-

No changes will be there in EBIDTA. However EPS for the year will be negative. As the company has corrected a lot and the management is foreseeing significally less cash generation from the facilities, it makes prudent to do one time write of this year only.

-

Writing off the identified CWIP will reduce the capital employed in the company, which can result in a higher ROCE in forthcoming years. This is because the capital employed will be lower due to the reduced CWIP whereas production and revenues will be generated from the said facilities.

-

Asset turn over will be more in forth coming years.

-

Now experienced investors like @harsh.beria93 and @Rafi_Syed will be able to answer how the management took such a big decision by investing in new P&M without doing a home work and where they went wrong.

“However EPS for the year will be negative.”

Can you pl explain how you determined that the EPS for the year would be negative?

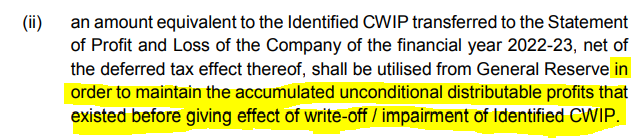

My reading of the proposal, particularly the highlighted text below, led me to understand that because the managemnt does not want to show a reduced EPS for the FY 2022-23, the CWIP write-off will be against accumulated balance in General Reserve.

(i) In respect of the Manufacturing Facilities or part thereof, for which the

commercial operation commences during the financial year 2022-23 and

capable of being used in the manner as intended by the management of the

Company, the amount of Identified CWIP shall be written-off to the Statement

of Profit and Loss of the financial year 2022-23;

In my understanding if they write off to the the Statement of Profit and Loss of the financial year 2022-23, the company has to show losses and ultimately -ve EPS.

In whatever manner the management presents in the books, the fact doesn’t change that 1150 cr of shareholders money has gone down the drain!!!

The networth and fixed assets would stand reduced to the extent of write off

Business calls do go wrong, but the relative magnitude of assets written off and time (doesn’t reflect in balance sheet) show some serious weakness on part of management.

Disc.

Was invested earlier. Fortunately exited around 700 when asset turnover was not improving

Q4 results are out (Link).

Key Takeaway for me: Provides a good example that why I must read the accounting notes!!!

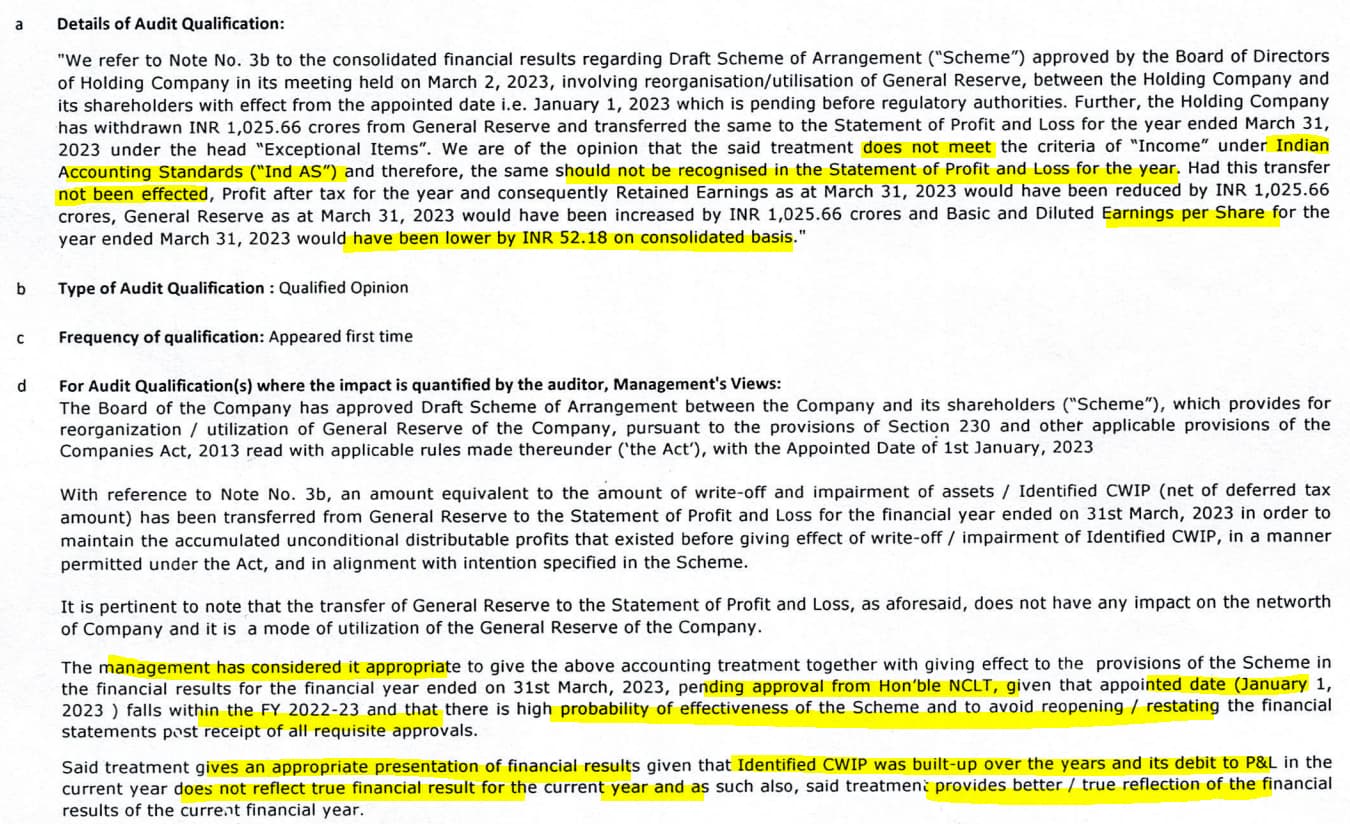

An accounting decision by the management to write-off and provision the impaired assets under CWIP (snapshot shown below).

Net result: Net Loss of ~670 Cr. switched to Net Profit of 342 Cr. None of these figures showed up in the PnL as all is managed in the accounting notes. This led to Qualified Opinion from the auditor since it does not follow Ind AS accounting standards,

Alembic continues to do its thing, adjusting the CWIP directly through reserves and not passing it via P&L statement. It lowers their book value, improves ROE and P&L looks clean. On the business front, large number of launches will happen in the next few quarters. Concall notes below

FY23Q4

- Wrote off 1150 cr. of CWIP (largely capitalized pre-operating expenses) without passing through P&L statement. Won’t be capitalizing any pre-operating expenses from now (65 cr. additional costs in Q4 P&L)

- Received PLI benefits of 21 cr.

- Price erosion is still in double digits

- Launched 5 products in Q4FY23, will launch 10 products in Q1FY24 and 20-25 in FY24

- R&D will be maintained at 500-525 cr.

- 15-20 ANDA filings in FY24

- Expect margins of 15% in FY24

- Will have 17.5% tax rate in FY25

- FY24 capex will be less than 250 cr.

Disclosure: Invested (position size here, no transactions in last-30 days)

Alembic Pharma gets EIR from USFDA for its solid oral formulation facility at Jarod

What is implication for the business? @harsh.beria93

Unnecessary & too much capex is called gold plating. This is done by promoters to take money out of the company for personal use. It is usually written off in the future.

I had mentioned this in October 2020 Alembic Pharma (Oral Solids ==> Injectables, Onco, Derma, Opthalmic) - #654 by vnktshb

But in the euphoria no one noticed I guess

Alembic has been showing very strong growth in API division and in International markets, with US price erosion still in double digits. They have launched 5 injectables so far, and plan to launch 20 products in FY24. Concall notes below.

FY24Q1

- Has grown at faster than IPM rate in both specialty and acute segments. Have increased marketing spends in India

- Growth is coming from International markets and API division

- US price erosion is still in double digit

- Filed 10-15 injectables & launched five products (4 oncology + 1 general injectable). Current portfolio is not large enough to fully benefit from current US shortages

- FY24 US launches: 20 products

- Competitive intensity is lower in injectables, there are lots of shortages in injectables

- ~200 people added in animal healthcare, has good launches lined up in non-antibiotic space, probiotics, and in some mainline veterinary products

- Staff cost has increased because of operationalization of new facilities

- R&D costs will be ~500 cr., as % of sales it will come down to 10%

Disclosure: Invested (position size here, no transactions in last-30 days)

Meaning of this? "Since the Company has already given the effect of provisions contained in the scheme of arrangement in its financial statements ending March 31, 2023, in view of the same captioned scheme is being returned. "

Alembic Pharma reported muted nos, with sales growing by 8% and EPS largely being flat. They have started launching injectable, onco and derma products in US. Their non-US market is doing very well. Concall notes below.

FY24Q2

- 12MW solar plant commissioned in October 2023, ROI of 18-20%

- Animal health business has now scaled to 98 cr. quarterly run rate (32% growth). Business has grown at 18% CAGR in last 5 years. Established a new division with 350 people. Margins are a tad lower than corporate level profitability

- New facilities contributed 60-70 cr. to quarterly expenses

- Have seen very good pickup in oncology product in US, injectable product has also seen good market share gains without much price erosion

- Out of 20 planned US launched, 10-12 will be OSDs and remaining will be ophthalmic injectable and derma products

- US filing rate has reduced from 20-25 products to 15 now (will reduce R&D spends)

- Will launch 10+ products in US in H2

Disclosure: Invested (position size here, bought shares in last-30 days)

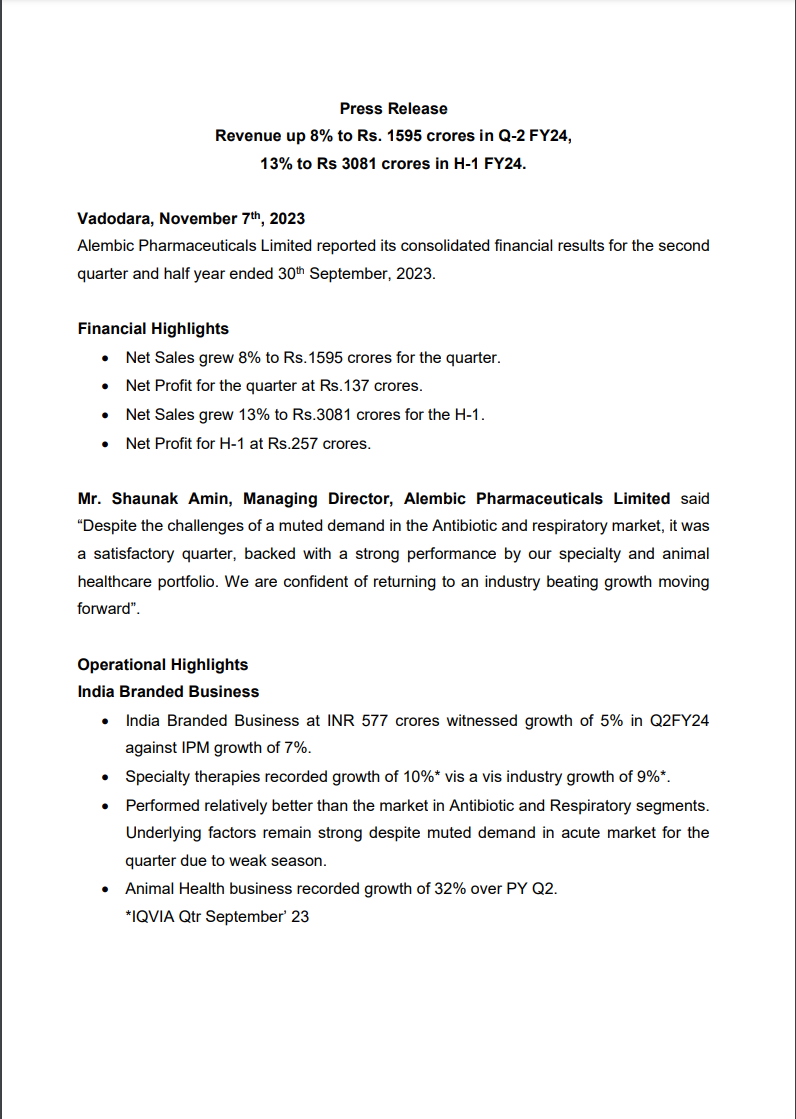

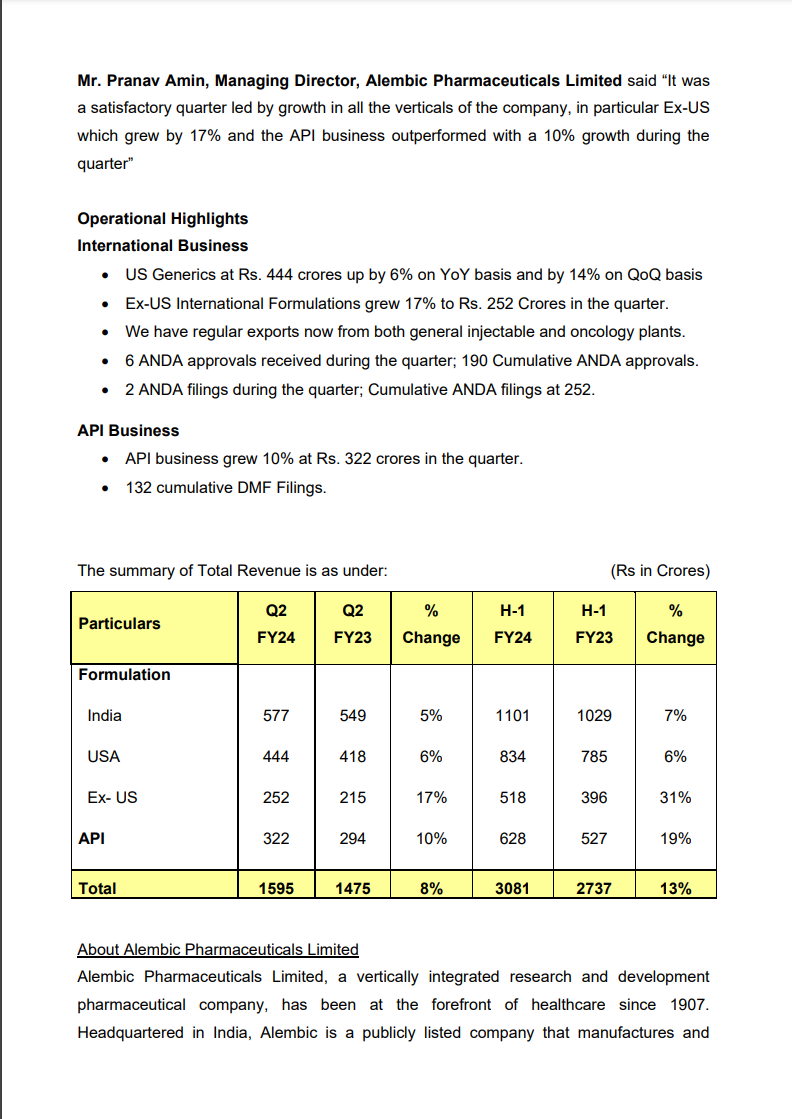

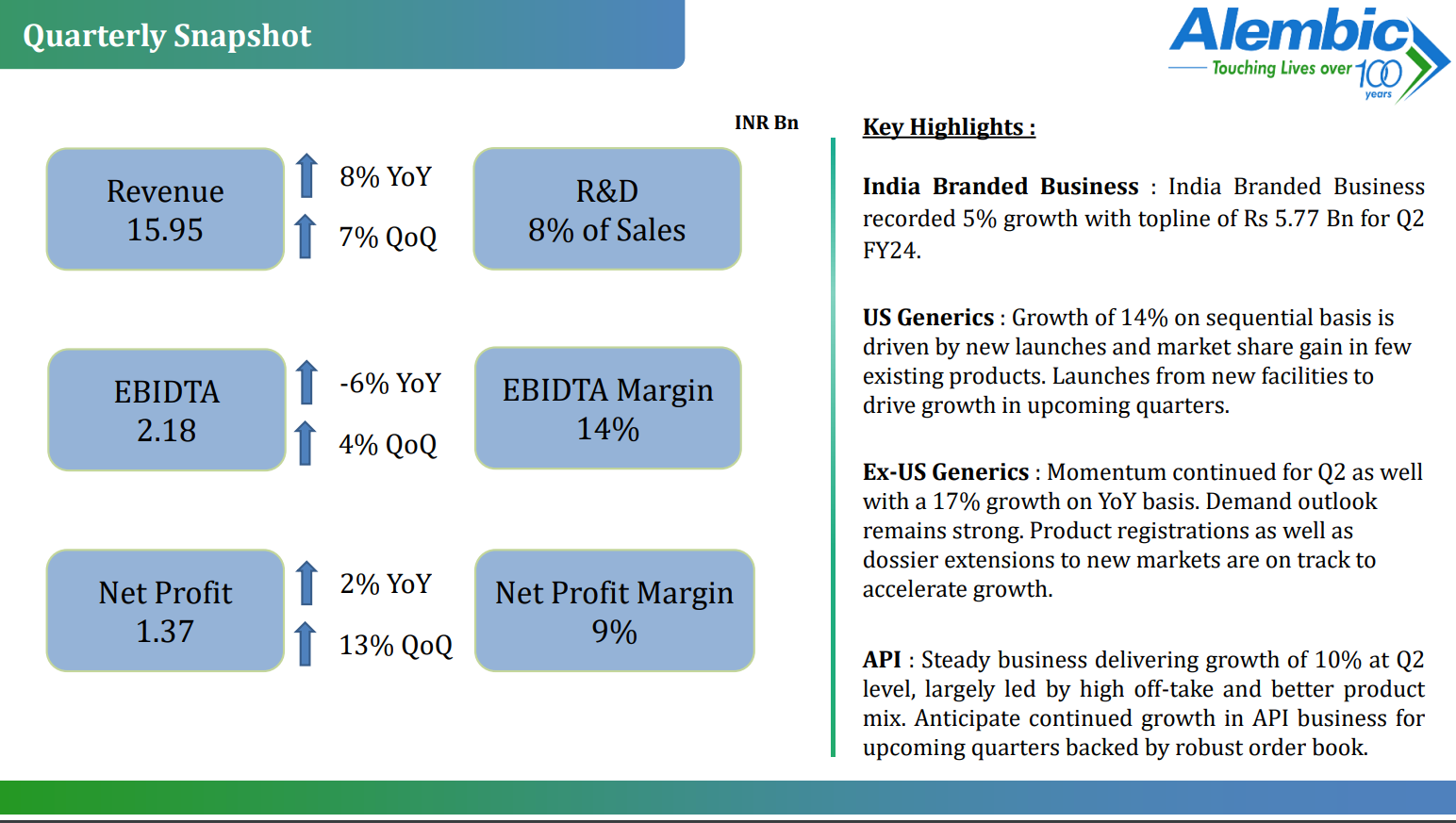

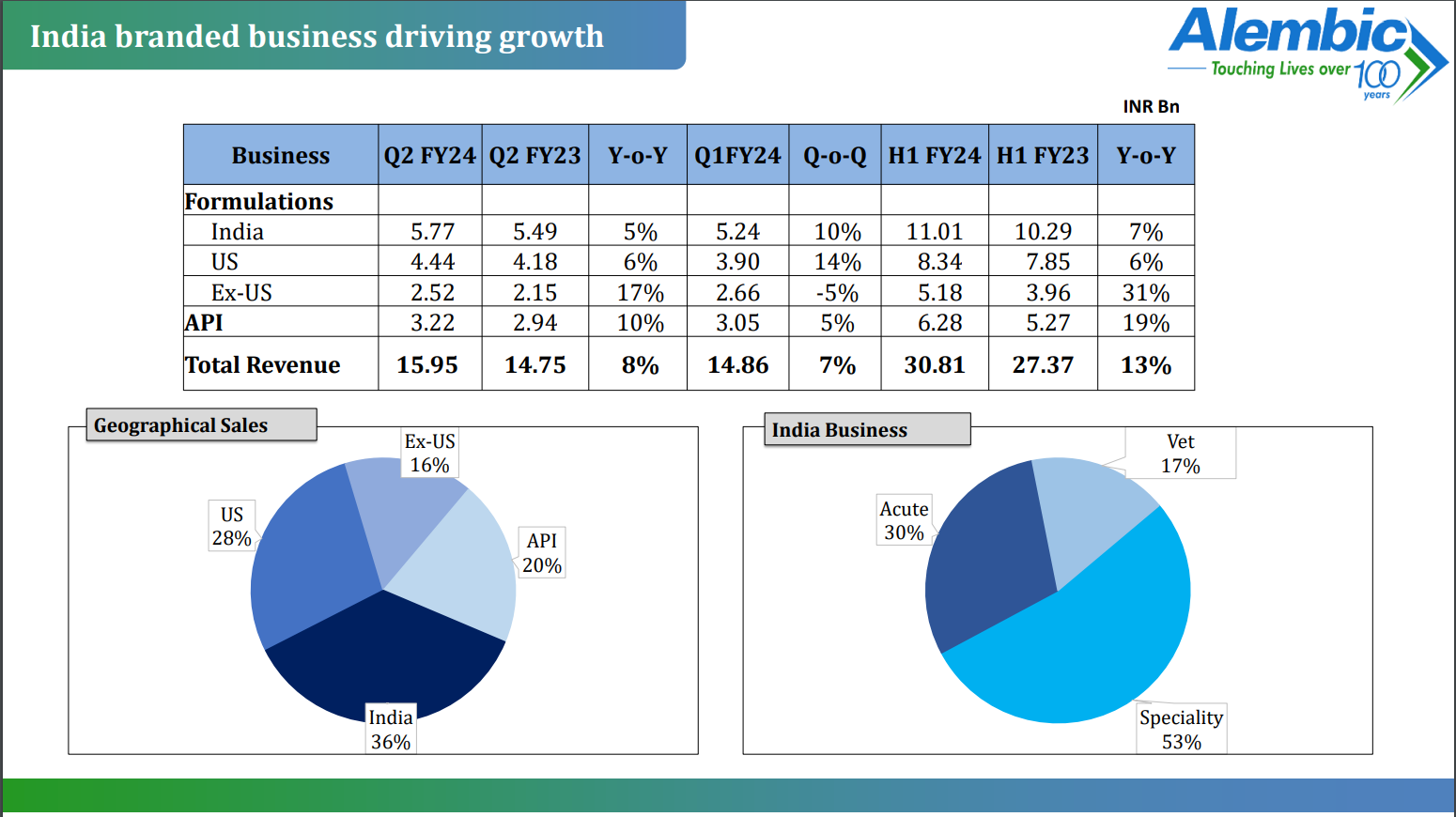

Alembic Pharmaceuticals Limited, released its unaudited financial results for the second quarter and half-year ended on September 30, 2023. Here is a detailed summary of the provided information:

- Financial Results:

- Net Sales for the quarter increased by 8% to Rs. 1595 crores.

- Net Profit for the quarter amounted to Rs. 137 crores.

- Net Sales for the first half of the fiscal year grew by 13% to Rs. 3081 crores.

- Net Profit for the first half of the fiscal year was Rs. 257 crores.

- Operational Highlights:

- Despite challenges in the antibiotic and respiratory market, Alembic Pharmaceuticals reported a satisfactory quarter, with strong performance in its specialty and animal healthcare portfolio.

- The India Branded Business witnessed 5% growth in Q2FY24, with specialty therapies growing by 10%.

- The company outperformed the market in antibiotic and respiratory segments.

- The Animal Health business recorded significant growth of 32% over the previous year’s Q2.

- The US Generics segment saw a 6% YoY growth and a 14% QoQ growth.

- Ex-US International Formulations experienced a 17% growth during the quarter.

- The company received 6 ANDA approvals and filed 2 ANDAs during the quarter.

- The API Business grew by 10% in the quarter, with 132 cumulative DMF filings.

- Total Revenue:

- The total revenue for the quarter was Rs. 1595 crores, an 8% increase compared to the previous year’s Q2.

- The total revenue for the first half of the fiscal year was Rs. 3081 crores, marking a 13% growth.

Alembic Pharma -

Company overview & Q3 FY 24 concall highlights -

Company’s manufacturing base -

Formulation facilities -

F1 @ Panelav - General oral solids

F2 @ Panelav - Oncology oral solids, Injectables

F3 @ Kharkhadi - General injectables, Ophthalmic products

F4 @ Jarod - General Oral solids

F5 @ Kharkhadi - Various Derma product forms

API facilities -

02 facilities at Panelav

01 facility at Kharkhadi

Company is ranked @ 20th position in the IPM

Supplying APIs to 60+ countries

Division wise sales mix for Q3 -

India formulations - 36 pc - 596 cr, up 9 pc

US formulations - 28 pc - 474 cr, up 9 pc

RoW formulations - 17 pc - 272 cr, up 32 pc

APIs - 19 pc, 326 cr, down 11 pc

India sales breakup -

Acute - 30 pc

Vet - 16 pc ( operating in Livestock and Poultry market )

Speciality - 54 pc

In India, 04 of company’s brands clock sales > 100 cr / yr

03 of company’s Veterinary brands clock sales > 30 cr / yr

No large capex is lined up for the US business in the foreaeable future

RoW growth driven by various partnerships that the company got into. Key RoW mkts include - EU, Canada, Australia, Brazil, RSA. Commenced ops from Chile. Aiming to expand to Mexico, ME and North Africa in near future

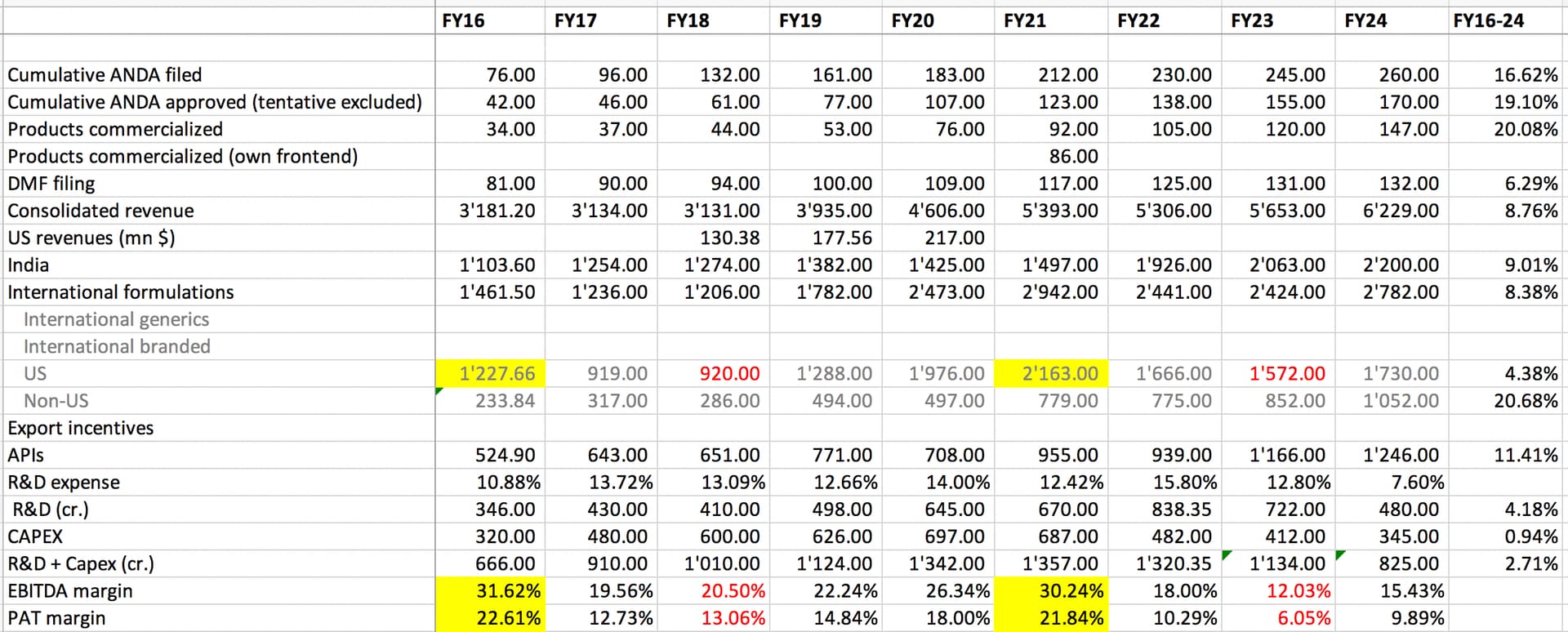

Company has been spending > 12 pc of their topline on R&D for last 5 yrs !!!

Veterinary and RoW businesses grew by 32 pc each in Q3

Company is sitting on a lot of operating leverage as its US facilities are under-utilised. As their utilisation goes up, return ratios, margins should get a good bump

Fall in API sales is due to slower off take by a few customers. Should correct in 2-3 Qtrs

Aim to launch 05 new products in US in Q4 followed by 10-15 launches in FY 25. These launches should help take the plant utilisation to higher levels

Company’s R&D focus these days is greater on Injectables vs Oral solids, Derma products

Company is working on GLP-1 products. These are complex generics. Launches are some time away

Company feels it has $ 230 million/yr kind of base business in US ( unless there r some major disruptions ). The Mkt is looking better now vs the last few yrs. The US business is already profitable

Disc: planning to take up a tracking position, biased, not SEBI registered

Business finally seems to be coming back on track (8% sales growth, 48% EPS growth). Reduction in R&D, lesser capex and new product launches has finally lent support to their margins. Concall notes below.

FY24Q3

- 5 products to be launched in Q4 (20 launches in 9MFY24)

- Animal healthcare business grew at 32% in 3QFY24 (24% CAGR in last 4-years) - headcount is 350 currently

- Believe that $230mn is base annual run rate in USA

- Have not got into long term contracts in USA because they don’t like the fine prints in these contracts

Disclosure: Invested (position size here, no transactions in last-30 days)

Q3 FY24 Earnings Conference Call of Alembic Pharmaceuticals Limited February 05, 2024

-

Specialty therapies performed better than the market. Gynecology, gastro, antidiabetic, and ophthalmology therapies outpaced the market growth

-

We performed relatively better than the market in antibiotics and respiratory segments on a higher basis in the previous year’s Q3

-

New launches continue to do well with promising future launches across key segments

-

Animal Health had a fantastic quarter and this is a business that’s been doing very well for us. It grew by 32% during the quarter

INTERNATIONAL BUSINESS:

-

We had a very satisfactory quarter with exceptional growth in the ex-US generics. The US business also grew 9% on the back of 11 launches. The US business is looking better right now with new facilities already commercialized. As they ramp up, we will get a lot of operating leverage, and cost improvements are also on track

-

There is no further large CAPEX needed for the international business and we will have only maintenance CAPEX as well as some API expansion, including in therapies such as GLP-1 and debottlenecking

-

The API business has been very strong for us over the last couple of years. The de-growth this quarter was due to lower offtake from a few select customers since it’s getting lumpy. I expect another quarter or two maybe weaker, and then we should be back to our regular growth rate that we demonstrated in the past

-

R&D expense was at 7% of sales at Rs. 114 crores for the quarter.

-

We filed 5 ANDAs during the quarter and cumulatively ended up filings at 257. We also received seven approvals and launched 11 products. We should launch about 5 products in the next quarter as well.

-

The U.S. generics business grew 9% to Rs. 474 crores for the quarter. The ex-US grew by 32% to Rs. 272 crores, and the API business grew by 11% to Rs. 289 crores.

Recovery continues for Alembic with them growing sales by 8% and EPS by 17%. Finally they seem to be getting closer to 20% EBITDA margins and have commercialized large number of products (27 in FY24, 25 planned in FY25). Concall notes below.

FY24Q4

-

7 products launched in Q4 in USA (27 launches in FY24). Expect to launch 25 products in FY25

-

Expect quarterly US sales of $50mn (lower than $55mn earlier guided) as there were one time opportunities in 3QFY24

-

Gross margins increased to 75% due to increased US sales in the US, R&D and other cost optimizations. Expects GMs to be 70%+

-

Expect 20% growth in ROW business. International business is now 40% of order book vs 20% earlier

-

API is regulated market business and higher margin than corporate margins

-

FY25 capex: maintenance (300 cr.)

-

R&D will increase to 550-600 cr. in FY25 (vs 480 cr. in FY24)

Disclosure: Invested (position size here, no transactions in last-30 days)

Alembic Pharma -

Q4 and FY 24 concall and results highlights -

Q4 outcomes -

Revenues - 1517 vs 1406 cr, up 8 pc

EBITDA - 260 vs 204 cr ( up 29 pc, margins @ 17 vs 14 pc )

PAT - 178 vs 153 cr, up 17 pc

FY 24 outcomes -

Revenues - 6229 vs 5653 cr

EBITDA - 932 vs 682 cr ( margins @ 15 vs 12 pc YoY )

PAT - 616 vs 342 cr

FY 24 Sales breakup -

India branded - 35 pc - 2200 cr ( includes the Veterinary business ) - grew by 7 pc in FY 24

US generics - 28 pc - 1730 cr - grew by 10 pc in FY 24

RoW formulations - 17 pc - 1052 cr - grew by 23 pc in FY 24

APIs - 20 pc - 1246 cr - grew by 7 pc in FY 24

India business -

Has grown at 11.4 pc CAGR for last 4 yrs

15 pc is under NLEM

Company’s 4 brands have sales > 100 cr

Total MRs @ 5000 +

16 pc of India sales come from Veterinary segment and 30 pc from acute therapies

Alembic is 18th largest Pharma company in India

Veterinary business ( operating in livestock and poultry segment ) has grown at a CAGR of 25 pc for last 4 yrs - now @ 355 cr / yr

US business -

7 products launched in FY 24 taking the total products launched to 147

25+ product launches planned in FY 25

No major Capex planned in next few yrs

Company’s base US business is about $ 200 million. Aiming to build up on this base

RoW business -

Has grown @ 21 pc CAGR for last 4 yrs

Company exports to - Europe, Canada, Australia,Brazil and South Africa

Currently ramping up operations in Chile, Middle East

APIs -

Supplying APIs to 60+ countries globally

( however, main focus is on regulated markets )

Has grown @ 15 pc CAGR for last 4 yrs

Future capacity expansion is on track

R&D expenses for FY 24 @ 480 cr @ 7.6 pc of sales

Current manufacturing base -

5 facilities - Formulations

2 facilities - APIs

Gross Debt now at 430 cr vs 620 cr on 31 Mar 23. Cash on books @ 120 cr

Company’s domestic business growth was mainly led by - gynae, veterinary, opthal, metabolic, GI, Cardio segments

Growth in anti-infectives, respiratory were tepid in the domestic mkts - pulling down overall domestic growth for the company

Expecting good ramp up and operational efficiencies to kick in for the US business in FY 25

Expecting strong growth momentum to continue for RoW business ( ie > 20 pc growth or thereabouts )

Confident of outgrowing the IPM for FY 25

Capex plan for FY 25 @ 300 cr or so - mainly towards de-bottlenecking and maintenance

As US business ramps up, company level EBITDA margins may to go 20 pc kind of levels due better utilisation of facilities ( provided there is no steep price erosions in US )

Disc : looking for dips in the stock price to start accumulating, biased, not SEBI registered, not a buy / sell recommendation

Key monitorable for Alembic Pharma shall be -

The pace of ramp up in US and RoW business - in order to better utilise their CAPEX done over the last few years

Extent of price erosion in US Mkt

Mkt share gains ( or mkt share losses ) in the Indian Mkt

Here are my notes from their AR24.

Manufacturing facilities:

-

All EIRs are in place

-

F1 (Panelav): Oral solids

-

F2 (Panelav): Oncology oral solids + oncology injectables

-

F3 (Karkhadi): General injectables+ Ophthalmic

-

F4 (Jarod): Oral solids + Oral suspensions. Transferred products from F1 to F4 to decongest F1

-

F5 (Karkhadi): Dermatology

-

Sikkim: Branded domestic business

-

Pithampur will come onstream in FY25 and complement Sikkim for domestic sales

-

3 API plants (2 in Panelav, 1 in Karkhadi)

US (sales: 1’730 cr., growth @10%)

-

Launched 27 products (15 were from new facilities), filed 15 ANDAs (12 complex filings), got 15 final approvals, filed 1 DMF

-

10 injectables launched so far

-

Reduced annual ANDA filings from 20-25 earlier to 15 now, product mix is changing to complex products

-

7 oncology product filings awaiting approvals

-

Filings catering to new therapies (oncology, dermatology and ophthalmology) and new platforms (injectables and inhalation) it stood 12 filings (out of 15 filings) in FY24. In FY25, the filings for these products and platforms will be ~14

-

54% of development pipeline for the US comprises non-OSD products

-

Made a meaningful entry into the peptide space with 2 ANDAs filed and setting up a kilo lab for peptide APIs

Non-US generic (sales: 1’052 cr., growth @23%)

-

14 launches in FY24

-

Will launch 25+ products in Chile in FY25 expanding product basked to 30+. Expect to start operations in Mexico in 2026

-

Received orders for 2 injectables from Malaysia and Chile which will be launched in FY25

-

Setup subsidiary in UAE with a scientific office. Filed 20 products in UAE and hopeful of securing approvals in 12-18 months

-

Have presence in 41 countries

-

Their strategy of developing B2B model has worked well in Europe

-

Favorable regulatory tailwinds in Australia helped them grow volumes

Domestic business (sales: 2’200 cr., growth @7% vs 8% for industry)

-

12 therapeutic areas, 20 marketing divisions, 5000+ MRs catering to 2.33 lakh doctors (vs 2.31 lakh in FY23)

-

Launched 15-20 new products

-

1.5% market share, 4 brands generating 100 cr.+ revenues, 9 leading brands, 69 brands above 10 cr. sales

-

MRs 5000+, gave iPads to MRs and upgraded to SalesForce

API (sales: 1’246 cr., growth @7%)

- 33% captive consumption

Animal healthcare

-

Created a new division for livestock products, 71 products launched in speciality and animal health spaces in FY23 and FY24.

-

Expanded team to 350 people

R&D 476 cr. (vs 731 cr. in FY23)

-

Investments in API, injectables and ophthalmic will increase

-

Largest investment in FY25 will be on peptide-based formulations and APIs for Para-IV filings

-

6 new technologies such as powder drug layering, laser drilled osmotic drug delivery, spray drying, hot melt extrusion, wet milling using Dyno-mill and dry granulation using roller compactor were introduced

-

New technologies to manufacture various dosage forms are through the technology of sterile powder namely lipid-based liposomes and polymer based microspheres. Nanoparticle delivery system technology is also introduced that uses nanoparticles for targeted administration and controlled release of therapeutic agents. Device capabilities have been introduced for manufacturing pre-filled syringes, pre-filled cartridges, pens and auto-injectors both upstream and downstream

-

800+ R&D team

Capex (345 cr.)

-

Capex cycle is over fulfilling demand over next 3-5 years, expect good free cashflow generation

-

Setup 12MW solar power plant for Panelav unit, setting up 11MW solar plant at Karakhadi in FY25

Miscellaneous

-

Employees : 14’858 (vs 14’593 in FY23)

-

KMP + close person remuneration: 75 cr. (vs 48 cr. in FY23)

-

Related party purchases from Shreno Publications: 50.95 cr. (vs 43.31 cr. in FY23)

-

CSR : Spent 13.19 cr. (transferred 2.94 cr. of obligations in April 2024)

-

8% increase for non-managerial personnel and 65% increase for managerial personnel (there was no commission paid in FY23 which was reinstated resulting in higher payout to KMPs)

-

# shareholders : 78’191 (vs 101’761 in FY23)

-

Auditor remuneration : 1.39 cr. (vs 1.3 cr. in FY23)

-

Tax liability : 13.22 cr. (vs 1.77 cr. in FY23)

-

Contingent liability : No major liability except corporate guarantee of 40.69 cr. (vs 106.72 cr. in FY23)

Disclosure: Invested (position size here, no transactions in last-30 days)

Q1 concall notes

FY25Q1

-

US grew by 18% , had 2 launches during Q1 and expect to launch 10 products in Q2

-

Will add OSD capacity to address the immediate demand in international markets

-

Seeing double-digit price erosion in US

-

India : Created new divisions in Gynac and Cardiac, MR count increased to 5,500+ (PCPM : 3.8 lakhs)

-

API decline of (-15%) was because of lesser supplies to a customer who got into FDA issues and lost market share

-

Animal healthcare continues doing well, growing by 23% . They now have 5 brands with 30cr.+ sales

-

Gross borrowings increased to 589 cr. (vs 430 cr. in March 2024)

Disclosure: Invested (no transactions in last-30 days)