The segment CHUK, on which people are betting on, is not growing. In last quarter it was flat QoQ with losses increasing to >2cr. Not a great play unless Chuk shows growth. It’s a story stock I believe and better to wait till Chuk starts contributing to bottom line. At this initial stage, Chuk should have shown exorbitant growth both YoY and QoQ

1 Like

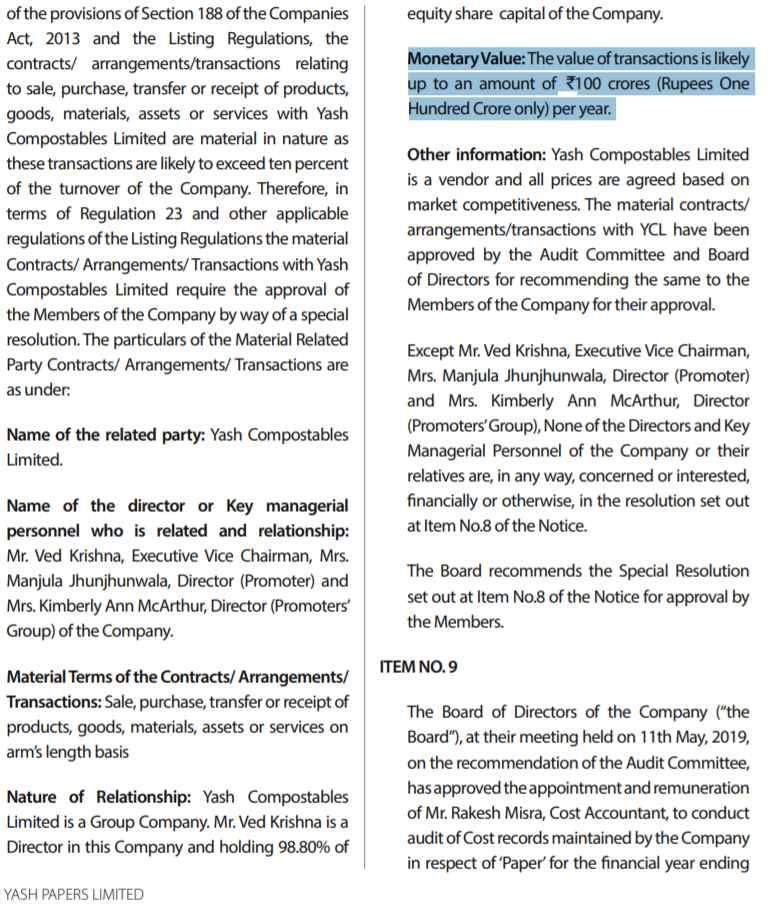

Looks like Yash Compostables Limited (which I presume distributes and markets Chuk), a promoter entity has been enabled to transact with Yash Papers upto 100 Cr/year. Is this another case of SKM Marketing and SKM Egg Products? How will Yash Papers shareholders see any returns if the Yash Compostables squeezes their margins?

3 Likes

Just for the benefit of everyone on this thread. I recently attended the Paperex 2019 in Delhi where they (Yash Pakka Limited) had a stall. They have launched 2 new papers - one for food packaging and other for carry bag. It appears from the conversation that there are no other Indian players who has come out with such quality of papers.

Disclosure: Invested.

3 Likes

Hi Amit,

Whats you view on recent price correction. I found in past 1 year 3 CFO resigned…

Regards

Sitansu

1 Like

Well its a personal opinion, of course; But looks like weak performance of tableware division is more the reason of the fall, rather than CFO resignation. Overall results are better because of the better performance of the paper division.

how good are they in cost comparison to other alternatives ?

Based on some industry feedback, it seems there are lot of cheap alternatives getting imported from China. No doubt the concept and quality of the products of this co are great but I’m not sure if India is ready as a market for mass adoption. Despite good PR and some success by way of bollywood endorsement, the sales are stuck at 5-6 Cr quarterly rate and at 25 Cr annual sales, the company would be making losses. Capex done was 60 Cr+…so they need to come to 40-50 Cr turnover run-rate to get some returns. Luckily paper industry is doing well and good profits in the other segment can take care of the drag. Would be important to understand the growth strategy and potential for this segment.

Ayush

PS: No holding

9 Likes

A lot of insights in this blog-

About their cost competitiveness with ECOWARE.

Business cycle of the paper industry ( where we are)

On Related Party Transactions -

and much more -

1 Like

the company is looking like a turnaround story.however, there are few areas which we need to look deeper than just sales numbers. the sale has been fantastic and grown at 20%. and while the costs looks as if it has been curtailed, as a % of sales it is in the 81-82% range in both 2018 and 2019 ending FY.

from the balance sheet, we have the below growth in sales volume in 2019 over 2018

| SALES | 2019 | 2018 | % CHANGE |

|---|---|---|---|

| KRAFT PAPER | 21098 | 19278 | 9% |

| POSTER PAPER | 17799 | 16998 | 5% |

| PULP | 7428 | 7429 | 0% |

| MOULDED PRODUCTS | 1150 | 119 | 866% |

| EGG TRAYS | 10185000 | 8228600 | 24% |

| TOTAL MT | 47475 | 43824 | 8% |

the total volume in MT has grown at a modest rate of only 8%. only moulded products or tableware has grown but its production started in feb 2018 only. so what caused this 20% jump in overall sales. for this looked at the revenue breakup.

2019 2018

PAPER SALES DOM 161 146 10%

PAPER SALES EXP 41 25.5 61%

PULP DOM 27.86 25.92 7%

EGG TRAY DOM 2.53 1.94 30%

UNIT PRICE PAPER 52 47 10%

UNIT PRICE PULP 37.51 34.89 7%

UNIT PRICE EXP 58.8 45.2 30%

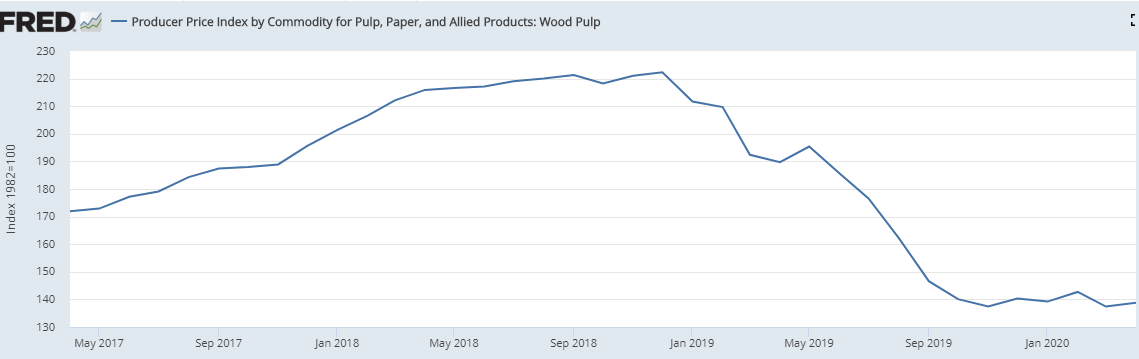

with this we can clearly see that domestic sales of paper and pulp has grown at a very modest 7-10% range. the driver has been export sales of paper which has grown by 61%. this is also true if we see the volume growth.

| EXPORT KRAFT PAPER | 4426 | 3766 | 18% |

|---|---|---|---|

| EXPORT POSTER PAPER | 2541 | 1875 | 36% |

| 6967 | 5641 | 24% |

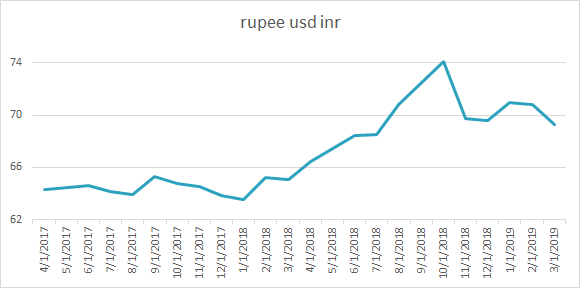

and one other factor which greatly helped the export sales was the deprecitating rupee and increasing price of paper. we can see rupee depreciated and the price of paper appreciated.

depreciating rupee

appreciating paper and pulp prices

However, the appreciation in paper and pulp prices seem to have tapered off. and the rupee only has depreciated further. i think when the new annual report comes out, we will see a growth in export volume and helped by depreciating rupee will offset this decrease in prices.

but we must remain cautious. clearly, the paper and pulp sales are growing domestically at a moderate rate. the tableware division really needs to turn things around for Yash. they are doing a capex of some 60 odd crores to enhance the tableware production so would be interesting to see if they can make it work.

3 Likes

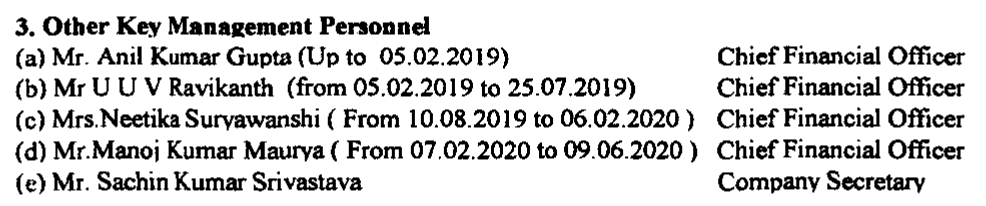

Why do CFOs of Yash Pakka keep resigning within a year? I have been seeing this trend for past 2-3 CFOs.

Another CFO resigned. https://www.bseindia.com/xml-data/corpfiling/AttachLive/3eae51b4-6793-48b0-96c3-c6bf13d4c728.pdf

4 Likes

Surprisingly the company secretary has remained the same.

4 CFO’s joined and left in 1.5 years. Taken from Yash pakka’s recent filing on BSE - https://www.bseindia.com/xml-data/corpfiling/AttachLive/ba6baf49-021f-4832-9fb7-05445c2b6e63.pdf

3 Likes

Latest Concall Update

Concall Dec 2020

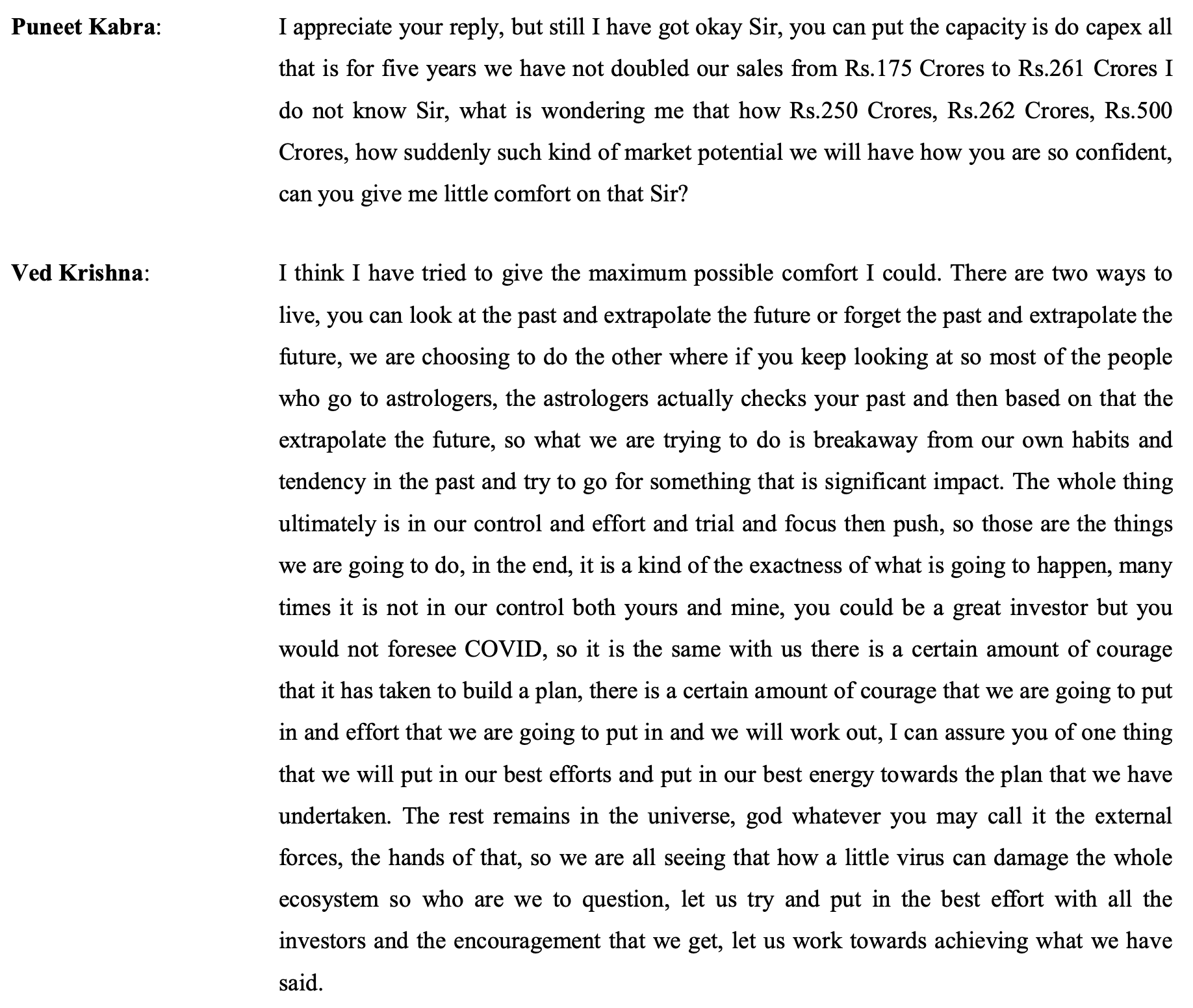

Ved, the MD, couldn’t give a satisfactory answer to the question about how revenue would suddenly increase to INR 500cr from ~ INR 200cr (FY 21 proj) or INR 261cr (FY 20)

3 Likes

Any views here:

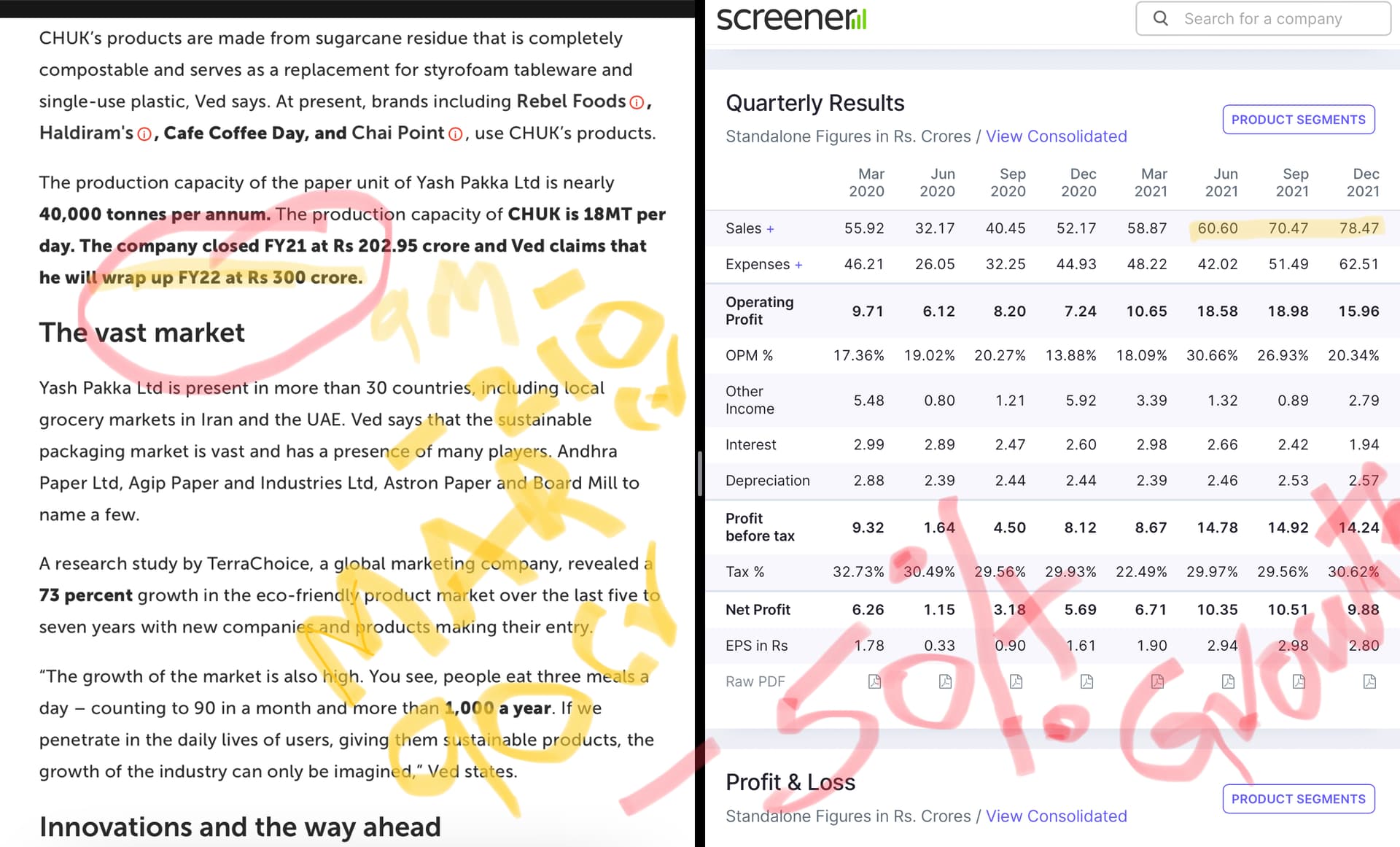

Today Randomly opened their AR - Just blown away by their 2025 targets:

-TTM sales 212 sales and 26 Cr profits.

-They are targeting to make 1360 sales with 240 Cr profit by 2025

-Present Market Cap around 305 Cr.

Source Q1FY22 Presentation and AR2021:

&

AR-FY2021

Q4FY21 Concall:

Capacity expansion, Capex Planned: 240 Cr, 75/25:Debt/Equity

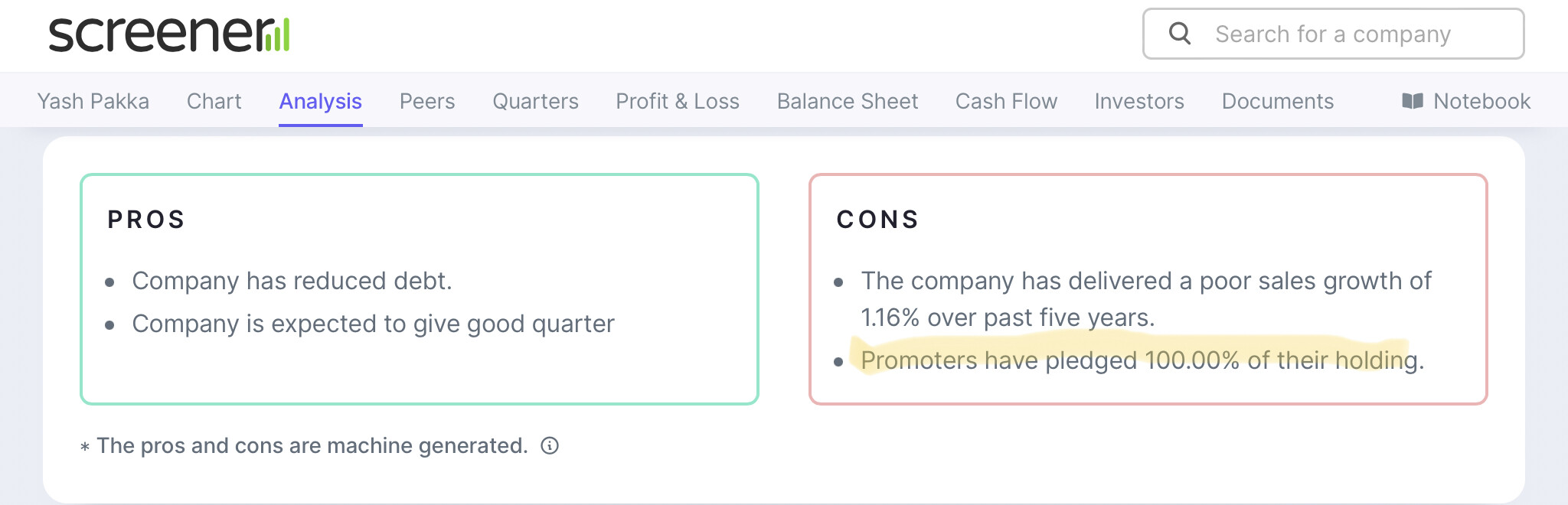

Note: All Promoter holding of 45.15% is pledged.

2 Likes

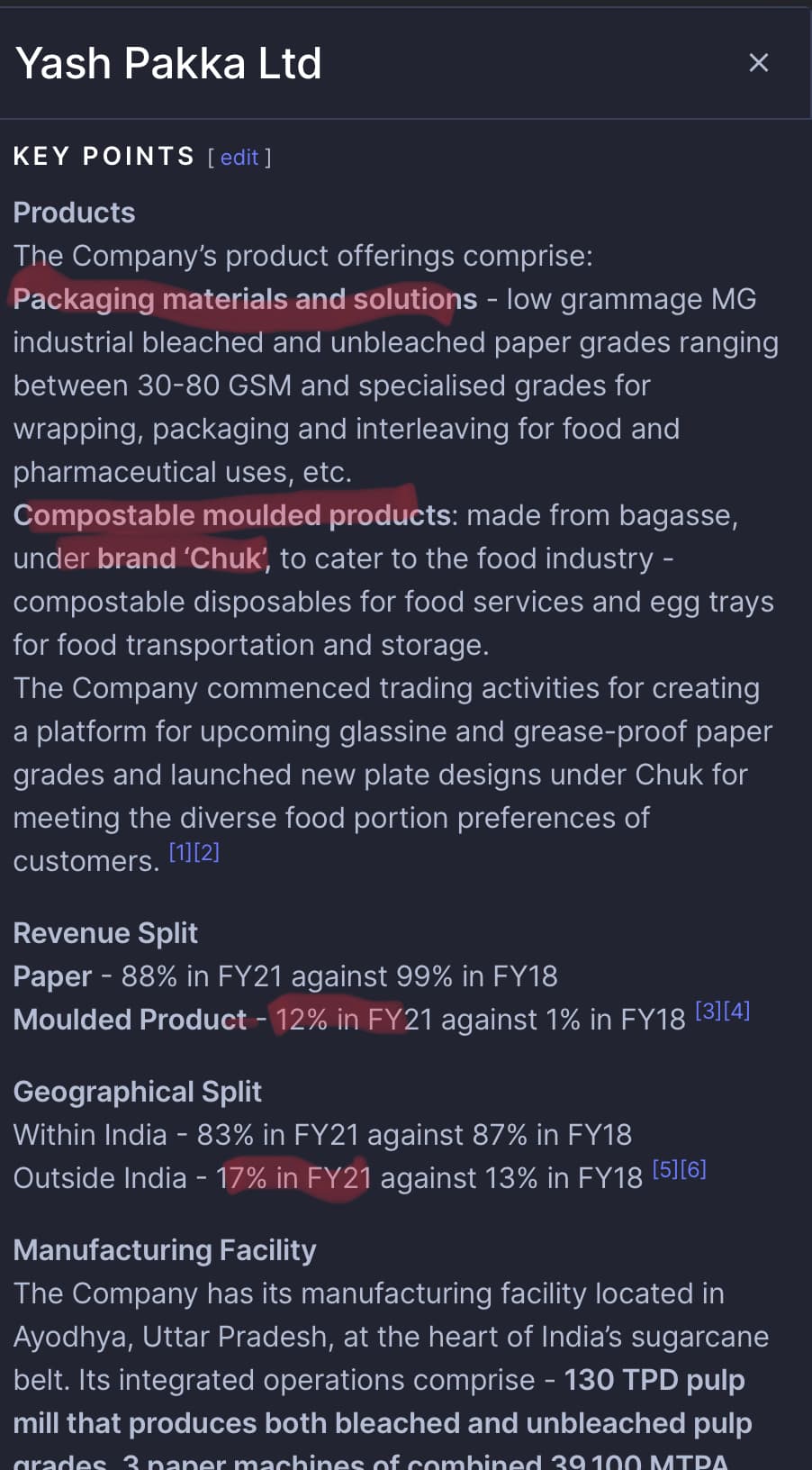

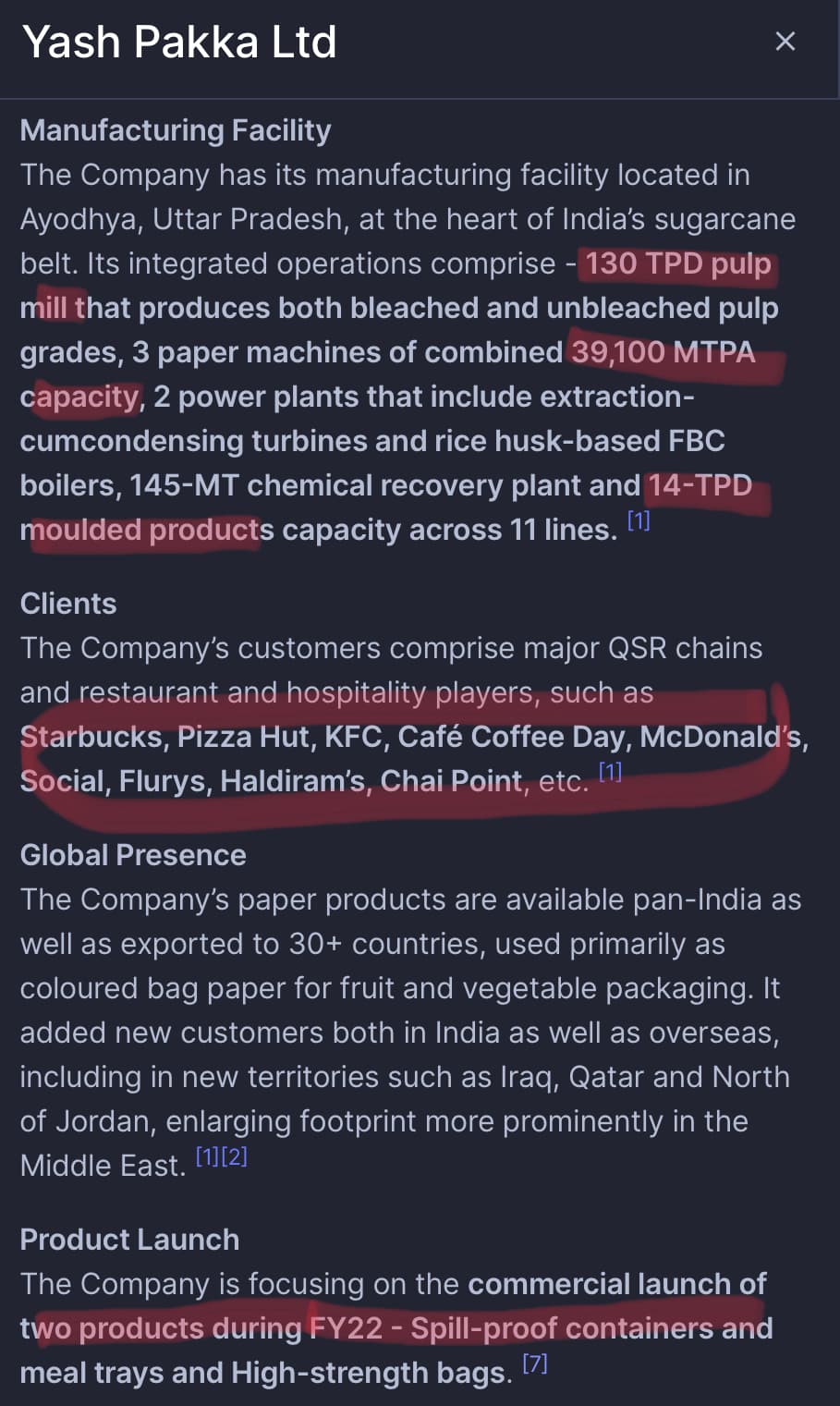

Our present: Our manufacturing facility is

located in Ayodhya, Uttar Pradesh, which is

at the heart of India’s sugarcane belt. Our

integrated operations comprise:

• 130-TPD pulp mill that produces both

bleached and unbleached pulp grades

• 3 paper machines of combined 39,100

MTPA capacity

• 2 power plants that include extraction-cumcondensing

turbines and rice husk-based

FBC boilers

• 145-MT chemical recovery plant

• 14-TPD moulded products capacity across 11 lines

Our paper portfolio: Our products are ubiquitous as they are used in everyday food and FMCG packaging. They comprise low grammage MG industrial bleached and unbleached paper grades ranging between 30-80 GSM. We also produce specialised grades for wrapping, packaging and

interleaving for food and pharmaceutical uses, etc.

Our export presence: Our paper products are available pan-India as well as exported to

30+ countries, used primarily as coloured bag paper for fruit and vegetable packaging.

Our moulded products: Moulded products under the “Chuk” brand are made from

bagasse, a fibre most suited to produce these lightweight products for ensuring ease

of handling, flexibility for protection against damage, and strength to prevent spillages.

The Chuk product range caters to the food industry and comprises compostable

disposables for food services and egg trays for food transportation and storage. Our

customers comprise major QSR chains and restaurant and hospitality players, such as

Starbucks, Pizza Hut, KFC, Café Coffee Day, McDonald’s, Social, Flurys, Haldiram’s, Chai

Point, etc.

Our long-term plans:

Focus on achieving

“Mission 2025” that envisages a turnover of Rs 13.6 bn and profit of Rs 2.4 bn.

There has been a significant shift in my role in the past year. I have now moved to a nonexecutive

position in the Indian operations and lead the global operations from the US.The idea there is to build towards stronger innovation collaborations and investments

in the compostable packaging space. We have established a 100% subsidiary in the

US and will begin to build towards global impact in the coming period.

I do remain involved as the strategic lead overall and we have various plans

to further strengthen our business. We are working on first strengthening the

financials and reducing leverage. We will then be looking towards further expanding

our manufacturing base and are scouting for opportunities for the same. We remain

focused on advancing our compostable products business and thus a strong

operating model is being evolved and implemented.

to during the year?

In 2020-21, while on the one side we

concentrated on the day-to-day, we also

focused on setting ourselves up for the

long-term. So, in a sense, we renewed our

strategy for accelerated growth and value

transformation.

We have chosen to focus our growth

initiatives in sustainable packaging, an area

where we have built leading market positions

and are driving frontline customer-centric

innovation. Thus, we are focusing on strong

and competitive asset creation to drive

accelerated growth. To strive further in

enhancing production capacity of paper and

compostable moulded products, we are:

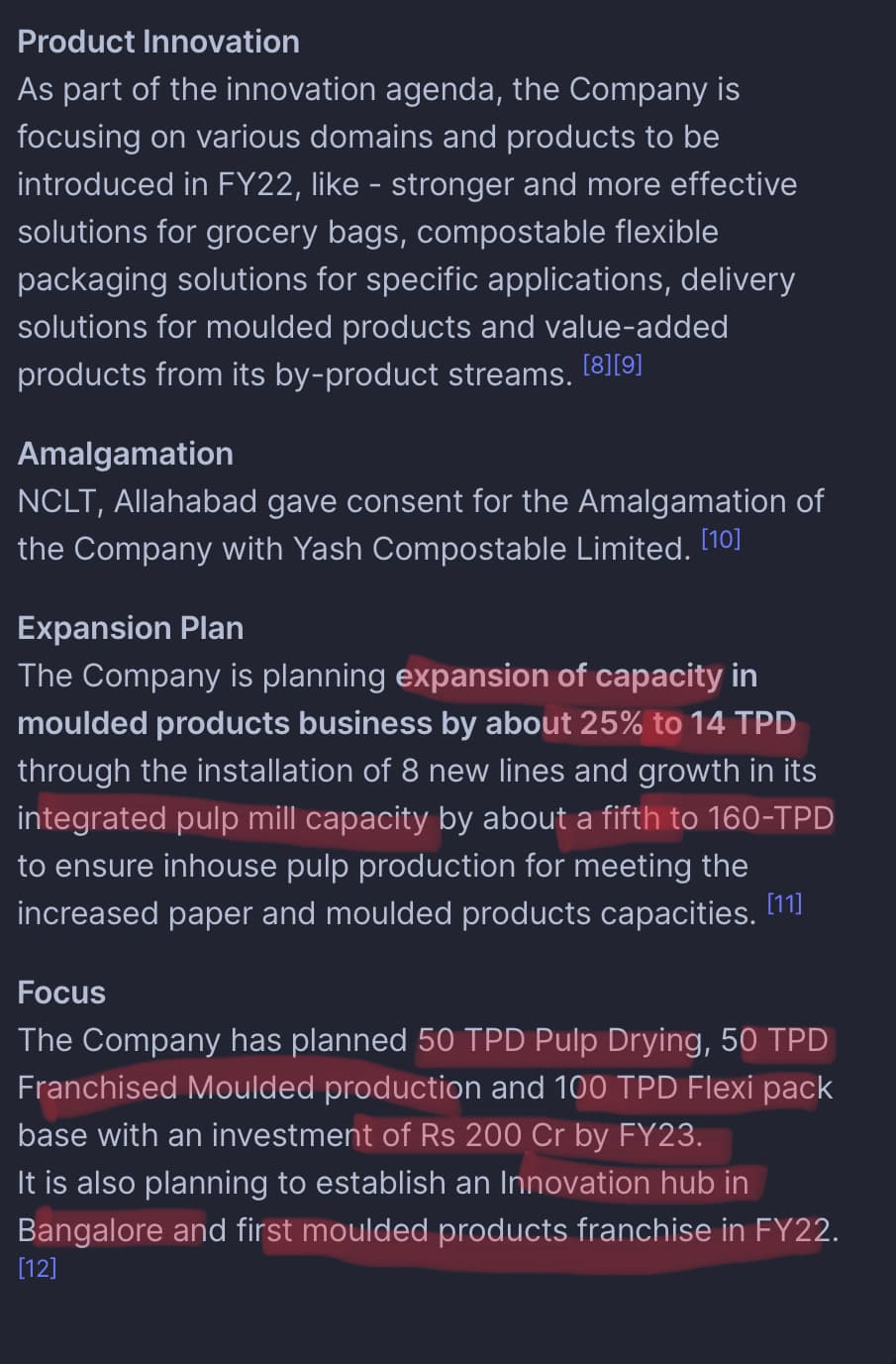

• Enhancing PM# 3 quality to ensure worldclass

paper with adequate high strength for

bag manufacturing for food packaging

• Expansion of capacity in our moulded

products business by about 25% to 14-TPD

through the installation of 8 new lines

• Growth in our integrated pulp mill capacity

by about a fifth to 160-TPD to ensure inhouse

pulp production for meeting the

increased paper and moulded products

capacities. Notably, our pulp mill capacity is

being expanded to a level that factors any

future inorganic growth opportunities in our

downstream products

• Co-generation enhancement to supplement

growth in production

Q. What prompted the expansion, especially

at this point of time?

Though this might appear as a countercyclical

investment today, the strategy was

seeded years ago. COVID-19 could have

derailed our plans, yet we decided to stay on

course precisely because of it, as the event

has accelerated demand for sustainable,

plastic-free and circular products. There

are huge concerns over plastic all over the

world. At least 22 countries have imposed

a complete ban on it. Paper on the other

hand is the most viable and effective solution

that can reduce fossil-based materials in

packaging. Our moulded products have

a similar identity as they are backyard

compostable and can easily go back to the

earth rather than ending up in landfill.

With the recent development at the domestic

level wherein the government has passed

legislation for enforcing ban on single-use

plastic, we see multifold demand in paper

for packaging where we already have an

entrenched presence through the highest

share of 50%+ in the domestic market. The

upcoming investment will only boost the

quality of our products to global standards

with agri residue as our key raw material.

Similarly, our compostable moulded products

will witness enormous demand, which will

be backed up by capacity enhancement

initiatives. Chuk is a brand widely known

for customer satisfaction and we are

further working to provide the full basket of

products as per customer expectations and

requirements.

Thus, there is a clear case building up

for our products and we are focused on

operationalising our new assets over the

medium-term.

Annual

What’s coming up for this year:

• Retrofitting PM#3 to improve paper quality

to manufacture specialised high-strength

bag paper

• Implementing advanced mill maintenance

practices to ensure best possible utilisation

• Identifying skill gaps and training to narrow

the gap and enhance productivity

• Maintain stock levels of less than 350 MT

• Enhancing export market share from 25%

to 35% (of total production) by augmenting

our global distribution network, especially

in untapped regions

• Building leading positions in glassine and

grease-proof paper, high-strength paper

bags for e-commerce, and paper for food

bags and wrapping

• Developing general and modern trade

channels and fortifying our presence in the

QSR segment

• Exploring an asset-light strategy in

moulded products manufacturing

3 Likes

Investor presentation…

Target set by the Company for 2025 are mind boggling …

Disclosure invested and 1% of my portfolio

2 Likes

Targets set are next to impossible to achieve. More concerning is the amount of debt company is taking compared to its size. If the projects didn’t work, company wouldn’t survive. Too risky right now.

3 Likes

Latest PPT:

The targets remains and the company mentioned in concall they will go for an asset light model.

1 Like

YASH PAKKA Q3 Concall Notes: Very Ambitious - CHUK de…….Let’s C……

Q3 Investor Presentation

- Refer Investor presentation for Team/New Business Heads and Quarter Nos. - Will end up with highest numbers Next quarter and FY22.

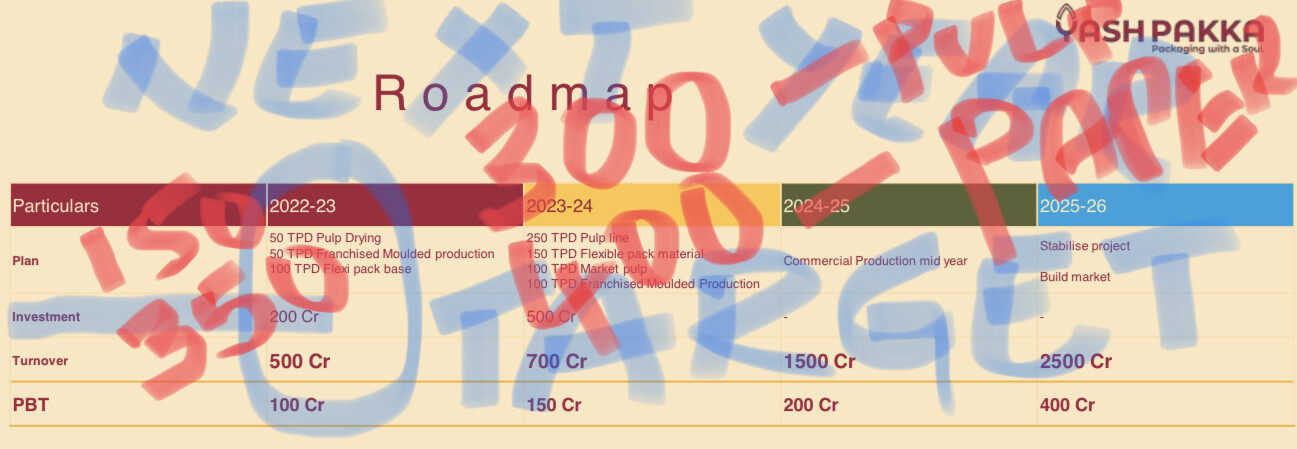

- FY 23 Sales break up Targets :

Pulp + moulded Products - 150Cr, Paper - 350 cr - FY 24 Sales break up Targets :

Pulp + moulded Products - 300Cr, Paper - 400 cr - Present Capacity Utilisation : Moulded - 58%, (Break even point is 65% for profits), Pulp+Paper-100%

- Strategy for Moulded Products - Franchisee route: For faster growth, Supply Pulp & Moulds, and buy back finished Moulded products, Started with first Franchisee-stabilising it, In this year to go with 3 Franchisee. Design with IP registration and Tool/mould will be owned by Company, No one can/should copy Design.

- Flexible Package - Different mix of products, looking at certain specific applications, MVP’s (minimum viable product ???) under trail, to go with minimum 100MTon/month and grow month on month, partnerships done, some technical success and outsourcing manufacturing with formulations, create the base paper(others paper now, later will be done with own paper), both food and non-food usage, done successfully sachets kind of products. Now doing food contact packaging. Very buoyant about this. Doing this with Global Companies, will share after success/confirmation.

- US Market -

- Moulded Products next year, set up franchise route, exploring Mexico with partners.

- Innovation partnership with US/EURO players, Flexible package (bio mimicry???) research/exploration with US base organisations

- Set up first Pulp Mill outside India with finance options, partnerships to set 200/250 TPD baggasse Pulp unit, 3 countries in exploration.

- Technological Platform for compostable package Industry with collaboration for investors/partners with revenue generating option.

- In Study stage for Revenues - High complex market, by March will decide/finalise Strategy.

- Appointed AFRY consultant for Market study

- Funding -

- 200cr - Debt + Equity with minimum dilution,

- Next cycle Capital (500cr/700Cr) raise explore with all options but won’t dilute at these valuations, will wait for market to recognise us and see.

-

Inventory : Very High - 1.5 years, RawMaterial Bagasse - seasonal procurement - Sep to Mar, so End of March always shows High Inventory. This is used for the next whole year. March 21 have some COVID impact. But Generally will have Baggase one year (10-12 months) inventory by March end to operate for the next year. Another Raw material Husk - Around 6months inventory - This is the nature of Business.

-

CHUK - From Investor - In Calcutta Seen Everywhere, Airports, QSR’s, In all Local Markets - why? Quality and Safety, Multiple key Accounts heads setup, regional heads, Larger institutions/QSR heads setup, Distribution/sales setup. Working this setup very well.

-

CHUK Competition : Zume, Ecoware. Price vs Utility - Zume is Higher and foreign brand, CHUK is Local brand, Premiumness, value, safety and affordable. Zume is premium product with Higher price point. Ecoware is great looking products, cheaper but CHUK beat handsomely in performance in Market. CHUK is priced between ZUME & Ecoware. Newer capacities are strategically placed to go wider and deeper. Next quarter planning - meals trays rolled out for delivery. Innovative products in lineup with customer feedback, safety, thinner and strong products in lineup based market wants/needs.

-

Future funding how?? - can see Sustainability/ESG funding is real and Huge Change happening. Company future plans/funding are still low in comparison with - Smaller US company - Footprint??? - Half of our size raised 1.6Billion USD. Funding should not be problem once we start delivering our promises. Once present 200cr expansion done, results/rewards are seen then lot of options to raise capital. Observation : Tone is confident this time.

-

Startup setup Culture is been followed in the organisation.

-

Current Debt including working capital - 80Cr, majority of this taken for Tableware Project from 2018, will be repaid in future, on the path to streamline our debt portfolio.

-

CHUK capacities- Present 14TPD, Planning to go 50TPD to 100TDP by Franchise root.

-

CHUK - Key is Scale and Size ( Decided to go by Franchise root), Our focus is investing/growing in Pulping.

-

Will Produce only very very High grade Paper above 150Rs/kg for Packaging.

-

Going with Apple Business Model, OEM model also being exploring. Idea to do at scale and size not small boutique route.

-

CHUK Challenges - Only around 8Cr per Quarter after 3 years ?? Machine Setup/Capacity Utilisation/Market Challenges with COVID. Over come all. Capacity utilisation to be 80% next 2 quarters.

-

CHUK partnered with Blinket in this Quarter, and in Talks with Zomota for potential Partnerships with Restaurants. Very buoyant in this space.

Yash Pakka’s CHUK brand enters partnership with Blinkit | PrintWeekIndia -

CHUK - From Investor - Seen everywhere, not only in QSR, even in Dhabas.

-

Sponsoring a conference in LONDON - For Rethinking Materials, to build Global think tank. Biology and Technology/ Global Compostable Packaging ………….

-

ESOPs/Equity - new Scheme is TeamSOPs in planning for the Team.

-

Raw Material Availability/Pricing for Bagasse- Power companies in plan to produce Ethonal/Power ??? - Have strong Longterm Relationship with near by Sugar Mills and exploring new partnerships. Bagasse won’t be converted into Ethonal, is only used as fuel to produce Ethonal, presently not big challenge. Stay competitive for procurement.

-

IRCTC - Not much supply now, complex structure, but open/exploring for major supply once IRCTC in full running.

-

Might have missed some points - So Take with some sugar and Salt.

From Screener.in

From Q3 Investor Presntation:

From above Interview:

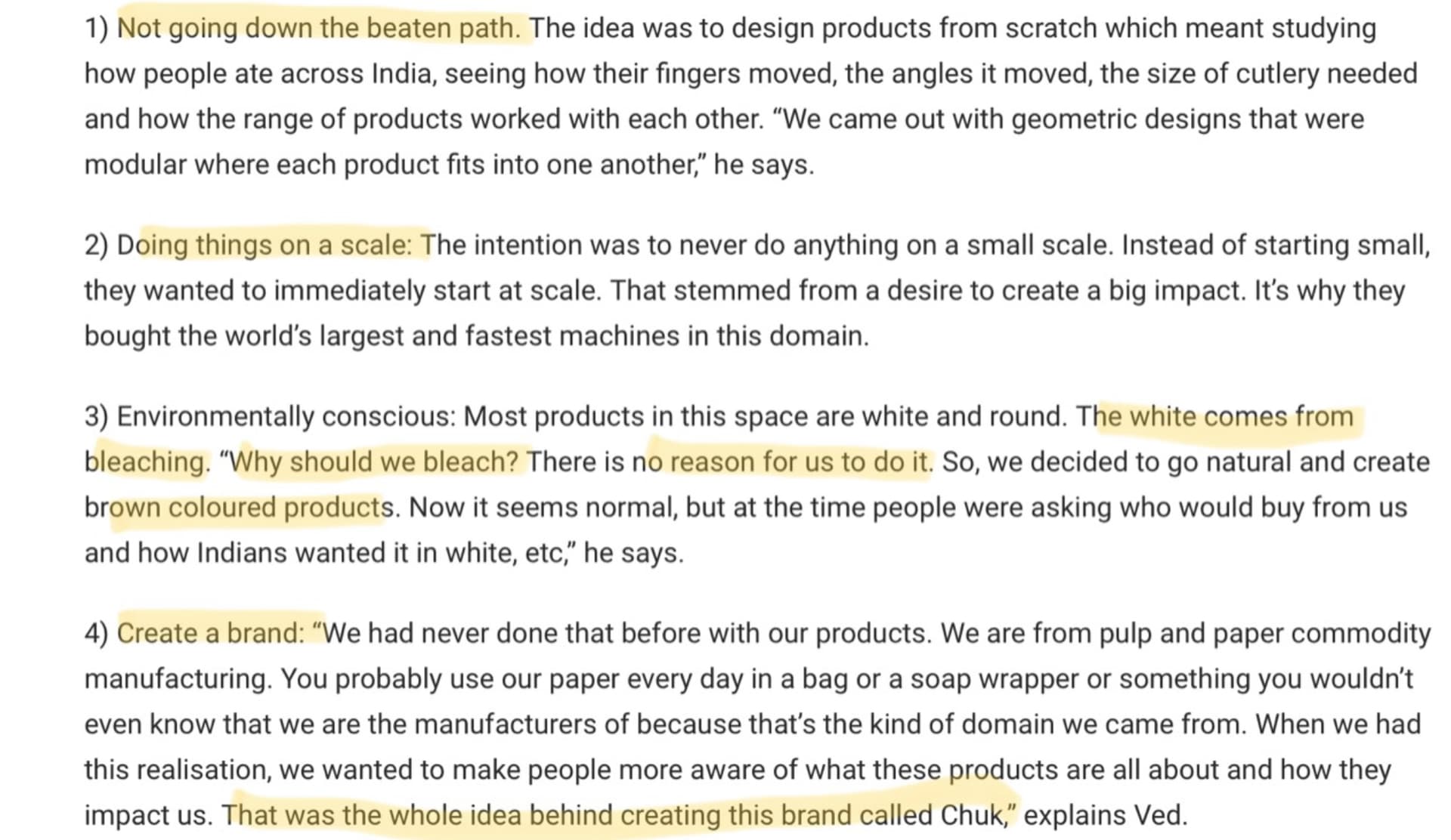

How CHUK was created:

Refer Satia Industries thread for Paper Industry and Tailwinds:

Risks:

Disclosure - Invested, Transactions in Last 15 days.

Not SEBI Registered. Read/Understand/Invest at your own Risk.

11 Likes