Blue jet healthcare - Not sure about the legality of posting charts after latest SEBI regulations, so sticking to only discussing fundamentals. There isn’t much in the chart anyway - it looks overbought on the daily and is in fact bearish.

What got me interested was the breakout growth, in revenues, profits, margins - so the obvious question was - is this lumpy one-off or is this sustainable? The growth is coming from an intermediate used in the manufacture of bempedoic acid which is used for lowering LDL-Cholesterol, just like statins. What’s also nice is that this isn’t some generic drug but is an NCE (Innovator: Esperion Therapeutics) which is seeing breakneck growth. The drug is sold as Nexlizet (Bempedoic acid and Ezetimibe) and Nexletol (Bempedoic acid) in the US and as Nustendi (Bempedoic acid and Ezetimibe) and Nilemdo (Bempedoic acid) in Europe. Daiichi Sankyo has license to manufacture and sell in Europe.

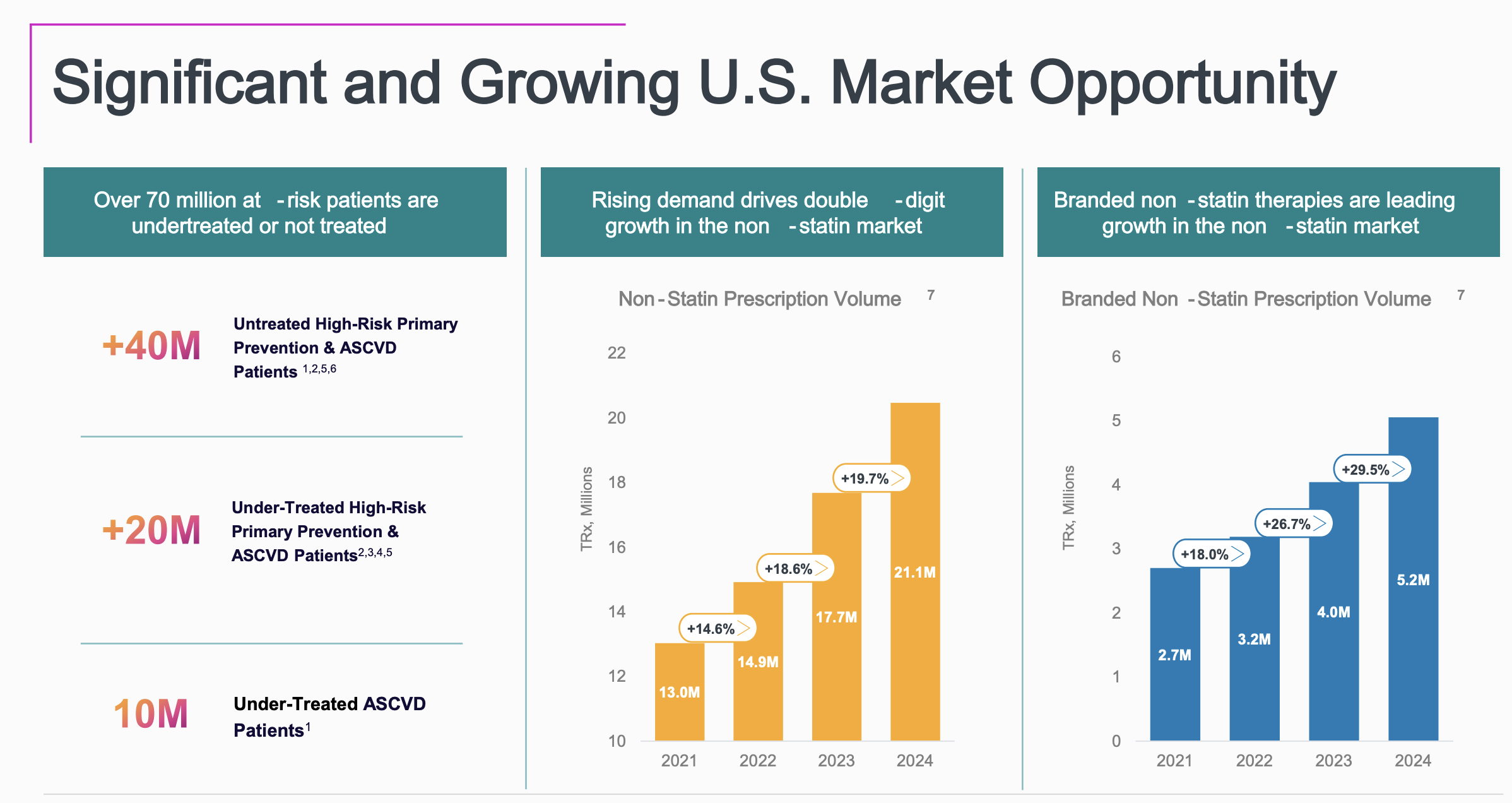

The US prescription growth is great even on a quarterly basis.

The overall TAM is 70 million patients in the US alone after the expanded label usage granted recently.

The non-statin growth has been strong due to multiple factors from statin-intolerance to side-effects of memory loss and muscluloskeletal issues.

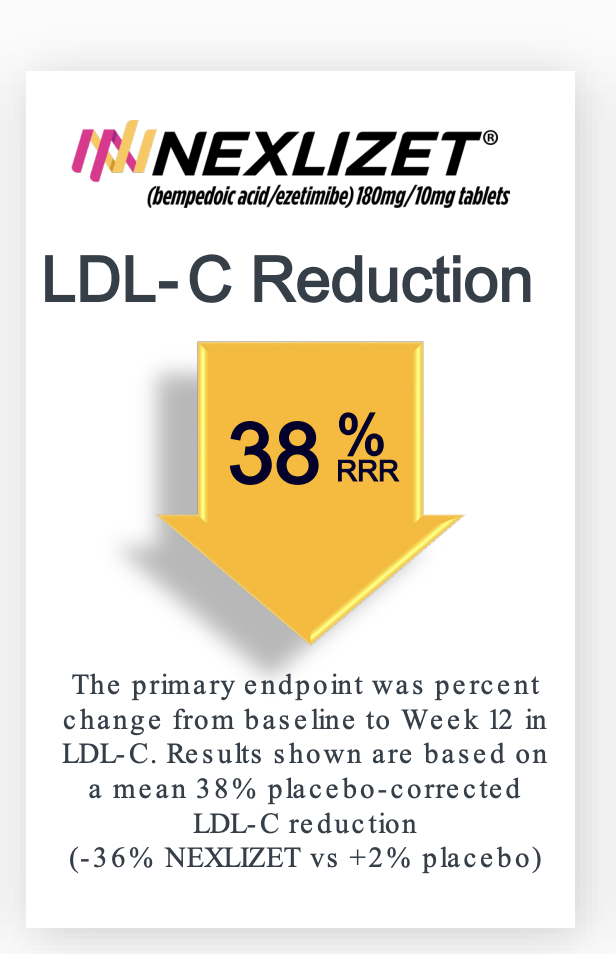

Nexlizet’s LDL-C reduction is comparable to statins and looks like docs are prescribing it alongside statins as well going by this podcast

Currently PCSK9 inhibitors seem to be used in cases with high LDL-C as a non-statin treatment. This itself (Repatha and Praluent which are mAbs) is a $3b market which a oral drug like Nexlizet can challenge. Insurance coverage as well is there for these drugs.

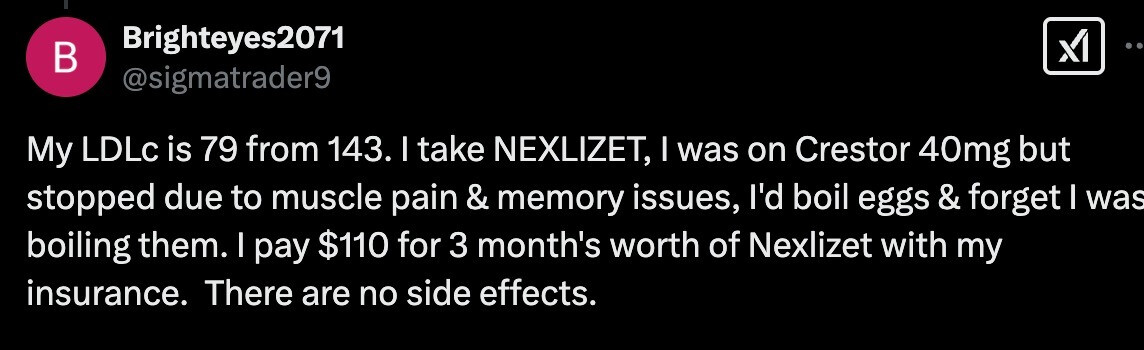

A real customer’s usage I saw on X.

The book “Ten Drugs”, talks about how statins were overprescribed and how Lipitor revenues soared to a cumulative $120b between '96 and '11. This is unfortunately how healthcare works which is an indicator for how Nexlizet prescriptions might go - its in stage 1 of Seige cycle (concept from the book of how uptake for drugs goes from Stage 1 to 3)

If the current rate of growth continues, there’s scope for a 500 Cr PAT in another 3-4 quarters.

There are some other triggers in the Contrast media business but they aren’t as exciting. (There’s a gadolinium based NCE called gadopiclenol for which Blue jet will supply intermediates from this quarter)

Risks:

- Growth might be led by inventory buildup expecting strong uptake, so could tail off after few quarters

- Neuland labs was the supplier of Bempedoic Acid API to Esperion as per reports few years back. Though they continue to supply, there’s an alternate supply chain for the API with Blue Jet intermediate + BA API from Fareva vallee, France. Not sure of exact dynamics here and how it might affect future sales

- Promoter holding is high post listing and should come down to 75% in 3 yrs (end of next yr), so there’s promoter stake sale on the horizon

Disc: Invested around 800-820.

Credits to @aga.ayush11 for digging deep on this one