Thanks @Meetkatrodiya for sharing the yearly split-up of exports by products and comparing Sales with Exports. The Q2/Q3 margins are indeed a mystery and I will just put the couple of points that I thought were worth looking at

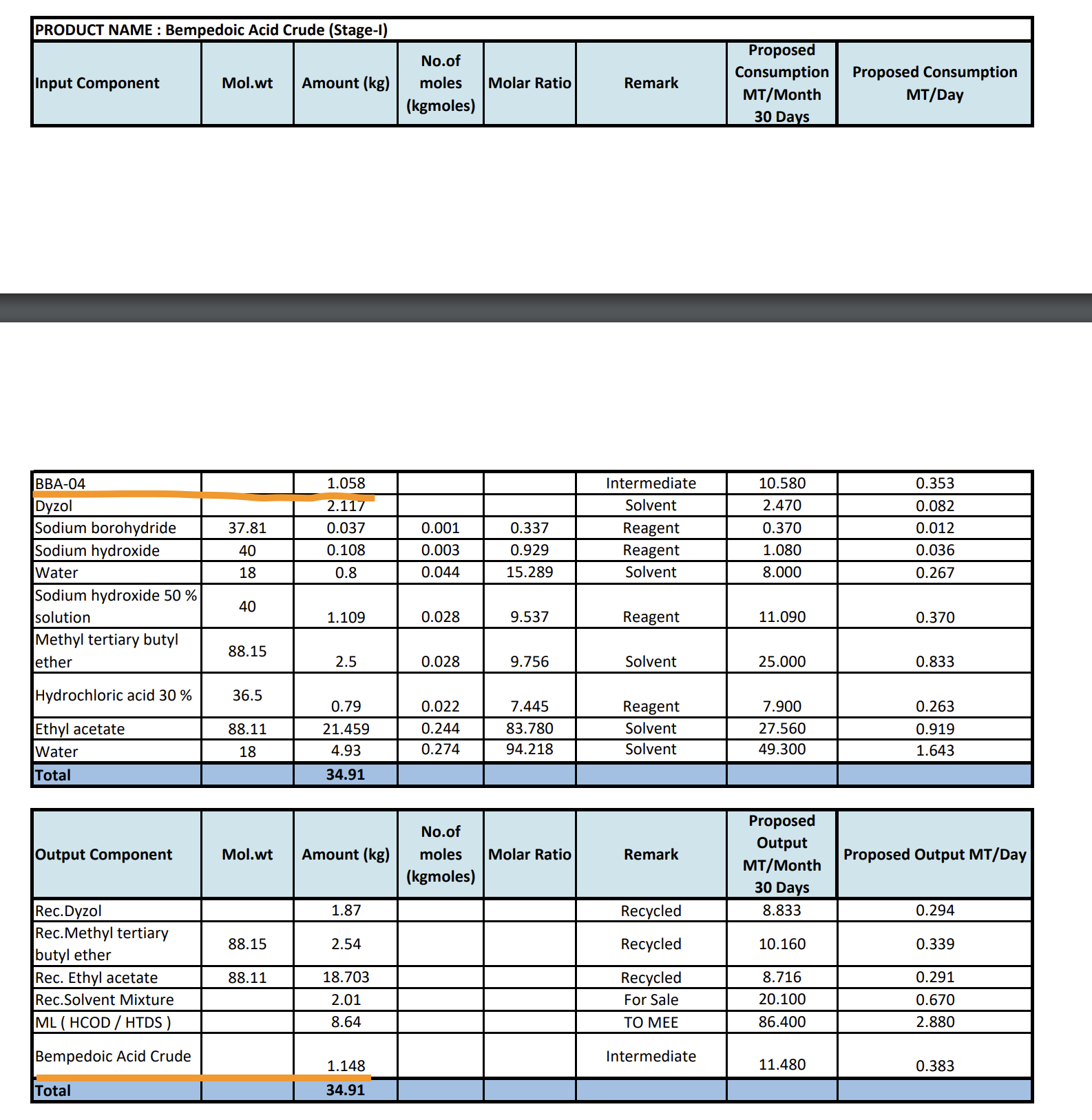

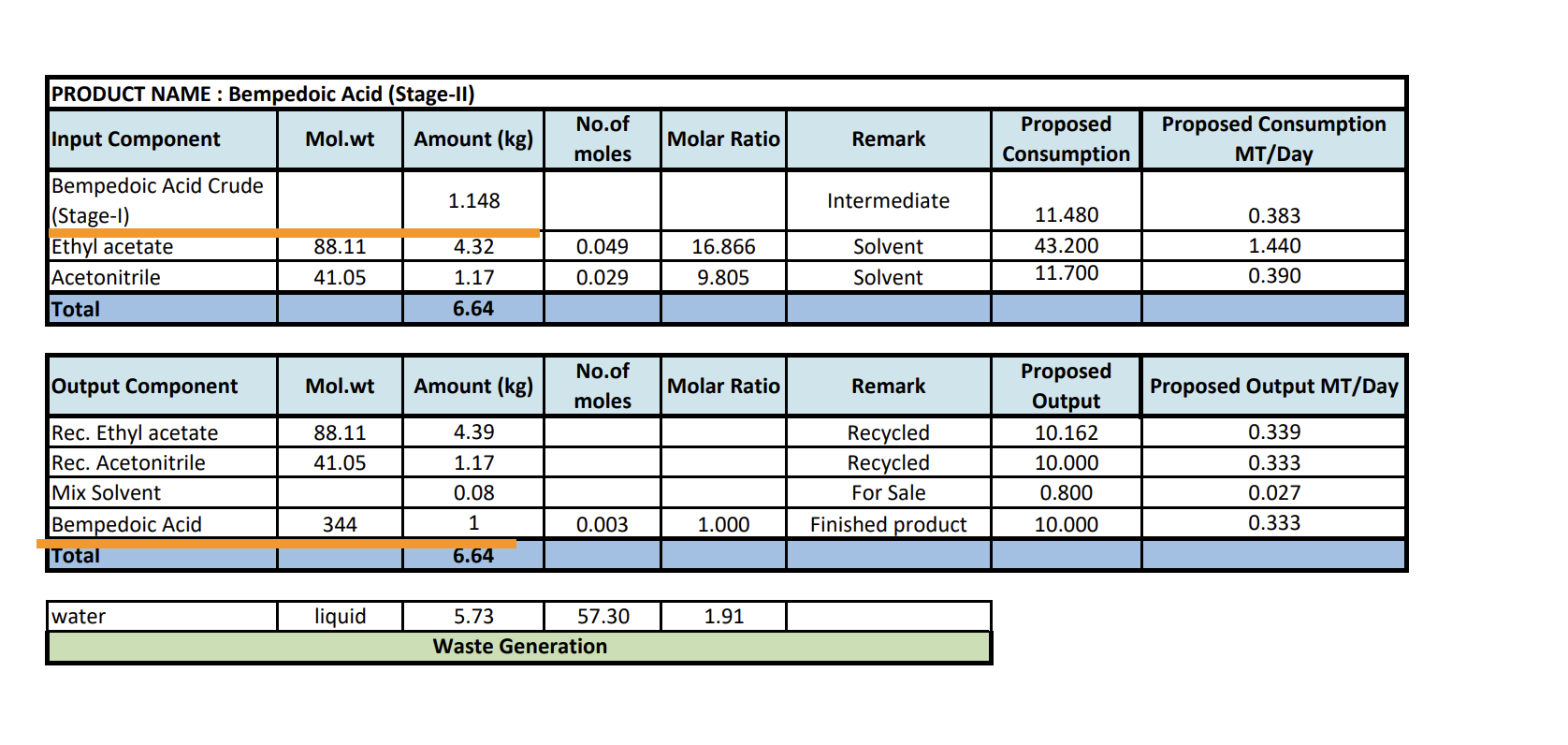

- Yield - Its possible that Neuland isn’t making good margins on BA. I know this might be difficult to believe but the yield that Neuland was getting as per EC is 1 kg of BA for 2.5 kg of intermediate. At that pricing, its hard to make a profit from the Intermediate to API conversion since BlueJet is selling Intermediate itself for $450 and Neuland is selling API for $950.

There is one more fact that goes with this, which is that Neuland has kept increasing API prices in the last 2-3 years - from $600 in Jun '23 to $750 in Mar '24 to $950 since Jun '24. Despite these hikes, the margins are still sub-par considering decent volume CMS API contributing to overall sales.

BlueJet EC had some interesting process changes to the one Neuland has.

BJ can convert 1.058 kg of intermediate to 1.148 kg Crude BA and further refine this Crude BA to get 1 kg of BA

This appears on paper to be a far superior process as it can mean undercutting Neuland on prices. But its worth noting its only on paper as of today since BlueJet isn’t manufacturing BA API but only BBA-04 which is the intermediate. But their documented process is quite different from Neuland and seems to give a way higher yield.

It is possible that Neuland is struggling with improving yield and so is selling BA at lower margins

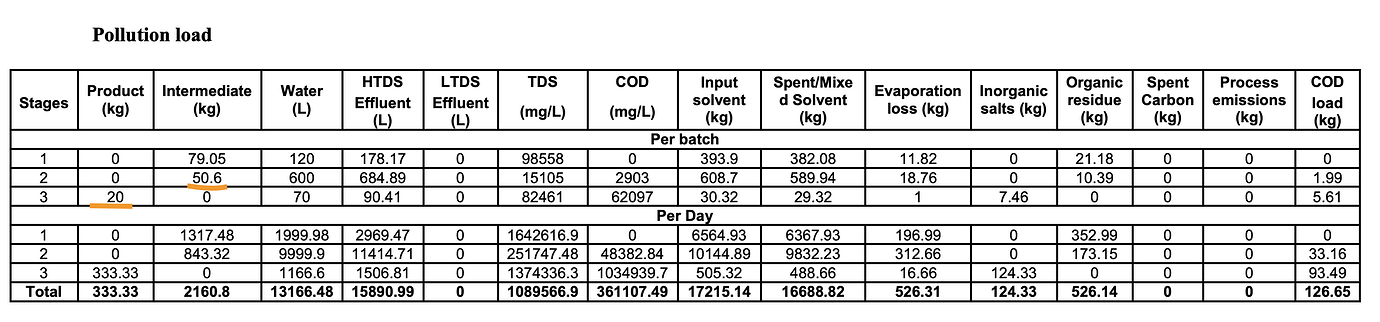

- Employee Cost - Neuland has higher employee cost which is having a huge impact on the margins. Neuland has 1600 employees as per AR

This is historic data - sales gone up 3x between FY16 to FY24 but staff cost gone up 5x

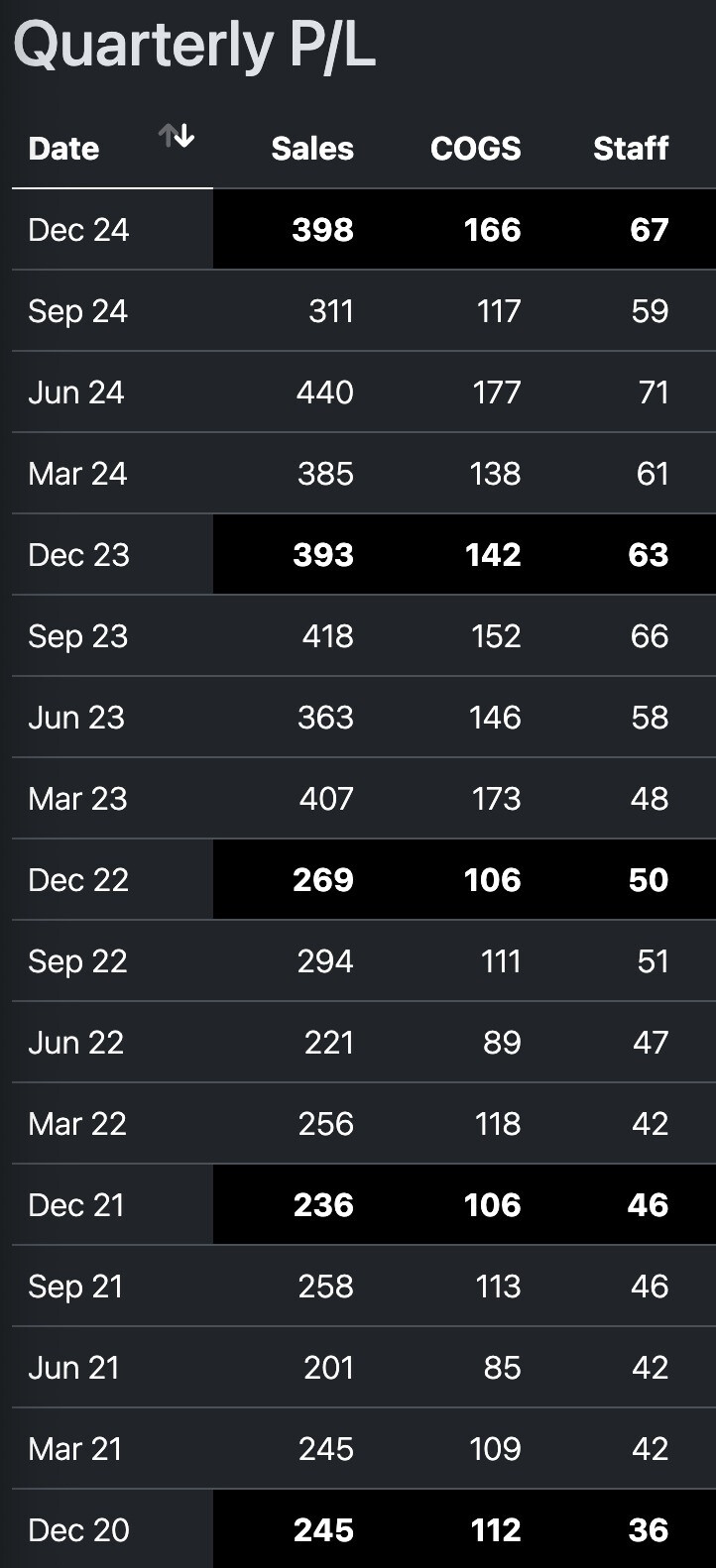

In the recent quarters as well Employee cost has scaled up alongside revenues, and so there’s no operating leverage. It almost appears like this is a highly labour intensive industry if you go just by numbers (in Q2 they had very good export at 83% and 50%+ was Xanomeline and BA, both of which are CMS molecules, but margins are 20% and 22% in Q2 and Q3, if they recorded that revenue here. In the unlikely event they upfronted revenue in Q1, you would note, that isn’t spectacular in terms of margins either for the export and CMS contribution.

In contrast, this is BlueJet’s last few quarters, with just 15% increase in employee cost (Employees have gone up from 387 as per AR in Mar '24 to 450 as of date which is in sync), they have achieved nearly doubling of salesin Dec '24 YoY. This is how commercial scaling of volumes should look like - with margins climbing with volumes - BJ margins went up from 33% to 39% and Employee cost went down from 7% to sub 5%.

- There is in general a mismatch of exports to sales in Neuland’s case which the management clarified back in Oct '24 that, that’s to be expected. But we would expect it to match broadly in a year at least - even in a year, there is quite a lot of mismatch (like 900 Cr exports in FY24 which is 58% of reported sales but AR reports exports as 78% of sales)

This is not to take anything away from the business - I look forward to Neuland scaling Bempedoic Acid, Xanomeline and maybe Viloxazine HCl as well in the future. All these are exciting innovator molecules with great potential. However, we need to see if they are able to run large scale production effectively and produce great margins through operating leverage. Difference between a 28% margin running at full tilt and making 40%+ margins is night and day in terms of actual numbers. The way BlueJet has scaled its operations in such a lean fashion is just eye-popping.

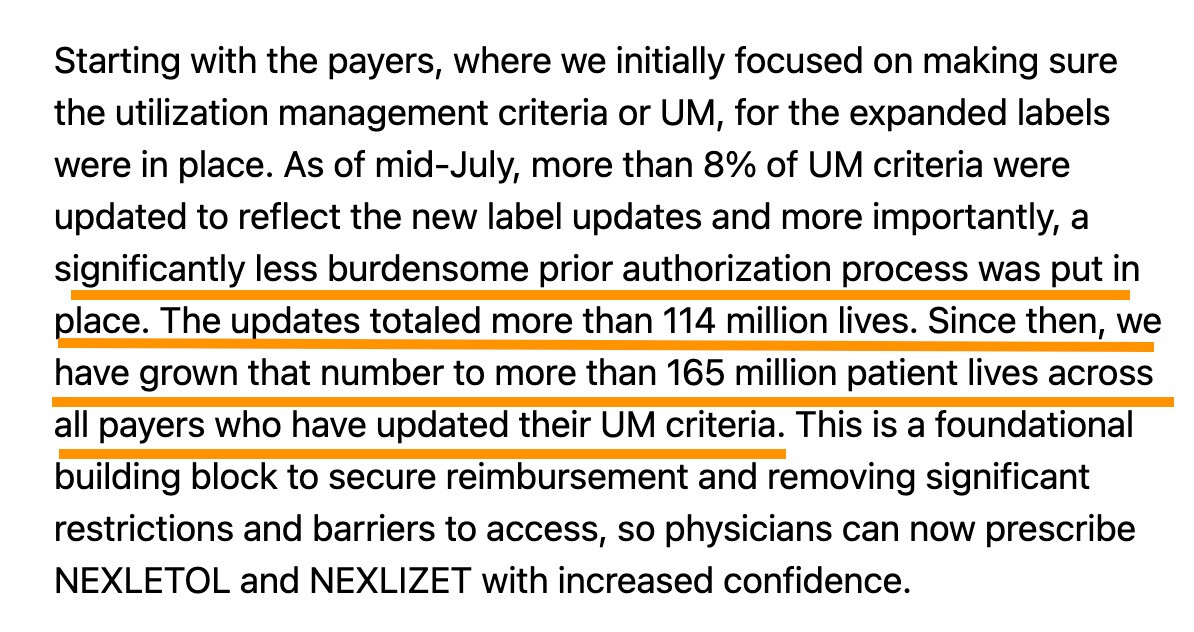

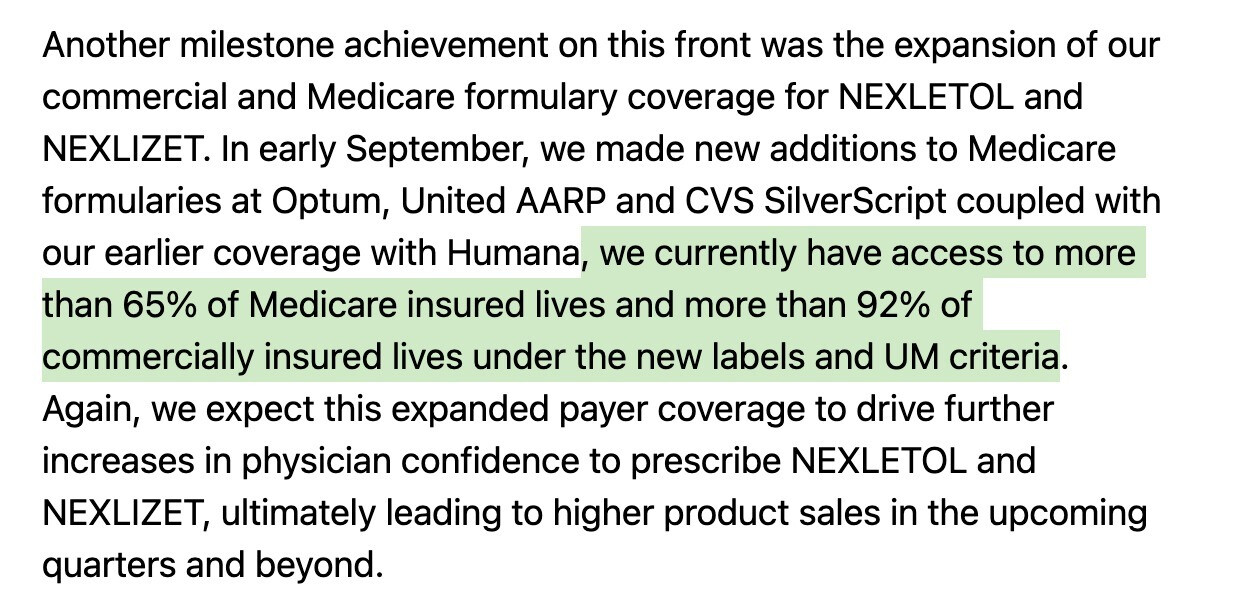

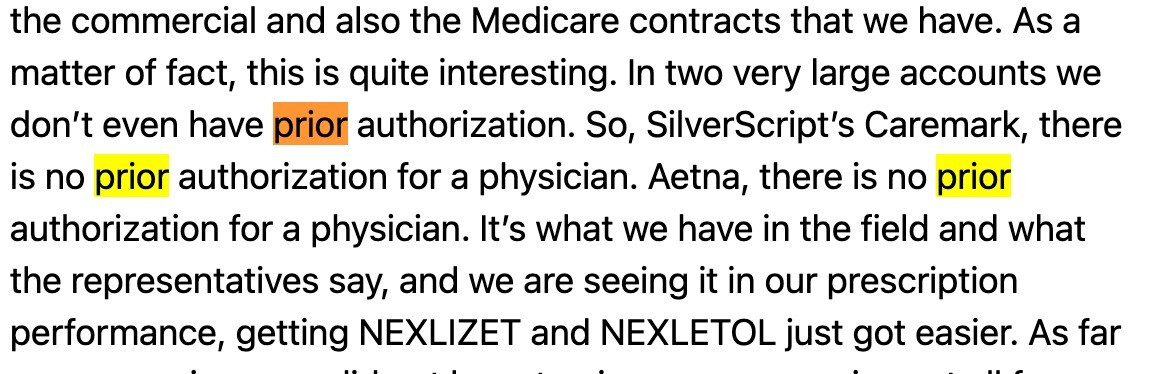

Esperion margins are poor bacause their US sales is flat despite 12% RPE growth in US (same $31m). This is not due to rising cost of tablets. From BlueJet’s side, the Intermediate cost has not changed in the last 2.5 years from between $450-$460. The higher cost is coming from discounts ESPR has given insurers to get their drugs added to the approved drugs list across plans and also from subsidizing medicare plans in last quarter (its called the donut hole or medicare coverage gap where patient has exhausted coverage and has to pay out of pocket which happens in Q4 - this is subsidised by ESPR). These are taken from last call.

They have also negotiated better coverage by avoiding prior auth or making it less stringent (approval from insurer) and also by removing step-change (trying cheaper ezetimibe before trying nexlizet which might be mandatory from insurer side) - all this requires ESPR to pay from their pocket and impacts margins - but its long term positive for them as it helps improve coverage and increase sales (which is good for BlueJet/Neuland)

Disc: Invested in BlueJet. Interested in Neuland