I was interested in the GLP-1 fill-and-finish as well which was why I bought before the demerger but it was not a big position to start with. Post demerger I sold Strides and wanted to hold Onesource but was surprised to see the promoter selling Onesource. In this market these sort of deeds at least put an intermediate top on the price. Along came Bluejet around the same time and I found it reasonable to switch.

Yes it is cheap any which way you look at it. I had shared this with a friend who invests in US markets few days back to have a look.

As of now they are serving probably somewhere between 0.25-0.5 million patients and when they reach a million patients, they should achieve a $1b in sales which will make it a blockbuster drug. At that time I wouldn’t be surprised if they achieve $1 in EPS which means they are trading at a P/E of 2. Japan/Canada markets are yet to be accessed as well on top of this. But then I dont invest in US markets and these sort of loss-making biotech are a dime a dozen there and of late looks like big pharma is looking for molecules in China since its cheaper there which is bound to derate US biotech further. But still knowing the molecule in the last week or so, I believe ESPR should do well too. No reason why Blue Jet shouldn’t do well as well (Varun Beverages and PepsiCo is a good analogue to this arrangement - VBL continues to do well for a bottler and has $20b mcap against $200b for PepsiCo though it has bottling rights for a fraction of the regions PepsiCo sells in while holding no patents)

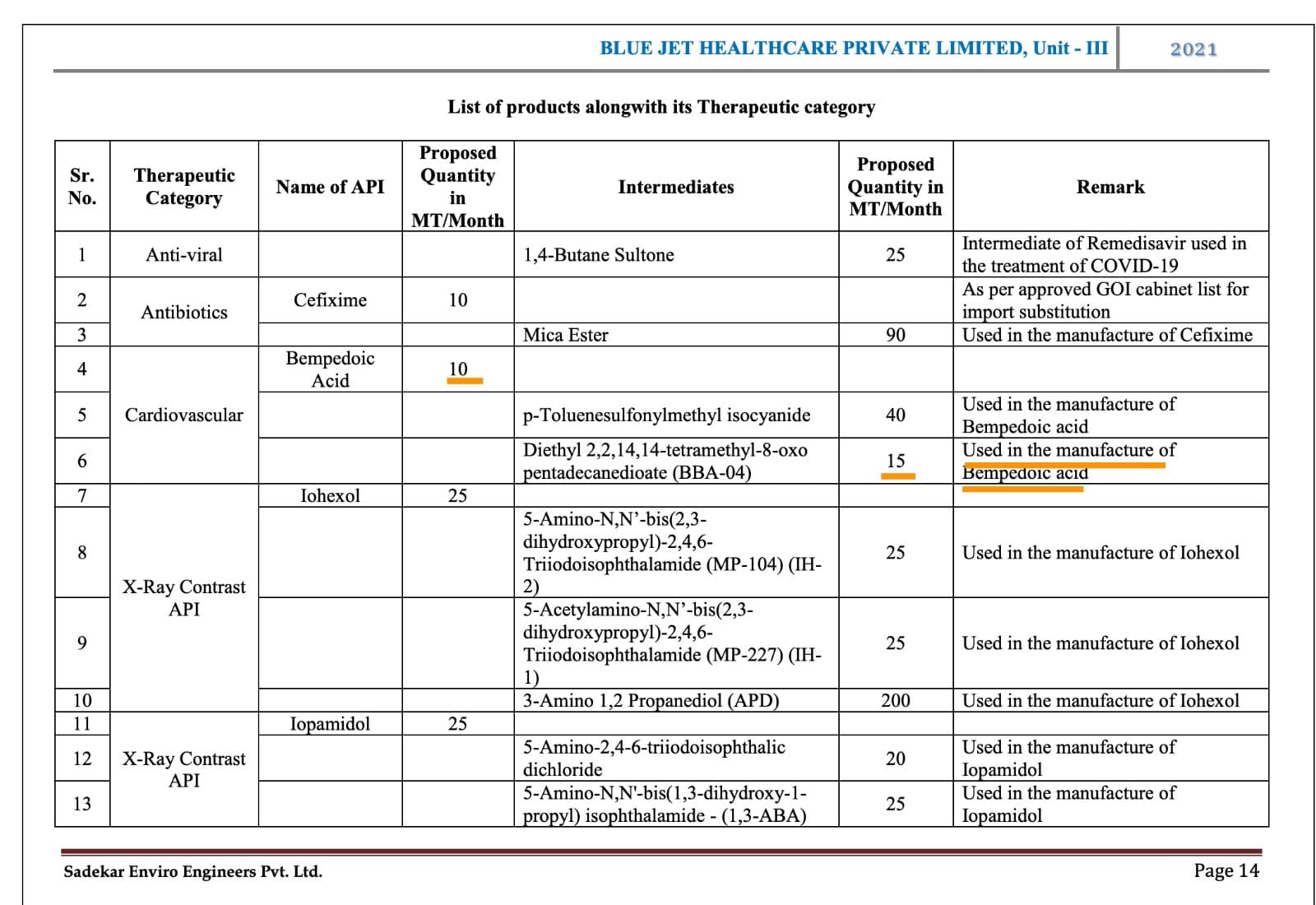

Since the last post, @aga.ayush11 @ganeshrpl and I found some more details. The EC for Unit-3 of Blue Jet shows intermediate capacity for Blue Jet at 180 MTPA (15x12) and they even have a sanctioned Bempedoic Acid capacity of 120 MTPA (which clearly is not operational as yet)

Debottlenecking this 180 MTPA is how they are probably going to double it to 360 MTPA going by the concall.

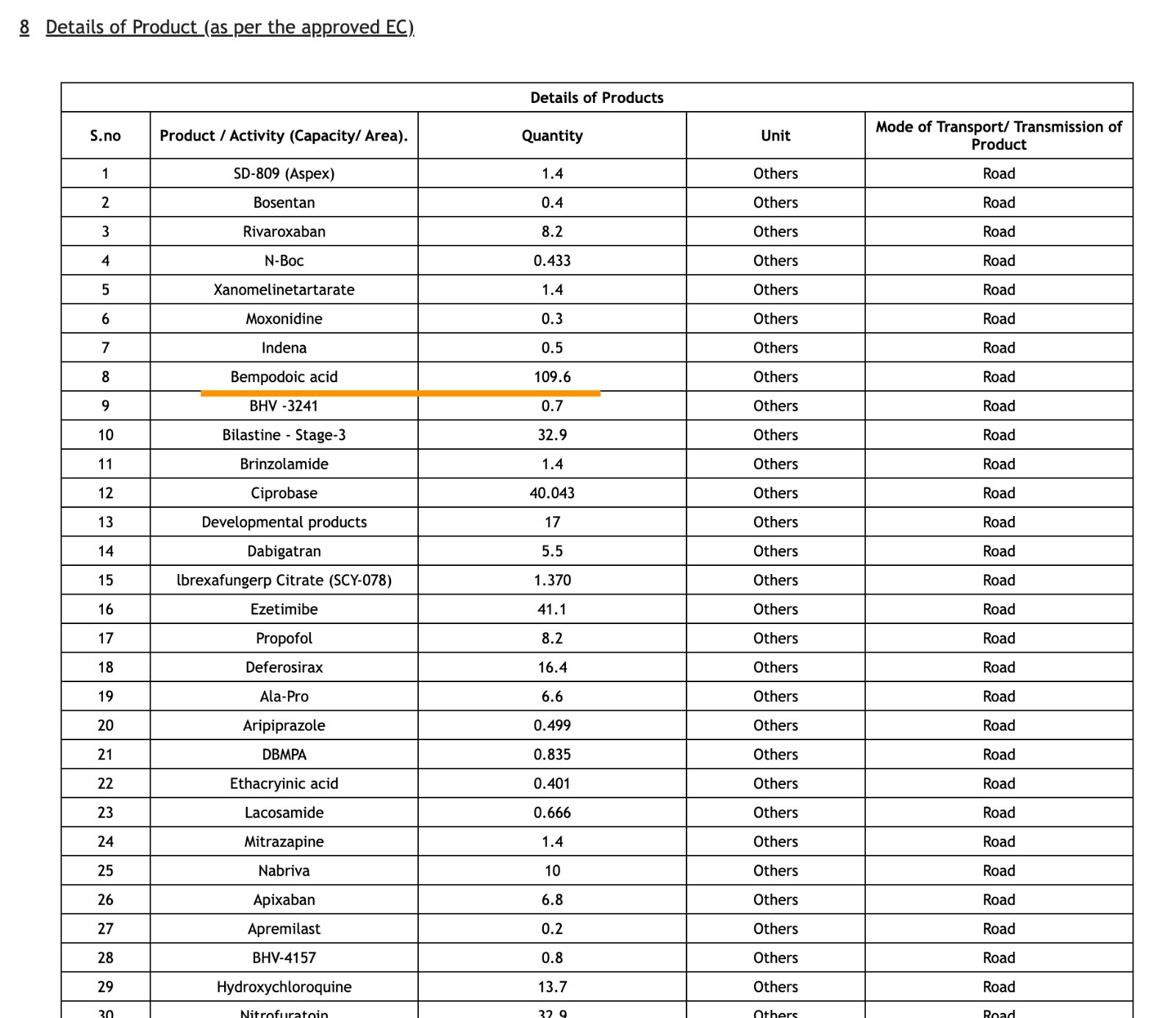

To put it in perspective Neuland has a sanctioned capacity of 40 MTPA (109.6x365) of Bempedoic Acid as per EC. As of now Blue Jet has a much larger intermediate capacity and also has BA capacity which isn’t put up though they have clearance.

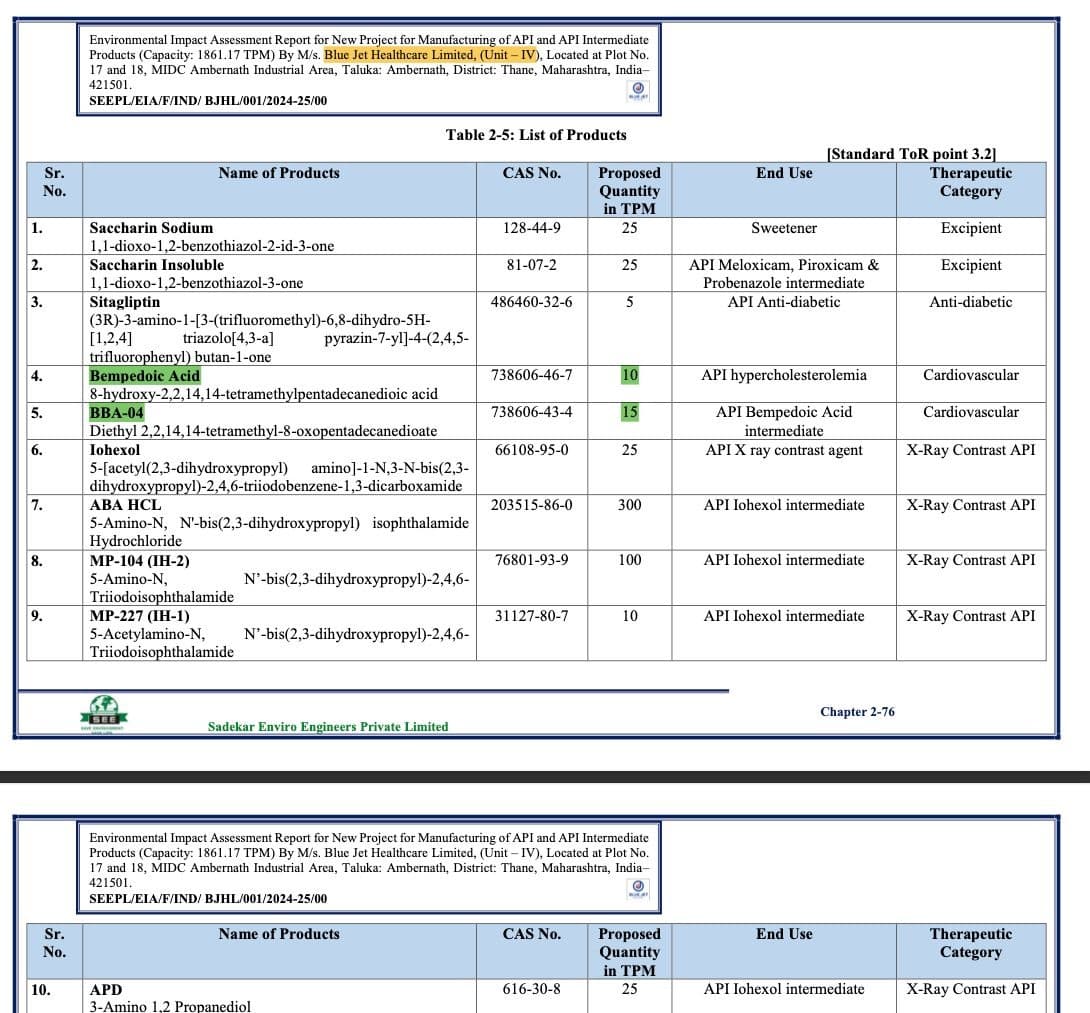

Other interesting thing is Blue Jet also has applied for EC in Oct '24 for Unit-4 to expand BA intermediate (180 MTPA again) and also BA itself (120 MTPA).

Why would they expand in Oct '24, that too double their capacity in a new unit while debottlenecking current capacity to double it already, if they didn’t have good visibility as of Q3? To me, it gives me confidence that Blue jet may have hit something big here. However, its better to wait a quarter or two until clarity emerges on what Neuland really has, as the molecule scales. Even if it does have additional capacity (there’s no EC we could find other than the 40 MTPA they have), there’s no reason why Blue Jet at least do as well as it did in Q3 and do a 500 Cr annualised PAT in FY26.

Disc: Invested and have recent buy transactions, so I am bound to be biased