Just my two cents,

Asked GPT for their comparable price range per patient,

Tldr; the price of obi quite higher than the BA, so the replacement of the drug shouldn’t happen in the pace which you might expect

Generated by AI

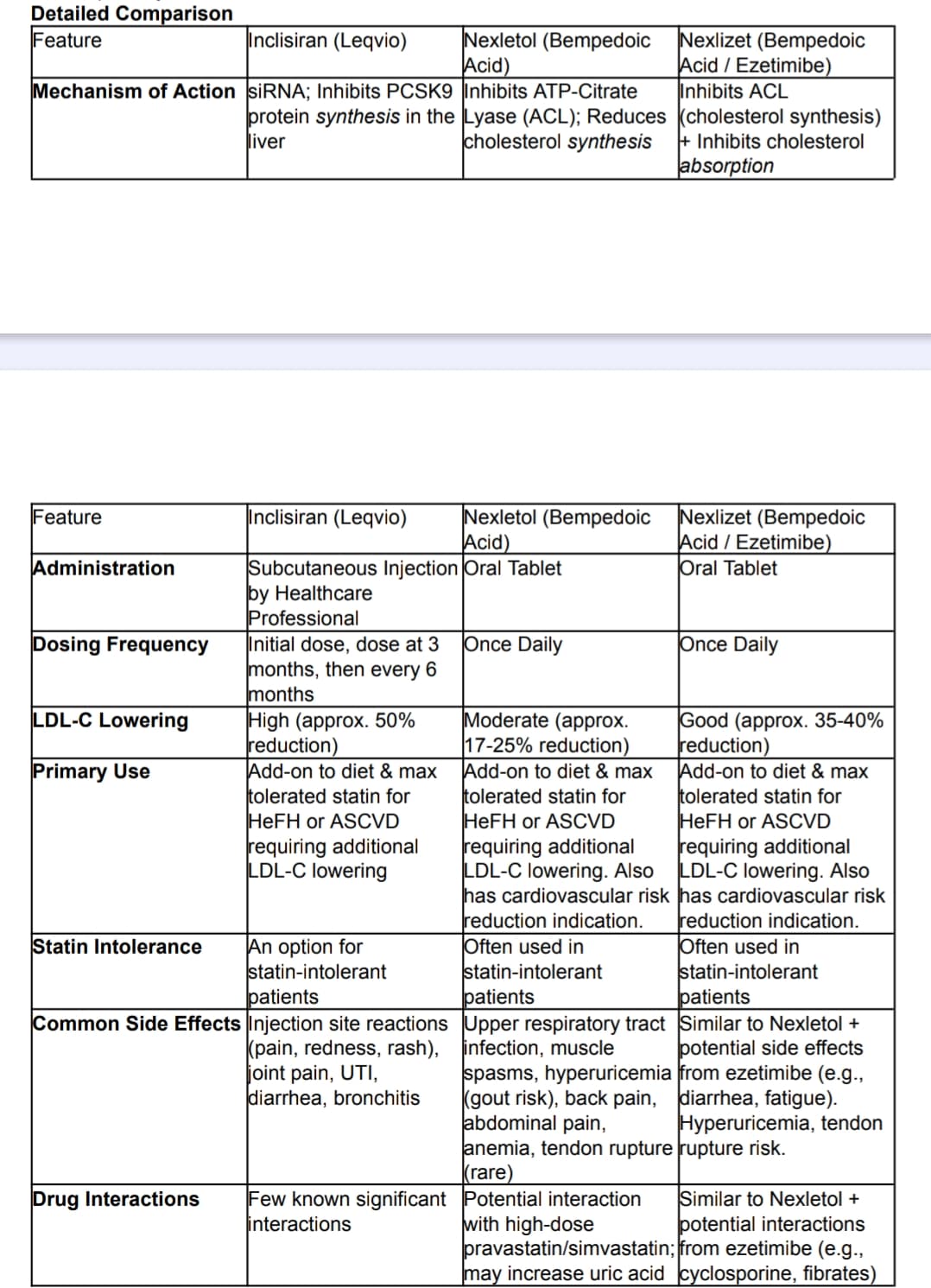

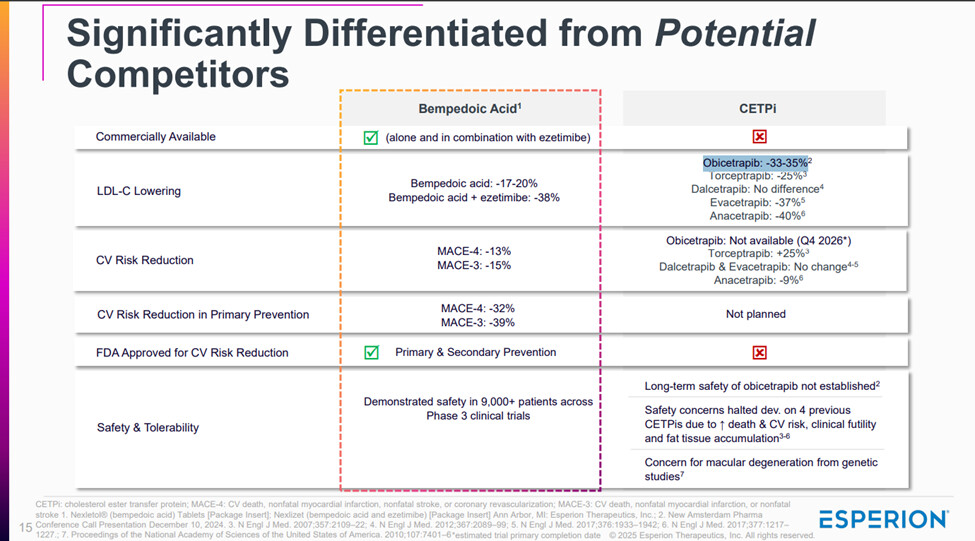

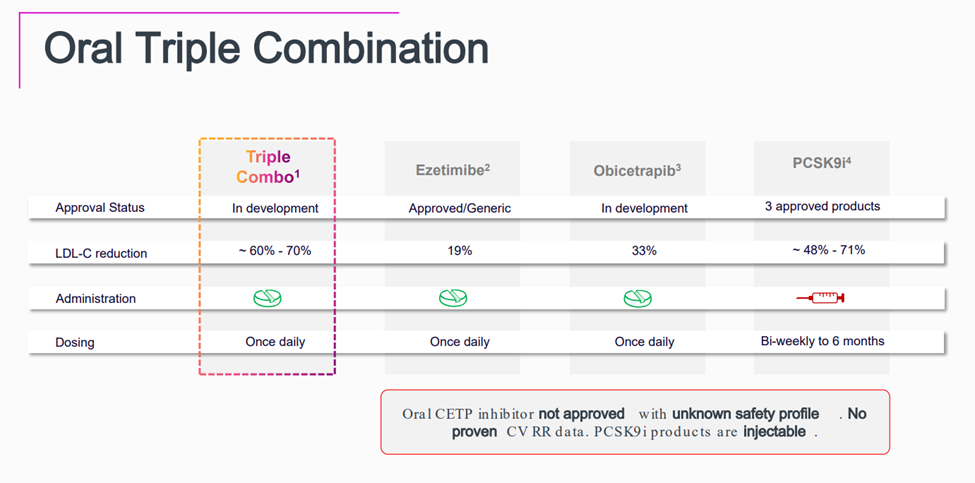

Obicetrapib is an exciting LDL-C lowering agent—at 10 mg daily, it achieves ~45–51% LDL-C reduction, outperforming both Bempedoic Acid (BA) 180 mg (~15–18%) and BA + Ezetimibe (~36–38%). However, per-patient economics remain a major obstacle to rapid adoption.

Key takeaway: While Obicetrapib may be clinically superior, its cost per 1% LDL-C reduction is not yet competitive. For large-scale use—particularly in value-sensitive systems like the NHS (UK) or public insurers in the EU—this matters.

Even if commercial pricing improves post-approval, formulary access, HTA assessments, and real-world cardiovascular outcome data will all influence its uptake.

Conclusion: Obicetrapib has clear therapeutic potential, but BA and BA+Ezetimibe will likely retain a strong role in lipid management until Obicetrapib demonstrates either a cost-effective pricing model or major long-term outcome benefits.

Another factor to consider is prescription behavior and clinical inertia, which are often shaped by existing guidelines and real-world usage.

Bempedoic Acid (BA) has already been incorporated into treatment frameworks like those by NICE in the UK, where it’s recommended for patients who are statin-intolerant or require additional LDL-C reduction. Its uptake is not just based on trial data, but on practical success in real-world settings, especially within public health systems.

Unless Obicetrapib gains similar guideline endorsement, demonstrates long-term cardiovascular benefits, and clears HTA hurdles, it’s unlikely to displace BA quickly—regardless of superior LDL-C reduction. Physicians tend to stick with what’s already proven, reimbursed, and familiar.

So while Obicetrapib is promising, prescription patterns won’t shift overnight without structural and clinical reinforcement.