confidence for doctors to write prescriptions, and can be used to influence insurance providers.

-

Esperion is working on a triple combo which includes bempedoic acid + ezetimibe + atorvastatin. This triple combo achieves much better LDL lowering (~60%) and can eat into Ezetimibe’s market share, and a portion of the statin market: those that are on the maximal dose of statins and don’t meet LDL-C targets. The triple combo is to be launched in 2027, meaning API stocking should start in 2026.

Access the dataset here: Bempedoic acid: BNF Code 0212000AK | OpenPrescribing

D: invested, biased. No recent transactions.

55 Likes

On going tiff between US and Canada and while this may or may not happen but Mr Trump beating on bringing pharma back to US (Psychological impact) and looming tariffs, can this impact bluejet business?

1 Like

Tax Demand of Rs 193

Blue Jet Tax Demand.pdf (323.6 KB)

1 Like

Equals almost full year profit, they are contesting backed up judicial precedents, but for sometime it can take a beating

3 Likes

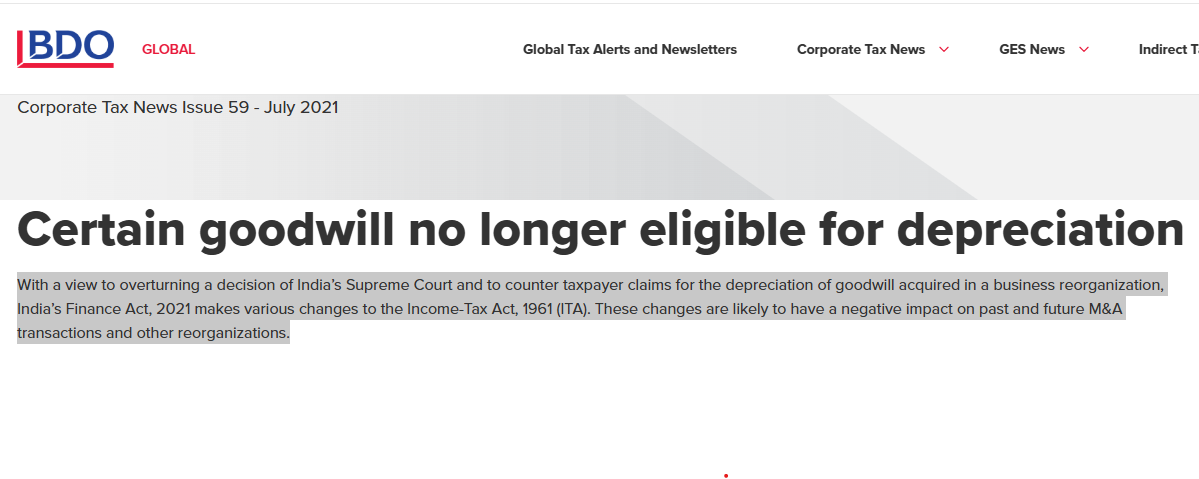

Good luck to the company. The Supreme Court decision to allow depreciation on goodwill was overturned by amending the Finance Act. Source: INDIA - Certain goodwill no longer eligible for depreciation - BDO

Disc: Not invested

4 Likes

The demand for the above years is essentially on account of disallowance of depreciation on goodwill in the Assessment year 2020-21 and disallowance of subsequent set-off of unabsorbed depreciation allowance.

I think change in Tax Structure came effect from Apr’21

2 Likes

As per company press release they have already provided for tax amount on conservative basis except for interest and penalty.

2 Likes

Thanks @Chins for the post on prescriptions and guidelines. My fav chart has to be this

Statin market itself is expanding at 10% on such a huge base of 60m prescriptions in just UK and non-statin market is only 6% of it (used to be 4.5% 2 yrs back). Non-statin market will get to 10% of statin market over next 3-4 years. And though Ezetemibe has 2x-ed over last 3 years - BA+BA/EZE has grown over 6.5x. So we have a category that is expanding and a sub-category that is expanding faster and BA expanding leaps and bounds within that.

So far my research into CDMO space led me through dosage, dosing frequency, prescriptions, unit cost, API cost, capacity, stoichiometry, yields, operating leverage etc. There is one more crucial bit to be added to this, especially when it comes to US market, which is the insurance landscape.

I have been doing some work to understand this in some detail, so will present what I have found. Its not particular to Bluejet but posting here since that’s what got me started on this journey.

In the US, there are 3 types of coverage for drugs -

- Medicare part D. (20%)

- Medicaid (20%)

- Pvt insurance. (60%)

In this Medicare part D and Medicaid data is public. You can look at prescription data, the way UK NHS provides - but with an unusable 2+ year lag (latest data is from 2022). However, the insurance coverage for drugs data is updated monthly!

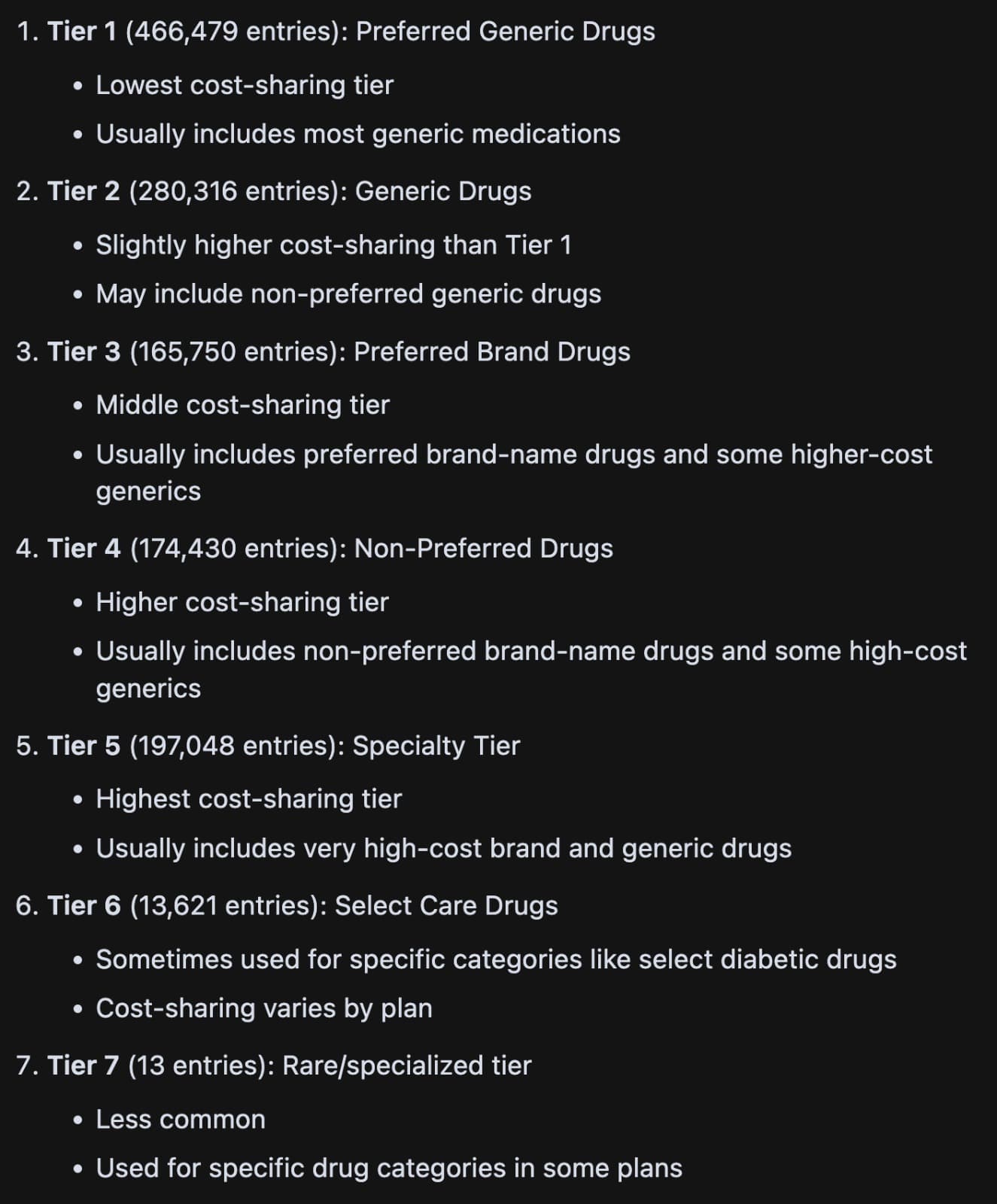

This would give us a fairly good idea of how the drug is covered by various formularies (simply a combination of drugs, which is attached to plans). There are however some basics about US insurance plans we need to understand. Drugs fall under different tiers from Tier 1-7.

Tier 1/2 are for generics. Tier 3 for branded drugs (cheaper ones like BA). Tier 4-7 are for expensive stuff - like Nubeqa, Cobenfy etc.

There are other modalities that insurance companies (payers in US parlance) use to control spending (Utilization management in their lingo) - they use something called “Prior Auth” (you need authorization from payer before you can prescribe - so doc’s office has to do some paperwork for this if set to “Yes” in the plan for the drug) and “Step Therapy” (Try a cheaper generic or cheaper branded drug before using this drug). They also have Quantity Limits (like 28 max for most pills, to ensure patients dont overdose)

I did some number crunching of the data available here

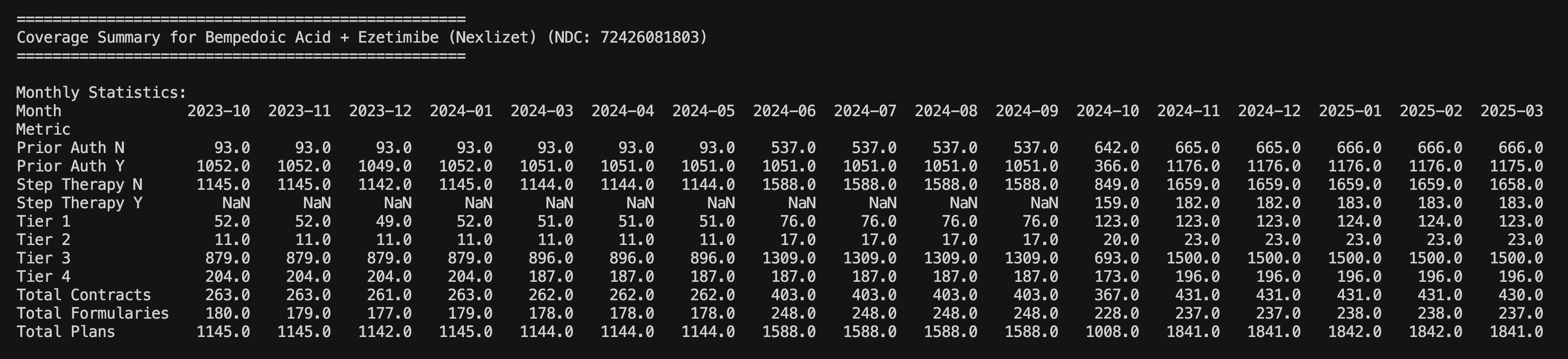

This is how it looks for Nexlizet

What’s nice to see is that post label expansion, the number of plans covering the drug has gone up from 1100 to 1800 levels today. Also % of plans which did not need “Prior Auth” (Prior Auth N) was < 10% before label expansion but is today > 30%. Although they are in 1800+ plans, this is still only around 50-60% of total plans (3600 odd). They don’t even have coverage across insurance companies (Total contracts is 430/725). So there’s still scope for them to expand coverage though they have managed to expand a lot since May. You can also understand seasonality in Oct '24 that ESPR management talked about as there was lot of rejig in plans that led to loss of sales.

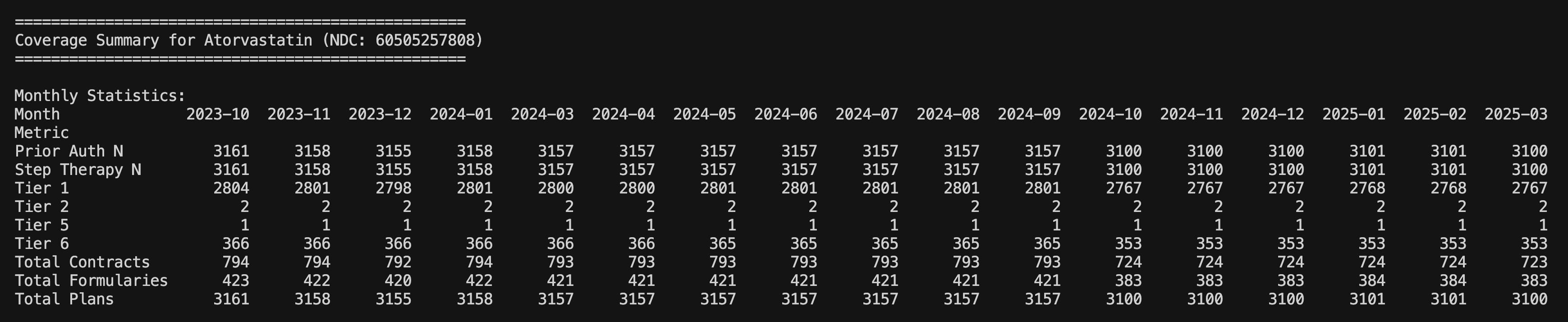

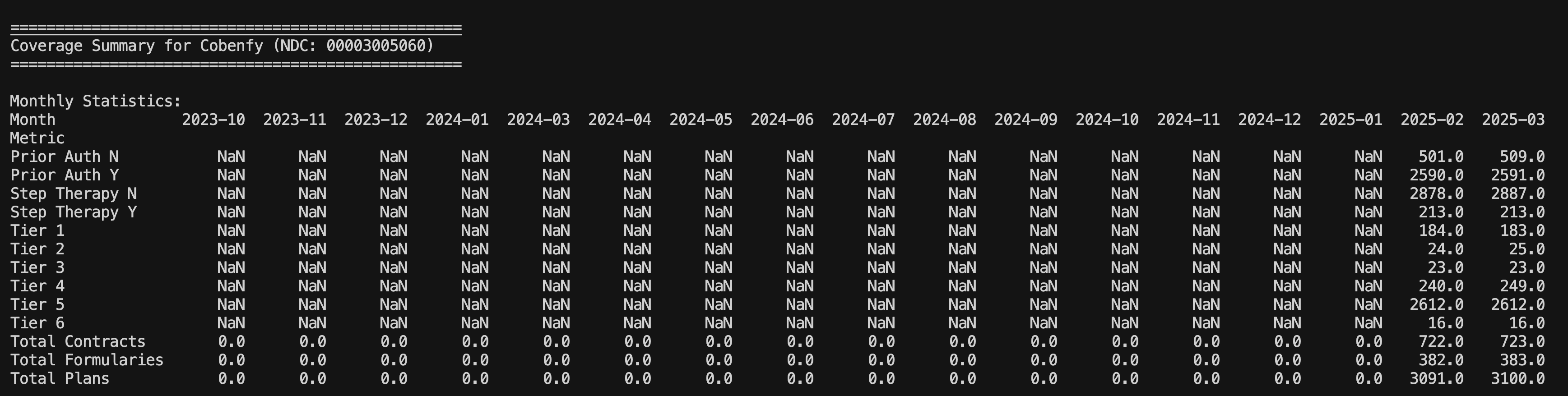

A look at few of the other drugs of interest

Atorva as can be seen is present in 3100 plans and all of them are almost in Tier 1. There’s no Prior Auth or Step Change required (its the first line of treatment)

Cobenfy is the schizophrenia drug Neuland is supplying API for. BMS has managed to get the drug in 3100 plans at launch! This is the muscle of a large pharma company. However, its worth noting that its all in Tier 5 and a lot of them need Prior Auth.

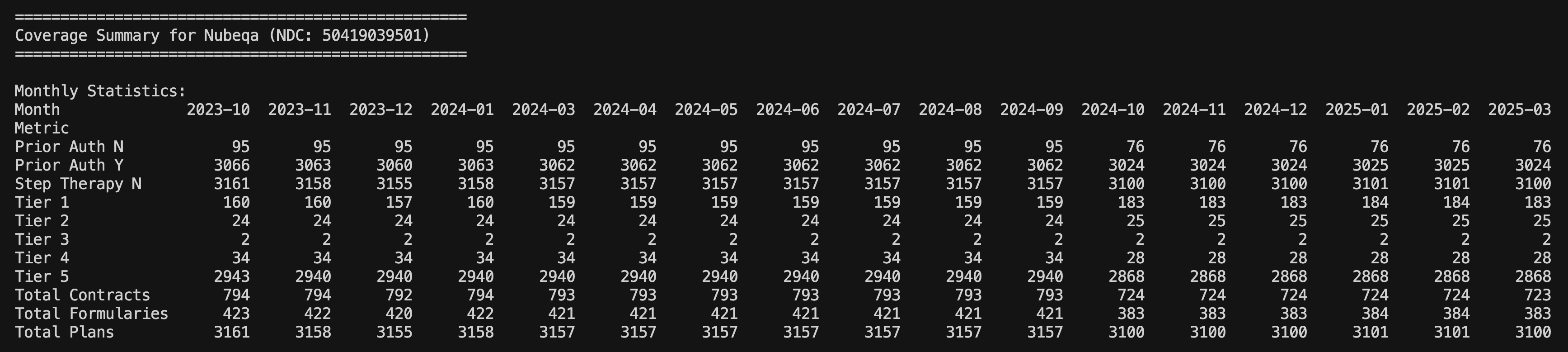

Bayer’s Nubeqa as well has the muscle in terms of number of plans but being expensive, almost all of them need Prior Auth and its in Tier 5.

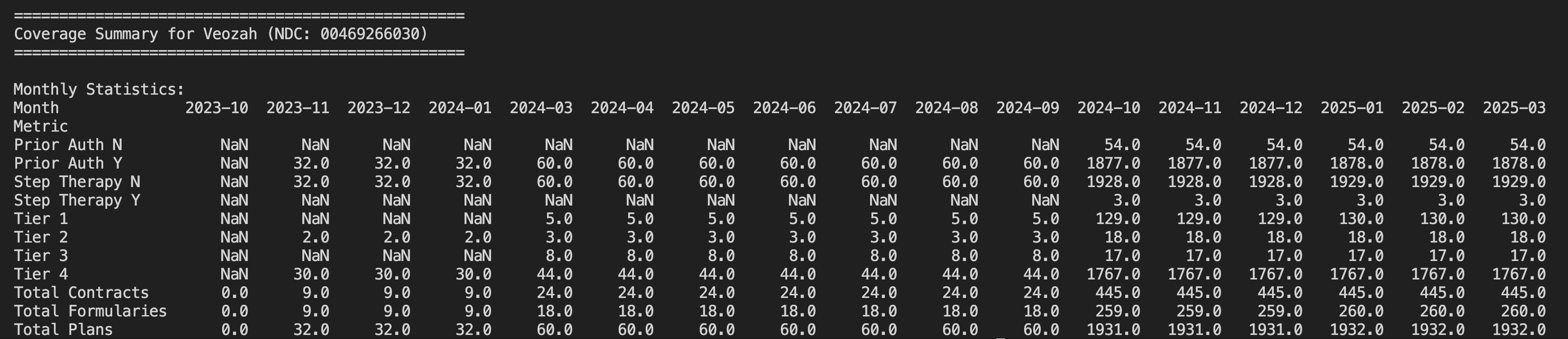

Veozah - This is competitor for Elinzanetant (Aarti supplies intermediate for). Its very clear this company also is like Esperion and has Okayish coverage only for its drug which is why it didnt do so well yet. (Bayer might be able to muscle through better as they did with Nubeqa perhaps)

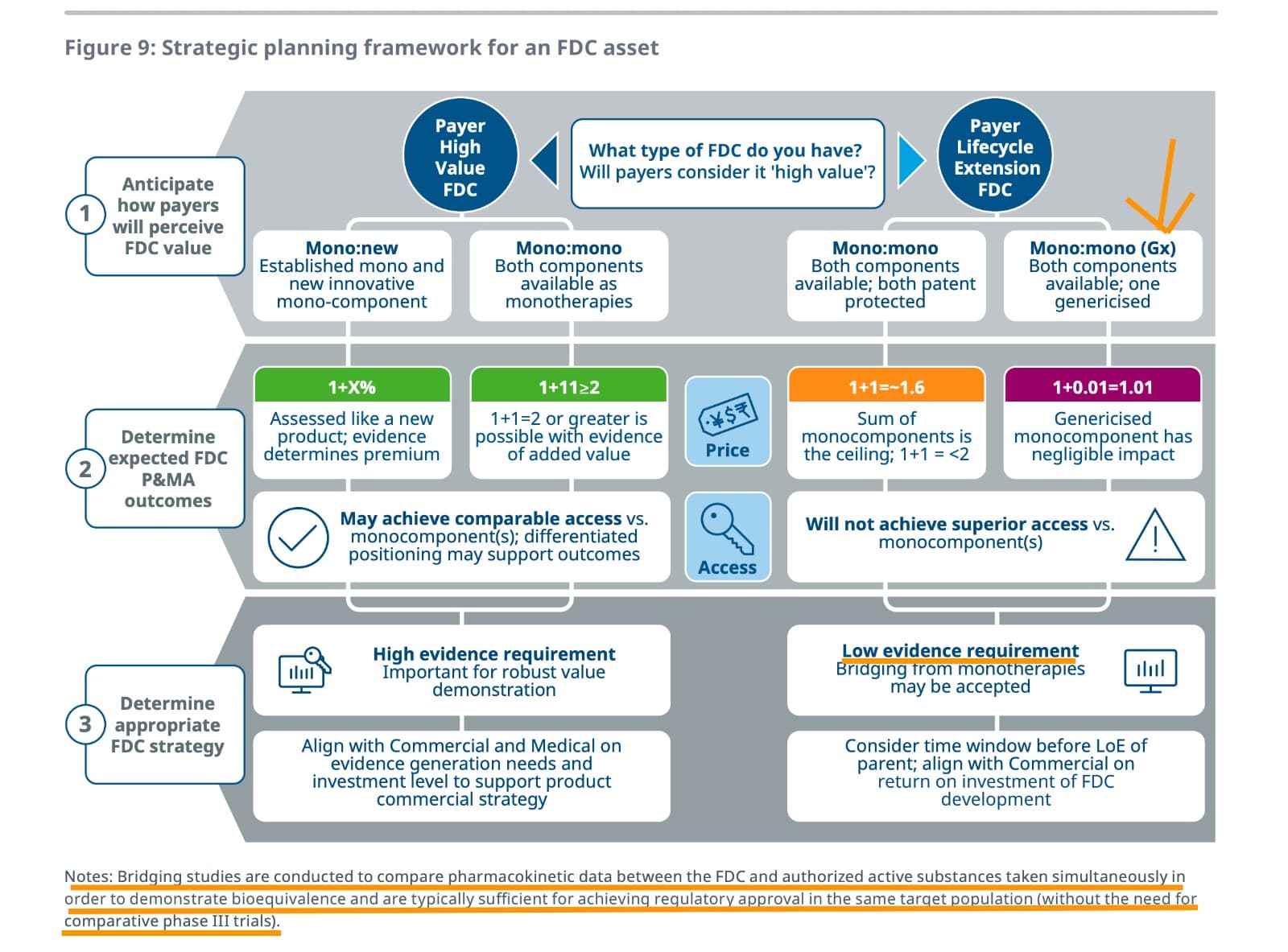

Moving on, there’s a nice [paper on FDCs] by IQVIA (https://www.iqvia.com/-/media/iqvia/pdfs/library/white-papers/not-all-fixed-dose-combinations-are-equal.pdf).

Some highlights I found interesting

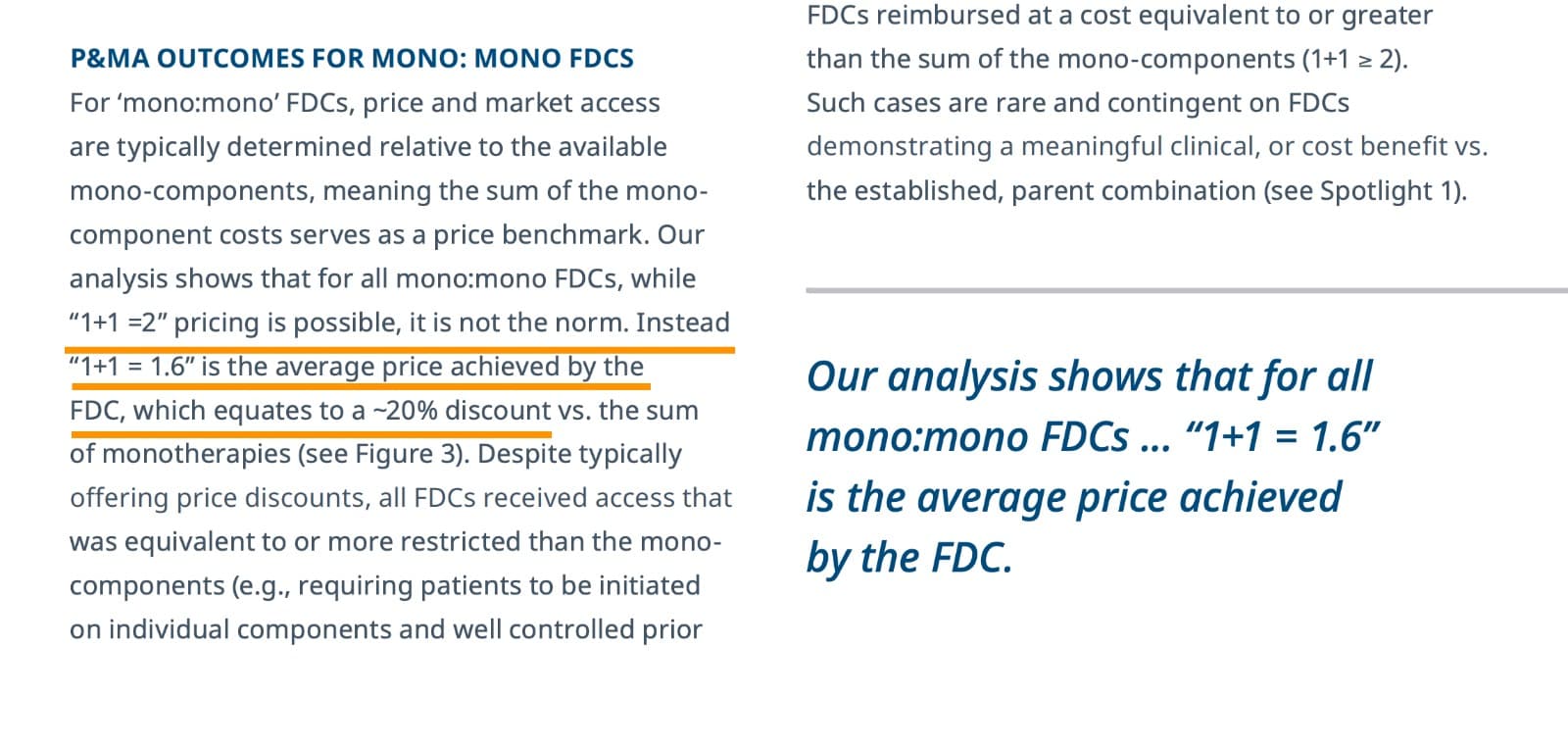

This gives an idea of how a fixed-dose combination is priced. when two mono therapies are combined. the price you achieve for FDC is 1.6 and not 2 (but in this there is a catch - that is that both should be branded drugs)

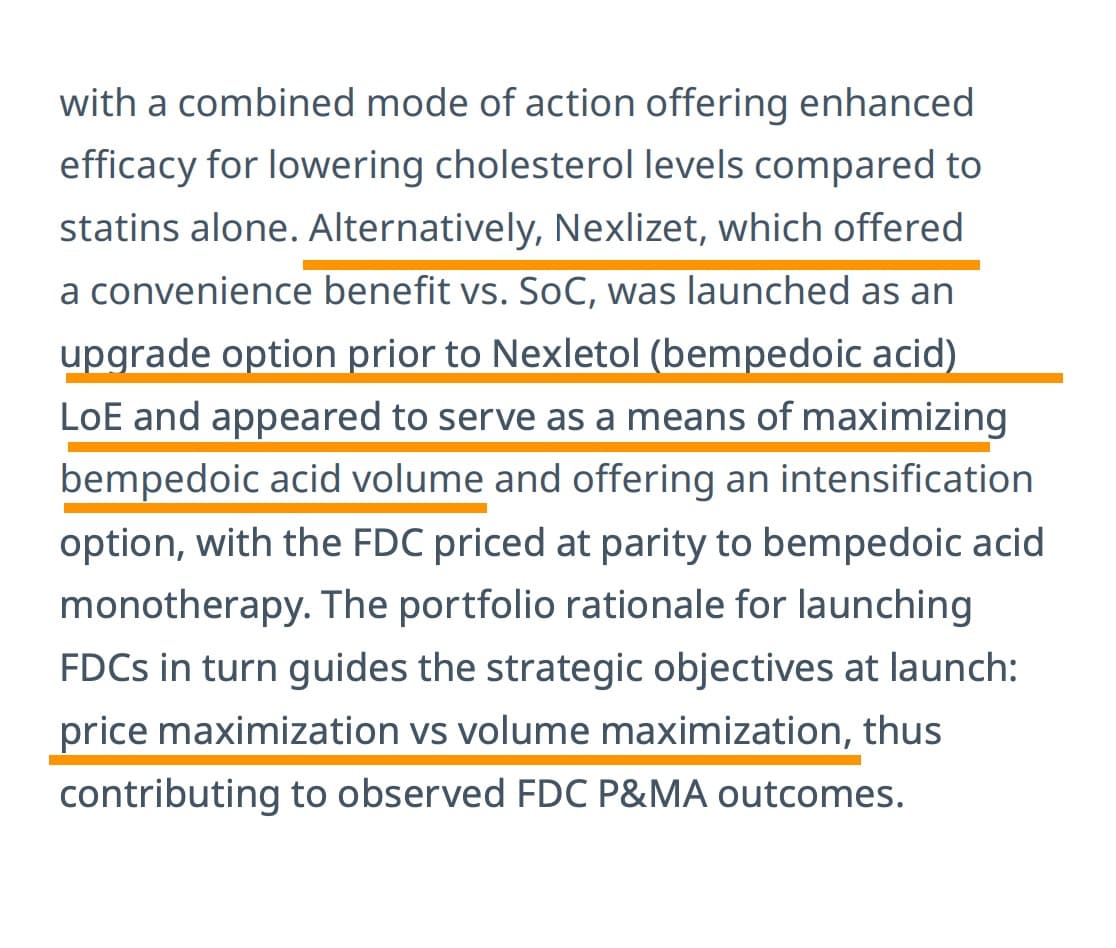

When a branded drug is combined with generic as in Nexletol (BA) + Zetia (Ezetimibe), then pricing diff between FDC and branded drug is negligible. Thats why Nexletol and Nexlizet are priced exactly the same. This works out well for the payer (insurer) who can pay less. It also makes sense as formulation, packaging, distribution cost of 2nd drug is saved

This maximises volume for BA, at the expense of margins (to the extent of subsidizing Ezetemibe)

This puts the triple combo in a different light. Not only will it offer patent extension from 2031 to perhaps 2036, it also helps to improve the volume as it will eat into Atorvastatin market sort of like an upsell (this unfortunately, is how US healthcare works)

The paper also explains why trials are not required for FDCs. Bridging studies are lot cheaper than phase-3 trials

That wraps up the work on insurance landscape and FDCs. Think I am done studying this space for now ![]()

Disc: Invested in BlueJet. Have starter positions in Neuland as well.

71 Likes

Been digging a bit deeper into the tax demand Blue Jet disclosed.

1/

Seem like the company had already anticipated the possibility of a tax claim around depreciation on goodwill. So they had proactively made a provision for the core tax amount in earlier years’ accounts. It’s good that the principal impact is likely already baked into earlier PATs. What’s pending now is clarity on how much of the interest and penalties will need to be provisioned in future quarters.

2/

But the interest and penalties were not included in those provisions. Likely because:

- Those amounts weren’t determined yet, or

- They were hoping they wouldn’t apply if they won the case.

So now the full demand is ₹193.39 cr, but only the interest and penalties would potentially hit the books from here on (since tax is already accounted for).

3/

I did not find the breakup publicly, so this next part is just my estimate, based on typical patterns in tax cases:

- Let’s assume the principal tax is ~₹120–130 cr

- That would imply interest + penalties = ~₹60–70 cr

– Interest (under Sec 234A/B/C) can add up over 3–4 years—possibly ₹40–50 cr

– Penalties could range from ₹0 to ₹20–30 cr, depending on how the case is judged

4/

The company says their position is backed by judicial precedents including SC rulings, and that they’ll be contesting the demand. So if they win or get relief, a portion of this may not materialize.

5/

Let’s see what this means for EPS.

As of Dec 2024:

- TTM EPS = ₹13.54

- Shares = ~17.5 crore

- PAT ≈ ₹237 crore

Now if we assume an additional ₹65 crore hit (interest + penalties) that wasn’t provided for:

Adjusted PAT = 237 - 65 = ₹172 crore

Revised EPS = 172 / 17.5 = ₹9.83

So the EPS drop could be ~27%, purely due to the unprovided portion of the demand.

6/

Now let’s consider the upside: What if the company wins the case (fully or partially)?

- Principal tax (~₹125 crore) is already provisioned. If reversed, that’s a direct PAT boost in future.

- Interest and penalties (~₹65 crore) may never get paid.

- So, full reversal could potentially increase PAT by ₹125 crore in a future year.

- That could translate to a one-time EPS gain of ₹7.14 to ₹10.85 per share (for 17.5 crore shares).

Disclaimer: I have a tracking position and was considering increasing my position, but holding off for now until there’s more visibility.

21 Likes

- During FY20, the company merged its sister entities. This led to goodwill of around 2000 crores. Depreciation on same around 200 crores. (Approximate figures)

- Is Valuation Justified? PAT of 130 crores, Valuation of 2200 crores. Looks justified given the chemical cycle of 2020, 40% margin business, 15x is good given the growth potential as capacity utilisation during that time was only 40%.

-In FY21, there was change in law regarding goodwill. Depreciation on goodwill on merger disallowed.

-This led to dispute and case is still pending

-The tax treatment for FY20 is done as per the original law which allowed depreciation/amortization on goodwill on merger.

-Since the search has been ongoing since FY24. The company has created provision for tax on same in books, except for interest and penalty. Provision as per September balance sheet is Rs. 114 crores.

Let’s see where this settles.

Disclosure: Invested.

12 Likes

Guys, request you all to please not litter the thread with posts that add very little value. Please put in some effort before making a post - consider it as a small gesture towards others in the forum. Littering online is as bad as littering in a physical public space. Places that are littered tend to attract more, just as in the physical world.

What affects the long term value of a company is the cash flows you expect the company to make, discounted back to the present day and the large component of terminal value (If interested, please check my notes from Damodaran’s little book on valuation). So the growth, discount rate, longevity etc. are what decide long-term value - its not one-offs and its never one-offs, unless the one-off cripples the firm debilitatingly to the point of no recovery.

In this case, BJ has already provided for 120 Cr (it has already hit the PnL in past years and the provision is part of the BS) and only ~70 Cr has to be accounted for which will likely occur over time based on when the case is heard. BJ is debt-free with healthy cash flows and great growth and if triple combo works out, even longevity till 2036 (for the BA business that is). None of these have changed that its worth making numerous posts.

If its still not clear, invert it - if a company with 14k Cr mcap has a one time “Other income” of 190 Cr, how does it affect its long-term value? It should barely move the needle upward (practically though, there are always uninformed price-setters who project a one-off and push the price up but it reverts back eventually). Why should a one-off the other way around be treated any different?

Disc: Invested

110 Likes