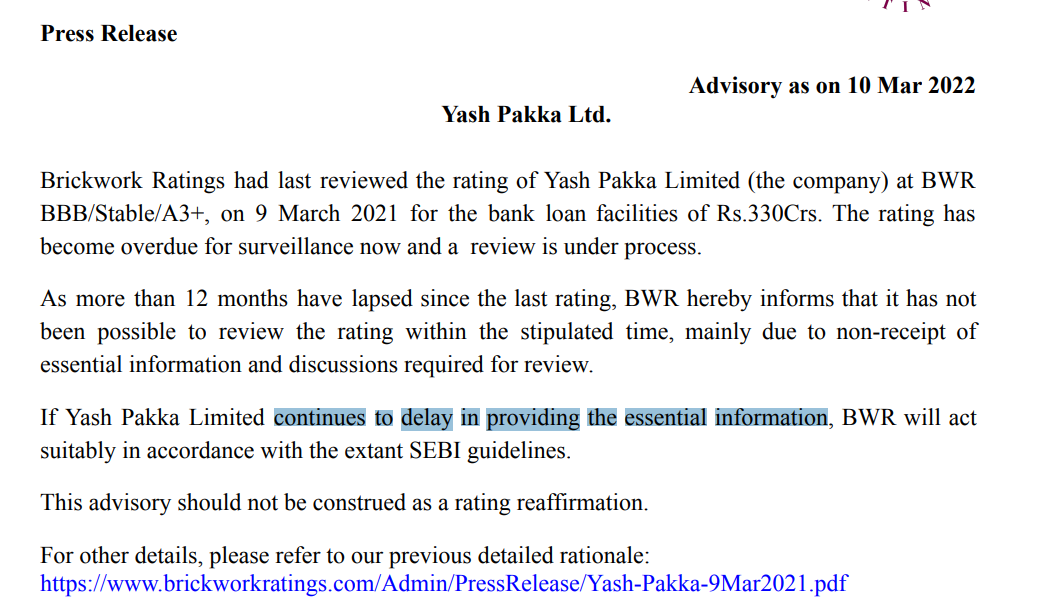

Not co-operating with Rating agency??

Based on my understanding, Company has decided to shift rating agency and, from now on, get it’s rating done by CARE.

Its a usual process followed by old rating agency before they withdraw their rating. new agency assigns rating.

1 Like

As far as I know it is not mandatory to provide the renewal fees / updates to any rating agency.

All the companies who hires these agencies go for Issuer Pays model.

Issuer pays model : Currently, the credit rating agencies follow the ‘issuer pays model’, under which the entity issuing the financial instrument pays the agency upfront to rate the underlying securities. However, the Committee observed that such a payment arrangement may lead to a ‘conflict of interest’ and could result in compromising the quality of analysis or the objectivity of the ratings assigned by the agencies. Therefore, it suggested that the Ministry of Finance or the regulators may consider other options as well, such as ‘investor pays model’ or ‘regulator pays model’ after weighing the relevant pros and cons. Alternately, within the existing framework, the appropriate rating fee structure, payable by the issuer may be decided by SEBI, in consultation with RBI and the credit rating agencies.

There is big debate on this model and there is a committee formed to come up with some better model. When a company hires a rating agency on “issues pays model - aka company pays the fees” to review their books and issue a rating. With this ratting, companies goes and negotiates for a better deal with the banks / FI

The recent ILFS fiasco is a best example why it is not enough to believe these rating agencies

4 Likes

Investment of 5Cr. in Pakka impact ltd.

Disclaimer: Invested

3 Likes

Am not invested, but I found this video related to this co. May be useful to a few of the VP friends.

4 Likes

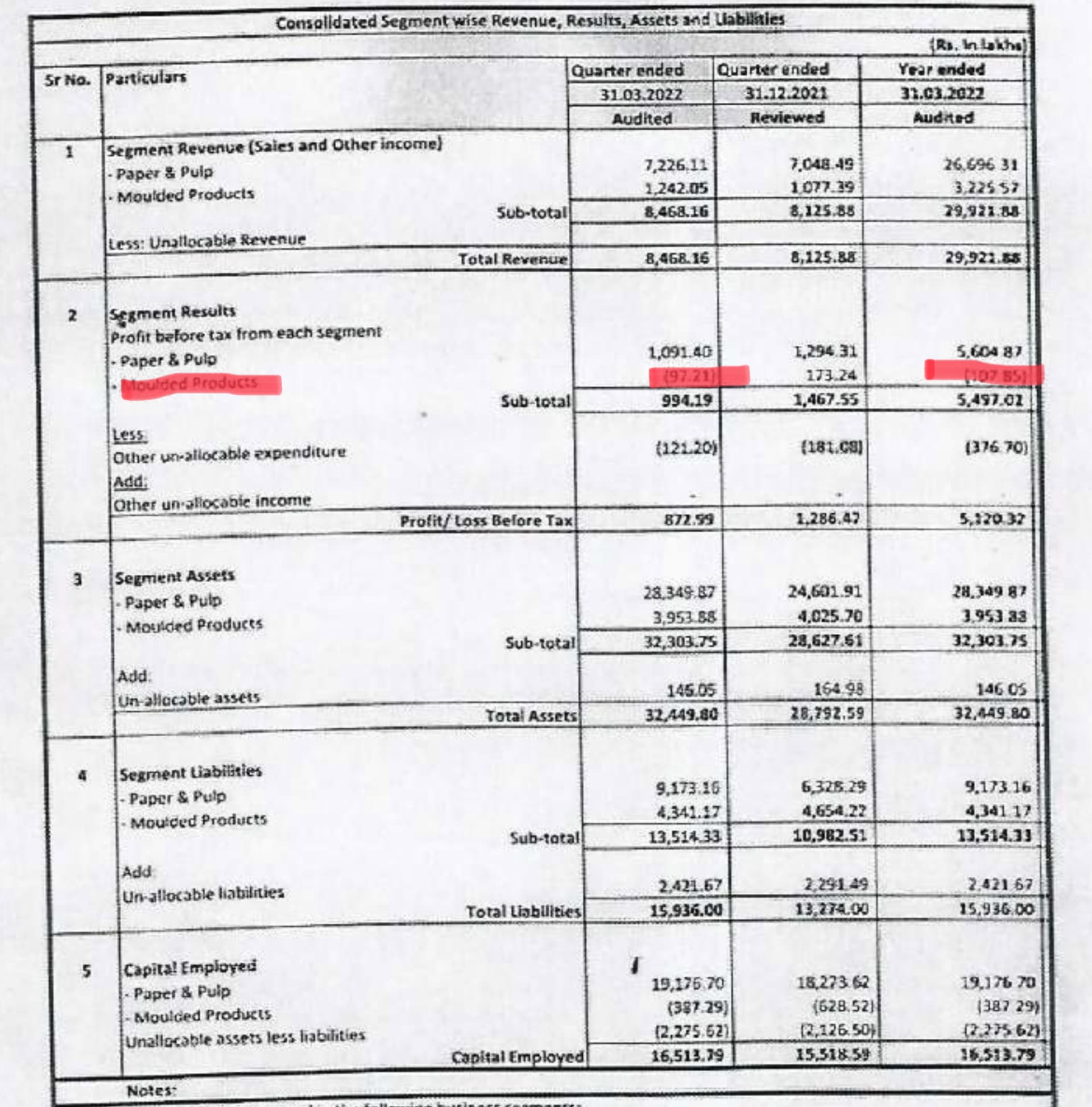

Results are below expectations

promoter pledged shares released

1689c711-a495-4a70-8a20-6d45c8f15cdd.pdf (1.1 MB)

Not so good results from Yash Pakka.

Moulded products has to turn positive for super performance.

Dividend of 2.00 Rs declared, 80 Rs stock price have 2.5% dividend yield - Down side may be protected??

But I am not sure y they give dividend, when require money to grow business. May be I can think of - to release pledge shares, which they have done from above post.

Let’s wait for Concall details.

Disclosure: Invested

3 Likes

YASH PAKKA Q4 Fy22 Concall Notes:

Investor Presentation Q4Fy22

https://www.bseindia.com/xml-data/corpfiling/AttachHis/07a6195e-8f03-40ef-a7b8-4a562806ce58.pdf

- [ ] Refer Investor presentation for Highlights:

- [ ] Commentary:

- [ ] Goals - very big and ambitious, only if v can execute. Big break through/achievement in Flexible packing like potato chips packaging, building bigger capacity.

- [ ] Another innovation v r working-mineral based compostable carry bag from minerals/pellets and bio waste.

- [ ] FY 23 : Around Capex 200 Cr, Sales Target - 500Crs

- [ ] FY 24 : Around Capex 500 Cr, Sales Target - 700Crs

- [ ] The above will be to achieve 2500 Cr turnover by 2025/26.

- [ ] Talking to every big FMCG company, all r talking, visiting our sites, in US also, clearly seeing a lot of focus on sustainability packaging.

- [ ] Broad Focus Areas- FOOD Packaging, Food Carry & Food Servicing in the next 5 years.

- [ ] Build a Strong Team - Business Heads : Paper+Pulp, Compostables(Moulded Products), Innovation, Technology (Refer GCAIMPACT.COM, GCAHUB.COM) & in Investment areas - Refer Slide 11 in Presentation.

- [ ] PakkaPTE - New subsidiary formed in Singapore.

- [ ] Key Actions in 2022 : Refer Slide 12 in Presentation.

- [ ] Ayodhya Plant (2 years delayed) Basic Engineering Finalised, Equipment ordered, finance to be finalised in this current quarter and moved ahead for this project.

- [ ] New site finalisation for Bagasse (probably outside India)- Next 6 months will be announced, in advance talks.

- [ ] Moulded Products (new ones??) - Done Beta launch, will launch at scale within year, Franchisee partnership for moulded products - supply pulp, will see big growth there - Refer below Q& A.

- [ ] Performance FY22: Highest ever production in Paper, pulp and Moulded products. Highest ever exports (10131 MT vs 6976 MT in FY19) - Refer slides 13/14/15/16.

- [ ] Merger completed, Pledge shares release approved by lead banker, Team Stock options plan approved, Innovation centre in Bangalore.

- [ ] Revenue from US entity will come from end of FY23(??). Good will of around 4Cr accounted during/for merger/consolidation process.

- [ ] Q & A :

- [ ] Input Costs: 24% Impact for Fy22, impact is sudden, not fully taken this year because order book is already there, going forward from Q1 some of the input costs will be considered/mitigated from pricing front. Out look for input costs still going up - Natural gas/Ukraine conflict.

- [ ] Bagasse also got hit on input pricing front, we already have/purchased Bagasse for this whole year( v purchased in 120 days(seasonal) for whole of next year FY23) so already input cost accounted for FY23. Margins may be better in Q1FY23 vs Q4FY22. Some impact on Borrowing/working capital requirements from the above input cost.

- [ ] On US operations:

- [ ] 1.Building the Team, identification of Site (New Factory) and Funding of the project. No income may be next two years from this.

- [ ] 2.North American market : Deep dive/Outsourcing model is being worked out in this quarter/Transport pulp longer distances - In 6 months partnership finalised. Make/supply products in a year, Revenue may be next year.

- [ ] 3.Innovation partnerships: Talking to large MNC/joint collaboration/fund rising etc….equity + Debt in US subsidiary.

- [ ] Innovation in Flexible Packaging: First in market/Patented?? Mineral Based Packaging??

- [ ] Lot of work done in flexible packaging, lot of trails done with lot of costumers, v r not the first one here, in India scenario probably v r first one, trying to bring out the balance between availability of materials/performance and the cost, Target is in 6 months v will have the product/customer/trails/ and in the market. Strong process followed.

- [ ] About Mineral pallets - Using industrial waste from our factory, trying to convert into pallets, which can be blown film into different bags, v can make prototype of this using bio polymer, very few companies doing outside India, no one in India is doing as far as they know, may or may not go for Patent as it may be get copied.

- [ ] What is the USP of this mineral product - Performance and Machinability of the Product is very strong and confidence to customer. Final product - Strong Base Paper will developed which can be sent to converter industry/coating and lamination in house???

- [ ] Substantial Turnaround of CHUK - two/three different things in working as v speak - Additional capacity through franchise manufacturing, Expect one Hope fully by next quarter (Q1 or Q2 ??), Launching newest line of products in the next quarter (Q1/Q2 ??) like (??)containers, also existing products ramp up, pretty exciting, quantum jump/leap hopefully in the next one or 2 quarters.

- [ ] May not savvy to meet DII or FII - Only on need basis if required only if it helps.

- [ ] Other Paper Industry companies had Sales realisation 15/20 % in Q3/Q4, but not for Yash Pakka ?? Different products/markets??

- [ ] All companies using different raw materials/requirements and also products (Satia - wheat, JK - wood based) in writing & printing paper, board paper, In different Market.

- [ ] We don’t look ourselves as Paper makers any more - More of sustainability Packaging- Every product v make as to have innovation with a solution - Brilliant answer.

- [ ] Plastic ban by July1st happens it will definitely helps, if not also no impact on business.

- [ ] Capex of 200 Crs how r u spending:

- [ ] 1. Improve Paper machine 3 and make it much better flexible packgae base called MG bleached/grease paper (not sure here terminology ??)

- [ ] 2. Another paper machine in Ayodhya for another Butter Paper or grease proof paper, used for flexible packaging.

- [ ] 3. Expand pulp significantly to support moulded products/franchise manufacturing.

- [ ] 4. Hopefully some for Mineral pellets commercial manufacturing in the next 6 months, if at all it happens?? - Palletisation mineral facility.

- [ ] 5. Upwards/more than of 200 Crs. for above in Ayodhya site - Debt/Equity or Stratergic investor?? - around 18 - 24 months project??

- [ ] Outside India Capex - Big plans of USD 200 Million for new site/factory, very initial stage planning?? - Refer commentary and US operations above.

- [ ] On Franchise Manufacturing of Moulded Products : Developing comprehensive frame work. Looking for partners with experience in Pulp/paper industry. Yash will provide Pulp/process engineering/Product management/operational hand holding till stability/buy back the capacity/product by increasing demand. Pay back for franchise will be around in 5 or 6 years of their investment.

- [ ] Zomato Partnership: Big focus Area - Still failing in producing/supply/manufacture in large scale, still in W.I.P. Zomato still patiently waiting for big launch, Hopefully in one or two quarters - may be v can see light at the end of the tunnel.

- [ ] Lead free Products (?? in Flexible packaging or in Moulded Products??) - Design/performance/testing done by key costumers - Unable to manufacture at scale. Still in trail and error, Hopefully in one or two quarters.

- [ ] FY23 Target of 500 Cr - From Moulded products - 100 Crs, Other 400 Crs from Pulp and Paper, better capacity utilisation/scaling of operations, Hopefully - This is the target v have chosen : we will give our best shot to achieve this.

- [ ] Other expenses in Q4: Mainly write up of 2 Crs, one time, impair of old assets, another is travel expenses increased post Covid.

- [ ] Pledge Shares Release - Lead Banker agreed, only procedure formality by 15 June.

- [ ] My Comments :

- [ ] They are Still in W.I.P - Still struggling to produce/manufacture in scale, trying to make quantum jump and perfect products.

- [ ] Still in cautious/dilemma about big Capex spend/ being finalising plans, may be from previous experience/struggle before committing/confirming to market.

- [ ] But Hats-off to them and their thinking, being a micro/small cap - Saying “we are not a paper company anymore but a sustainable package solution provider/innovator”. Their Margins are supporting this, improving from 15 to 22% over the last 10 years.

- [ ] Let’s C when they deliver the products from incubation - start crawling/walking and up running - Long way to go.

- [ ] Might have missed some points - So Take with some Sugar and Salt.

- [ ] Disclosure - Invested, Not SEBI Registered. Read/Understand/Invest at your own Risk.

5 Likes

Promoter Issuew in Yash Pakka

Promoter Issues .pdf (1.9 MB)

Pledge, Issue Warrents, Get Morey shares again pledge.

Seems management more interested to fill their own pockets vs creating value for shareholders

6 Likes

Its a very insightful post by you and clearly highlights the corporate issue in the company. This can be the reason that the market is not willing to pay high PE or atleast the industry-par PE to the script.

Share Warrants:- Promoter Ved Krishna allotted share warrants to himself during the year

2016 at the price of 15rs per warrant. 75,40,000 equity warrants were issued aggregating to

`11.31/- crores.

Share price of the Company in 2016 was hovering at around Rs 15-20.

All the pledges have since been released.

Can you please provide pledge details where it has been mentioned that the pledge by promoters was for their personal use.

Hi Value 2017. Good question you have put you.

This is as per 24th Feb 2021 conference call

Management here says the loans taken are for the expansion of the business and now they understand the investor concerns and are working to de-pledge the same. Note this was feb 2021.

Nothing has been done as the numbers do not connect with what they said.

Today around 15 months since they have been trying no de pledge yet.

The rise in equity was mainly due to the conversion of warrants. 10 FV + 5 rs premium that is 15 bucks as stated earlier.

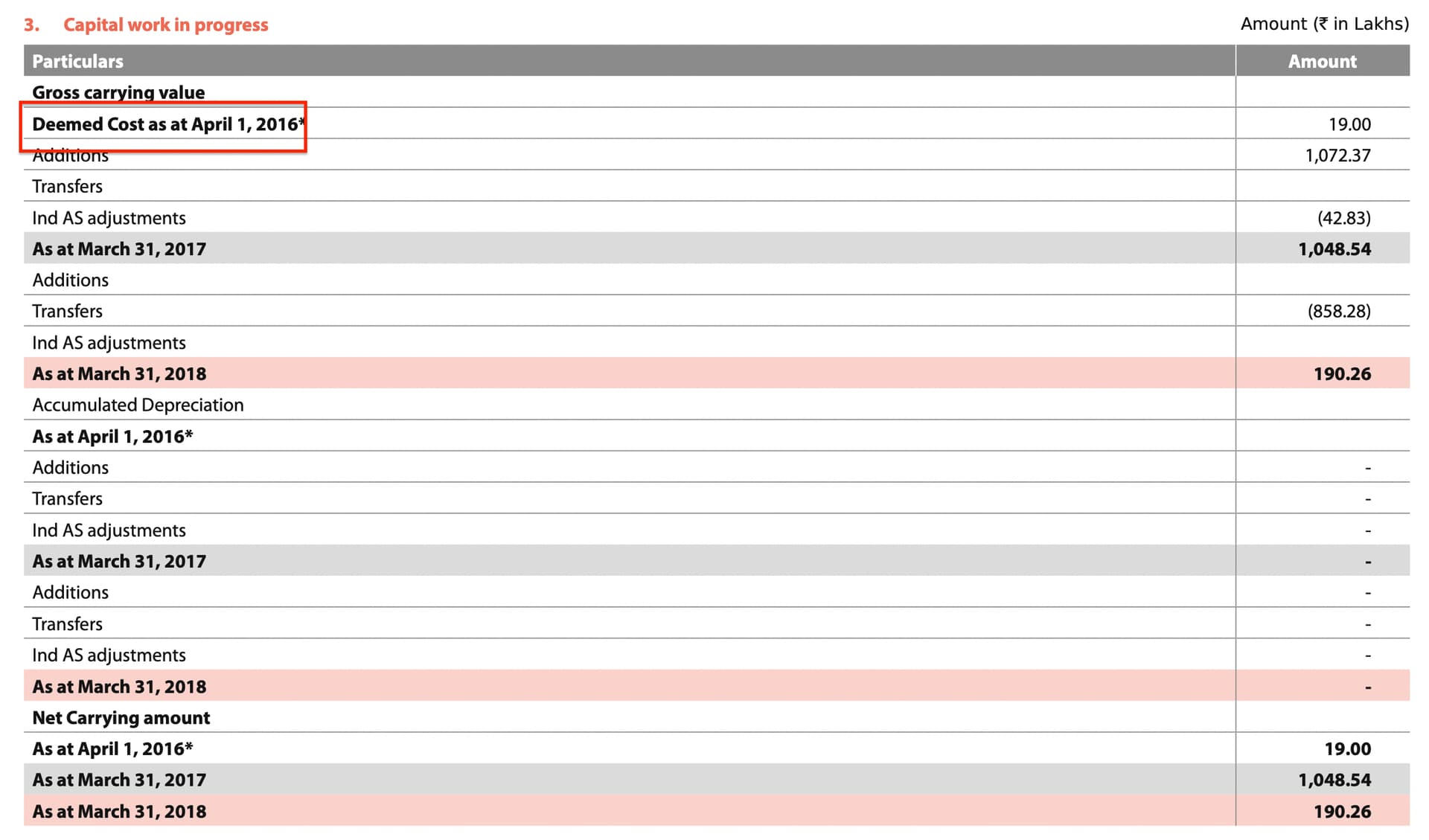

The increase in the assets was roughly 60-70 crores. In the same period the stock price went from 15 bucks to 60 bucks.

How did this fixed asset block move up. With investments in the business. ?? Looking at the said data in their annual report its difficult to understand.

In a nutshell if the share pledge was done for doing investments in the business. The assets have been adjusted IND IAS taking deemed cost of assets as on 1st April 2016. Then what was share pledge done for. Secondly managment is trying and been 14-15 months after trying attempts nothing has been done.

Some snippets as per my limited understanding whey the promoters might not have used the funds in the business as per my earlier post.

Thank You

5 Likes

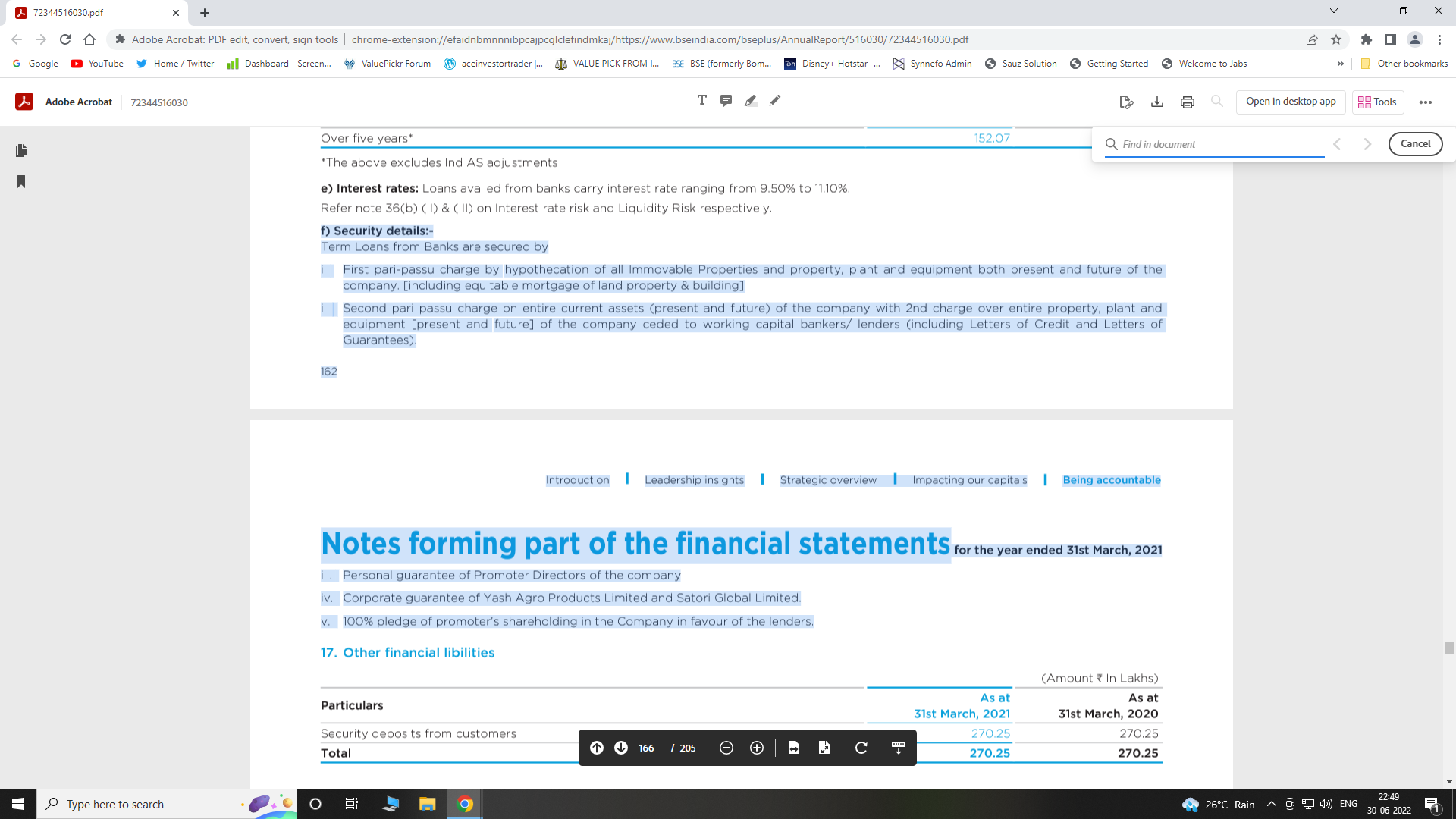

As per above AR 2021 and also old ARs, promoters have provided personal guarantee for loans and security.

Also try to match cash flow for particular year of conversion of shares and addition of fixed assets it looks like it is matching.

Promoters again have increased shareholding by merging Yash compostable to yash pakka.

1 Like

Its not getting clear, what you want to say. Its very much eveident and repeated multiple times in the Concal that pledging of shares was with lenders against the debt taken by the Company. the Company also confirmed in recent concall that the lead Bank SBI has given their consent for release of pledge and that the same will be released once other formalities are complted. Furhter for your clarification ,Lenders even ask for pledge for working capital limits also.

Disclosure : Invested since last 9 months at the level of 85 and 2% of my portfolio.

4 Likes

Short note on Yash Pakka Limited

Yash Pakka Limited.pdf (877.4 KB)

6 Likes

Informative and helpful article covering imp aspect of management. Thanks for sharing.

Disc: Not Invested

1 Like

Can anyone share latest concall link? Lik shared by company is not working .

1 Like