The below post is a copy paste from @phreakv6 original post on the above link:

Before I proceed, credit where its due - This idea originated with @Anant whose inputs prodded me to look deeper into this story and @Sanjay_Kumar_E who is the nuts and bolts man whose ability to wade in deeper than the rest regardless of industry is simply unparalleled. I am simply piecing together everything in a way I can explain to my 10 year old son.

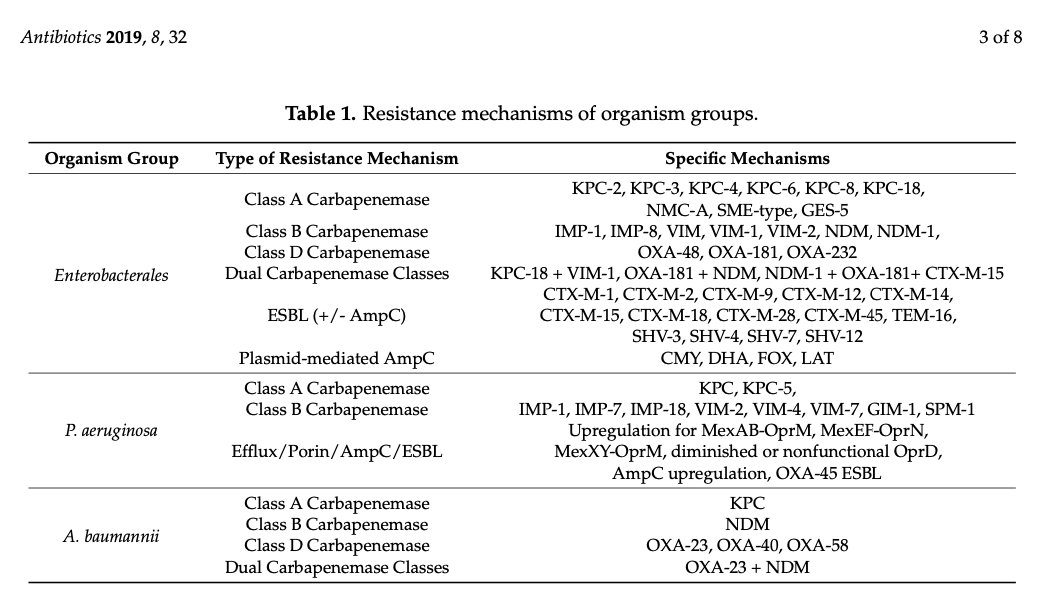

Understanding Antibiotics

I usually avoid stocks with large pledging (I assume fraud), stay away from businesses that are complex to understand (complexity needn’t be in comprehension of the business but the dynamism of its moving parts as well) and ignore turnarounds. This one has got all these in troves so should be a strong avoid, yet here I am, ready to make a fool of myself.

The following is my understanding of things - it is aimed at people like me with no prior medical background and is written in layman language to develop an intuition as to how things work.

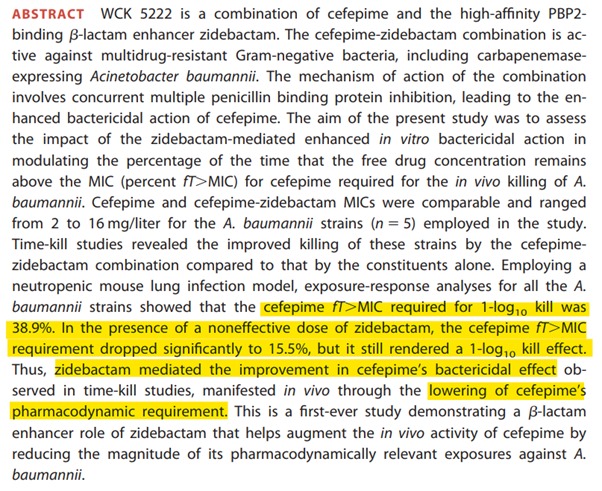

To understand WCK 5222, it is important to have a lot of pre-requisites. It is probably these pre-requisites that are keeping people out.

Antibiotics are class of compounds that are used to treat bacterial infections. All of us have had one at some point of time. Azithromycin is probably the most common we would have been prescribed at some point. Most of us have heard of Penicillin which is the first antibiotic discovered by Fleming in 1928, by accident and developed into practical antibiotic much later in 1940s. Since then it has revolutionised medicine right from its use in WW-II.

Antibiotics typically work by killing (bactericidal) or impeding growth (bacteriostatic). They do this by compromising integrity of cell wall or messing with the processes within the cell.

Since penicillin, we have discovered several classes and numerous antibiotics that work against various types of bacteria. Important thing to understand is that, as our antibiotics are evolving, so are the bacteria themselves as drug resistant varieties proliferate, needing newer antibiotics

A lot of names get thrown around and its easy to get lost in names of antibiotics. It is always easier for our brains to view things in categories based on some attributes.

| Class | Examples | How they work? |

|---|---|---|

| Penicillins | Penicillin, Amocixillin, Ampicillin | Interferes with cell wall synthesis |

| Cephalosporins | Cephalexin, Ceftriaxone | Disrupts cell wall formation |

| Macrolides | Erythromycin, Clarithromycin, Azithromycin | Inhibits protein synthesis |

| Fluoroquinolones | Ciprofloxacin, Levofloxacin, Moxifloxacin | Inhibits DNA replication |

| Tetracyclines | Tetracycline, Doxycycline | Interferes with protein synthesis |

| Carbapenems | Imipenem, Meropenem | Inhibits cellwall synthesis in MDR (multi-drug resistant) bacteria. Most potent class |

There are others like Sulfonamides, Aminoglycosides, Glycopeptides, so this is not an exhaustive list.

Few things to understand before we proceed further

In Vitro vs In Vivo

In vitro experiments are conducted outside a living organism, typically in a lab, with lab equipment (petri dishes and test tubes) while In vivo are studies conducted with living organisms (rats, mice). Important thing to understand is that even if an experiment is successful In Vitro, it could fail In Vivo, for various reasons.

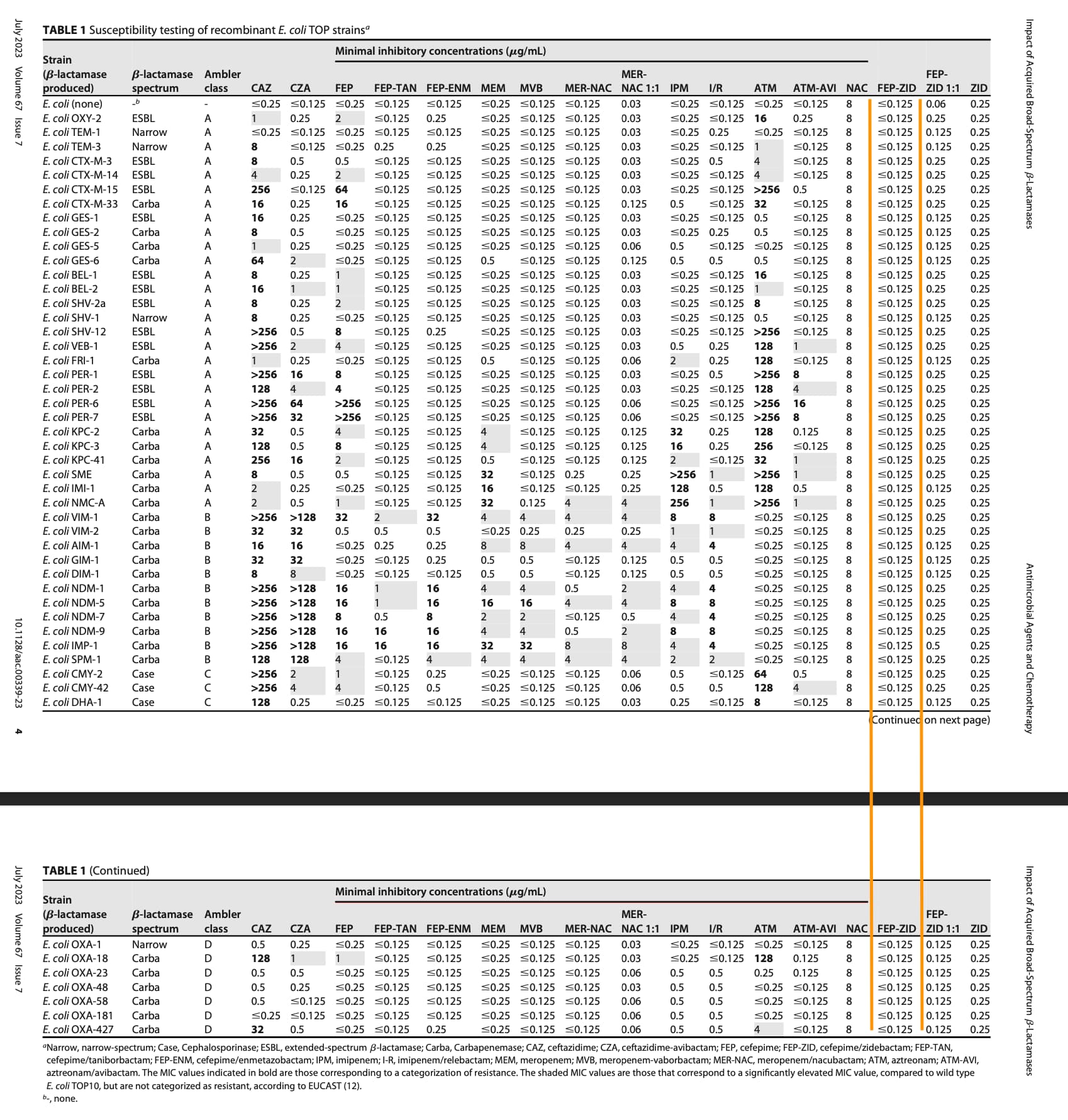

MIC

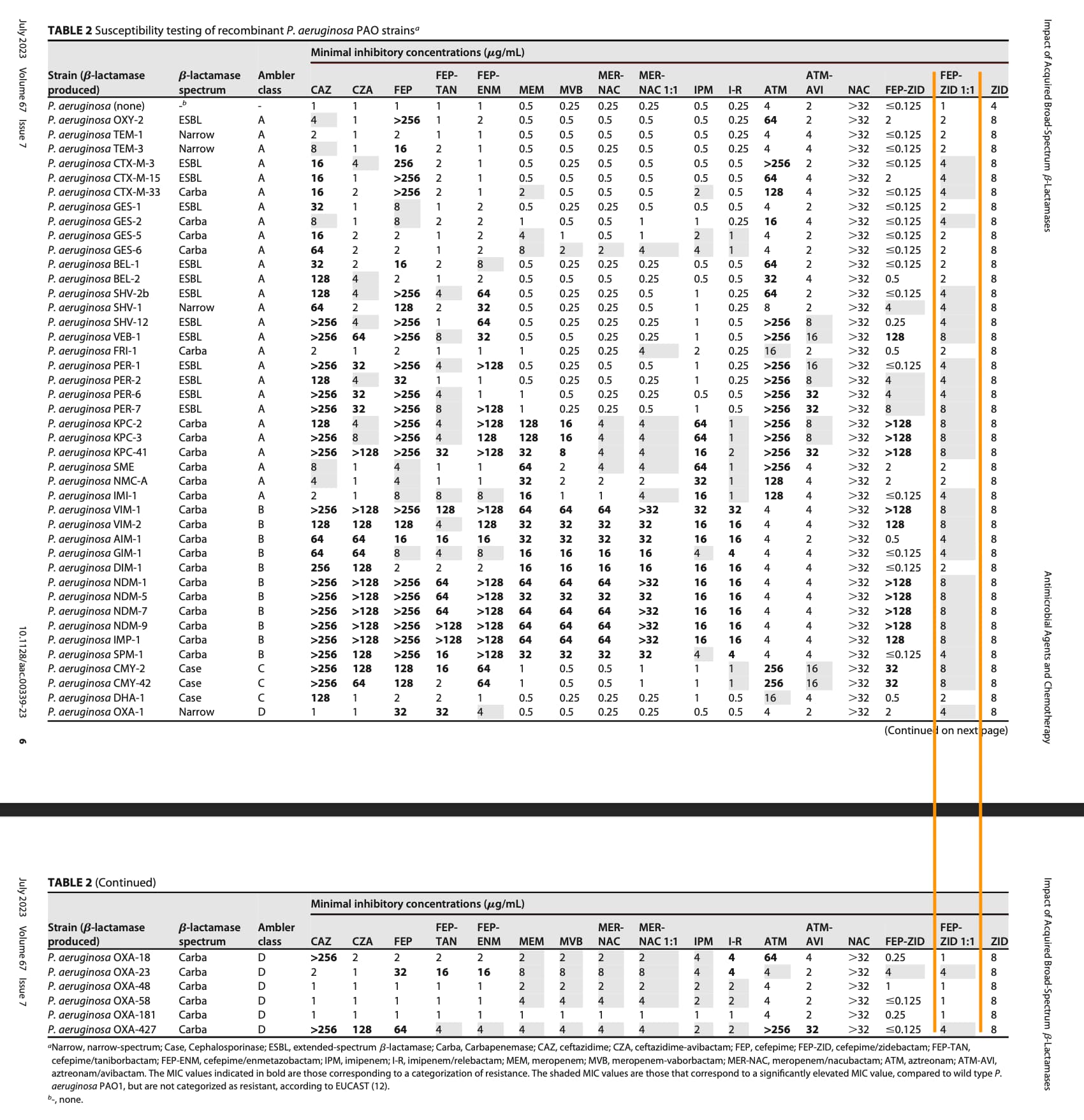

MIC stands for ‘Minimum Inhibitory Concentration’. It is the lowest concentration of the drug that inhibits growth of a given strain of bacteria, typically expressed in micrograms/milliliter (μg/mL). Needless to say, this varies a lot between drugs and strains of bacteria and there are standard ways of representation of a AST (Antibiotic susceptibility testing).

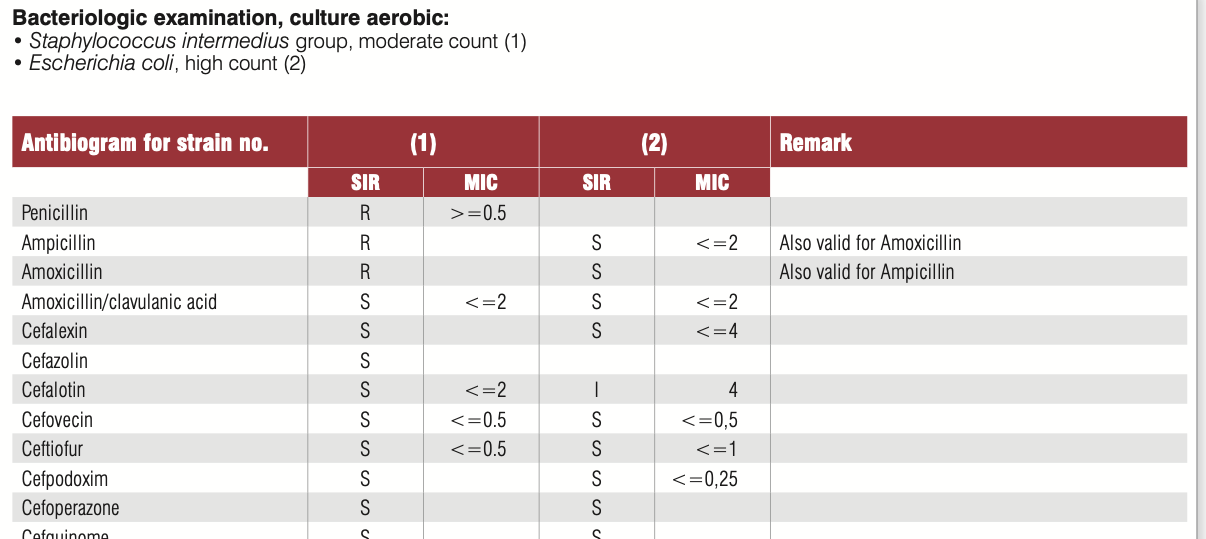

A typical AST result looks like this.

In this, the SIR column is one of S/I/R which is Susceptible (Bacteria is susceptible to the dosage), Intermediate (May be effective at higher dosage) and Resistant (Drug not effective). MIC values usually have a ≤ sign when organism is susceptible. The above tables has two specimens (1) and (2) and have. SIR and MIC for the these two specimens against various antibiotics. Penicillin is not effective against (1) while Cefalotin is effective at a MIC of 2 μg/mL.

You will also notice that several different antibiotics can be effective against a microorganism. How does one choose which one to use? is the next natural question that arises

PK/PD

Just because a drug is effective In-vitro doesn’t mean it will be In-vivo. The reasons can be many but fall into these two categories Phamacokinetics (PK) and Pharmacodynamics (PD). In layman language - PK is what the body does to the drug and PD is what the drug does to the organism.

So Pharmacokinetics (PK) is the kinetics of drug absorption, distribution from where its administered, Metabolism within the body (how its used up) and Excretion (How its removed). As you can see, all these will in turn affect how much of the drug is available in the tissue or plasma to come close to the In vitro experiment if it was in fact successful

Pharmacodynamics (PD) deals with antimicrobial activity that is desirable (inhibition or killing) and undesirable (adverse effects to the host). We cannot keep increasing the concentrations of the drug if it is adverse to the host or worse, it helps to develop resistance in the microorganism thereby making it useless.

Breakpoints

This segues us nicely into the concept of “Breakpoints”

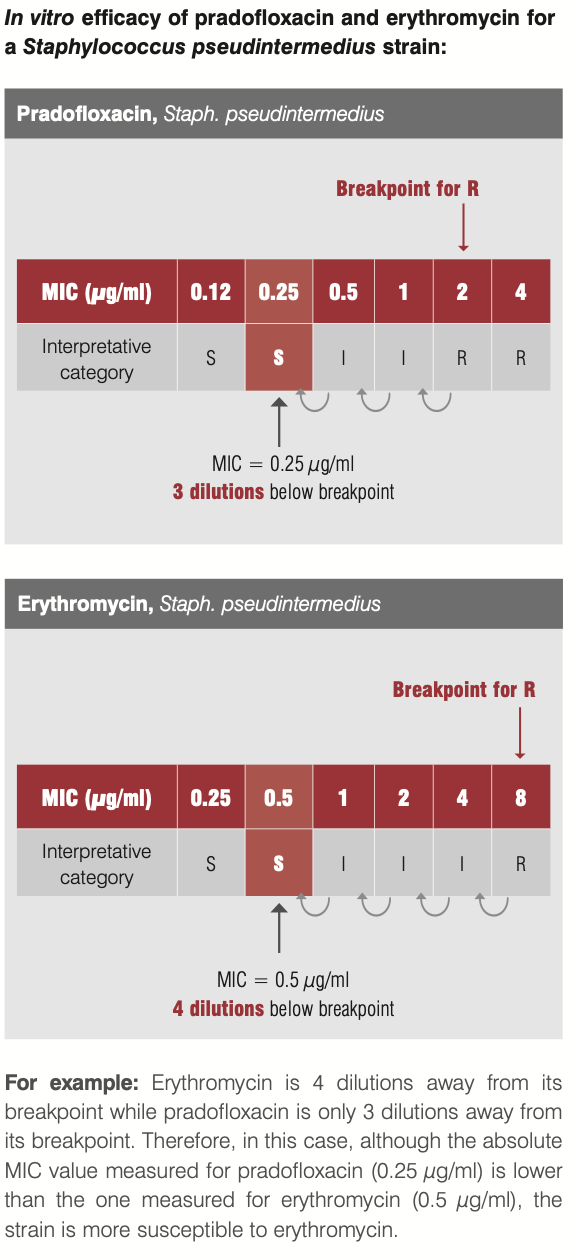

To get back to the question of which antibiotic to use when bacteria is showing sensitivity to multiple antibiotics, our intuition should tell us that lower the MIC, the better it might be. Our intuition couldn’t be more wrong.

Take this eg. of efficacy of pradofoxacin and erythromycin against staph infection. Though our intuition may tell us Pradofloxacin at MIC of 0.25 should be better than Erythromycin at 0.5, it is the latter that is a better drug since its 4 dilutions away from the breakpoint where the organism starts developing resistance to the drug.

But who sets these breakpoints? These are internationally governed by bodies like CLSI (Clinical and Lab Standards Institute), EUCAST, FDA. These get reviewed periodically based on scientifically available evidence.

If a drug can work at much lower dilutions away from breakpoint, it might be preferred - all else remaining equal

So hopefully that helps to develop the intuition between In Vitro and In Vivo

MDR/XDR

MDR and XDR stand for Multi-drug resistant and Extremely drug-resistant. You would have noticed in the Antibiotics table that Carbapenems are used in XDR cases where all else fails

Pharmacodynamics

Re-visiting this again separately, since this is important to understand further. So we know that drug is effective at MIC and above but below breakpoint. But it doesn’t tell us for how long and how much higher it needs to stay to be effective.

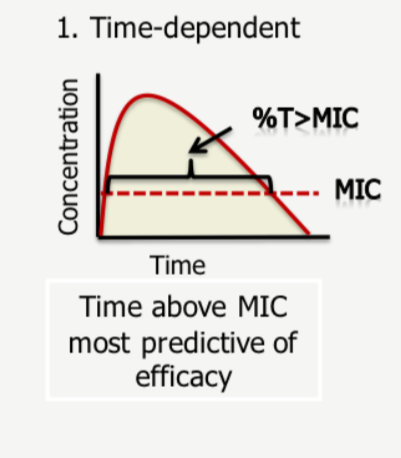

Based on In Vitro experiments, the effect of the drug on the microorganisms are classified as time-dependent or concentration-dependent or AUC dependent.

Time-dependent bactericidal effect

The drug needs to stay above MIC for a certain amount for time (dosing interval) for it to be effective. Typically drugs that interfere with cell-wall of the bacteria (penicillins, carbapenems) need to stay above MIC for a period of time.

So the percentage of time the drug spends above the MIC value is crucial here.

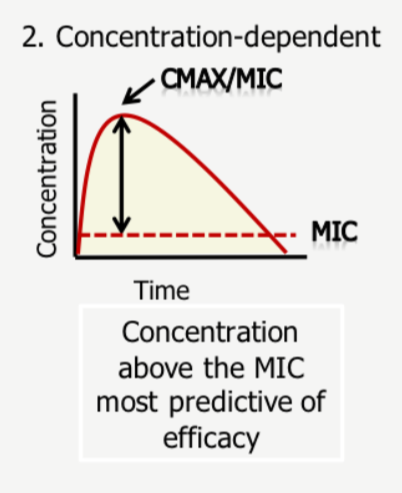

Concentration-dependent bactericidal effect

Max MIC or CMAX is the most-important predictor of success here. So achieving max safe concentrations at the site of infection is crucial

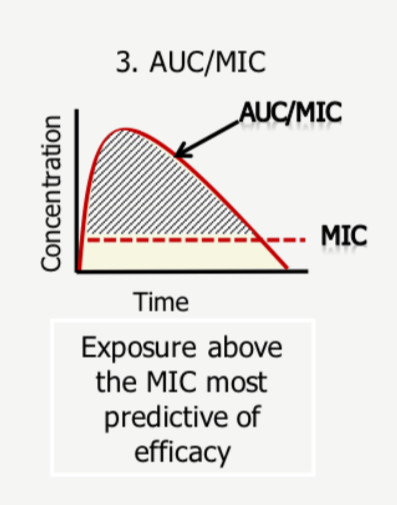

AUC/MIC

This is a combination of time-dependent and concentration-dependent as it requires a cumulative exposure of certain concentration over a period of time

AUC simply stands for Area under curve - so efficacy depends on maximising this area - its intuitive to understand here that if CMAX or T% is low, this treatment becomes ineffective - so both needs to be maximised to maximise the area under curve.

When CLSI sets breakpoints, it goes by this information from the reports - what it specifically looks for to set a susceptible breakpoint is a the highest MIC achieved for efficacy in 90% of patient population

There are more nuances here in terms of MIC and %T which we can get into at a later point but for now this should suffice.

The effectiveness of the drug on the bacteria is measured through base-10 log notations. So 1 log would be a 10^1 reduction and 2-log would be 10^2 reduction and so on in orders of magnitude. So in a colony of 1 million microbes, 1-log would achieve a 90% kill, 2-log a 99% kill and 5-log a 99.999% kill and so on. FDA is happy with a 1-log kill (90% reduction) to approve a drug.

This much is of course is table-stakes to understand papers on WCK-5222 - in terms of chances of approval, in terms of market size and so on (if it can replace existing drugs, market size will be bigger). I will try to summarise the rest in another post or two next week, if time and interest permits.

References:

microbiology-guide-interpreting-mic.pdf (235.1 KB)

Understanding Pharmacokinetics (PK) and Pharmacodynamics (PD).pdf (437.6 KB)

Disc: Invested (This is just an academic exercise at understanding antibiotics and then on to WCK 5222 and hopefully inspire others to pursue this. This could be a very high-risk bet, so please don’t go by fancy jargon in this post to plonk your money. Effort required to understand doesn’t translate to returns, and in fact could be inversely correlated)