BlueJet Healthcare

Leagcy : 55Y

Contrast Media (Part of the diagnostic sector)

This is growing @ 10% CAGR

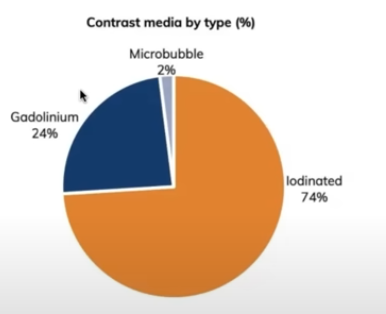

Contrast Media : Contrast media are agents used in medical imaging to enhance the visibility of body tissues under X-rays, CT-scan, MRI or ultrasound. Bluejet supplies a critical building block and several advanced intermediates primarily to three of the largest contrast media manufacturers including

- GE Healthcare

- Guerbet

- Bracco

Entry barriers for becoming a vendor to any of these players are high coz of :

- Internal standards fr product impurity/features profile

- Stickiness

- Long term supply contracts

It has had long-standing relationships

- 4-25Y of relationship with 3 largest manufacturers.

- Top 4 players accounts for ~75% global market share

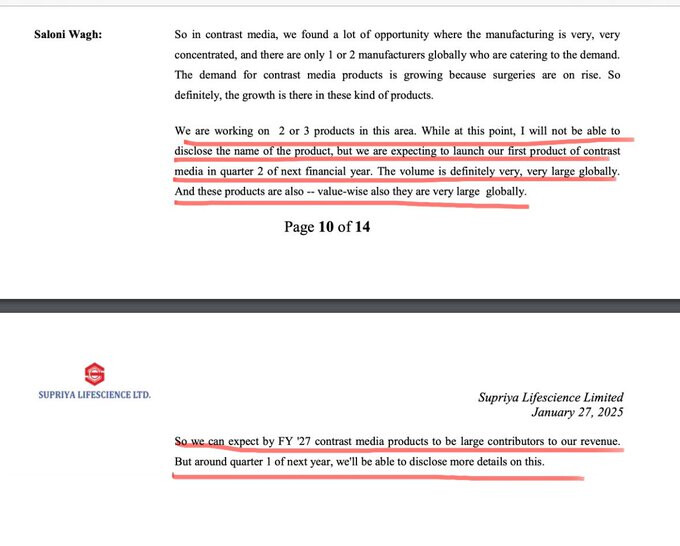

In H1FY24 - Bluejet commercialised its contrast media intermediate PF comprising 19 products

End Uses : X-ray & CT Scan, MRI Scan

High Intensity Sweeteners

They are mainly into MnC driven by FMCG segment. Lot of stickiness + this is contract driven

End Uses : Table-top sweeteners, oral care products, beverages

CDMO

This part is grown @ 30-40% CAGR

- Markets predominantly in regulated markets

The business is designed in such a way that if they are supplying intermediates and the moment when they supply advanced intermediate ie the next level these businesses get a Quantum jump in value. This inturn helps beat the industry growth rate.

Capacities are fungible too.

End Uses : Cardiovascular system, central nervous system, oncology

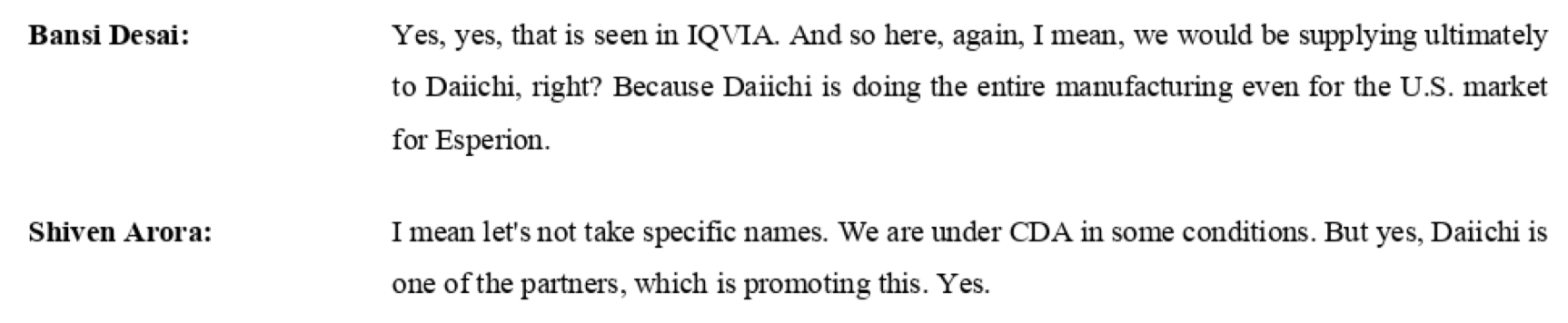

Innovator mentioned being Esperion Therapeutics Inc

![]()

PI/API to benefit from intermediate for bempedoic acid

The drug is sold as Nexlizet (Bempedoic acid and Ezetimibe) and Nexletol (Bempedoic acid) in the US and as Nustendi (Bempedoic acid and Ezetimibe) and Nilemdo (Bempedoic acid) in Europe. Daiichi Sankyo has license to manufacture and sell in Europe.

Few terms i thought of just blabbering about so that you feel that technically empowered to some extent :

Where Nexlizet (Bempedoic Acid) Stands in the Siege Cycle:

![]() Stage 1 (Introduction & Early Adoption):

Stage 1 (Introduction & Early Adoption):

- Nexlizet is still in the early adoption phase, especially as a “statin alternative” for patients who experience muscle pain or intolerance.

- Revenue is still low compared to statins, but Esperion Therapeutics is pushing for wider prescriptions.

- It has already been FDA-approved and shown cardiovascular benefits in trials, which will help in insurance coverage expansion.

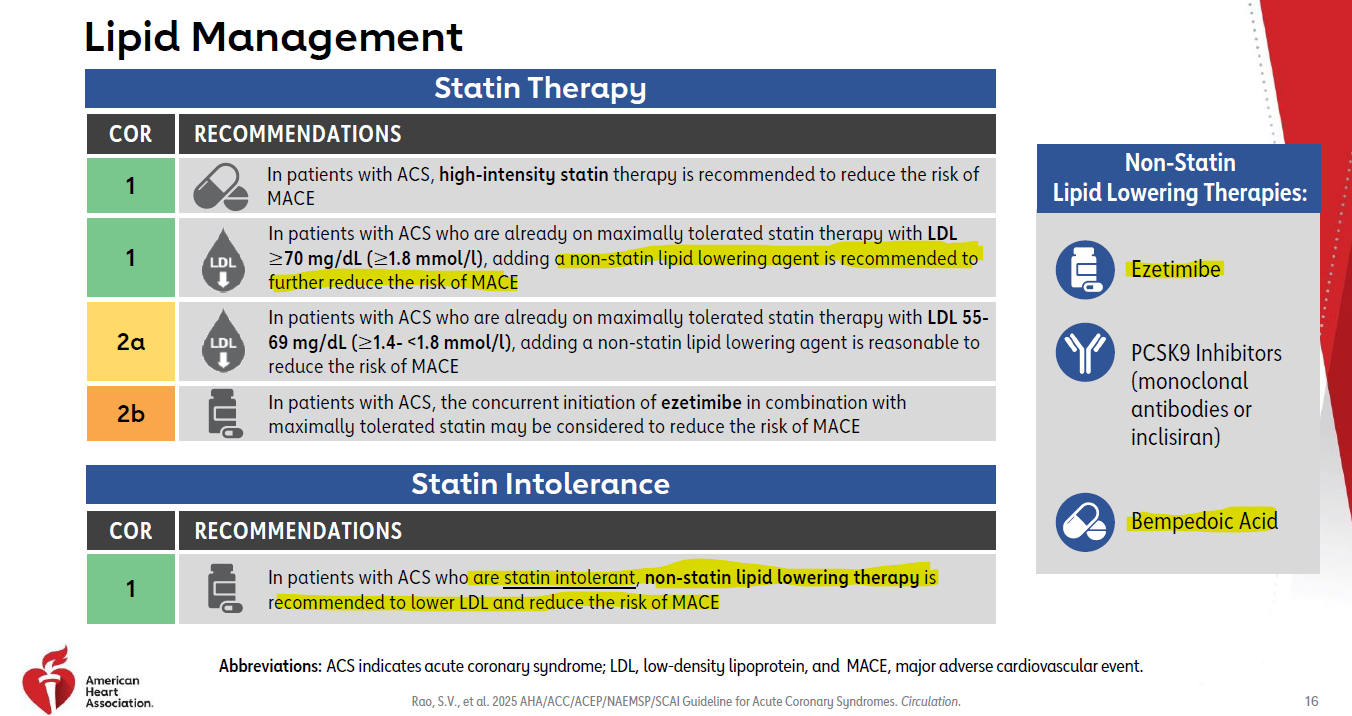

Why is Bempedoic Acid Important?

- Alternative to statins: Useful for people who experience muscle pain or side effects from statins

- Add-on therapy: Can be combined with statins or ezetimibe for greater LDL reduction

- Lower risk of muscle-related side effects: Unlike statins, it is not activated in muscle cells, reducing the risk of myopathy

Book : Ten Drugs

Typical life cycle of blockbuster drugs in three phases:

![]() Stage 1: Discovery & Early Adoption – A new drug is introduced, often with excitement and aggressive marketing. Sales grow as doctors start prescribing it.

Stage 1: Discovery & Early Adoption – A new drug is introduced, often with excitement and aggressive marketing. Sales grow as doctors start prescribing it.

![]() Stage 2: Widespread Use & Peak Revenue – The drug becomes mainstream, generating billions in revenue. Pharmaceutical companies push it heavily, and prescriptions soar.

Stage 2: Widespread Use & Peak Revenue – The drug becomes mainstream, generating billions in revenue. Pharmaceutical companies push it heavily, and prescriptions soar.

![]() Stage 3: Saturation, Decline & Resistance – Side effects, competition (generics, new drugs), or shifting medical guidelines slow down sales. Sometimes, lawsuits or safety concerns emerge.

Stage 3: Saturation, Decline & Resistance – Side effects, competition (generics, new drugs), or shifting medical guidelines slow down sales. Sometimes, lawsuits or safety concerns emerge.

![]() Example:

Example:

- Statins (Lipitor) → Stage 1 (1996 launch), Stage 2 ($120B in sales from 1996-2011), Stage 3 (Generic competition & alternative treatments).

- Bempedoic Acid (Nexlizet) is likely in Stage 1 now.

Key Features of Bempedoic Acid:

- Brand Name: Nexletol (in the U.S.), Nilemdo (in Europe)

- Developed by: Esperion Therapeutics

- Approved for: Lowering LDL cholesterol in patients with hypercholesterolemia or cardiovascular disease, particularly for those who cannot tolerate statins

Financials

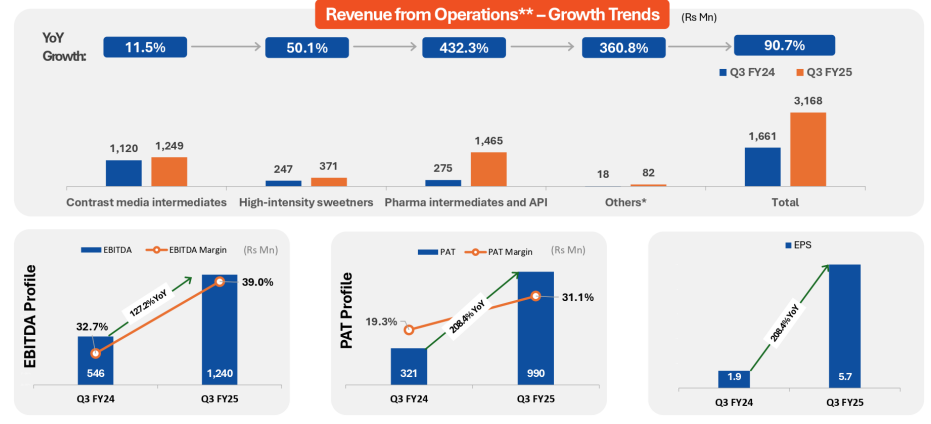

- Margins making > 30% margins - showing business is doing something uniquely Vs others

ROCE > 30% - Sales have grown 5-10% approx

- Shareholder pattern

- The company continues to remain debt free with robust Liquidity

- Capex is always in line with customer lockins so which will always come with certainty

Risks

- Competition in CDMO/ Contrast Media

- SUPRIYA Lifescience getting into Contrast Media. Healthcare has 68% revenue coming from this segment. Interesting to watch the competition ahead.

- Promoter holding is high and they would need to bring it down to 75%

- Client concentration in contrast media - But its a innovator dominated industry - Basically front end market is highly concentrated so there is low risk wrt client concentration - And may be an advantage.

D: Invested