Assumptions in DCF are important and there should be a reasoning behind each of them instead of random numbers. Otherwise, Garbage in = Garbage out.

-

Royalty - Orchid will get 6-8% royalty from Allecra for Enmetazobactam because they sold the drug when it was in pre-clinical stage. Wockhardt will sell WCK-5222 either post Phase 3 trials or after NDA application/approval. So they can get 15-20%.

-

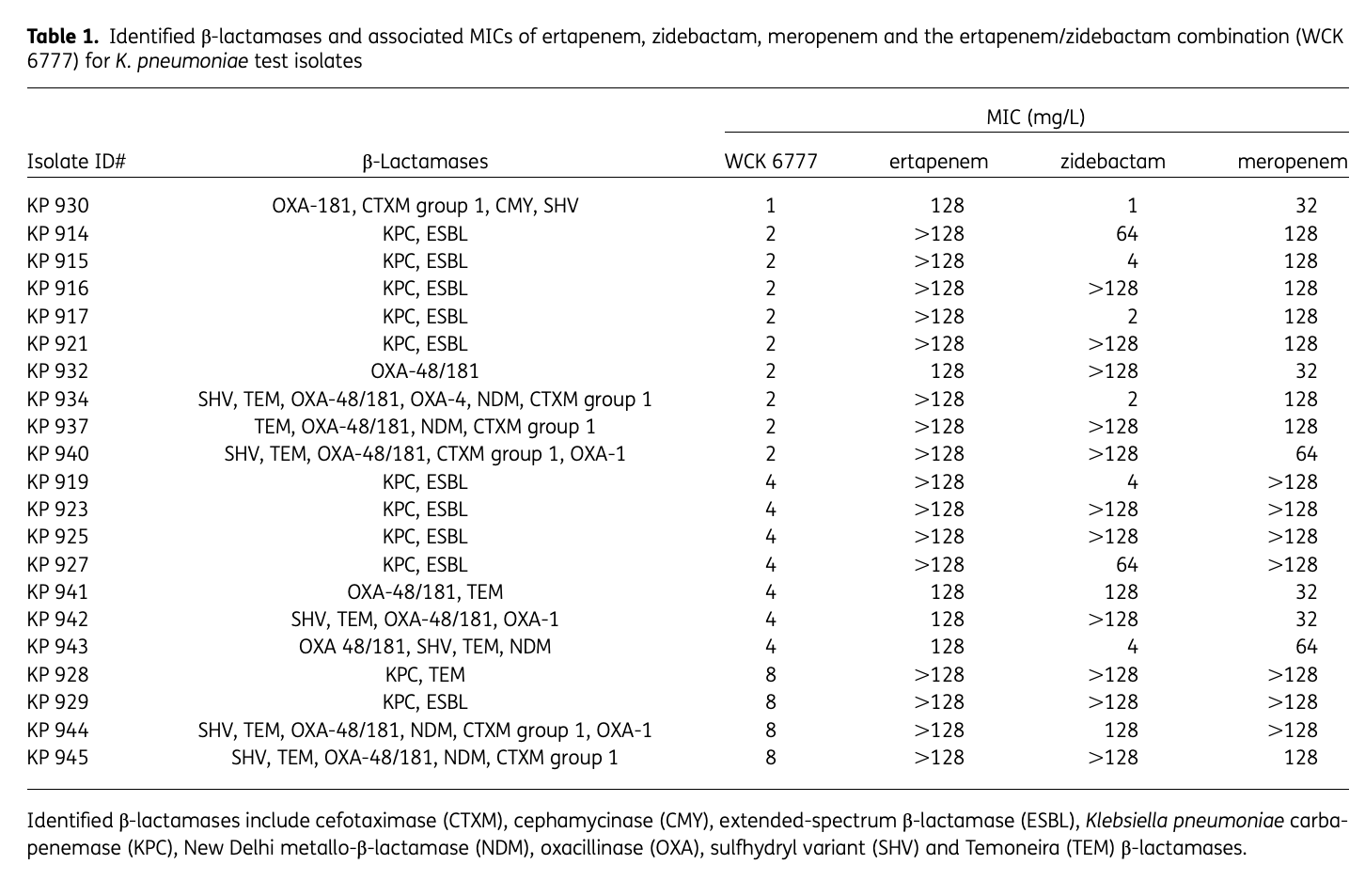

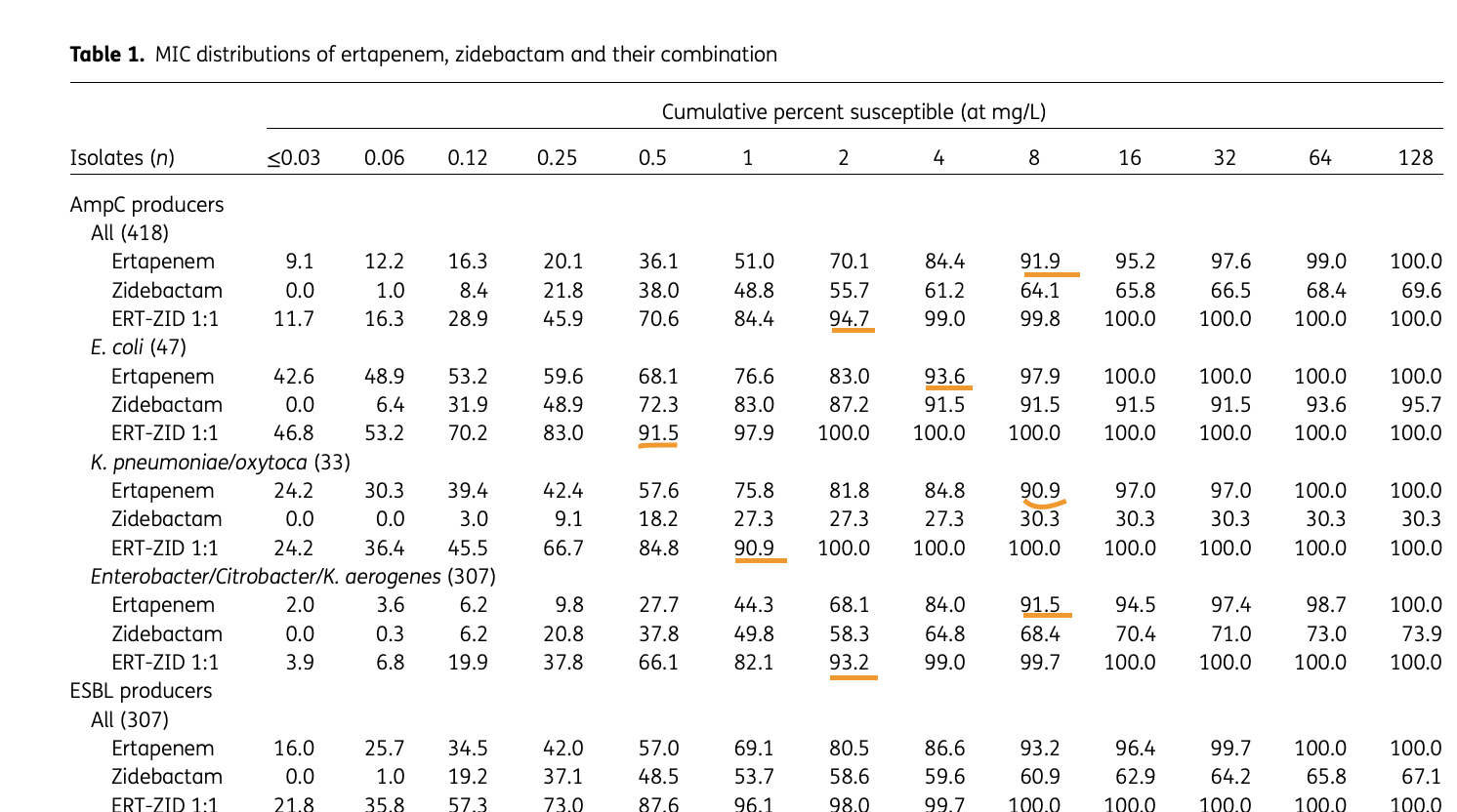

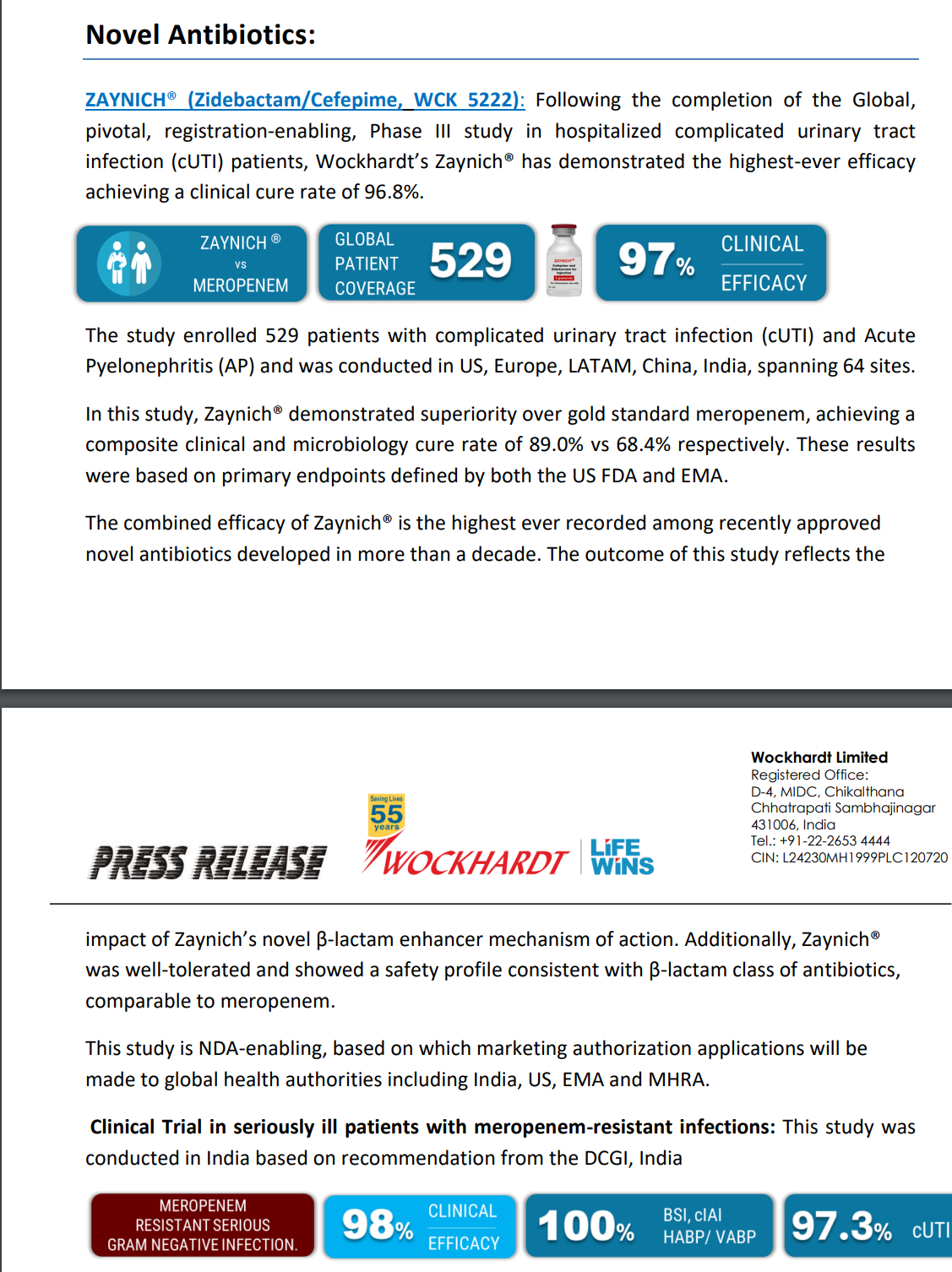

Peak sales - Avibactam (Zavicefta in EU and Avycaz in US) with 1/3rd the spectrum coverage of WCK-5222 is doing $800 Mn - $1 Bn and is still growing despite losing exclusivity. So WCK-5222’s market can be 3x of Avibactam and hence $2.4 - $3 Bn is a reasonable estimate. Avibactam is effective against only Enterobacterales whereas WCK 5222 is effective against all 3 - Enterobacterales, Pseudomonas and Acinetobacter. Double clicking on the $3 Bn figure, WCK 5222 can probably do $1Bn each in US, EU and China/ROW.

(Please note that Zavicefta did ~100% growth in 2 consecutive years. We will be using this assumption.)

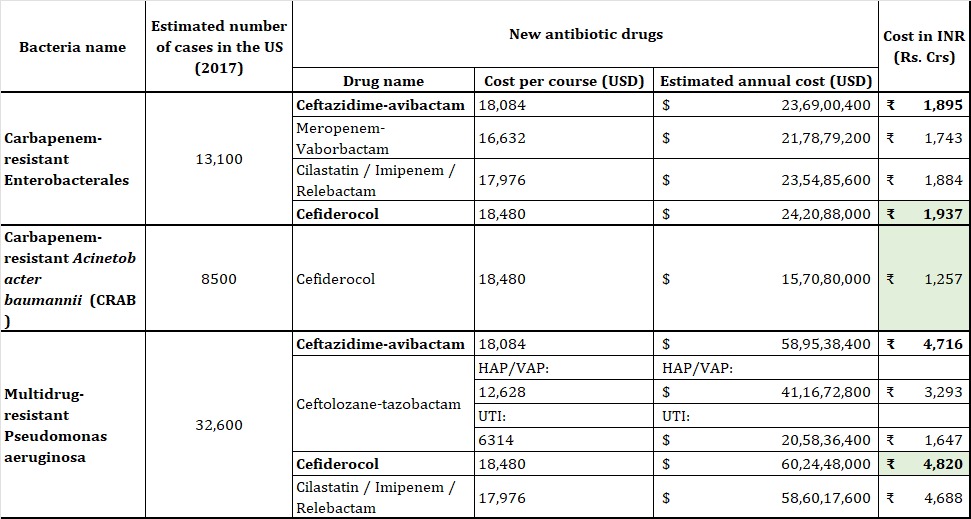

If you interested, can go through this paper on US which estimates the cost of antibiotics:

The cost is around $1 Bn for US based 2017 numbers:

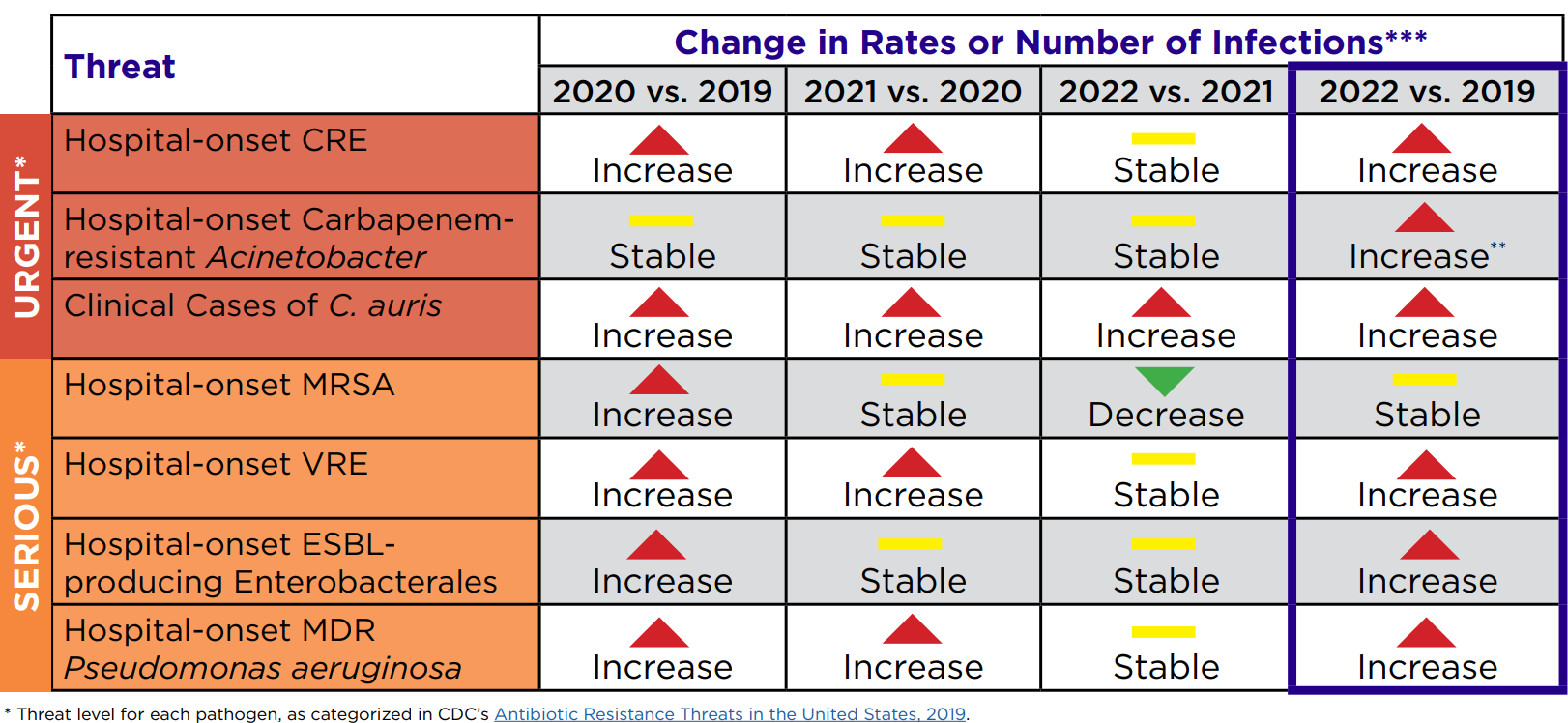

We know from CDC report that antimicrobial resistance has only gone up post Covid:

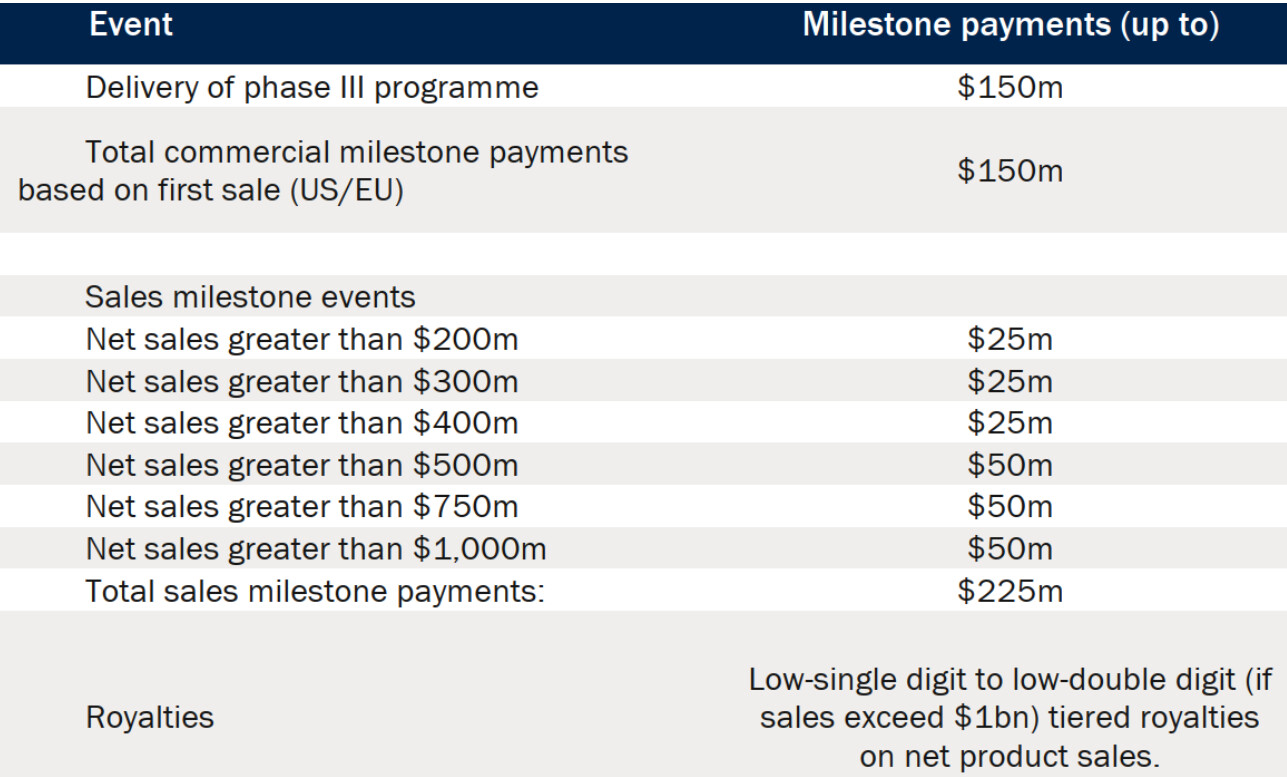

- Upfront / milestone payment - An industry professional told me that usually Big Pharma companies pay 20-25% of the peak sales potential as upfront payment. It will either be in one shot or based on milestones - both regulatory and sales based.

For example:

In September’22, GSK entered into an exclusive licensing agreement with Spero Therapeutics to

commercialise Tebipenem HBr in all regions except certain Asian countries. Tebipenem HBr is an oral

carbapenem antibiotic which was indicated for complicated urinary tract infections (cUTI) and had been

given QIDP and fast track designations by the USFDA.

Spero received an upfront payment of $66m and would have received $300 Mn milestone payments and $225 Mn sales based payment.

Plus Royalties if sales exceed $1bn.

(Note - this drug failed Phase 3)

Given the peak sales for WCK-5222 can be anywhere from $2Bn to $3Bn, the upfront/milestone payments that Wockhardt will get can be $400 Mn to $750 Mn. Plus Royalty.

-

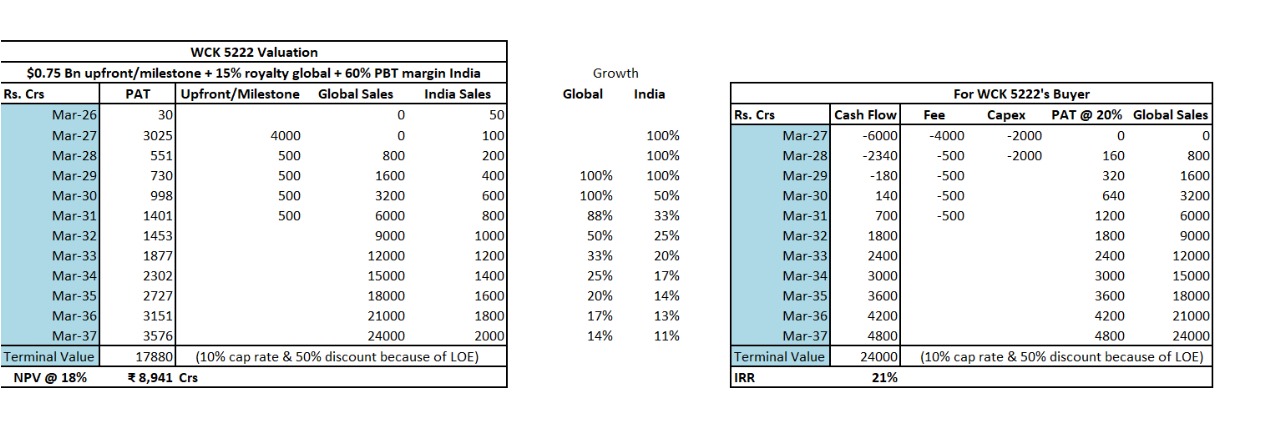

Dr. Habil had indicated in media interviews that Wockhardt will retain India market for themselves and out license the other markets. So Wockhardt will sell WCK-5222 directly in India. NCE is very high margin - 80-85% Gross and 65-70% EBITDA margin. I am assuming 60% PBT margin on India sales of WCK 5222. (Not getting into details of India market size as we will have to talk about number of ICU cases etc)

-

Terminal Value - As Bharani pointed out, Carbapenem market is $4 Bn but if you take just take Meropenem, which is the comparator drug in WCK-5222’s phase 3, is doing $1 Bn in sales. Despite going off patent many many years ago. I think WCK 5222 will go off patent by 2037 and I am reducing the peak cash flow by 50% and capping it at 10% to arrive at terminal value.

-

We can’t just look at Wockhardt’s perspective. We will also have to see if the buyer will make money.

Assuming 4000 Crs capex (very aggressive estimate, can even be half), 6000 Crs ($750 Mn) as upfront & milestone payment and 15% royalty to Wockhardt. Buyer, at 20% PAT margin, will get ~20% IRR.

NPV of WCK 5222 comes out to around ~9000 Crs. Shaving off 1000 Crs for my bias, WCK 5222 is worth 8000 Crs today. Roughly $1 Bn.

Wockhardt is trading at 12,000 Crs M Cap which means the base business is being valued at 4000 Crs.

Based on a discount rate of 18%. So WCK-5222 alone can double the stock every 4 years?

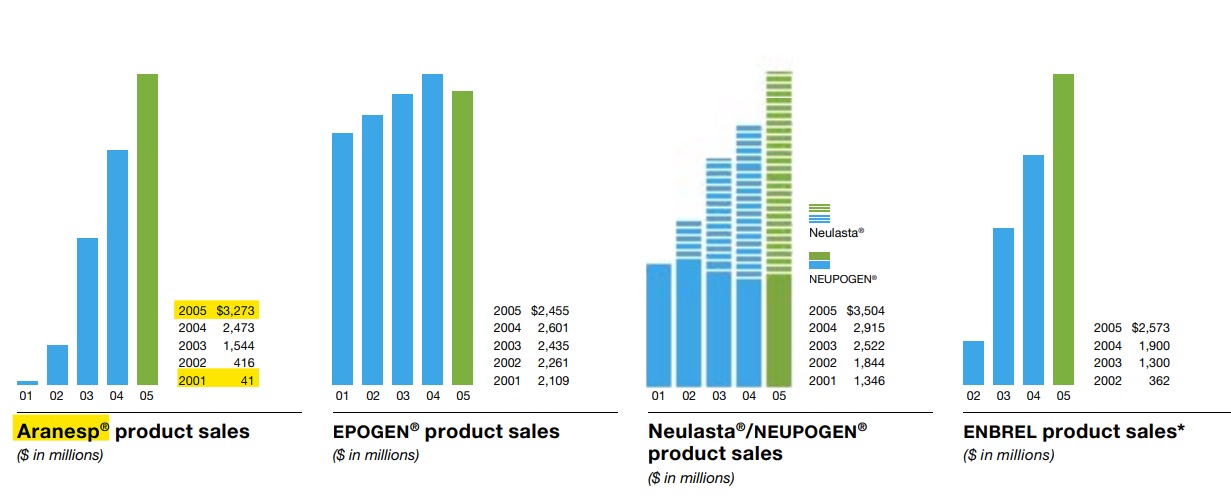

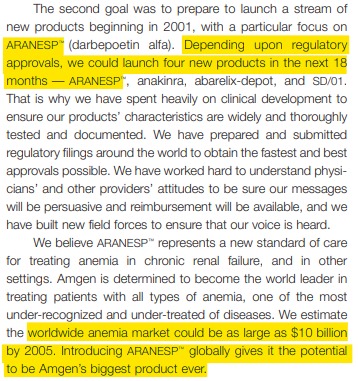

Also, you might question the growth rates assumed. Is it possible? We have already seen Zavicefta doubling for 2 straight years. Has it happened before? My friend @Ahmed_Madha pointed me to Amgen’s wonder drug Aranesp.

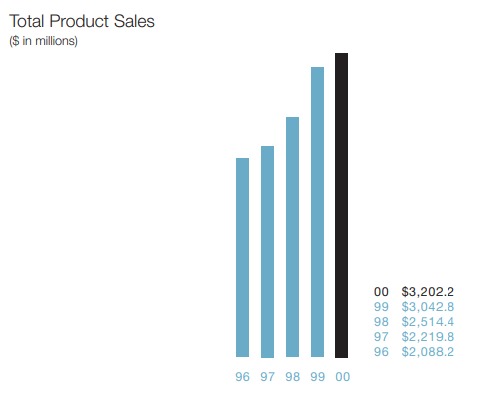

Amgen did $3 Bn Sales in 2000:

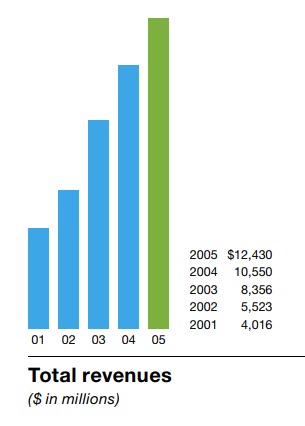

5 years later, the Sales had quadrupled to $12 Bn:

$3 Bn came from Aranesp - a drug for treating Anemia (kidney and cancer):

Of the $10 Bn anemia market, Aranesp has managed to capture $3 Bn:

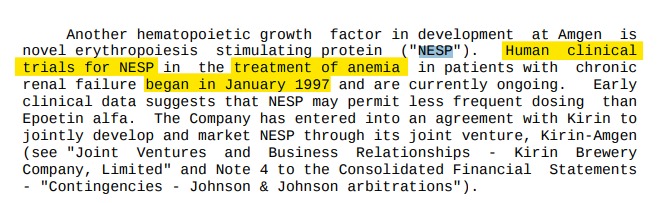

The clinical trials started in 1997. The marketing started in 2001:

Stock price move happened in between:

$20 to $80 even before the marketing of the product started!

By the way, Aranesp is still doing $1.5 Bn in sales. (Terminal Value!)

Risks:

-

Phase-3 success but we have evidence to suggest it can be successful.

-

Loss of exclusivity / patent expiry earlier than expected if US FDA approves any ANDA/FTF/505b(2) which I don’t have enough clarity on.

-

Biggest risk in my opinion is what Wockhardt will do with 15,000-20,000 Crs cash flows that they will generate in the next 10 years.

Buying at current price is being naive. Not when market was giving zero value to WCK 5222.